Nobody but Biden could so handicap an economy with horrible fiscal policies, massive debt, inflation and open borders. And then go to the Virgin Islands for yet another taxpayer paid vacation. Biden has spent 40% of his Presidency on vacations.

Bidenomics is a disaster for the US middle class. And Bidenomics with its inflation has led The Fed to counterattack and raises interest rates, leading to losses for The Federal Reserve (which is paid for by US Treasury) of over $130 billion.

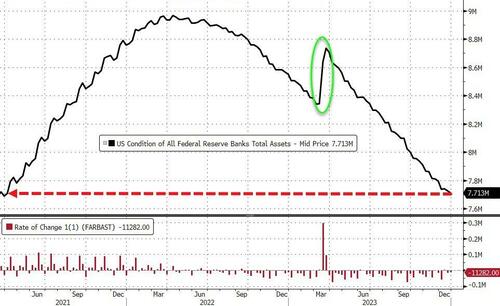

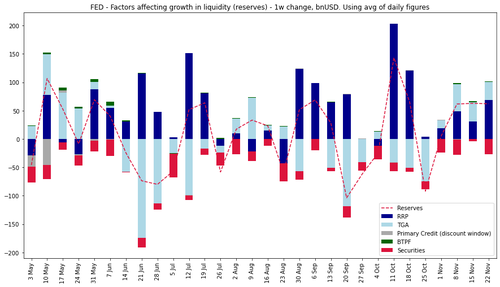

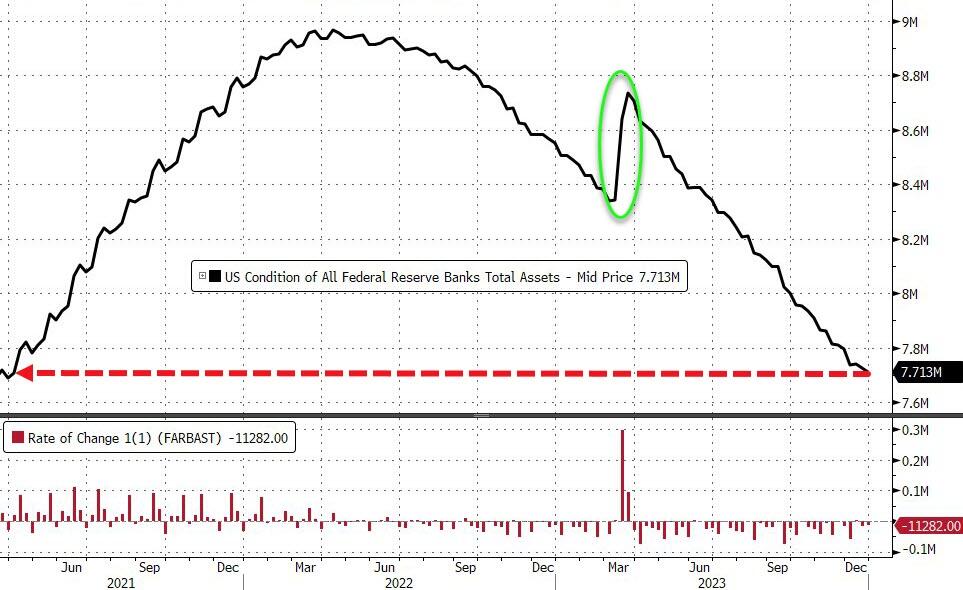

The Fed’s balance sheet shrank by $11.3BN last week to its lowest level since March 2021, but still remains elevated.

Source: Bloomberg

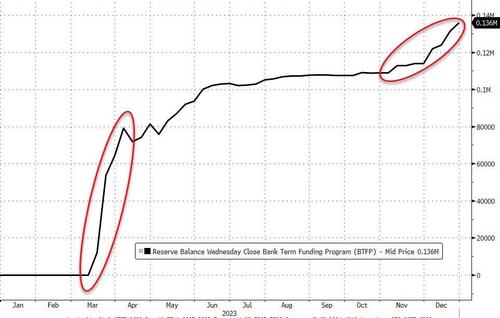

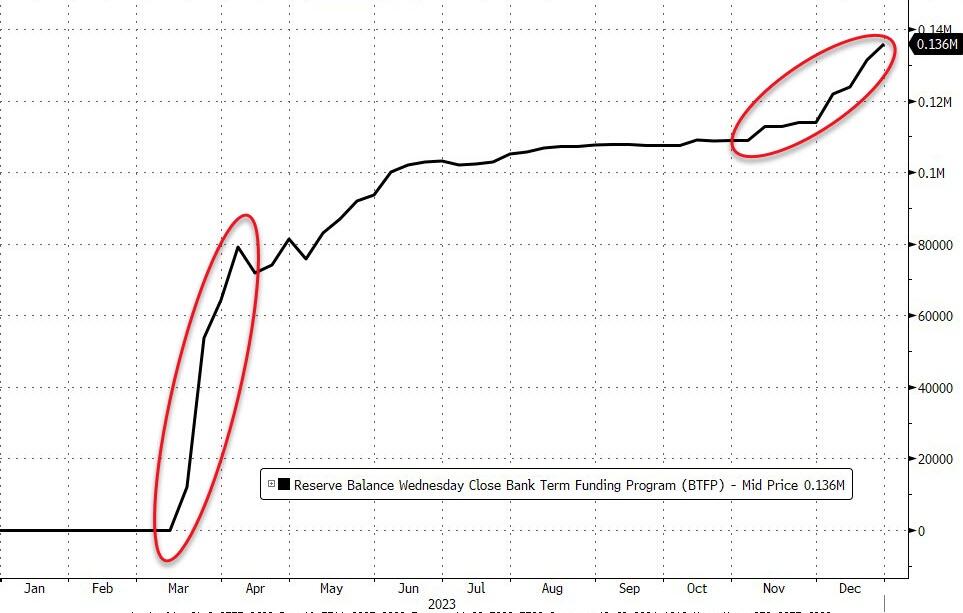

Usage of The Fed’s bank bailout facility rose by another $4.5BN last week to a new record high of $136BN…

Source: Bloomberg

The BTFP-Fed Arb continues to offer ‘free-money’ (and usage of the BTFP has risen by $26.7BN since the arb existed):

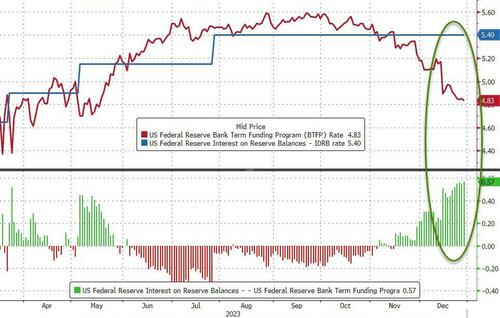

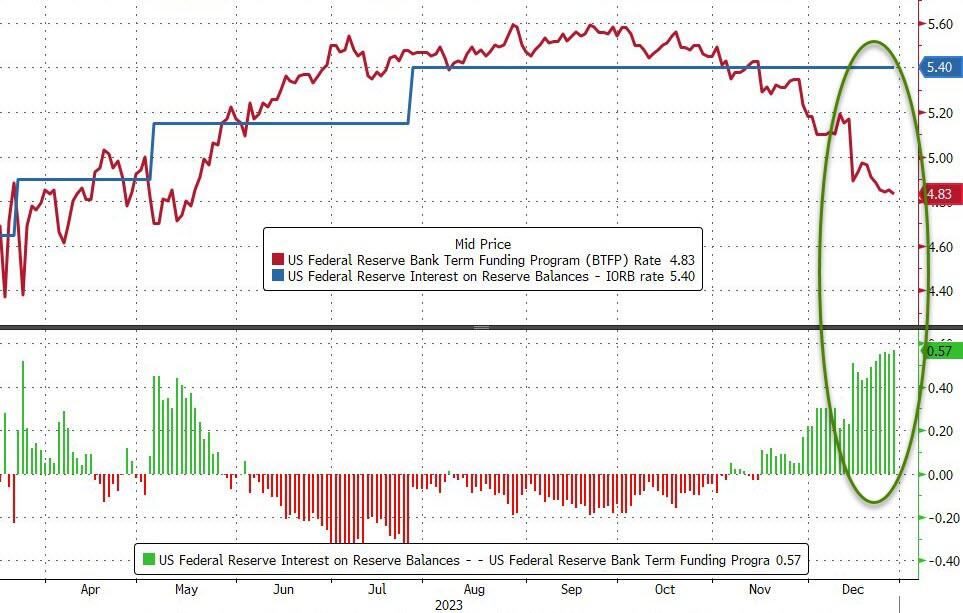

The rate on the Fed’s Bank Term Funding Program – which allows banks and credit unions to borrow funds for up to one year, pledging US Treasuries and agency debt as collateral valued at par – is the one-year overnight index swap rate plus 10 basis points.

That figure is currently 4.83%, down from 5.59% in September.

For institutions that have an account at the Fed, they can borrow from the BTFP at 4.83% and park that at the central bank to earn 5.40% – the interest on reserve balances.

Source: Bloomberg

The 57bp spread is the widest level since the Fed introduced the facility to support a struggling banking system after the collapse of California’s Silicon Valley Bank and Signature Bank in New York.

