We are truly addicted to gov! Or at least cheap money from The Federal Reserve.

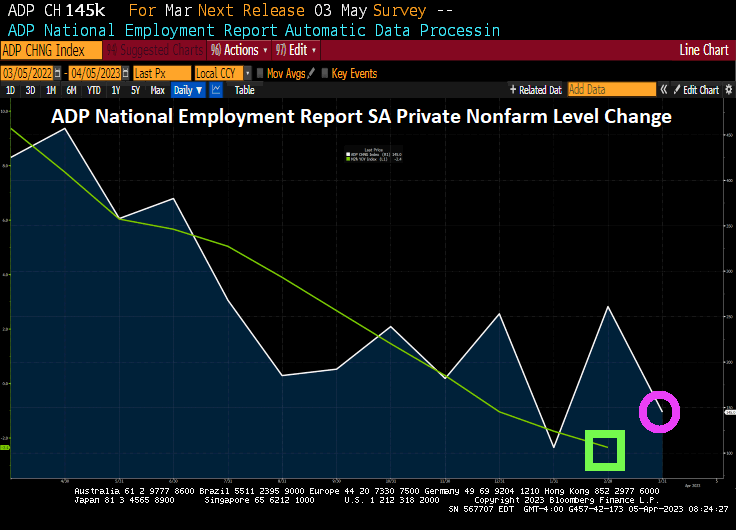

March’s ADP job report shows the US economy only added 145k jobs as The Fed removes its punch bowl. For the moment.

Its simply irresistable for the government to turn back on the printing press.

And then we have domestic banks reporting stronger demand for C&I Loans and real estate loan (for construction and development purposes) slumping to financial crisis lows.

Thanks to Yellen’s catestrophic Too-Low-For-Too-Long (TLFTL) and insane Federal spending, we are seeing the aftermath of The Fed trying to fight inflation. A fire sale of failed bank assets!!

With interest rates still rising, prices retreating and credit evaporating—and a stressed-out banking system moving to shore up balance sheets—expect more fire sales of older CMBS loans and an acceleration of plunging CRE values in markets across the US.

Last month, a fire sale of CMBS loans was lit as $72B in assets from the failed Silicon Valley Bank (SVB) were sold. The SVB assets—including about $13B in real estate exposure and at least $2.6B worth of CRE loans—were sold at a discount of $16.5B, which translates into about 77 cents on the dollar, according to a report in MarketWatch.

The Federal Deposit Insurance Corp. has lit a fuse on an even larger fire sale of assets—a bonfire in terms of CRE loans—for NYC-based Signature Bank, which like SVB was a regional bank that collapsed and was taken over by regulators last month.

FDIC last week tapped Newmark to sell $60B in assets held by Signature, according to the Wall Street Journal, including nearly $36B in CMBS loans backed primarily by multifamily properties, the lion’s share of them in New York City. Since 2020, Signature initiated more than $13.4B in loans backed by NYC buildings, the most of any lender.

Experts who specialize in pricing CRE loans believe a discounted sale as large as the disposal of Signature’s assets will speed a markdown of valuations by banks who until recently have been reluctant to set off a downward spiral. The 77 cents on the dollar benchmark established by the SVB sale likely will be the top end of where prices are heading, the experts say.

“The SVB trade created a baseline for the market. To me, that’s the top end, not the bottom end, for CRE loans,” David Blatt, CEO of CapStack Partners, told MarketWatch. CapStack is a credit fund that buys CMBS loans from banks and originates short-term bridge loans and mezzanine debt.

“What everybody has been operating under is this hold-to-maturity veneer,” Blatt said, referring to banks that have continued to value loans at 100 cents on the dollar, known as par.

In the wake of the SVB asset sale, “there’s just no way these things get resolved at par,” Blatt said, adding “the write-down is kind of implied.”

“Everybody is dusting off their old playbook. There just hasn’t been [as] much distress for years,” Jack Mullen, founder of Summer Street Advisors, told Marketwatch. “People are not going to let it carry into next year. On the regulatory side, it’s coming to the front of the line. People are super-mindful about it.”

The rising cost of debt was cutting into the value of older, low-coupon loans before SVB and Signature were shut down. Now, everyone is guessing how low will prices go on CMBS loans in the wake of the fire sales of the fallen lenders’ portfolios.

A recent advisory from Cohen & Steers estimates the decline in values will likely be at least 25%. Loans associated with multifamily properties won’t be immune from the valuation hit; apartment rents declined for the fifth time in six months from January to February.

