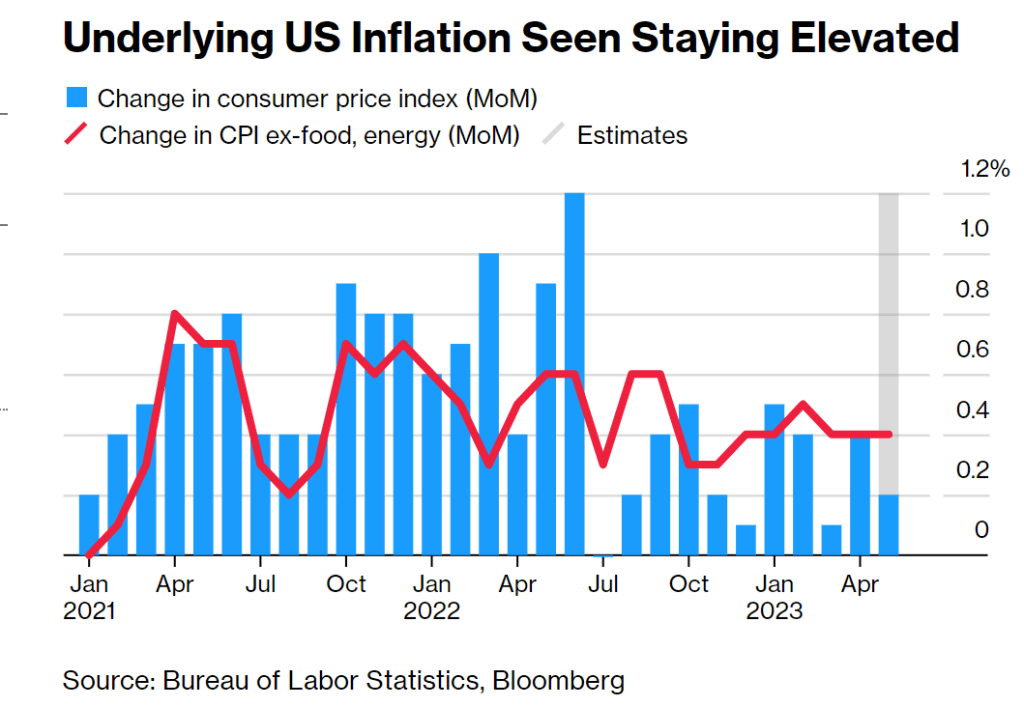

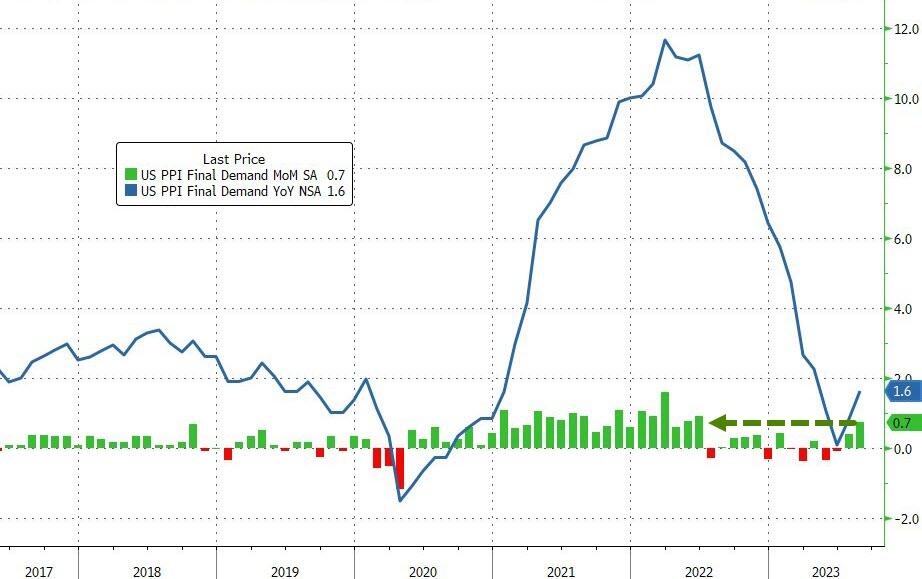

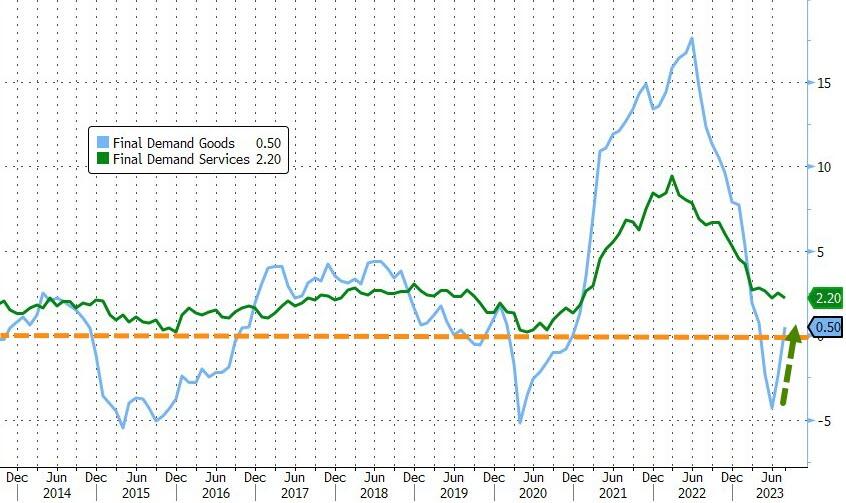

Producer Prices rose 0.7% MoM in August (up from +0.3% in July and hotter than the +0.4% exp). That is the hottest PPI since June 2022, and pushed YoY prices up 1.6%…

Source: Bloomberg

Goods prices are reaccelerating fast, now back into inflation YoY (as Services cost growth slowed only modestly)…

Source: Bloomberg

As a reminder, much of last month’s PPI rise was driven by a big jump in portfolio management costs – as stocks soared. August saw a further rise in those costs…

Source: Bloomberg

More problematically, the pipeline for PPI appears to have inflected as intermediate demand is re-accelerating…