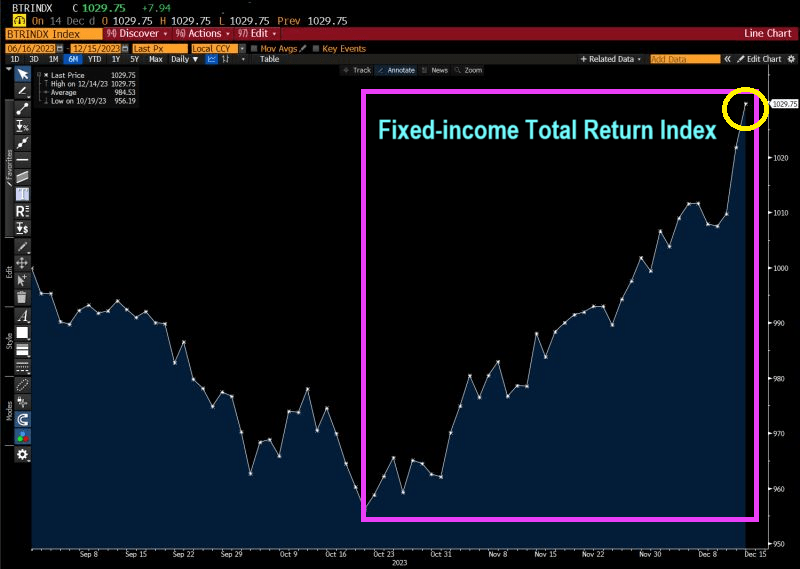

Like the spaghetti western “The Good, The Bad And The Ugly,” Bidenomics has had similar effects on financing. Some good, some bad and a lot of uglies.

The good! For investors like pension funds the own US Treasuries, inflation has led The Federal Reserve to raise interest rates. This is good for investors holding short-term debt. The Bianco Fixed Income Total Return Index is soaring!!

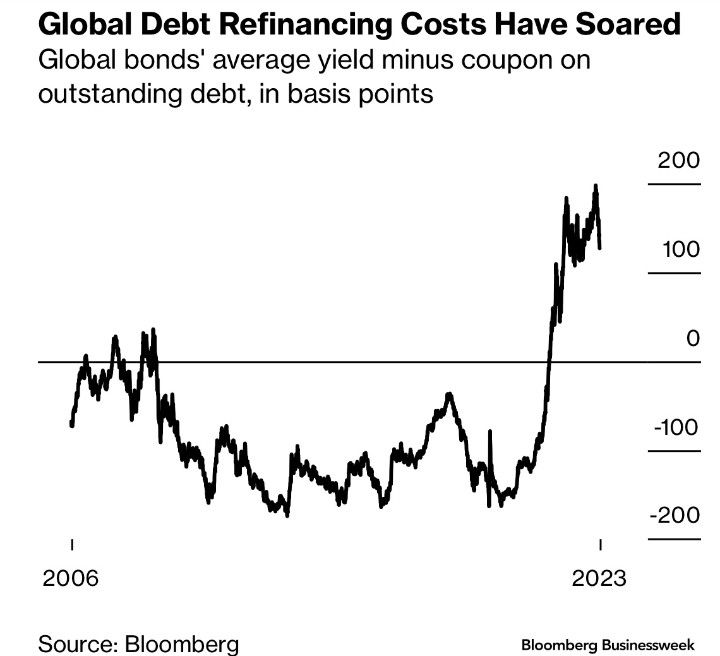

The Bad: Well, the flip-side of the same coin is that debt refinancing costs have soared.