For office properties, especially in Manhattan, the decline in value will be much steeper. Older NYC office properties are facing a cliff-diving plunge of up to 70%.

CMBX S15 is plummeting like a paralyzed falcon after The Fed started raising rates.

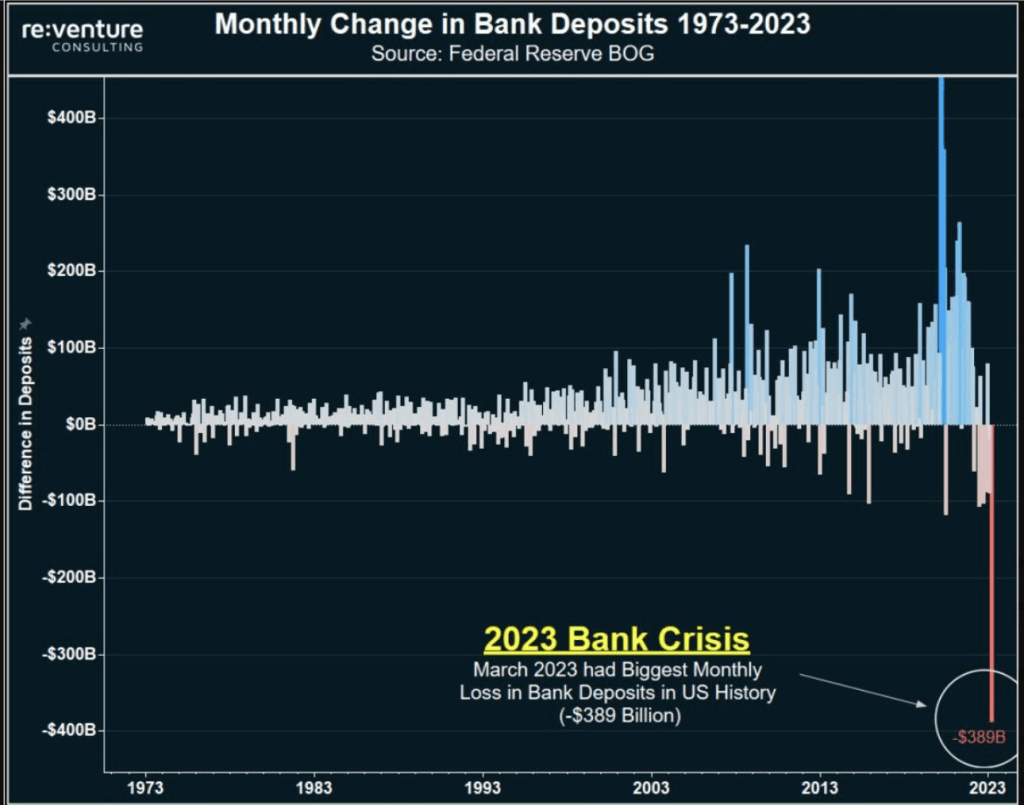

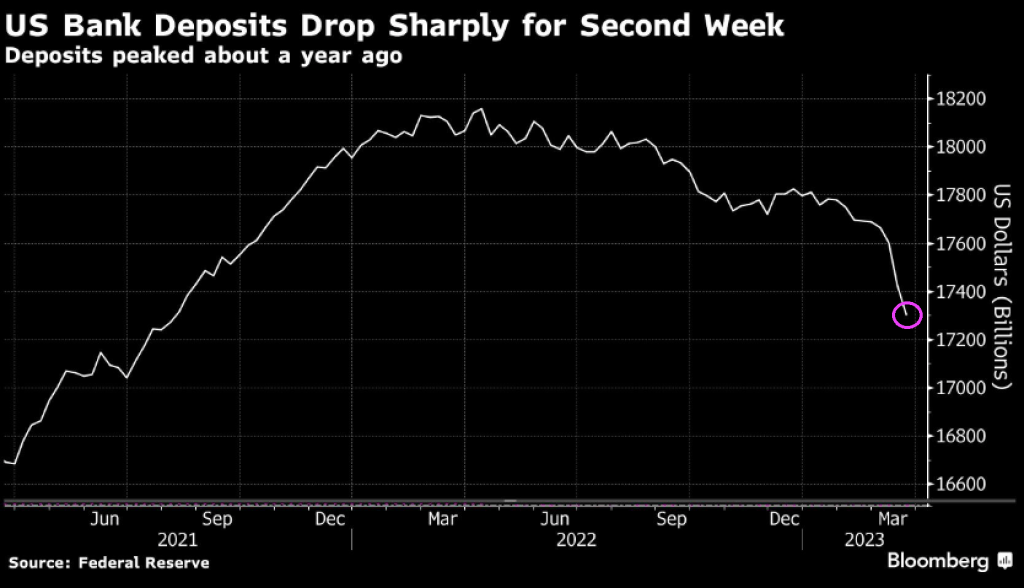

As bank deposits continue to crash and burn.