What is Bidenomics? It isn’t what Press Secretary Karine Jean Pierre thinks. She said Biden hates “trick down economics”. Instead, Biden prefers a Soviet-style command economy where The Federal Government spends trillions of dollars and directs where the money goes. We also have the Socialist Federal Reserve that relies on rate manipulation to achieve policy results.

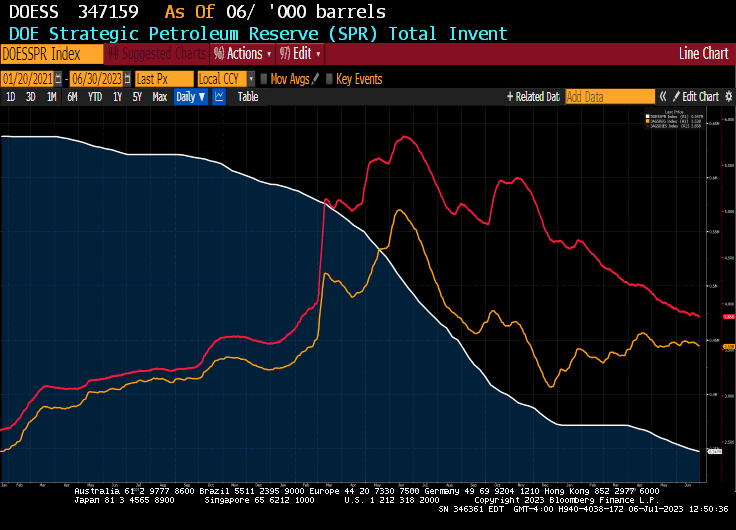

A good example of Biden’s Soviet-style “Bidenomics” is his use of the Strategic Petroleum Reserve (SPR). Biden has now drained almost 50% of the SPR from when he was sworn in as President. And has drained the SPR for 14 straigth weeks to manipulate gasoline and diesel fuel prices in an effort to lower fuel prices ahead of the 2024 Presidential election. Watch Biden suddenly stop caring about fuel prices once he wins reelection!