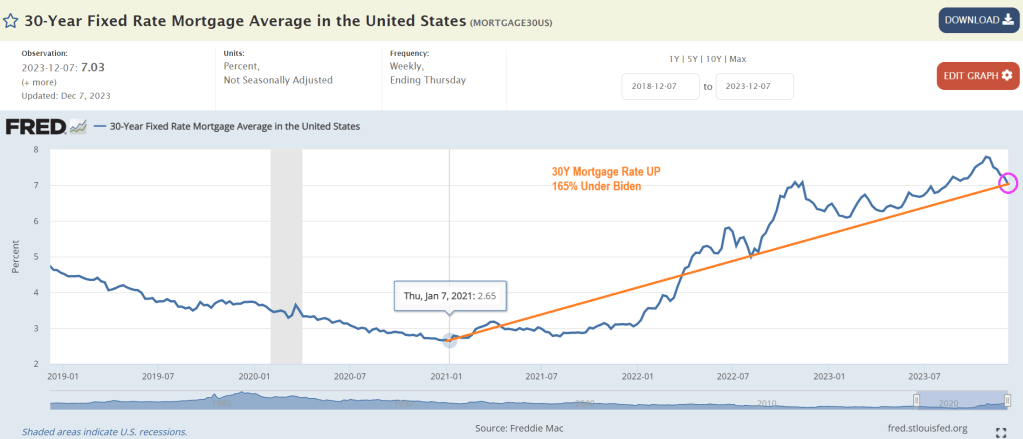

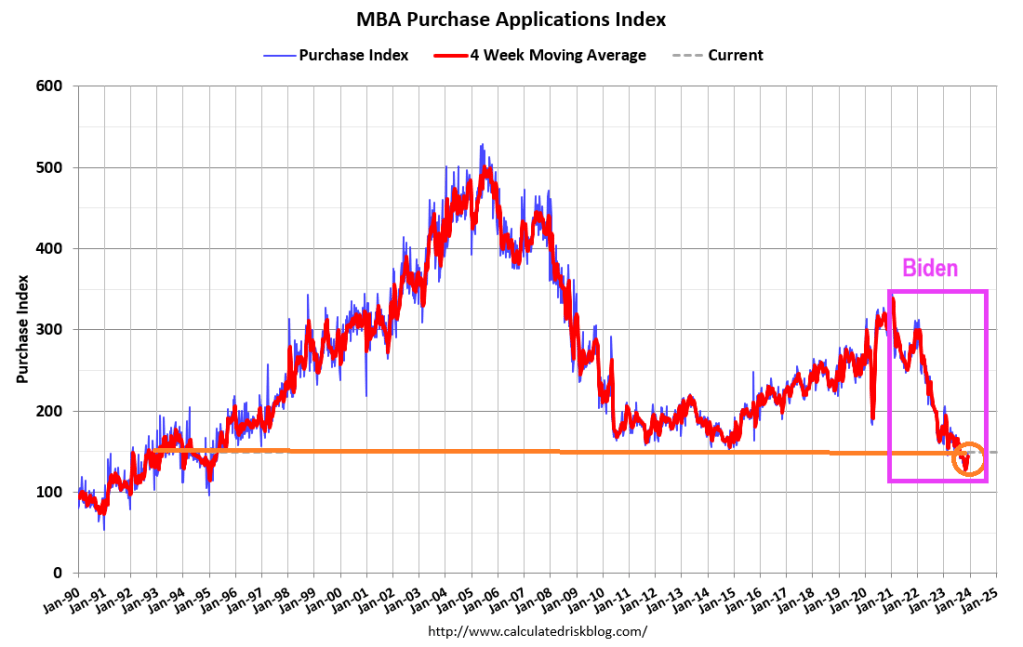

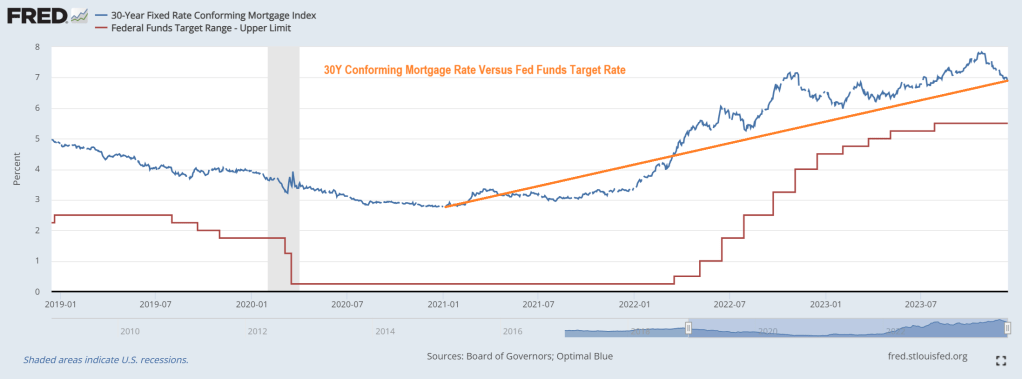

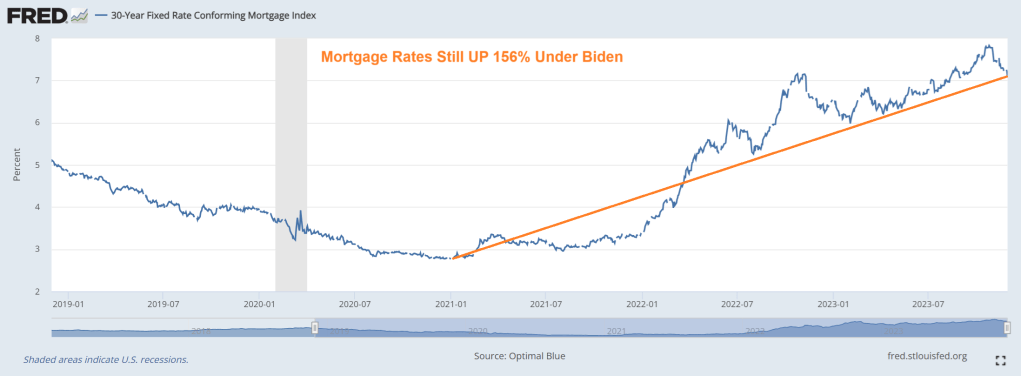

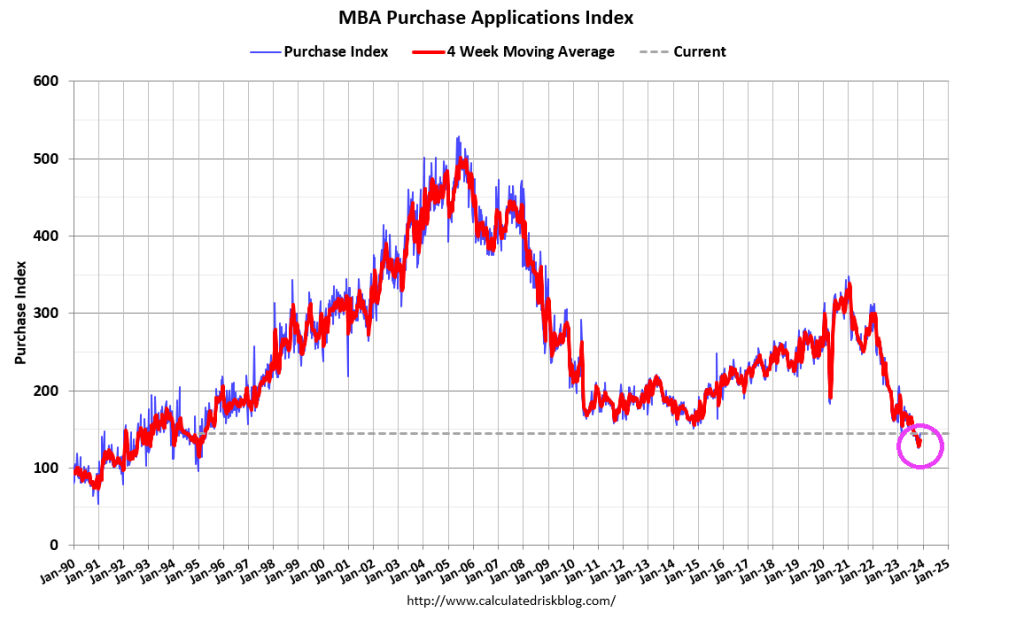

The Ugly. There are many contenders for losers under Bidenomics and current Fed (garbled) policies. But I choose … mortgage demand collapse with rising home prices and rising mortgage rates. Mortgage rates are up 165% under Biden.

And mortgage demand (applications) have been crushed.

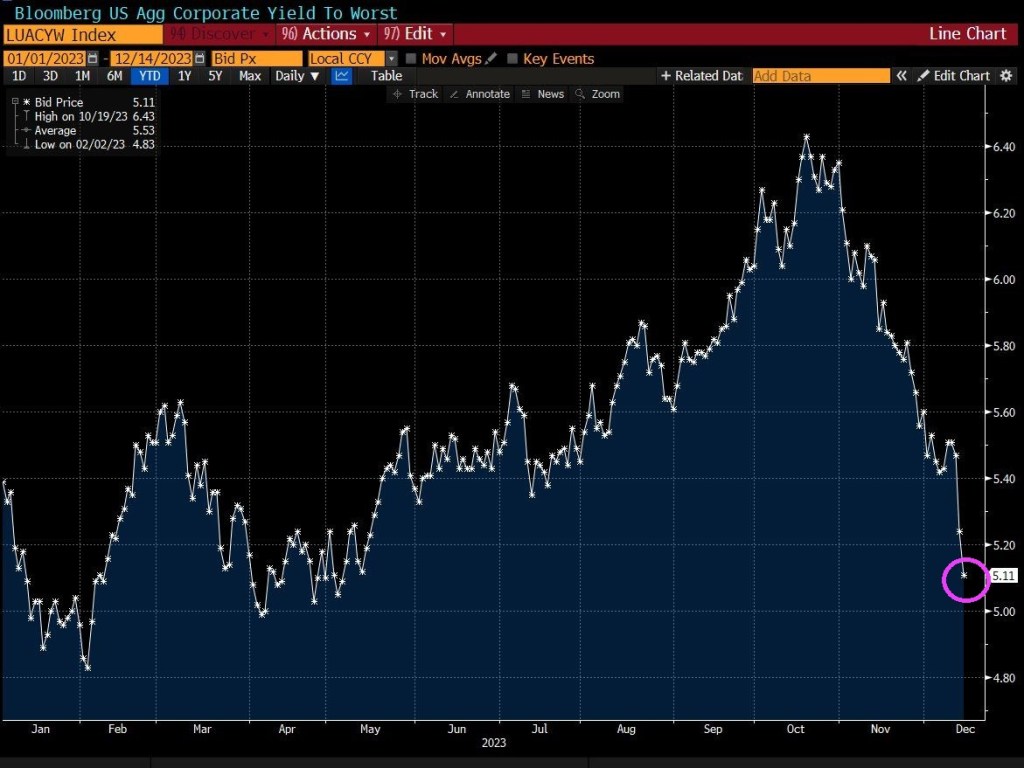

Also on the ugly side, global aggregate corporate yields have collapsed.

So, there have been winners with Bidenomics (the top 1%), and lots of losers.

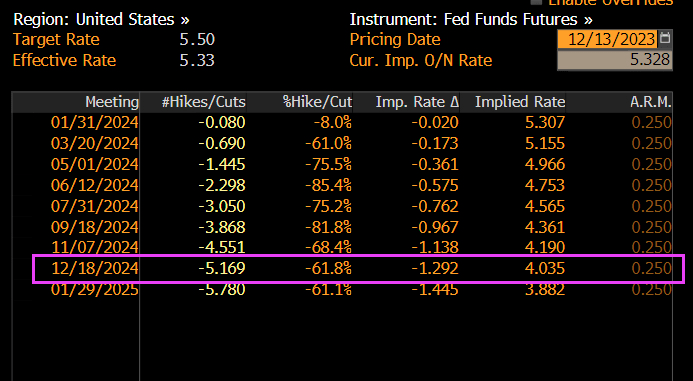

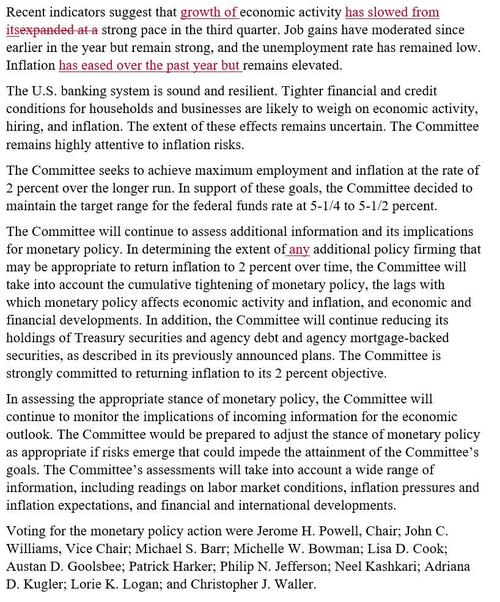

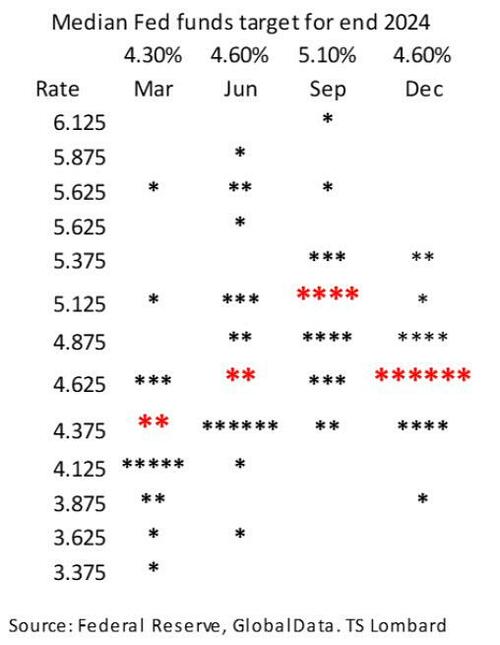

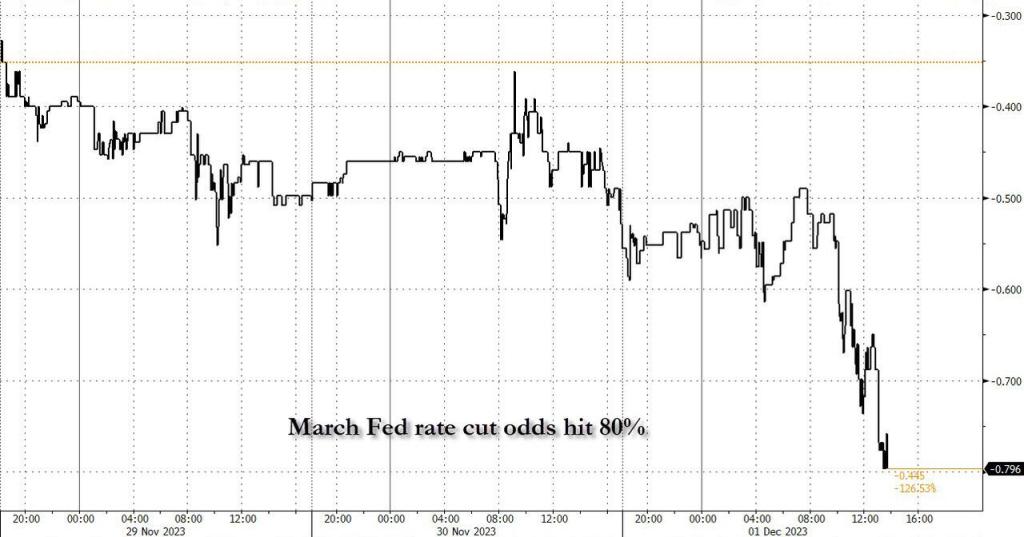

… it was the dot plot, where the median 2024 dot plot now forecasts 3 rate cuts up from 2, that shocked traders: in a very rare admission by the Fed, the central bank confirmed that the pre-meeting market pricing of multiple cuts in 2024 were correct in interpreting the Fed’s intentions. It also confirmed – yet again – that the market was right and every single FOMC member was wrong. In retrospect, none of this should have been a shock.

