I must admit, Joe Biden has a horribly misleading nickname “Middle Class Joe.” Between Biden’s horrible energy policies and Pelosi’s/Schumer’s spending binges, the US middle class and low wage workers have suffered mightely with the inflation tax. Throw in Jerome Powell and The Federal Reserve’s manic money printing and the American middle class has a problem.

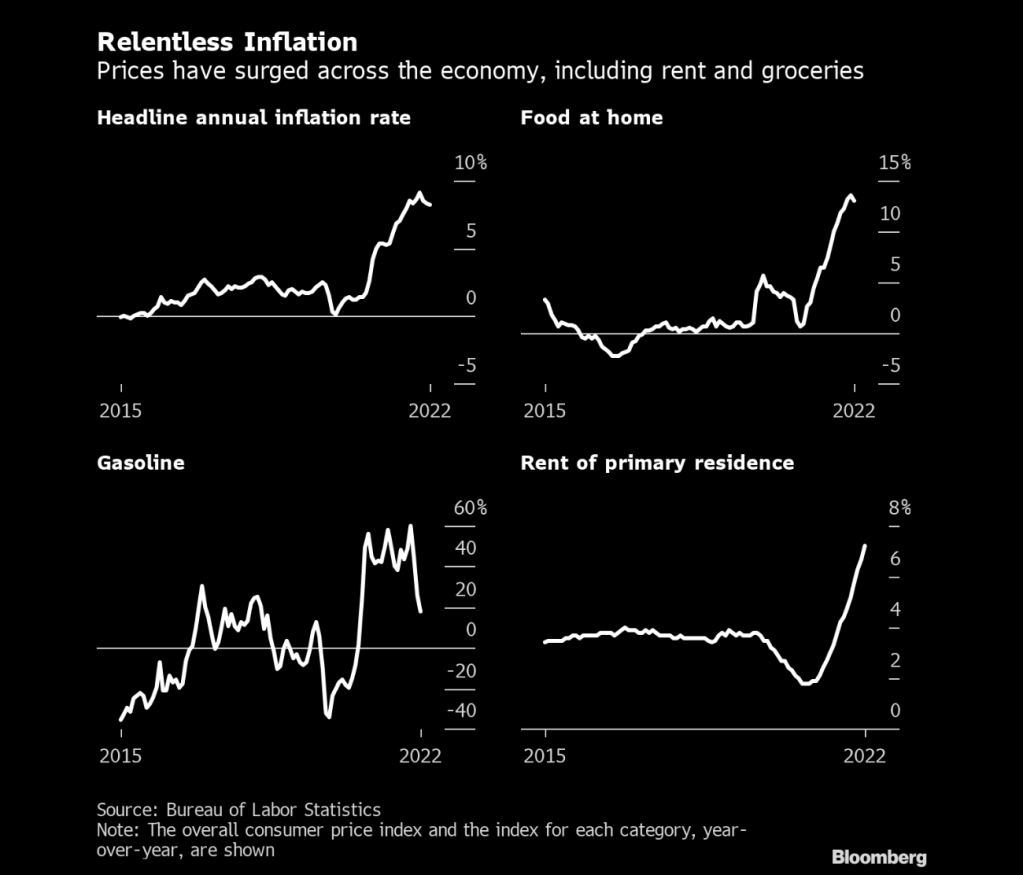

US inflation peaked at 9.1% year-over-year (YoY), but has declined to a still painful 7.1% YoY as The Fed removes it aggressive monetary stimulus. But to cope with persistent US inflation, consumers have had to dip into savings and use more credit cards. As a consequence, personal savings plunged -64.8% YoY while consumer credit rose 7.9% YoY.

The other tax on the middle class and low-wage workers is the 21 straight months of negative REAL weekly earnings growth.

On the housing front, REAL home prices are growing at 1.5% YoY while REAL weekly wage growth is still NEGATIVE at -3.13% YoY.

Make no mistake, inflation caused by The Fed and Federal governments spending is a tax on the middle class and low wage workers.

Biden, Pelosi, Schumer and Powell are the 4 Horseman of the Inflation Apocalypse.

One of the big problems with Federal goverment and Federal Reserve monetary stimulus is … it wears out. Just look at M2 Money growth.

US existing homes sales fell -7.70% in November to 4.09 million units SAAR. And since the same month last year, existing home sales are down -35.4% YoY.

Existing home sales were the lowest in November since 2010.

The good news? The median price of existing homes fell to 3.21% YoY. The bad news? The ark is really bad pointing to a bad December. Inventory for sale (orange line) remains below pre-Covid shutdown levels.