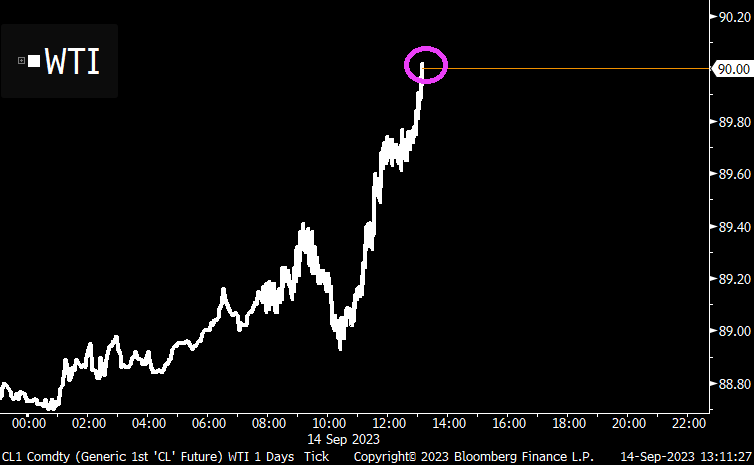

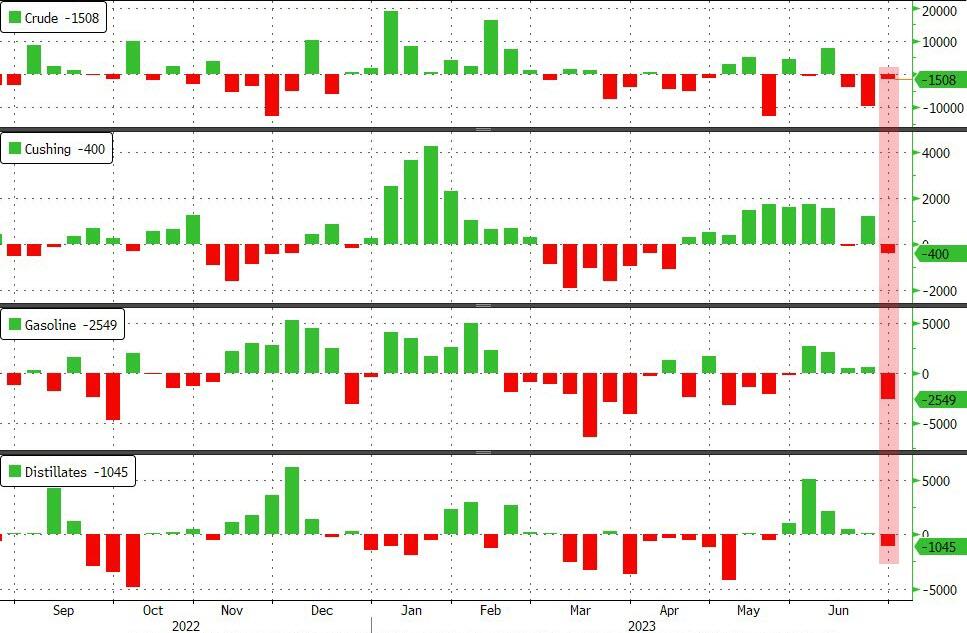

After last week’s huge draw, expectations were for a smaller draw (which API showed last night), but the actual crude draw was smaller – just 1.5mm barrels. Stocks at the Cushing hub fell 400k barrels and products also saw notable draws..

At least we now know who left cocaine in the White House!

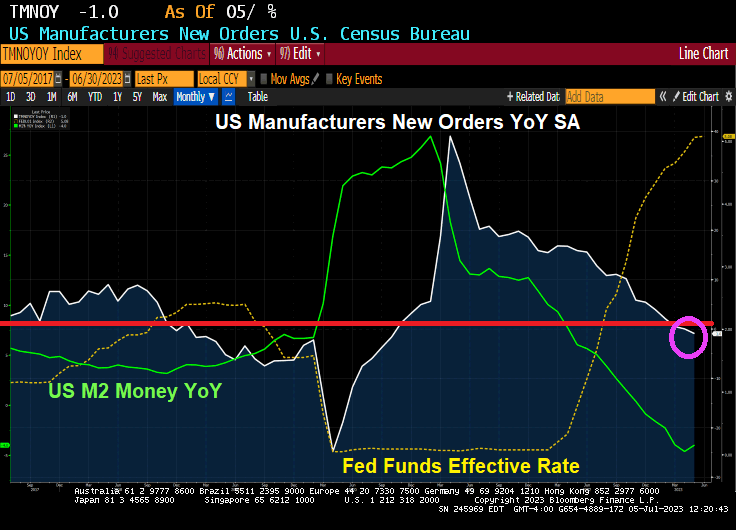

As Powell and The Gang raise interest rates, the more the economy is … slip slidin’ away. US Manufacturers New Orders YoY in May declined -1.0% for the first time since Covid.

The film “The Core” was a silly film, but core inflation in the US is a serious problem for the middle class and low-wage workers. It remains elevated despite Treasury Secretary Janet “The Marxist Gnome” Yellen saying it was “transitory.” Looks pretty permanent to me!