Commenting on the dot plot, TS Lombard’s Steven Blitz said that “for a group that prizes the pricing of its policy intentions in the forward markets as being more important to shifting market conditions than the spot rate, they h d to know that moving the median forecast for Fed funds at the end of 2024 back to June levels would be a bullish signal.“

Or maybe concerns about the market’s reaction were of secondary importance to a Fed which had gotten the tap on the shoulder by the Biden admin and its Democratic cronies on the Hill, terrified about their re-election chances now that the snake of Identity Politics is finally eating its poisonous tail. Indeed, almost as if having seen the collapse in the recent approval polls, Biden’s handlers made some very persuasive phone calls to the Fed. After all, only something as ridiculous – and serious – as steady political pressure can explain the unprecedented U-Turn by the Fed chair, one which even shocked Powell’s own mouthpiece, Nikileaks, who commented on the “Powell pivot” saying “what a difference two weeks can make.”

But markets are behaving as if The Fed will begin cutting rates. Look at the US 2-year Treasury yield on Wednesday AFTER the Fed minutes were released.

Bear in mind that mortgage rates are up 149% under Biden. And mortgage payments up 88%. Yikes!

Mortgage applications increased 7.4 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending December 8, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 7.4 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 6 percent compared with the previous week. The seasonally adjusted Purchase Index increased 4 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 18 percent lower than the same week one year ago.

The Refinance Index increased 19 percent from the previous week and was 27 percent higher than the same week one year ago.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($726,200 or less) decreased to 7.07 percent from 7.17 percent, with points decreasing to 0.59 from 0.60 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

And Freddie Mac’s 30-year mortgage rate is UP 165% under Biden.

Like WEF’s Klaus Schwab, Biden doesn’t want you to have a low rate mortgage for Christmas!

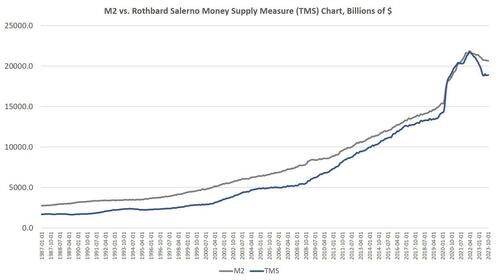

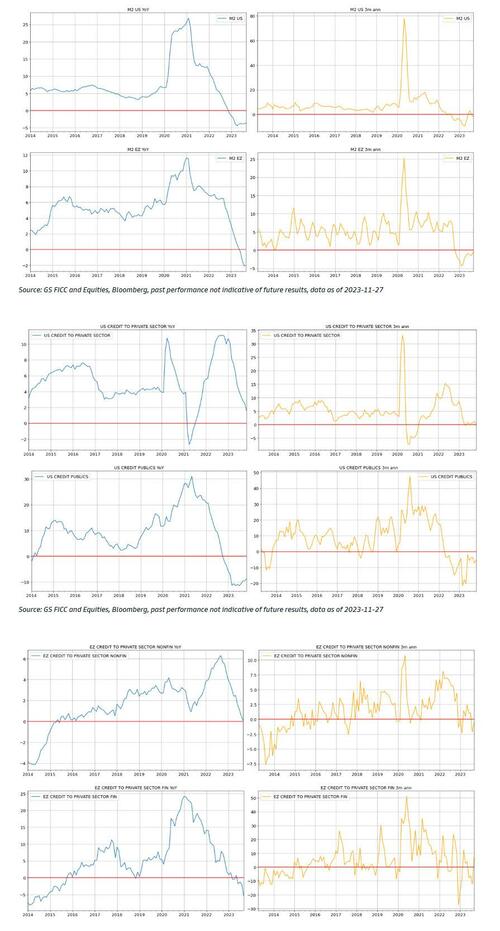

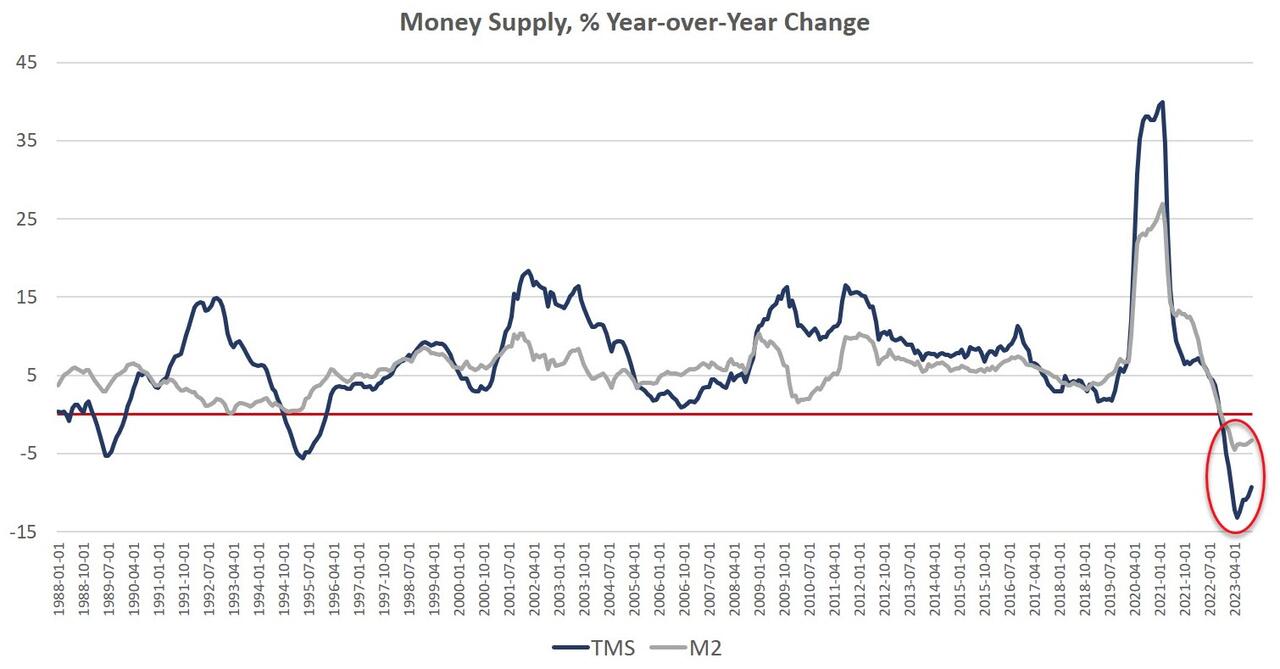

Since April 2021, money supply growth has slowed quickly, and since November, we’ve been seeing the money supply repeatedly contract year over year. The last time the year-over-year (YOY) change in the money supply slipped into negative territory was in November 1994. At that time, negative growth continued for fifteen months, finally turning positive again in January 1996.

Money-supply growth has now been negative for twelve months in a row. During October 2023, the downturn continued as YOY growth in the money supply was at –9.33 percent. That’s up slightly from September’s rate decline which was of –10.49 percent, and was far below October 2022’s rate of 2.14 percent. With negative growth now falling near or below –10 percent for the eighth month in a row, money-supply contraction is the largest we’ve seen since the Great Depression. Prior to this year, at no other point for at least sixty years has the money supply fallen by more than 6 percent (YoY) in any month.

The money supply metric used here—the “true,” or Rothbard-Salerno, money supply measure (TMS)—is the metric developed by Murray Rothbard and Joseph Salerno, and is designed to provide a better measure of money supply fluctuations than M2. (The Mises Institute now offers regular updates on this metric and its growth.)

In recent months, M2 growth rates have followed a similar course to TMS growth rates, although TMS has fallen faster than M2. In October 2023, the M2 growth rate was –3.35 percent. That’s down from September’s growth rate of –3.35 percent. October 2023’s growth rate was also well down from October 2022’s rate of 1.42 percent.

Money supply growth can often be a helpful measure of economic activity and an indicator of coming recessions. During periods of economic boom, money supply tends to grow quickly as commercial banks make more loans. Recessions, on the other hand, tend to be preceded by slowing rates of money supply growth.

It should be noted that the money supply does not need to actually contract to signal a recession and the boom-bust cycle. As shown by Ludwig von Mises, recessions are often preceded by a mere slowing in money supply growth. But the drop into negative territory we’ve seen in recent months does help illustrate just how far and how rapidly money supply growth has fallen. That is generally a red flag for economic growth and employment.