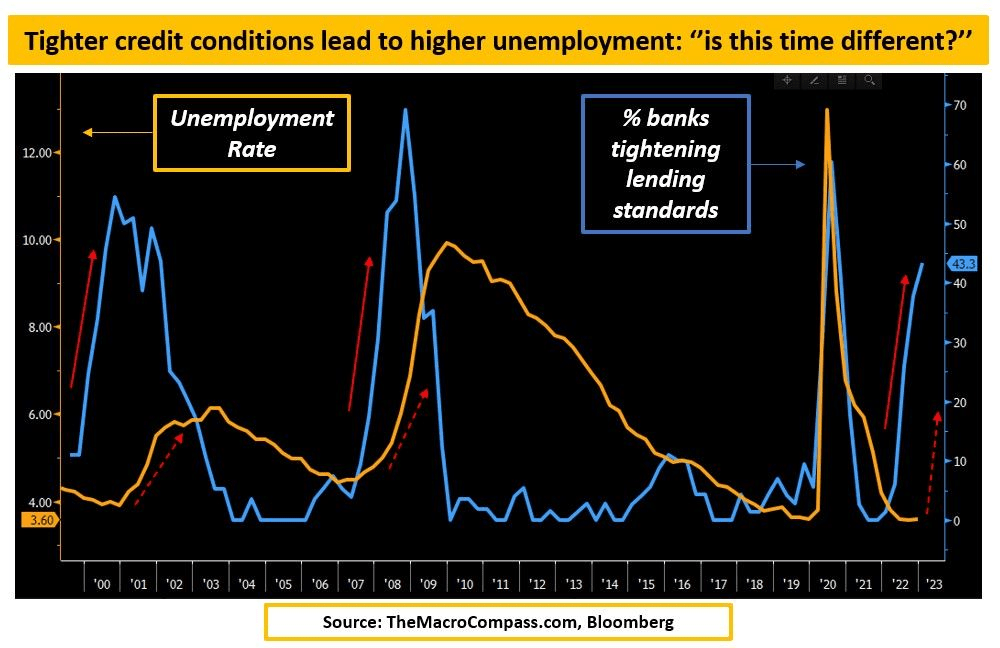

Now we have banks tightening lending standards.

So instead of The Boston Strangler, we have the DC Strangler.

Talk about an economy that seems dependent on Federal government money printing. The US economy seems hopelessly addicted to gov money printing.

Today, US job openings fell in February to 9,931k. While that is still a large number, look at the chart of job openings and M2 Money printing. There is a one year lag between maximum printing and job openings. But M2 Money growth has collapsed.

Silicon Valley Bank’s blunders were encouraged by US regulation, went untested by the Federal Reserve and were “hiding in plain sight” until Wall Street and depositors grew alarmed.

That’s JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon’s assessment of the US banking crisis that sent markets careening last month, an episode he predicts is “not yet over” and will be felt for years. He said US authorities shouldn’t “overreact” with more rules.

In his wide-ranging annual letter to shareholders on Tuesday, Dimon described his firm’s aspirations for using artificial intelligence and ChatGPT, weighed in on geopolitics, and provided updates on JPMorgan’s activities in Ohio. This time, many of his sharpest remarks ripped at regulation, including capital rules that pushed banks to binge on low-interest assets that lost value as interest rates shot up.

“Ironically, banks were incented to own very safe government securities because they were considered highly liquid by regulators and carried very low capital requirements,” Dimon said. “Even worse,” he added, the Federal Reserve didn’t stress-test banks on what would happen as rates jumped.

When Silicon Valley Bank’s uninsured depositors realized it was losing money selling securities to keep up with withdrawal requests, they raced to pull their cash. Regulators then intervened and seized it.