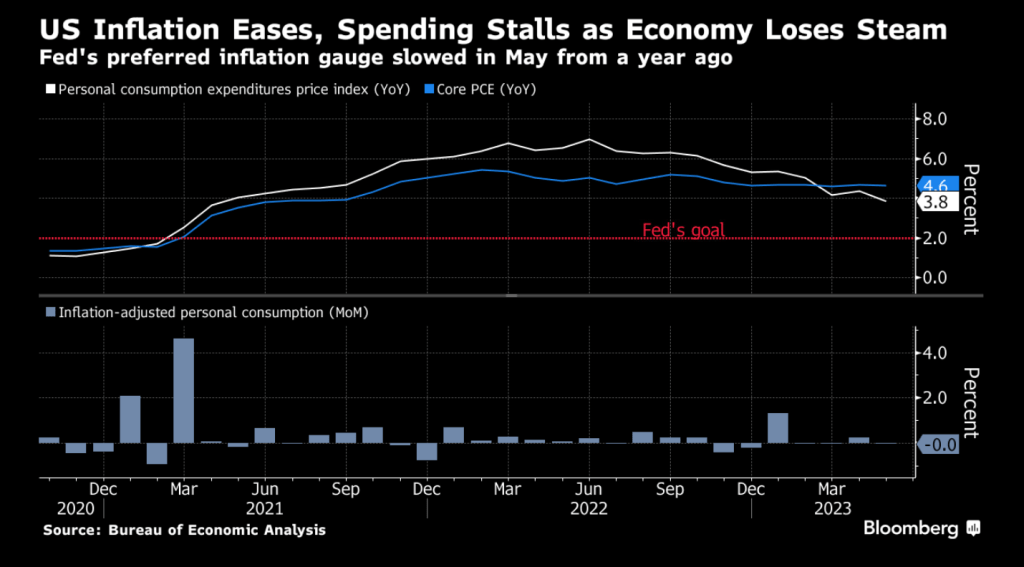

The Federal Reserve’s preferred measures of US inflation cooled (slightly) in May and consumer spending stagnated, suggesting the economy’s main engine is starting to lose some momentum.

The personal consumption expenditures price index rose 0.1% in May, Commerce Department figures showed Friday. From a year ago, the measure eased to the slowest pace in more than two years.

Consumer spending, adjusted for prices, was little changed after a downwardly revised 0.2% gain in April. From February through May, household spending has essentially stalled after an early-year surge. Spending on merchandise dropped, while outlays for services increased.

Excluding food and energy, the so-called core PCE price index increased 4.6% from May 2022. That’s in line with annual readings back to late 2022 and shows minimal relief from elevated price pressures. Economists consider this to be a better gauge of underlying inflation.

Indicator

Actual

Estimate

PCE price index (MoM)

+0.1%

+0.1%

Core PCE price index (MoM)

+0.3%

+0.3%

PCE price index (YoY)

+3.8%

+3.8%

Core PCE price index (YoY)

+4.6%

+4.7%

Real consumer spending (MoM)

0.0%

+0.1%

Under the hood of the government report, a key metric flagged by Fed Chair Jerome Powell showed a welcome slowdown. Services inflation excluding housing and energy services increased 0.2% in May from a month earlier, the smallest advance since July of last year, according to Bloomberg calculations. The figure was up 4.5% from a year ago.

The Taylor Rule now suggests a target rate of 10%. We are just halfway to target!

Meanwhile, Yellen Plans July China Trip, While US Preps Investment Curbs. Trying to convince China that the US won’t default on its $32 TRILLION and growing debt?

