Inflation is stubborn because “goin’ green!” by 1) restricting US fossil fuel production and exploration and 2) Biden/Congress endless spending splurge since Covid. So, The Federal Reserve has a tough problem: cooling inflation while US energy prices are up 54% under Biden. And those higher energy prices have percolated through the entire economy in terms of food prices and heating prices.

Where do we sit? The US Treasury 10yr-2yr yield curve remains inverted (a sign of impending recession). Mortgage rates are the highest in 14 years as The Fed tightens.

If we look at Fed Funds Futures data, we can see that traders expect The Fed’s target rate to rise to 4.395% by March 2023’s FOMC meeting. Then traders expect The Fed to take their enormous foot off the tightening pedal.

Yes, inflation is crushing the middle class and low-wage workers. Average hourly earnings YoY after we subtract inflation are negative.

Taylor Rule? Currently, the Taylor Rule based on Core inflation of 4.56% YoY suggests a Fed target rate of 9.14%. Since traders anticipate the target rate to peak at 4.395%, The Fed will almost be halfway towards cooling inflation.

The problem is … Fed Chair Powell and Treasury Secretary Yellen don’t like rules limiting their “power.” Powell and Yellen think the Taylor Rule is a New Jersey ham product.

Raging US inflation is resulting in Federal Reserve monetary tightening, causing the 30-year US mortgage rate to hit it highest level since November 2008 (the beginning of Fed Quantitative Easing). Bankrate’s 30-year mortgage rate just hit 6.28%, the highest rate in 14 years.

The Biden Administration will be remembered for crippling inflation, the highest in 40 years AND the highest mortgage rate in 14 years.

And with Fed chatter about hiking rates, Dr T (me) predicts pain for the mortgage market.

Freddie Mac’s 30-year mortgage commitment rate just rose to its highest level since … The Fed initiated Quantitative Easing (aka, fanatical money printing) during the financial crisis.

The good news? The US inflation report is likely to show a slowing of the inflation rate to around 8% YoY and -0.1% MoM. Why? Gasoline prices are cooling thanks to the global economic slowdown.

While gasoline and food prices are falling, CORE US inflation, the inflation rate excluding food and energy, is expected to rise to around 6.1% YoY and +0.30% for August.

As inflation burns the US middle class and low wage workers, The Federal Reserve reaffirmed at Jackson Hole that they are the NEW Smoky The Bear (only The Fed can fight inflation fire!) But of course, Federal spending and energy policies can drive up prices too.

Having said that, the 2-year Treasury yield and 30yr mortgage rate are rising rapidly.

The Fed is trying to cool demand by raising rates after lax monetary policy since late 2008.

While the US 2-year Treasury yield is up only slightly today, the Eurozone is seeing their 2-year sovereign yields spiking by 11-15+%.

Biden is the opposite of the miserly Scrooge McDuck. He gives billions to Ukraine and spends trillions on various Federal projects without batting an eye as to how and who is going to pay for all the spending. And Biden’s latest election pandering is no different.

Speaker Pelosi claims that Biden’s bold action on student loan forgiveness is a strong step in Democrats’ fight to … make college even MORE expensive and lead to colleges hiring even MORE administrators (aka, apparatchiks) making colleges even MORE bogged-down in red tape.

And Speaker Pelosi, the costs of Biden’s midterm election buy of votes is estimated to be $300 BILLION. And a report from the Brookings Institution observed that one-third of student debt is owed by the wealthiest 20% of households, while only 8% is owned by the bottom 20%.

So, Biden is letting AOC write-off $10k of her student loan obligation. Bear in mind that the $10k forgiveness is taxed by The Federal government as income.

It looks like The Fed will have to expand the M2 Money supply to pay for “Billions Biden’s” spending spree.

US mortgage applications just hit the lowest levels in 22 years, January 2000 as The Federal Reserve continues monetary tightening to combat Bidenflation.