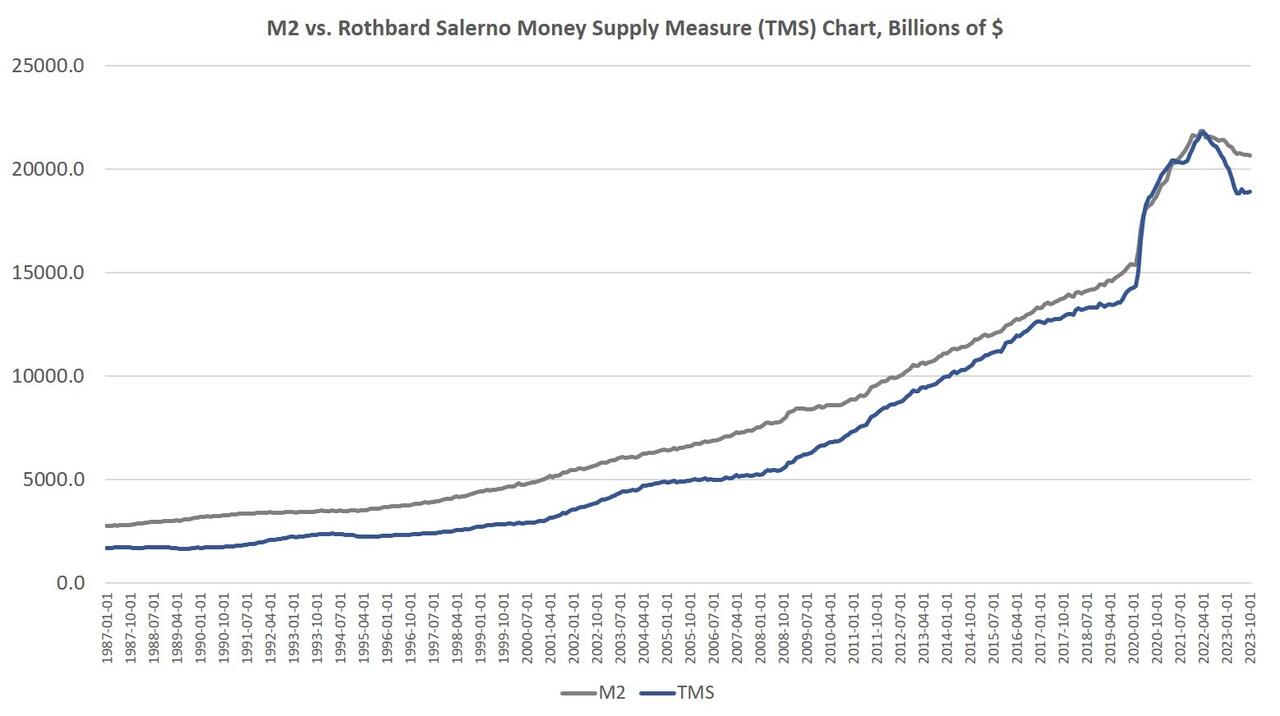

The fact that the money supply is shrinking at all is remarkable because the money supply in modern times almost never gets smaller. The money supply has now fallen by $2.8 trillion (or 13.1 percent) since the peak in April 2022. Proportionally, the drop in money supply since 2022 is the largest fall we’ve seen since the Depression. (Rothbard estimates that in the lead-up to the Great Depression, the money supply fell by 12 percent from its peak of $73 billion in mid-1929 to $64 billion at the end of 1932.)

In spite of this recent drop in total money supply, the trend in money-supply remains well above what existed during the twenty-year period from 1989 to 2009. To return to this trend, the money supply would have to drop at least another $3 trillion or so—or 15 percent—down to a total below $15 trillion. Moreover, as of October, total money supply was still up 32 percent (or $4.6 trillion) since January 2020.

Since 2009, the TMS money supply is now up by nearly 186 percent. (M2 has grown by 141 percent in that period.) Out of the current money supply of $18.9 trillion, $4.6 trillion—or 24 percent—of that has been created since January 2020. Since 2009, $12.2 trillion of the current money supply has been created. In other words, nearly two-thirds of the total existing money supply have been created just in the past thirteen years.

With these kinds of totals, a ten-percent drop only puts a small dent in the huge edifice of newly created money. The US economy still faces a very large monetary overhang from the past several years, and this is partly why after eighteen months of slowing money-supply growth, we are only now starting to see a slowdown in the labor market. (For example, job openings have fallen 22 percent over the past year, but have not yet returned to pre-covid levels.) The inflationary boom has not yet ended.

Nonetheless, the monetary slowdown has been sufficient to considerably weaken the economy. The Philadelphia Fed’s manufacturing index is in recession territory. The Leading Indicators index keeps looking worse. The yield curve points to recession. Temp jobs were down, year-over-year, which often indicates approaching recession. Default rates are rising.

Money Supply and Rising Interest Rates

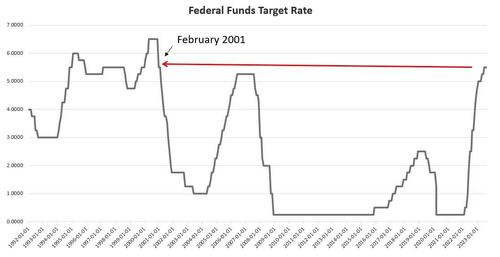

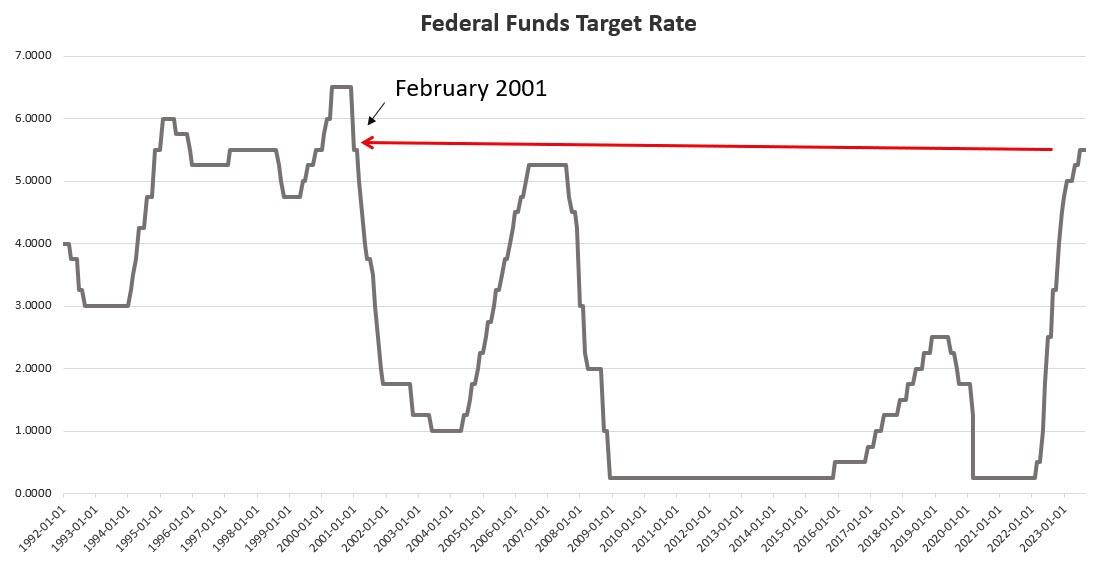

An inflationary boom begins to turn to bust once new injections of money subside, and we are seeing this now. Not surprisingly, the current signs of malaise come after the Federal Reserve finally pulled its foot slightly off the money-creation accelerator after more than a decade of quantitative easing, financial repression, and a general devotion to easy money. As of early December, the Fed has allowed the federal funds rate to rise to 5.50 percent, the highest since 2001. This has meant short-term interest rates overall have risen as well. In October, for example, the yield on 3-month Treasurys reached 5.6 percent, the highest level measured since December 2000.

Without ongoing access to easy money at near-zero rates, banks are less enthusiastic about making loans, and many marginal companies will no longer be able to stave off financial trouble by refinancing or taking out new loans. Commercial bankruptcy filings increased sizably during 2023, and continue to surge into the last quarter of the year. As reported by Monitor Daily:

The bankruptcy filing by WeWork in November propelled November commercial Chapter 11 filings to 842, an increase of 141% compared with the 349 filings registered in November 2022, according to data provided by Epiq Bankruptcy.

The case filed by WeWork on Nov. 6 included 517 related filings, according to analysis from the American Bankruptcy Institute, representing the third-most related filings in a case since the U.S. Bankruptcy Code became effective in 1979.

Overall commercial filings increased 21% to 2,252 in November, up from the 1,864 commercial filings registered in November 2022. Small business filings, captured as Subchapter V elections within Chapter 11, increased 79% to 181 in November, up from 101 in November 2022.

There were 37,860 total bankruptcy filings in November, a 21% increase from the November 2022 total of 31,187. Individual bankruptcy filings also registered a 21% year-over-year increase, as the 35,608 in November represented an increase over the 29,323 filings in November 2022. There were 20,250 individual Chapter 7 filings in November, a 23% increase compared with the 16,421 filings recorded in November 2022, and there were 15,280 individual Chapter 13 filings in November, a 19% increase compared with the 12,862 filings last November.

Lending for private consumption is getting more expensive also. In October, the average 30-year mortgage rate rose to 7.62 percent, the highest point reached since November 2000.

These factors all point toward a bubble that is in the process of popping. The situation is unsustainable, yet the Fed cannot change course without reigniting a new surge in price inflation. Although some professional economists insist that price inflation has all but disappeared, the sentiment on the ground is clearly one in which most workers believe their wages are not keeping up with rising prices. Any surge in prices would be especially problematic given the rising cost of living. Ordinary Americans face a similar problem with home prices. According to the Atlanta Fed, the housing affordability index is now the worst it’s been since 2006, in the midst of the Housing Bubble.

If the Fed reverses course now, and embraces a new flood of new money, prices will only spiral upward. It didn’t have to be this way, but ordinary people are now paying the price for a decade of easy money cheered by Wall Street and the profligates in Washington. The only way to put the economy on a more stable long-term path is for the Fed to stop pumping new money into the economy. That means a falling money supply and popping economic bubbles.

But it also lays the groundwork for a real economy – i.e., an economy not built on endless bubbles – built by saving and investment rather than spending made possible by artificially low interest rates and easy money.

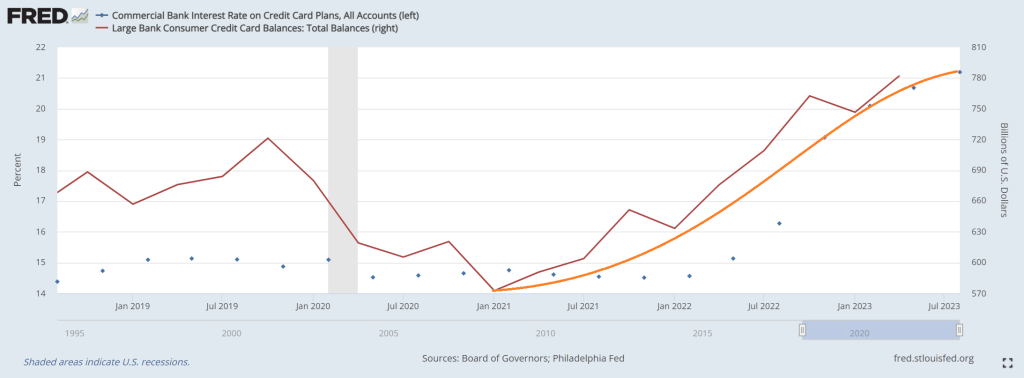

Then we have US consumers, attempting to cope with Biden’s inflation, by paying all-time highs on credit cards while trying to service ever-growing credit card balances.