The Federal Reserve forecast for the US economy is a dismal 0.50% YoY. Do I detect a trend?

The FOMC forecast for 2023 and 2024. Core PCE YoY (inflation) is forecast to drop to 3.50%, still considerably higher than The Fed’s target rate of inflation of 2%. And unemployment is forecast to be 4.60%.

To cope with Bidenflation, US personal savings rate as of October is -67.9% YoY. The “good” news is that rents YoY are crashing. But food prices under Inflation Joe remain very high. But most everything is slowing down, not due to Biden’s policies, but a global and US economic slowdown.

With a big slowdown coming our way, you can understand why The Fed’s December Dot Plot is showing declining Fed Funds Target rate starts declining in 2024.

Even US mortgage rates are headed down.

Speaking of going down, cryptos are down across the board with Cardano leading the decline at -6.91%.

Central bankers won’t ride to the rescue when growth slows in this new regime, contrary to what investors have come to expect. They are deliberately causing recessions by overtightening policy to try to rein in inflation. That makes recession foretold. We see central banks eventually backing off from rate hikes as the economic damage becomes reality. We expect inflation to cool but stay persistently higher than central bank targets of 2%.

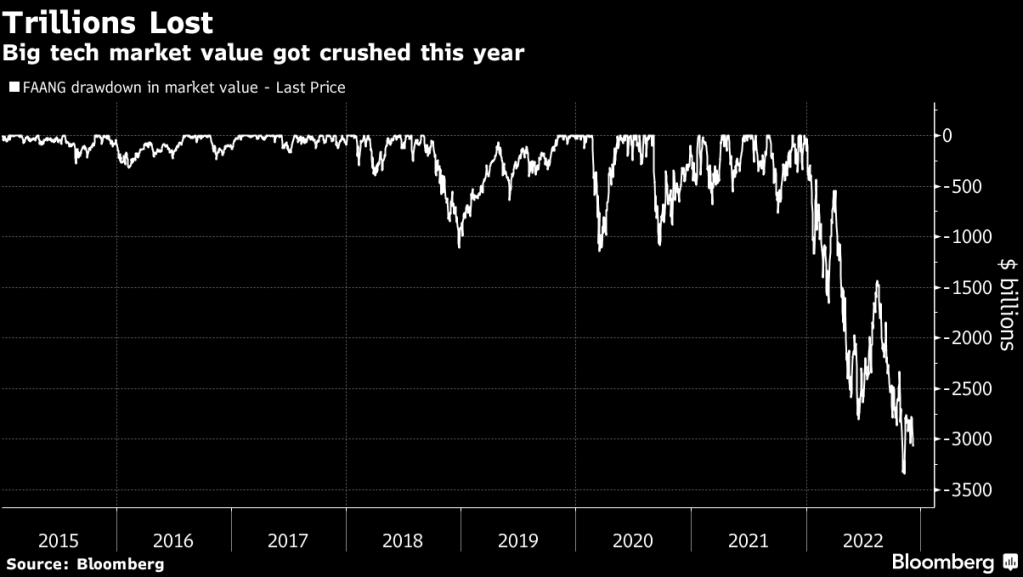

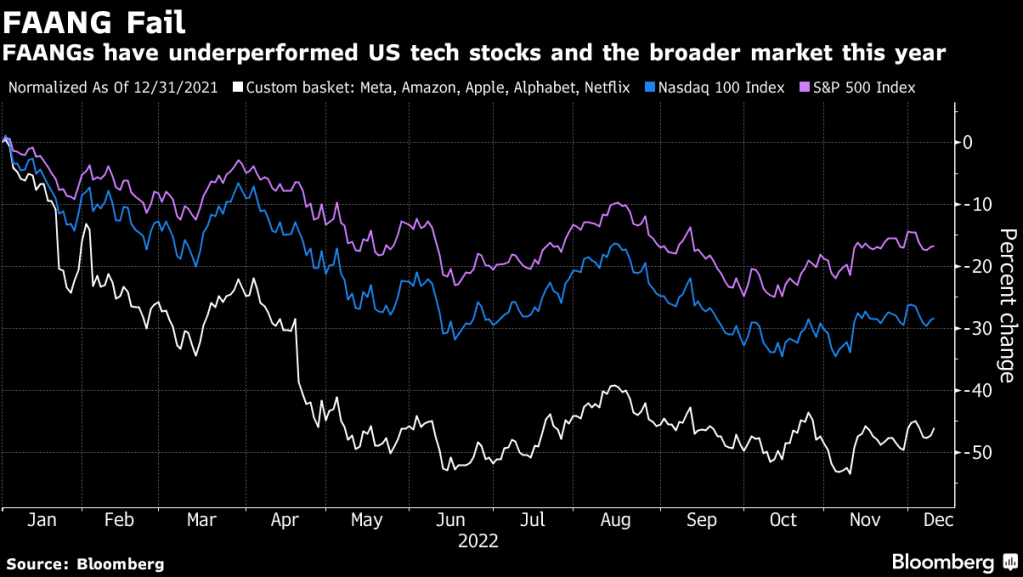

For some investors, this year’s rout in high-flying technology stocks is more than a bear market: It’s the end of an era for a handful of giant companies such as Facebook parent Meta Platforms Inc. and Amazon.com Inc.

Those companies — known along with Apple Inc., Netflix Inc. and Google parent Alphabet Inc. as the FAANGs — led the move to a digital world and helped power a 13-year bull run. And FAANG drawdown have reached over $3 trillion.

FAANGs (Meta, Amazon, Apple, Alphabet, Netflix) are getting clobbered in 2022.

Typically, when The Fed prints too much money, such as 10% or higher (red line), inflation follows. Particularly when The Fed prints at 25% YoY in Q4 2020, it was followed by the highest inflation rate in 40 years. But if M2 Money continues to slow, inflation will likely slow, but not to The Fed’s target of 2%.