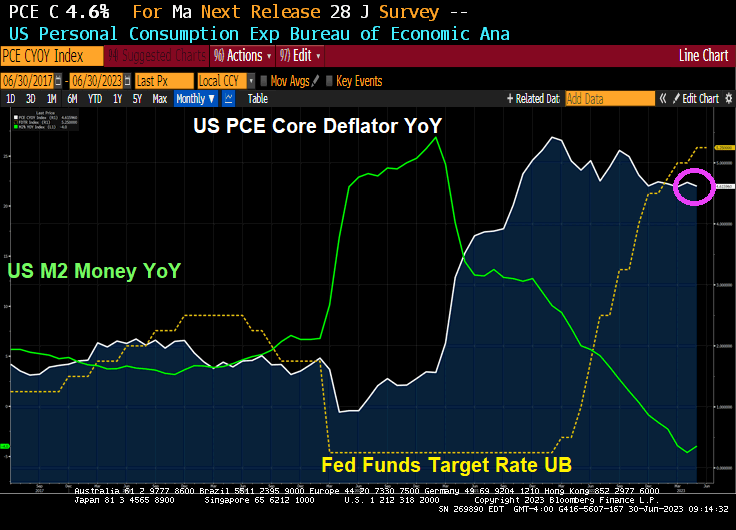

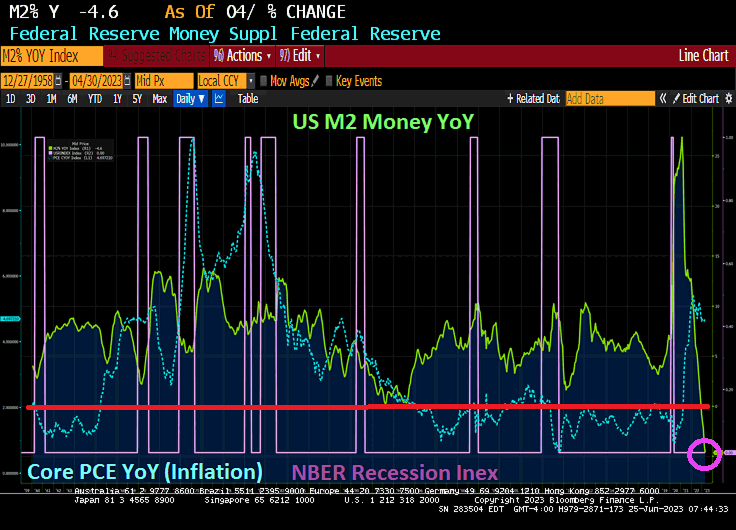

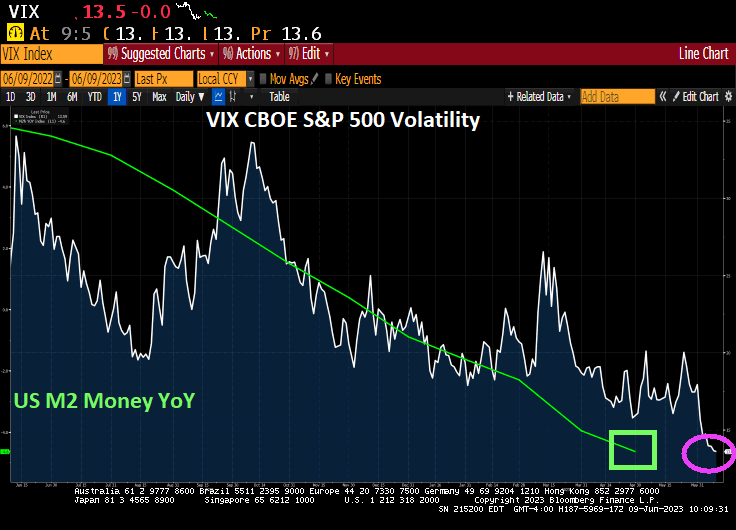

Money supply growth fell again in April from Jerome Powell And The Fed, plummeting further into negative territory after turning negative in November 2022 for the first time in twenty-eight years. April’s drop continues a steep downward trend from the unprecedented highs experienced during much of the past two years.

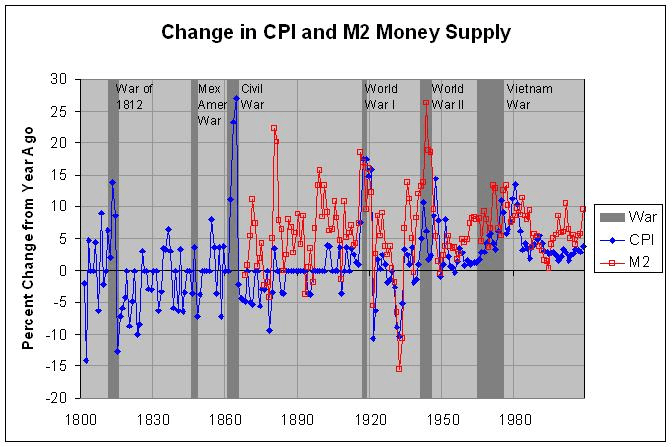

Yes, The Fed is printing money like it is going out of style! The war on Covid was similar to other wars fought where the US printed boatloads of money to pay for WWI. WWII, Korea and Vietnam wars. And the war against the middle class (known as The Best Depression). Apparently, The Fed is still waging war against the middle class.

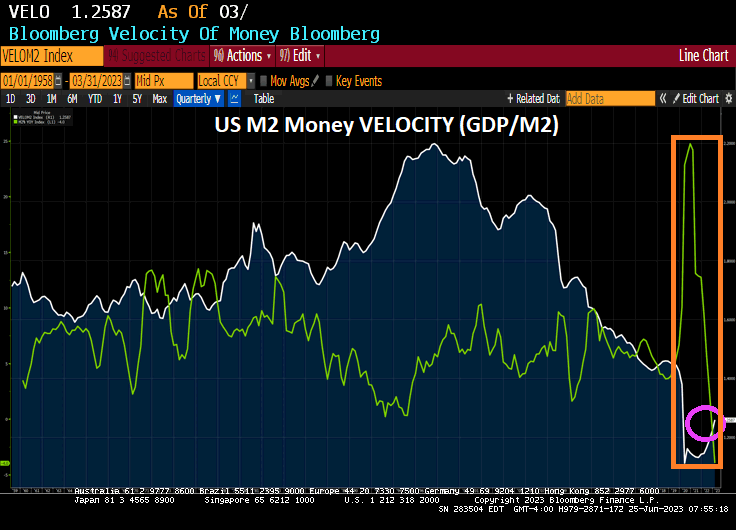

US M2 Money VELOCITY (GDP/M2) is near an all-time low after The Fed went berserk with money printing to combat the Covid economic and school shutdowns.