You might as well face it, markets are “addicted to gov.” Government monetary interference, that is. Government money printing and massive Federal spending.

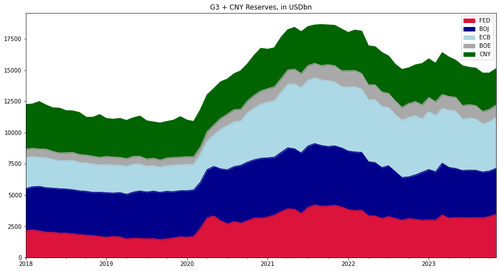

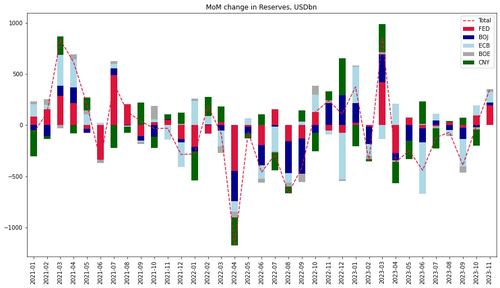

According to Goldman calculations, $350BN of liquidity (in USD terms) was added in November from the G4 central banks + the PBOC was nothing short of a fire hose.

In fact, this was the third largest monthly increase this year after January and March 2023.

The US addition of $60bn for a third consecutive week plus weaker dollar are the main drivers.

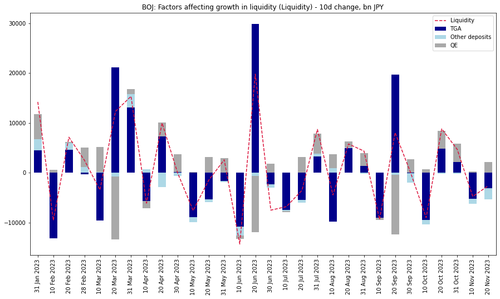

While the BoJ keeps adding liquidity via bond purchases, increases in the TGA balances in the past 20 days have net drained Yen liquidity.

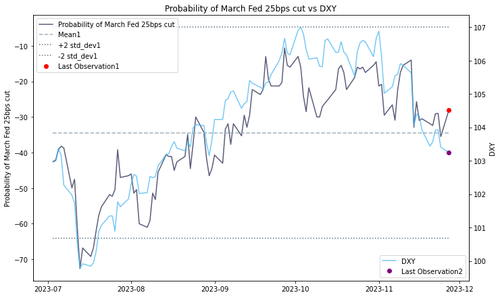

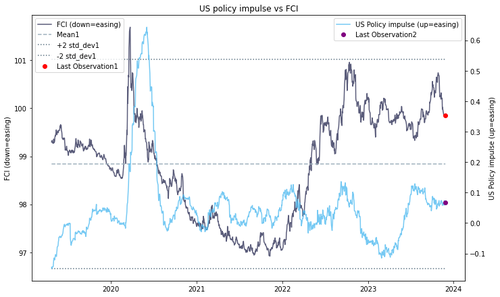

Looking forward over the year end and at the start of 2024, Goldman thinks that the US can keep adding liquidity via high bill issuance and RRP withdrawal over the next couple of months (something we discussed last month in “How Treasury Averted A Bond Market “Earthquake” In The Last Second: What Everyone Missed In The TBAC’s Remarkable Refunding Presentation“), while the dollar contribution to benign liquidity conditions could face some headwinds due to the risk of pricing out of some of the March Fed cuts as a result of the strong positive FCI impulse in November.

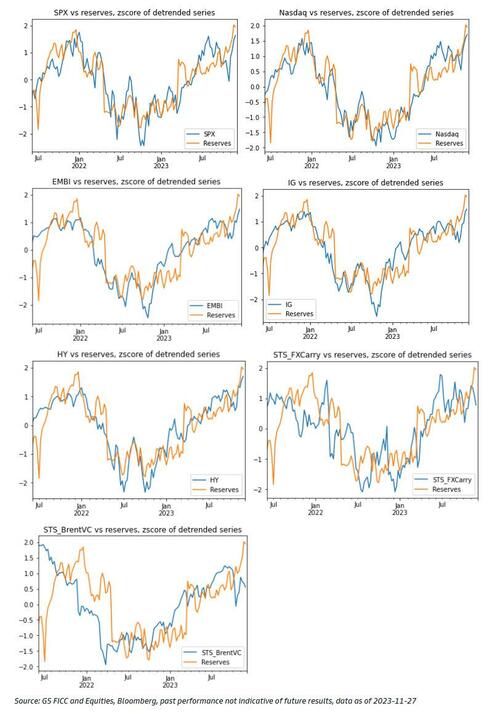

Goldman’s one-factor model for risky assets based on the liquidity cycle suggests that US IG and EM hard currency debt are cheap and the bank’s STS FX carry and Brent Vol Carry indices have under-performed the benign liquidity environment and may catch up the next two months.

The US and Eurozone money supply and lending growth indicators remain weak, implying extended downside bias in domestic demand and inflation in H1-2024 (i.e., higher likelihood for easing absent a reflationary shock out of China or a supply-driven commodity price surge).

Finally, The US policy impulse (comprising of liquidity, fiscal stance, as well as nominal and real forward rates) has moved sideways in October and November after some renewed tightening in September. The GS FCI index eased nearly -100 basis points (-1.4z) in November.

Doctor, doctor (Yellen), we got a bad case of distortionomics (where the 1% wins and the 99% fall behind). After all, under Dr. Yellen as our Treasury Secretary, we are suffering from massive fiscal inferno with wild government spending. I would use “Government Gone Wild!” but the thought of Yellen … well, never mind.

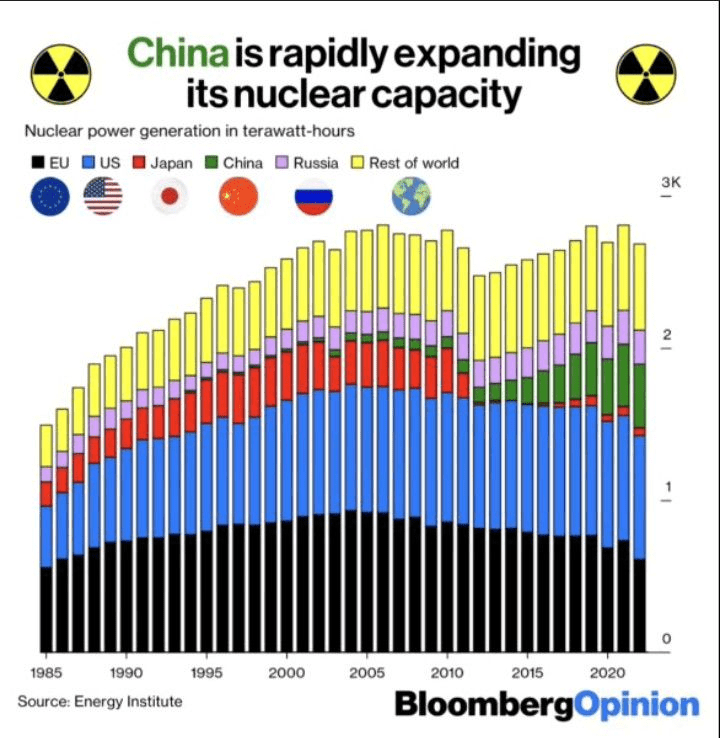

Meanwhile, while John Kerry pushes for ending ALL coal powered plants (good luck charging the thousands of EV charging stations on wind/solar power!), China is building NUCLEAR plants. While US green wimps (Kerry comes to mind) whine whenever nuclear plants are mentioned for the US.