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 19, 2022. The Refinance Index decreased 3 percent from the previous week and was 83 percent lower than the same week one year ago.The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 21 percent lower than the same week one year ago.

MBA mortgage applications just declined to their lowest level in 22 years (January 2000) as The Fed has begun raising rates to fight inflation caused by 1) excessive monetary stimulus since late 2008, 2) Biden’s green energy policies driving up transportation costs, 3) distortionary Federal spending (e.g., Covid relief, infrastructure bills and now green energy/IRS spending by Biden/Pelosi/Schumer).

Here is the data summary for the latest MBA applications report.

Fed Chair Jerome Powell shrinking The Fed’s balance sheet.

The National Association of Realtors’ Homebuyer Affordability Index for fixed-rate mortgages is now at the lowest reading since 2006 and the peak of the 2005-2007 housing bubble that burst catastrophically.

The reason? The Federal Reserve, in their attempt to put out the inflation fire (caused by 1) excessive monetary stimulus since late 2008, 2) rampant Federal spending and 3) Biden’s green energy policies, driving up prices.

If we compare mortgage rates with the US Treasury 10Y-2Y yield curve, you can see that the yield curve remains inverted (historically a bad sign). This may signal an eventual loosening of monetary policy by March 2023.

Dear Mr. Fantasy, play us a tune, something to make us all happy (like hitting 2% inflation WITHOUT crashing the economy). Do anything take us out of this gloom (caused by The Fed, Biden’s energy policies and Federal spending). Sing a song, play guitar, Make it snappy. Or in the case of housing, make it crappy.

(Bloomberg) — Federal Reserve Bank of Richmond President Thomas Barkin said the central bank was resolved to curb red-hot inflation, even if that meant risking a US economic recession.

“We’re committed to returning inflation to our 2% target and we’ll do what it takes to get there,” Barkin said Friday during an event in Ocean City, Maryland. He said that this could be achieved without a “tremendous decline in activity” but acknowledged that there were risks.

“There’s a path to getting inflation under control but a recession could happen in the process,” he said.

The US central bank hiked interest rates by 75 basis points in July for the second straight month as policy makers tackle inflation that’s running near 40-year highs. Fed officials speaking in recent days have said more rate increases are needed, but they are still deciding how big to move at their next policy meeting.

St. Louis Fed President James Bullard, one of the most hawkish policy makers, on Thursday urged another 75 basis-point move while Kansas City’s Esther George struck a more cautious tone.

Well, The Fed (aka, Der Kommissars) let the monetary stimulus blow out of control since 2000.

With the 2001 recession, The Fed crashed the target rate (white line) causing home price growth (blue line) to soar. Then The Fed decided that the economy was overheated and cranked up their target rate. This sudden rise in The Fed’s target rate helped to slow/crash housing prices. Resulting in … a frantic decrease in the target rate (late 2007- late 2008) and the adoption of asset purchases of Treasury Notes/Bonds and Agency Mortgage-backed Securities in late 2008.

The Bernanke/Yellen “loose as a goose” policies from late 2008 to Feb 2018 created a total mess. Bernanke/Yellen raised the target rate only one before Trump was elected President, and 8 times AFTER Trump was elected. And Yellen’s Fed began to let the balance sheet shrink a bit before Covid struck in early 2020. And with Covid came another massive expansion of The Fed’s Balance Sheet WHICH HAS NOT YET BEEN WITHDRAWN (despite Fed talking heads saying it would be reduced).

Here we sit with The Fed NOW trying to extinguish inflation (yellow line) by raising their target rate (white line) but NOT shrinking the balance sheet (orange line).

Wonder why this is a horrible homeless problem in the US, particularly in California? While Stanford University has an excellent study of the causes of California’s homeless problem, there is another cause of homelessness … The Federal Reserve’s insane monetary policies since late 2008. The Case-Shiller National Home Price Index is 65% higher in May than during the calamitous home price bubble of 2005-2007, helping to exacerbate the homeless problem.