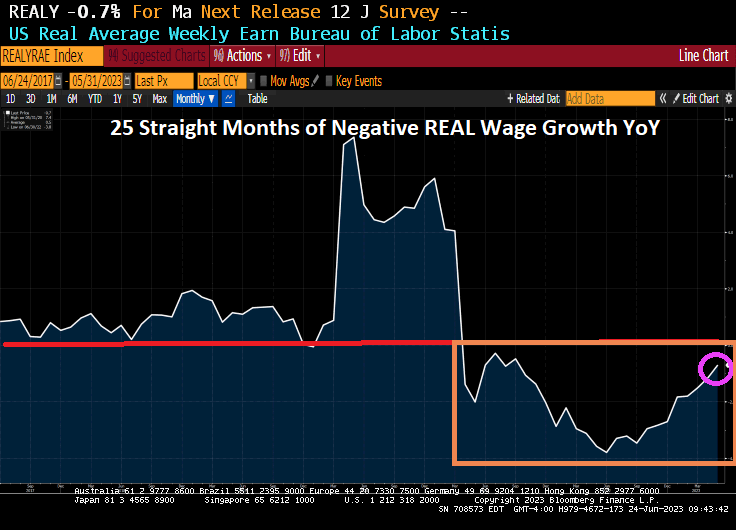

Then with The Fed’s massive monetary expansion and sudden contraction, we have REAL average weekly earnings growth YoY in negative territory for 25 straight months.

The Walking Dead’s Negan, the poster child for The Federal Reserve.

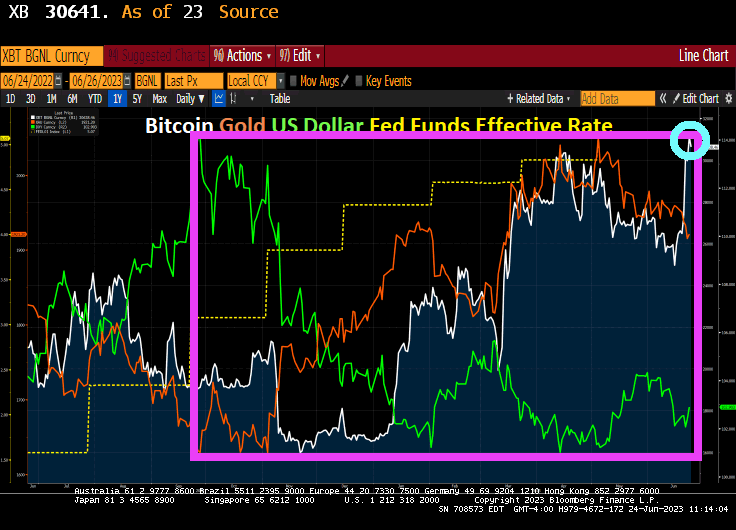

Well, with Jerome Powell And The Fed tightening monetary policy (about half way there!), we have seen competitors to the US Dollar Bitcoin and Gold have soared since September 26, 2022. Bitcoin is up 61%, Gold is up 18% and the US Dollar is down -10%.