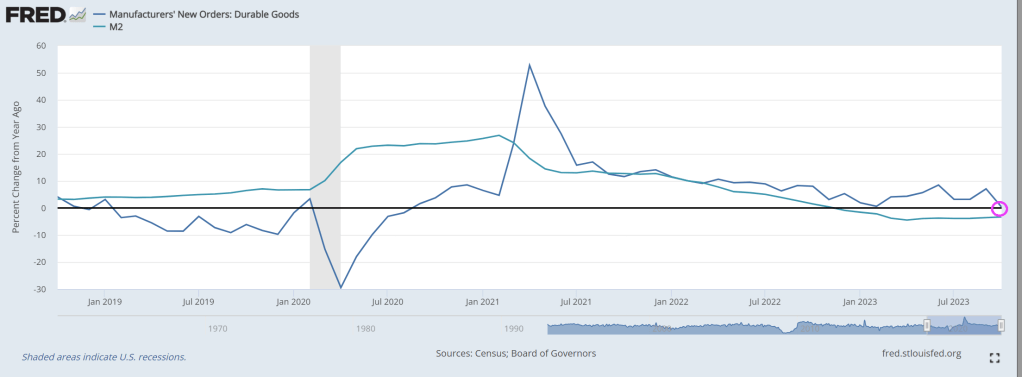

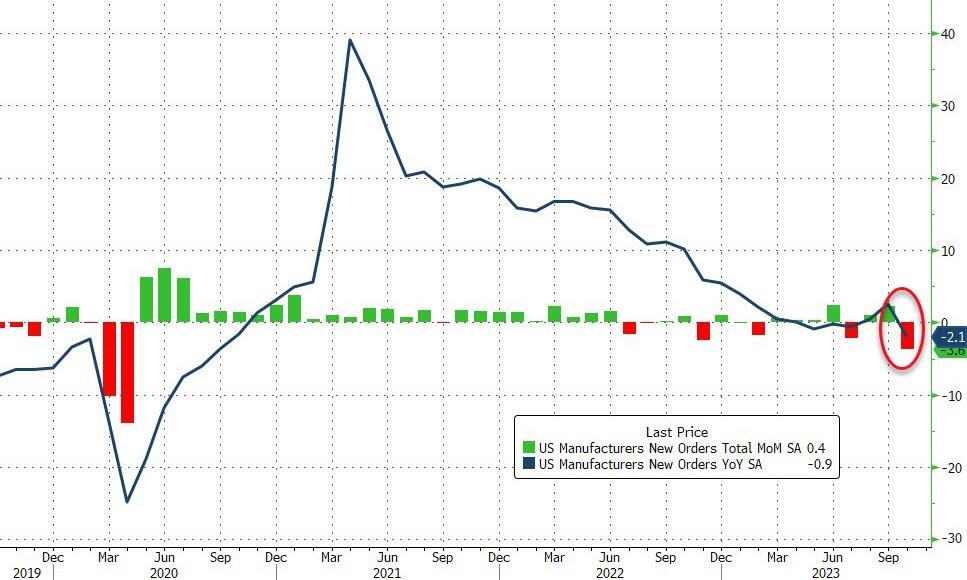

Factory orders tumbled even more than expected, down 3.6% MoM – the biggest drop since the COVID lockdowns (April 2020). September was also revised lower (making October’s decline even worse) from +2.8% MoM to +2.3% MoM…

Source: Bloomberg

The big monthly decline and revisions dragged orders down 2.1% YoY (the biggest drop since Sept 2020).

Core factory orders also dropped (-1.2% Mom), leaving them down 2.2% YoY – the eight month in a row of annual declines…

Source: Bloomberg

The final Durable Goods Orders data for October confirmed the preliminary print plunge down 5.4% MoM.

Finally, we note that it could have been a lot worse as Defense spending shot up 24.7% MoM (as non-defense dropped 15.8% MoM0…

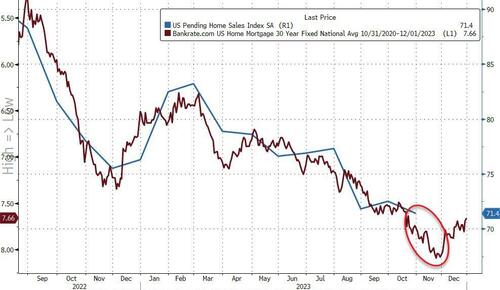

The US housing and mortgage markets are thunderstruck by The Fed’s attempts at cooling inflation down to 2%.

After a small bounce last month – following the puke in August – pending home sales dropped 1.5% MoM in October (better than the 2.0% MoM decline expected). This left YoY sales down 6.6% (negative for the 23rd straight month)…

Source: Bloomberg

The Pending Home Sales Index dropped back to a new record low…

Source: Bloomberg

By region, only the Northeast saw an increase in pending sales last month.

Sales fell the most in the West, down 6%, while contract signings in the South and Midwest slipped 1.9% and 0.4%, respectively.

Home sales are rising in places with more inventory, Lawrence Yun, NAR’s chief economist said, noting that purchases of new houses are up so far this year because of builders’ ability to create inventory.

“During October, mortgage rates were at their highest, and contract signings for existing homes were at their lowest in more than 20 years,” Yun said in a statement.

“Recent weeks’ successive declines in mortgage rates will help qualify more home buyers, but limited housing inventory is significantly preventing housing demand from fully being satisfied.”

The trend in pending home sales is following the mortgage rate (with a one month lag) and is set to fall further still…

Source: Bloomberg

The pending-home sales report is a leading indicator of existing-home sales given houses typically go under contract a month or two before they’re sold.

How long with Powell and his pals be able to keep this ‘higher for longer’ stress up as Americans’ largest source of wealth evaporates?

Mortgage rates have fallen recently, but are still up a staggering 156% under Biden.

And mortgage purchase applications keep falling.

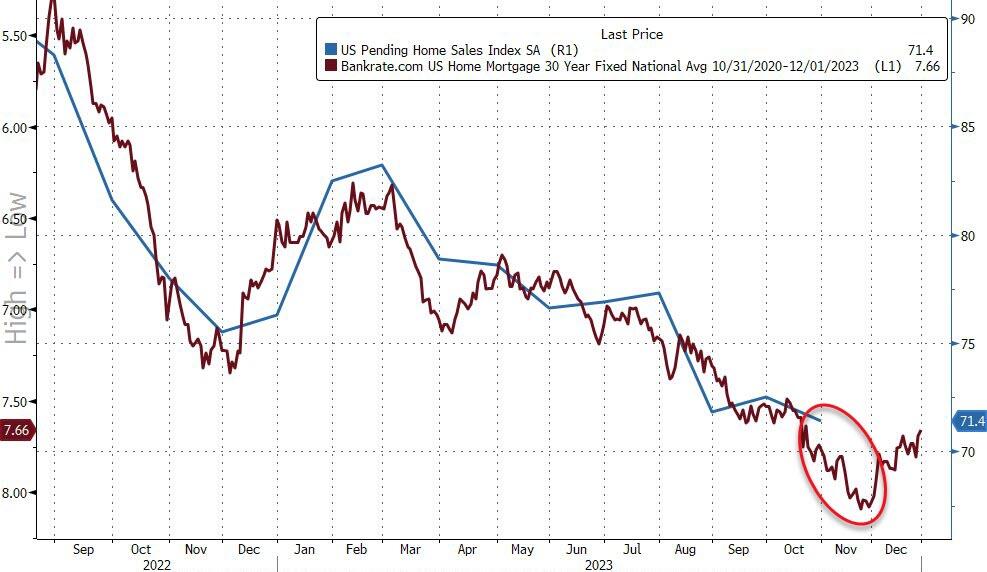

Here is The Fed keeping a close eye on the housing and mortgage market.

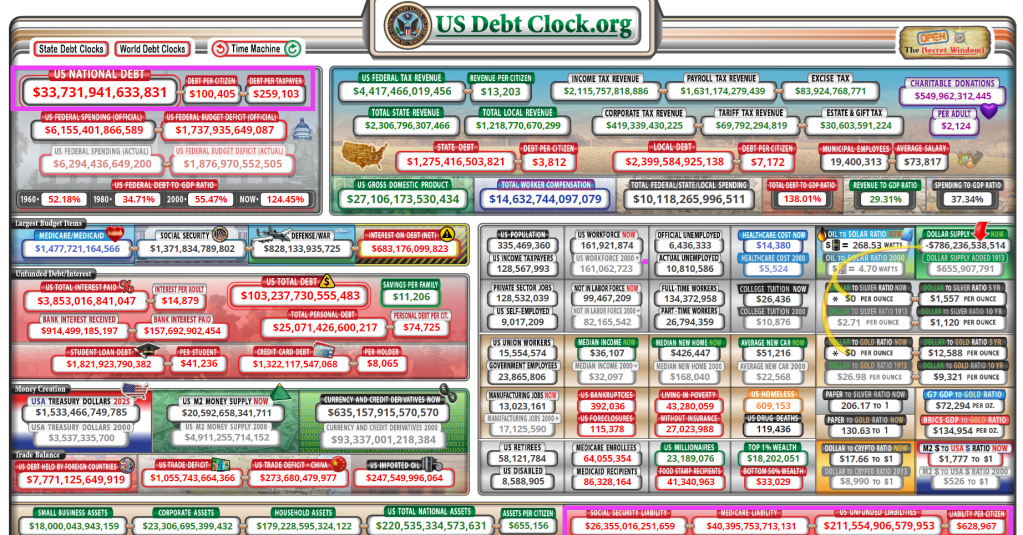

In fact, Congress and the Biden (mis) Administration are spending like the proverbial drunk sailors in port. US national debt is up to $33.7 TRILLION. That transates to $259,103 per taxpayer. With US debt to GDP of 138%!

Now, HERE IS THE REAL BAD NEWS! Unfunded promises that politicians made to Americans (Social Security, Medicare, Medicaid, etc.) now stands at $211.6 TRILLION. That equates to $629,000 per citizen. Maybe that should be the deal at the southern border: all immigrants must pay $629,000 for admission!