Despite what Minneapolis Fed’s Neal Kashkari said about The Fed having infinite printing resourses, The Fed is going to fight inflation THAT THEY HELPED CAUSE. Biden’s energy policies (did you see that Elon Musk has a car that uses plentiful hydrogen?), and excessive Federal spending by Biden/Pelosi/Schumer, are culprits in creating the supply chain problems facing America. BUT after the 25% surge in M2 Money in 2020 and 2021, we saw M2 Money VELOCITY crash and burn to its lowest level in history. Which means the “bang for the buck” for printing more money is negligible.

Of course, big tech firms got caught influencing the 2020 Presidential election (see Musk’s release of Twitter files) and engaged in restriction of the 1st Amendment (Freedom of Speech). How much will that impact FAANG stocks going foward?

And yes, the US Treasury yield curve is inverted pointing to a recession in 2023.

And yes, apparently Biden was complicit in the Twitter fiasco.

Why is this terrifying? Blockchain technology is a fantastic innovation for processing payments given its ledger capabiliities. But that means that The Federal Reserve might be able to look at your complete history of expenditures. Or worse, perhaps even shut down your ability to make payments, This may lead to a China-style “social credit score” where the Fed and the Federal government punish people for driving “too much” increasing your carbon footprint or eating non-Federal government approved foods and lowering your social credit score.

Will there be safeguards? Allegedly, but remember the FBI hid Hunter Biden’s laptop prior to the Presidential election of late 2020. And HOW did our nation’s regulators completely drop the ball on Sam Bankman-Fried (or Spam Bankfraud)?

The US midterm elections are Tuesday. I was denied an absentee ballot for some reason, but I will get my disabled body over to the local precinct to cast my ballot.

Fortunately for Democrats, the next inflation report is not due out until November 10th. Because the forecast for the next inflation report is ugly.

Headline CPI YoY = 7.9%

Core CPI YoY = 6.5%

These numbers are slightly lower than the last inflation report, but Americans are still suffering mightily under Biden’s Reign of Error.

Diesel fuel prices, the lifeline of the food industry, is up 102% under Biden’s mandates with the inventory of diesel fuel down 36%.

Inflation is relentless like Jason from Halloween.