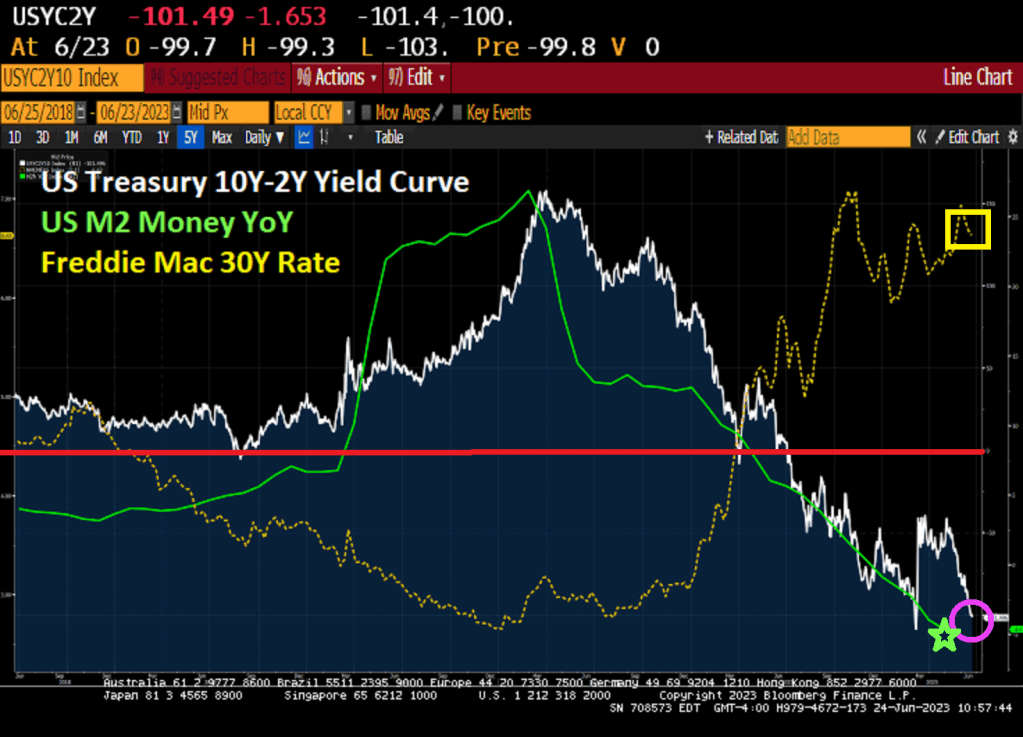

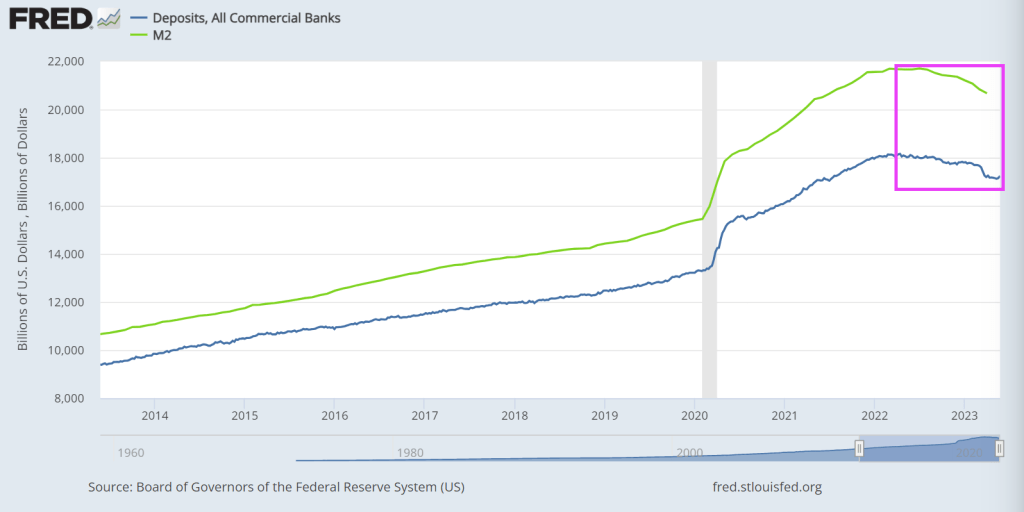

Mortgage rates hover around 7% as the US Treasury 10-2Y curve inverts to over -100 basis points with M2 Money growth crashed and burned.

Federal Reserve policymakers are about to take their first break from an interest-rate hiking campaign that started 15 months ago, even as they confront a resilient US economy and persistent inflation.

The Federal Open Market Committee on Wednesday is expected to maintain its benchmark lending rate at the 5%-5.25% range, marking the first skip after 10 consecutive increases going back to March of last year. While officials’ efforts have helped to reduce price pressures in the US economy, inflation remains well above their goal.

Source: Bureau of Labor Statistics, Bloomberg

Investors’ focus will be on the Fed’s quarterly dot plot in its Summary of Economic Projections, which is expected to show the policy benchmark rate at 5.1% at the end of 2023.

By contrast, markets are pricing in the possibility of a quarter-point hike in July followed by a similar-sized cut by December, and some Fed policymakers have emphasized that a pause in the hiking cycle shouldn’t be seen as the final increase.

Fed Chair Jerome Powell, who’ll hold a press conference after the meeting, has suggested he favors a break from hiking to assess the impact both of past moves and of recent banking failures on credit conditions and the economy. His commentary will be scrutinized for hints of the committee.

Remember, there is still over $8 TRILLION in Fed assets held sloshing around the economy. The Fed never really removed the excess liquidity and it continues to stoke asset bubbles.

Bear in mind that The Fed is pausing at 5.25% Fed Target Rate, while the Taylor Rule suggests rate hikes to 10.12%. So, Foul Powell is pausing at just over the half way mark.

Of course, Biden’s and Congress’ massive spending spree is causing inflation, and The Fed has no control over Biden/Congress irresponsible spending.

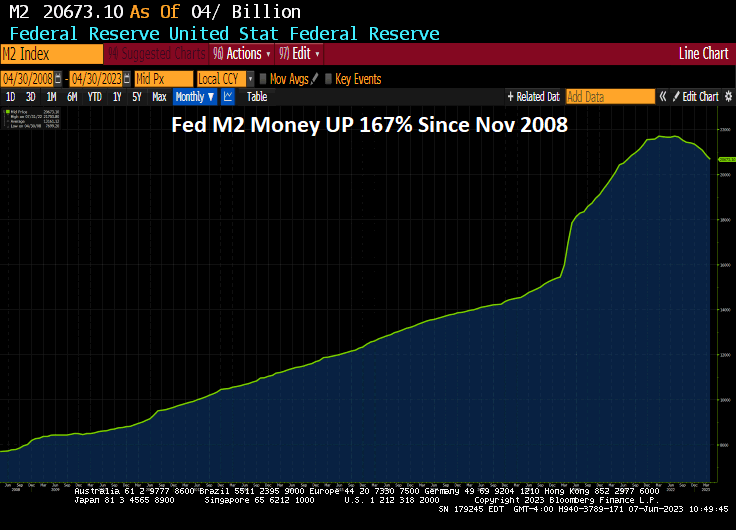

One has to wonder about The Feral Reserve. Since The Great Recession of 2008, The Federal Reserve has printed a staggering amount of money (know as QE). There is still about $8.3 TRILLION in monetary stimulus sloshing around the economy.