One of the many problems created by the reckless Bernanke/Yellen/Powell monetary policies is the M2 Money Velocity is near an all-time low making a return to “easy money policies” far more difficult.

I won’t post any photos of the homeless encampments in Los Angeles since it is very sad. But here is a photo of the Dunder-Mifflin paper company “office” on Saticoy Street. The point is that thanks to The Federal Reserve’s loose monetary policies, housing is unaffordable for millions of households forcing many to live on the streets.

Figure 2: Median Rent for a Two-Bedroom Apartment, California, 2022

And a point of trivia. The Office’s Charles Miner (played by the GREAT Idris Elba) was allegedly hired from Saticoy Steel. The Dunder-Mifflin paper company site was on Saticoy Street in sunny LA, not Scranton PA.

Good luck to The Federal Reserve in combating inflation without causing a recession.

The 2020 Covid outbreak led to a massive (and generally awful) reaction. There were economic shutdowns that caused extensive damage (particularly to small firms), but it was the massive overreaction by The Federal government in terms of Covid relief and The Federal Reserve’s expansion of the money supply that caused considerable damage.

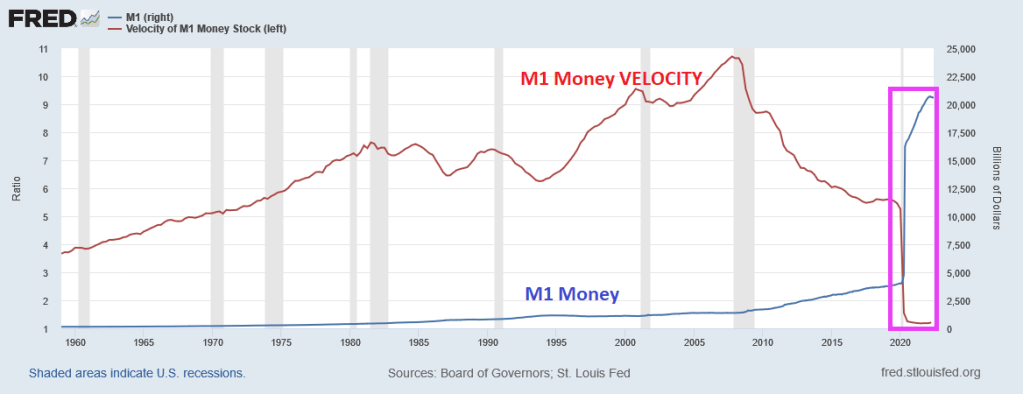

One truly horrific chart is that of M1 Money and M1 Money Velocity (M1/GDP). M1 Money surged with Covid driving M1 Money Velocity down to levels never seem before.

The broader measure of money, M2, isn’t as dramatic, but we also see that M2 Money VELOCITY has plunged to levels never seen before.

What does low money velocity indicate? Simply put, The Fed is printing trillions of dollars, but GDP isn’t moving much. But that won’t stop Congress from spending (and using The Fed to buy its debt).

So, here we sit. This morning, the US Treasury yield curve (10Y-2Y) remains inverted. This AM, the curve inverted another -.591 basis points to -42.725, a sign of impending recession.

Yes, we are living through Jay Powell’s famous chili episode where money velocity is near historic lows and we have an inverted yield curve.

BTW, congratulations to Will Zalatoris (aka, Happy Gilmore’s caddy) for his first PGA Tour victory at the FedEx St. Jude Championship!

Agency mortgage-backed securities (MBS) prices started to degrade as The Federal Reserve started to try to combat inflation caused by Biden’s energy policies and rampant Federal spending. That is, under June when the implied Fed O/N rate (red line) cooled and the 30-year mortgage rate (blue line) has come down a little.

In terms of duration risk, the FNCL 3% MBS duration has risen with anticipated Fed tightening.

So, further Fed tightening will result in greater MBS losses AND rising duration risk.

You must be logged in to post a comment.