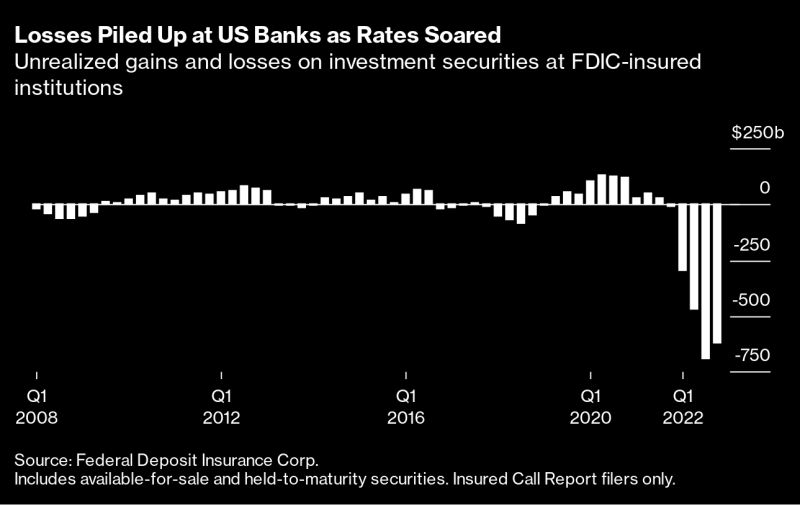

Yes. Banking regulators were so focused on credit-exposure of banks (remember the subprime crisis of 2008?) that they really screwed up by having banks load-up on low credit-risk assets that usually have interest rate risk associated with them like Treasuries and mortgage-backed securities (MBS). What could go wrong?

What went wrong was that interest rates rose and unrealized losses on Treasuries and Agency MBS exploded.

Here is a chart of urealized losses on investment securities that banks have accumulated.

Apparently, The Fed and FDIC (and the myriad of Federal and State regulators) sit high on a mountain top and ignore interest rate risk.

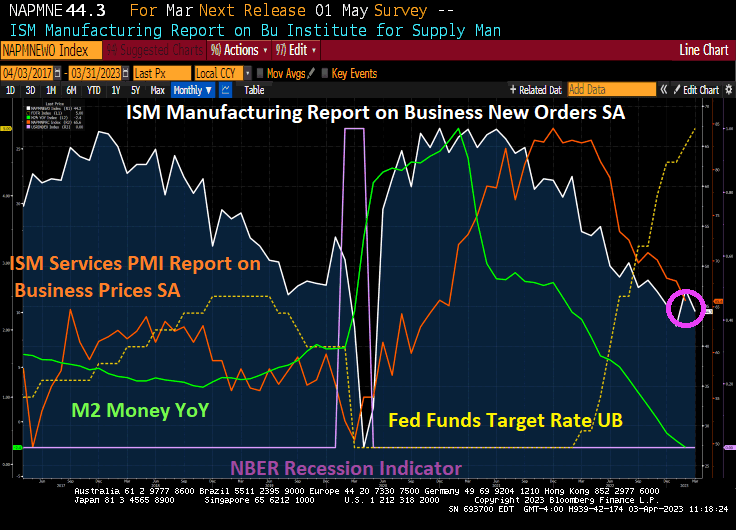

Not only did the ISM Manfacturimng Report on New Business Order fall to 44.3, but price PAID also fell as The Fed hikes rates (yellow line) and slowing M2 Money growth (green line).

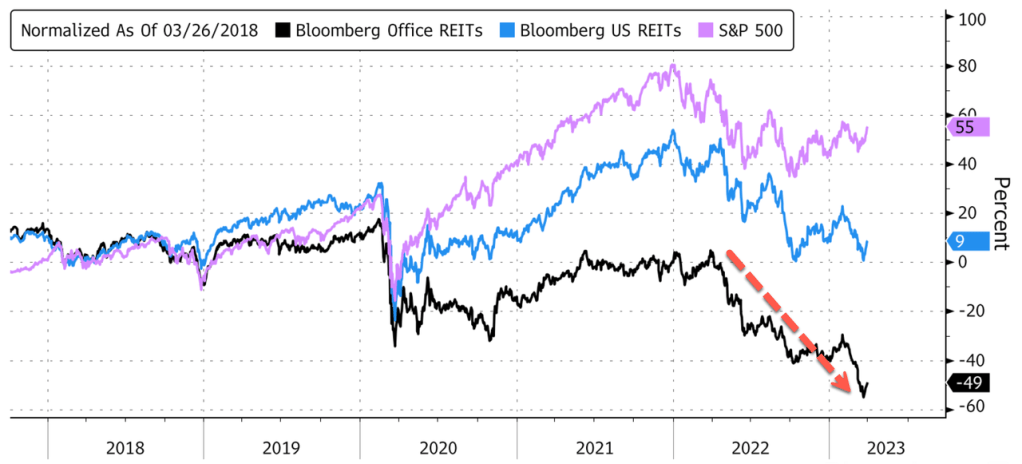

Office REITs are really hurting as Count Powellula sucks the blood (liquidity) from the market.