And M2 Money printing is up 167% since November 2008.

So, despite the talking heads from The Fed and CNBC, etc blathering about Fed tightening, there remains over $8 TRILLION in monetary stimulus chasing asset prices.

Is The Fed ACTUALLY the US economy? Or is The Fed the financing arm of the Democrat party?

Yes, The Fed looks like they are pausing .. rate hikes.

But it isn’t just San Francisco. Phil Hall reports that Fitch Ratings reduced its 2023 outlook for the U.S. real estate investment trust (REIT) sector outlook from “Neutral” to “Deteriorating,” citing the tumult in the commercial real estate space.

While Fitch noted that most of its rated REITs “have the capacity to withstand such a slowdown within rating sensitivities [and] those with ample dry powder could capitalize on distressed property sales by weaker capitalized players.” But at the same time, the ratings agency warned that banks – which account for nearly half of the $5.5 trillion commercial mortgage market – saw their lending levels drop by 20% between February and April, with more tightening expected.

“At minimum, this will lead to further contractions in CRE credit, further limiting conditions for property transactions,” Fitch added in its announcement of the outlook reduction, adding that “CRE transaction volume has steadily declined since early 2022 due to the confluence of operating fundamentals pressure, higher interest and capitalization rates, limited buyer financing, and looming recession risk. The rapid jump in rates has resulted in unusually wide value discrepancies between buyers and sellers across most property types and markets, particularly in the struggling office sector. Our forward-looking U.S. equity REIT ratings incorporate assumptions about future property disposition volumes and valuations.”

Fitch predicted the U.S. economy will go into a recession, most likely late in the year – a previous forecast put the downturn at mid-year – and forecasted property performances will vary by sector over the next two years.

“Sectors experiencing strong fundamentals, such as industrial and shopping centers, will likely see some cooling in demand, with tenants showing greater reluctance to lease space, including delaying decisions, resulting in less pricing power for landlords,” Fitch continued. “Tighter lending conditions and weaker economic growth will add to the secular pressures facing some property formats (e.g. office, enclosed malls). The office REIT sector has met, or modestly underperformed, our low expectations during 2023. Leasing volumes have generally underperformed as occupiers add the business cycle to the list concerns and reasons for conservatism, along with secular pressure from remote work. Conversely, the industrial sector, although no longer white hot, continues to deliver above average occupancies and outsized rent growth that have modestly exceeded our projections.”

While Fitch stressed that REITs were “unlikely to directly encounter meaningful stress” based on the recent problems in the banking industry, although it also acknowledged that it did not expect “REITs’ access to unsecured revolvers will be impeded, although facilities up for renewal will likely see higher pricing and some banks have reduced appetites for traditional bank syndicate activities, such as making funded term loans – particularly in hard hit sectors, such as office. We also do not expect meaningful portfolio vacancies caused by bank tenant failures, which are unlikely to be widespread.”

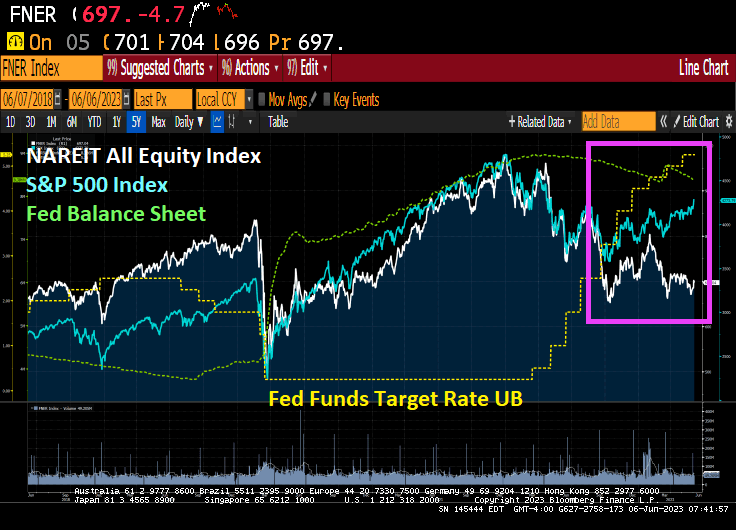

The NAREIT All-equity index has gotten pummelled by the S&P 500 index since The Fed started tightening monetary policy to fight inflation …. that The Fed helped cause in the first place.

Under Biden, the US is beginning to morph into a lawless Socialist sewer like Venezuela. Joe Maduro??

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.