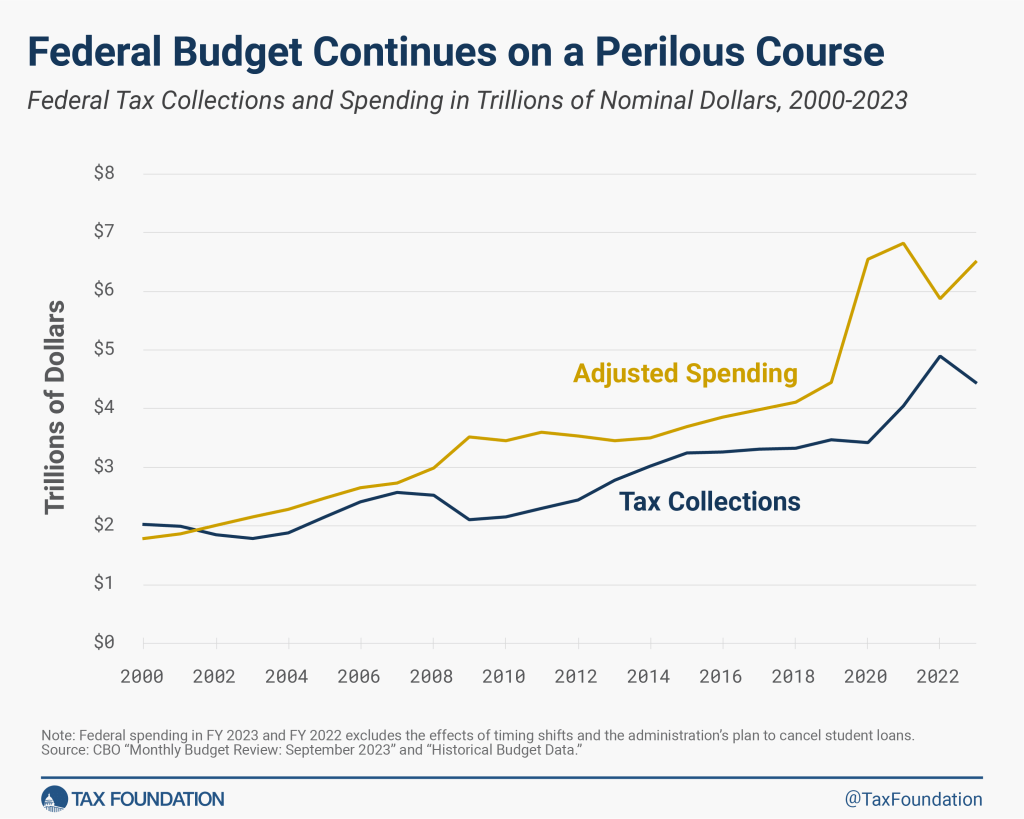

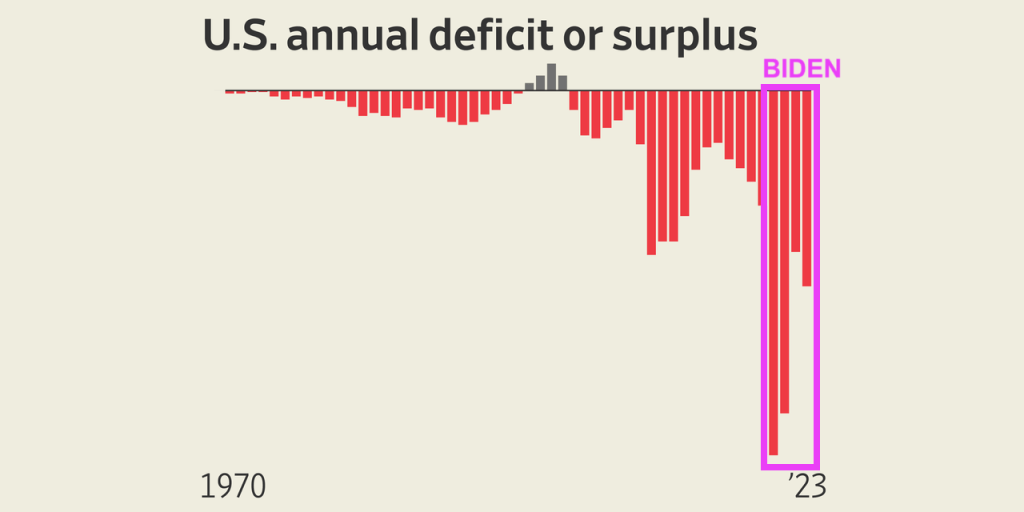

And the Federal budget deficit keeps on getting worse.

The budget deficits under Biden/Yellen have been the worst in history. So much for Biden whispering “Bidenomics is working!”

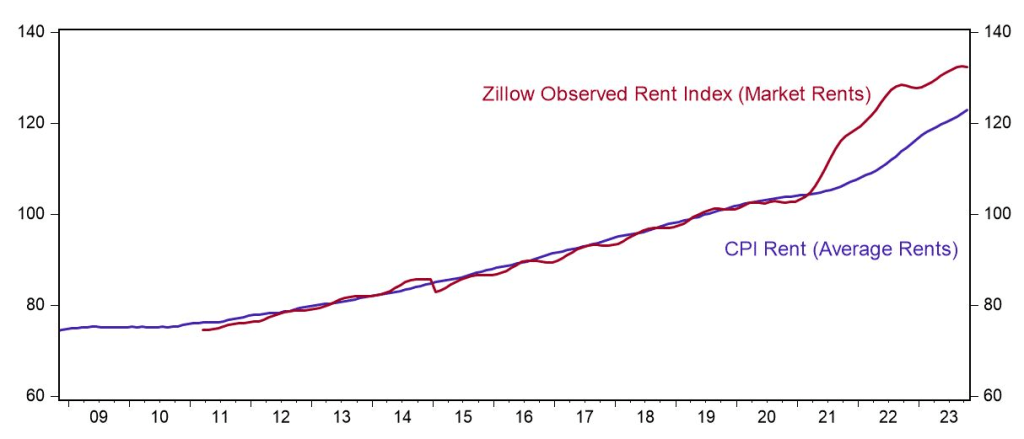

Rents in the US remain unaffordable to many.

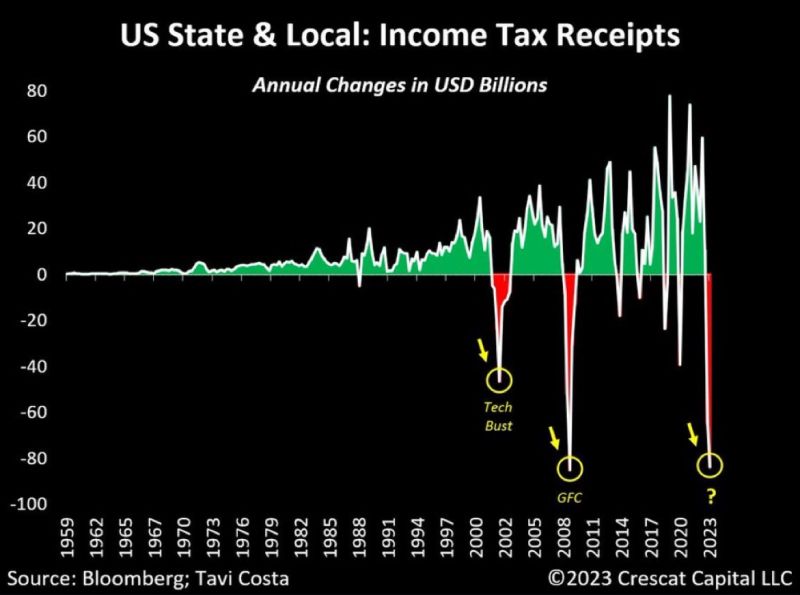

And Yellen, our nation’s financial consigliari, hasn’t said much about the dire decline in income tax receipts.

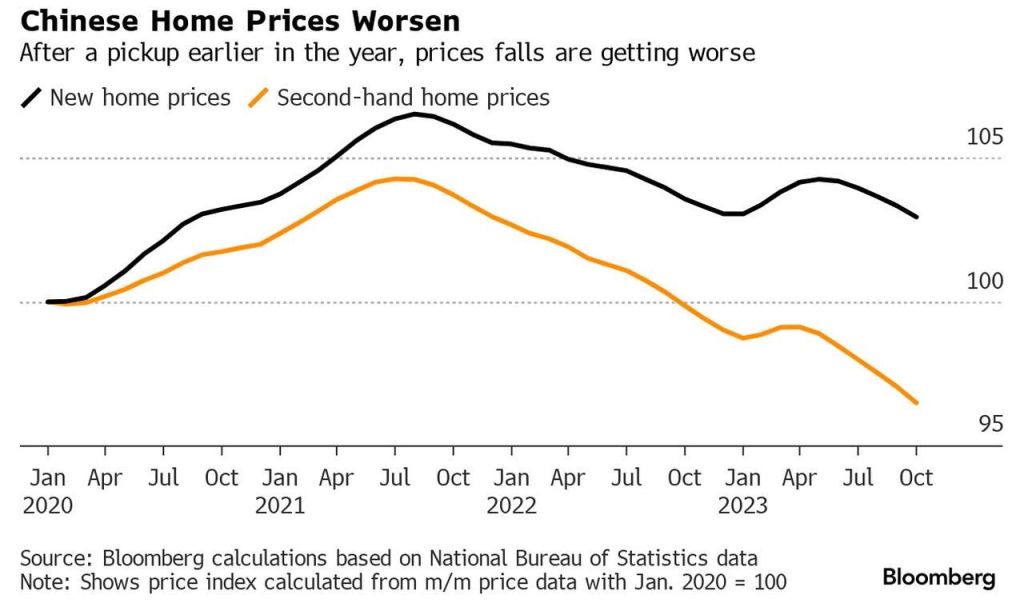

But Biden’s favorite country China, a classic top-down command economy like Biden and Yellen love,

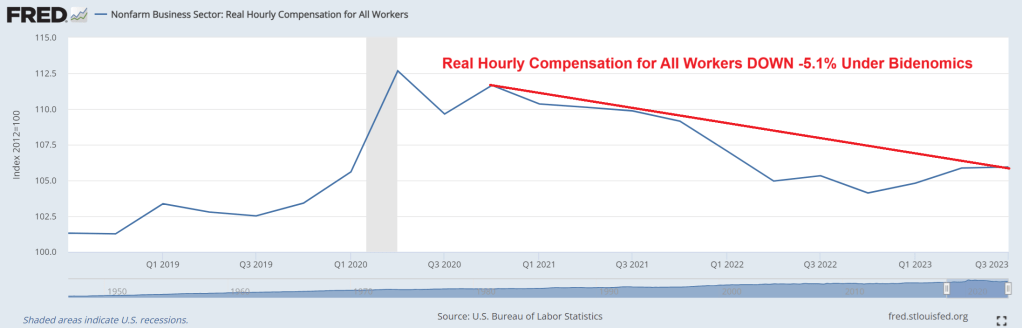

On Sunday, President Joe Biden tweeted, “Right now, real wages for the average American worker is higher than it was before the pandemic, with lower wage workers seeing the largest gains. That’s Bidenomics.” That’s right, Joe! Except real hourly compensation has DECLINED by -5.1% under Biden.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.