Count Powellula. “I vant to suck the blood from your economy.”

To show you how Yellen/Powell’s Too Low For Too Long (TLFTL) monetary polices coupled with Biden/Pelosi/Schumer’s (add McConnell to this foul-smelling witches’ brew), Powell and The Gang (aka, The Fed) slammed on the monetary brakes. On a year-over-year basis, M2 Money growth has crashed tl -3.13%. The shocking number is The Fed Fund Effective Rate which rose over 5,000% YoY.

Actually, the US has been on a money printing spree since 1995, but it was Covid spending and monetary expansion in 2020 that crushed M2 Money Velocity (GDP/M2).

Here is Supernatural’s Leviathan monster Dick Roman handing an award to sparkless President Joe Biden. But Biden did spark massive inflation that crushed the US middle class and low wage workers.

Former Fed Chair (and current Treasury Secretary) Janet Yellen protected President Obama by raising The Fed’s target rate only once while Obama was in office. Then raised rates 8 times after Donald Trump was elected in November 2016. Well, Fed Chair Jerome Powell was following Yellen’s TLFTL (Too Low For Too Long) playbook by delaying raising rates once inflation hit 2% in March 2021. Then Powell started raising rates like crazy, unlike Yellen and her zero interest rate policies (ZIRP or ZORP for zero OUTRAGEOUS rate policy).

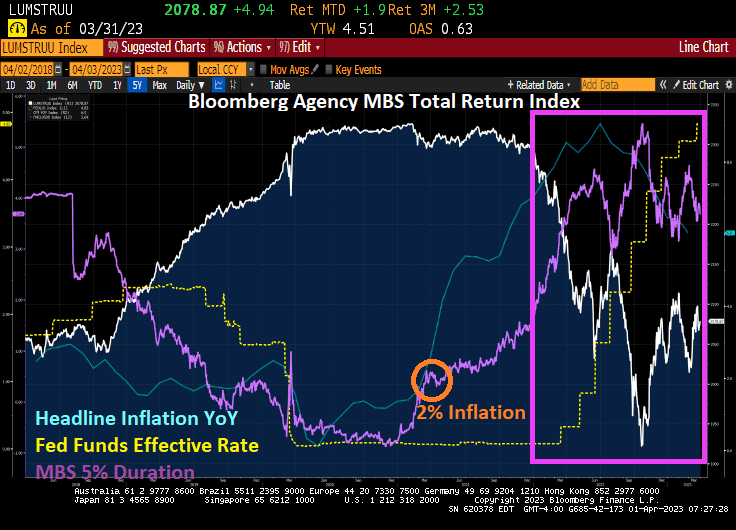

One of the safe assets that Federal regulators encouraged banks to hold was agency mortgage-backed securities. The orange circle denotes when headline inflation YoY hit 2% (March 2021). Powell and the gang waited over a year (remember, they said inflation was “transitory”). But another Democrat, Biden, was now President and Powell (like Yellen) didn’t want to rock the boat. So, Powell and the gang waited until headline inflation hit 7% before they took action. Like Yellen, Powell waited too long .

The result? Agency mortgage-backed securities (MBS) got clobbered (white line) as MBS duration (purple line) rose dramatically. Duration is the weighted-average life of MBS and is a measure of risk.

Any surprise that unrealized losses have been piling up at US banks? Not really, only some regional banks weren’t paying attention and got crushed.

And US bank deposits are crashing despite Biden’s and Yellen’s saying the “all is well!”

Yellen and Powell praising ZORP (Zero OUTRAGEOUS rate policies).

Well, the University of Michigan consumer sentiment indices are out for March … and they are ugly.

As a baseline, consumer confidence in February 2020 (just before Covid) was 101. After Covid and massive Fed stimulus and Federal government spending spree, consumer confidence in March fell to 62.0, a far cry from 101 under Trump.

Even worse, the UMich buying conditions for housing hit 142 in February 2020 but has declined to 47 in March 2023.

Why would ANYONE have confidence in the US economy under a complete fool with dementia like “China Joe” Biden??

You must be logged in to post a comment.