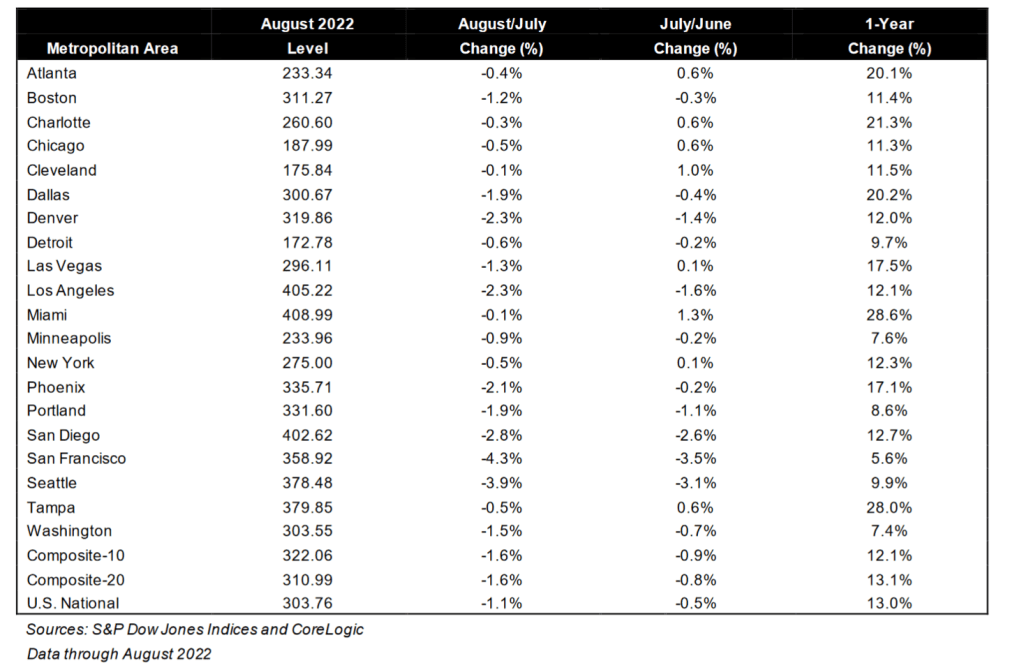

Alarm! US home prices are decelerating as inflation rages and The Fed tightens.

Home price growth in the US slowed the most on record as a doubling of borrowing costs (thanks to the US Federal Reserve) has sapped demand.

A national measure of prices increased 13% in August from a year earlier, but is down from 20.79% in March, the S&P CoreLogic Case-Shiller index showed Tuesday. That’s the biggest deceleration in the index’s history.

The housing market has started to slump as the Federal Reserve hikes interest rates to curb the hottest inflation in decades. Even with the deceleration, prices remain high compared to last year. Coupled with mortgage rates that are edging closer to 7%, many would-be buyers have been shut out, while some sellers have retreated.

While 13% growth sounds good, it is not good for renters looking to buy a home.

According to S&P/CoreLogic/Case-Shiller, Southern (red) cities Atlanta, Charlotte, Dallas, Miami and Tampa all still grew at over 20% YoY. Other cities like blue cities Detroit, Minneapolis, Portland, San Francisco, Seattle and Washington DC are grew at UNDER 10% YoY.

On related news, I always said in my classes that +/- 10 basis point in the US Treasury yield is a big deal. This morning, the US Treasury 10-year yield is DOWN -16.1 bps. In fact, the 10-year yields are down across the board globally.

Pension funds hold large positions in US Treasuries and Agency Mortgage-backed Securities (MBS). As does America’s central bank, The Federal Reserve. All are suffering losses as The Fed fights inflation.

(Bloomberg) — Week by week, the bond-market crash just keeps getting worse and there’s no clear end in sight.

With central banks worldwide aggressively ratcheting up interest rates in the face of stubbornly high inflation, prices (created by The Fed, Biden’s Green Energy Follicies and reckless Federal spending) are tumbling as traders race to catch up. And with that has come a grim parade of superlatives on how bad it has become.

On Friday, the UK’s five-year bonds tumbled by the most since at least 1992 after the government rolled out a massive tax-cut plan that may only strengthen the Bank of England’s hand. Two-year US Treasuries are in the middle of the the longest losing streak since at least 1976, dropping for 12 straight days. Worldwide, Bank of America Corp. strategists said government bond markets are on course for the worst year since 1949, when Europe was rebuilding from the ruins of World War Two.

The escalating losses reflect how far the Federal Reserve and other central banks have shifted away from the monetary policies of the pandemic, when they held rates near zero to keep their economies going. The reversal has exerted a major drag on everything from stock prices to oil as investors brace for an economic slowdown.

And as The Fed tries to combat stubborn inflation (caused by The Fed, Biden’s Green Energy folly and reckless Federal spending), you can see the US government security liquidity is worsening.

At least inflation has produced one “positive.” REAL mortgage rates are NEGATIVE since Freddie Mac’s 30-year mortgage rate less headline inflation is currently -2.975%.

Then we have Agency MBS (example, FNCL 3% MBS) plunging like a paralyzed falcon as duration risk increases with Fed rate tightening.

Fed Funds Futures data points to tightening until May ’23, then a reversal of rate hikes.

Inflation is stubborn because “goin’ green!” by 1) restricting US fossil fuel production and exploration and 2) Biden/Congress endless spending splurge since Covid. So, The Federal Reserve has a tough problem: cooling inflation while US energy prices are up 54% under Biden. And those higher energy prices have percolated through the entire economy in terms of food prices and heating prices.

Where do we sit? The US Treasury 10yr-2yr yield curve remains inverted (a sign of impending recession). Mortgage rates are the highest in 14 years as The Fed tightens.

If we look at Fed Funds Futures data, we can see that traders expect The Fed’s target rate to rise to 4.395% by March 2023’s FOMC meeting. Then traders expect The Fed to take their enormous foot off the tightening pedal.

Yes, inflation is crushing the middle class and low-wage workers. Average hourly earnings YoY after we subtract inflation are negative.

Taylor Rule? Currently, the Taylor Rule based on Core inflation of 4.56% YoY suggests a Fed target rate of 9.14%. Since traders anticipate the target rate to peak at 4.395%, The Fed will almost be halfway towards cooling inflation.

The problem is … Fed Chair Powell and Treasury Secretary Yellen don’t like rules limiting their “power.” Powell and Yellen think the Taylor Rule is a New Jersey ham product.

Dear Mr. Fantasy, play us a tune, something to make us all happy (like hitting 2% inflation WITHOUT crashing the economy). Do anything take us out of this gloom (caused by The Fed, Biden’s energy policies and Federal spending). Sing a song, play guitar, Make it snappy. Or in the case of housing, make it crappy.

(Bloomberg) — Federal Reserve Bank of Richmond President Thomas Barkin said the central bank was resolved to curb red-hot inflation, even if that meant risking a US economic recession.

“We’re committed to returning inflation to our 2% target and we’ll do what it takes to get there,” Barkin said Friday during an event in Ocean City, Maryland. He said that this could be achieved without a “tremendous decline in activity” but acknowledged that there were risks.

“There’s a path to getting inflation under control but a recession could happen in the process,” he said.

The US central bank hiked interest rates by 75 basis points in July for the second straight month as policy makers tackle inflation that’s running near 40-year highs. Fed officials speaking in recent days have said more rate increases are needed, but they are still deciding how big to move at their next policy meeting.

St. Louis Fed President James Bullard, one of the most hawkish policy makers, on Thursday urged another 75 basis-point move while Kansas City’s Esther George struck a more cautious tone.

Well, The Fed (aka, Der Kommissars) let the monetary stimulus blow out of control since 2000.

With the 2001 recession, The Fed crashed the target rate (white line) causing home price growth (blue line) to soar. Then The Fed decided that the economy was overheated and cranked up their target rate. This sudden rise in The Fed’s target rate helped to slow/crash housing prices. Resulting in … a frantic decrease in the target rate (late 2007- late 2008) and the adoption of asset purchases of Treasury Notes/Bonds and Agency Mortgage-backed Securities in late 2008.

The Bernanke/Yellen “loose as a goose” policies from late 2008 to Feb 2018 created a total mess. Bernanke/Yellen raised the target rate only one before Trump was elected President, and 8 times AFTER Trump was elected. And Yellen’s Fed began to let the balance sheet shrink a bit before Covid struck in early 2020. And with Covid came another massive expansion of The Fed’s Balance Sheet WHICH HAS NOT YET BEEN WITHDRAWN (despite Fed talking heads saying it would be reduced).

Here we sit with The Fed NOW trying to extinguish inflation (yellow line) by raising their target rate (white line) but NOT shrinking the balance sheet (orange line).

Wonder why this is a horrible homeless problem in the US, particularly in California? While Stanford University has an excellent study of the causes of California’s homeless problem, there is another cause of homelessness … The Federal Reserve’s insane monetary policies since late 2008. The Case-Shiller National Home Price Index is 65% higher in May than during the calamitous home price bubble of 2005-2007, helping to exacerbate the homeless problem.

One of the many problems created by the reckless Bernanke/Yellen/Powell monetary policies is the M2 Money Velocity is near an all-time low making a return to “easy money policies” far more difficult.

I won’t post any photos of the homeless encampments in Los Angeles since it is very sad. But here is a photo of the Dunder-Mifflin paper company “office” on Saticoy Street. The point is that thanks to The Federal Reserve’s loose monetary policies, housing is unaffordable for millions of households forcing many to live on the streets.

Figure 2: Median Rent for a Two-Bedroom Apartment, California, 2022

And a point of trivia. The Office’s Charles Miner (played by the GREAT Idris Elba) was allegedly hired from Saticoy Steel. The Dunder-Mifflin paper company site was on Saticoy Street in sunny LA, not Scranton PA.

Good luck to The Federal Reserve in combating inflation without causing a recession.

You must be logged in to post a comment.