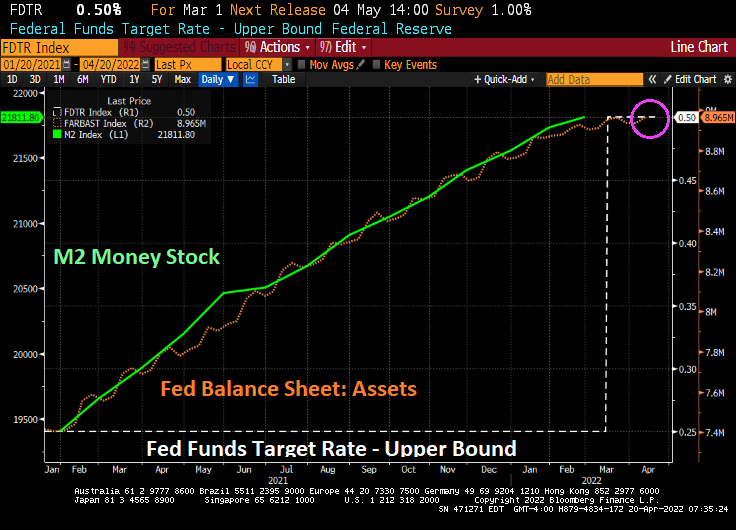

Federal Reserve Chair Jerome Powell said he saw merit in the argument for front-loading interest-rate increases, including a half percentage-point hike next month.“

I would say that 50 basis points will be on the table for the May meeting,” Powell told an IMF-hosted panel on Thursday in Washington that he shared with European Central Bank

President Christine Lagarde and other officials. “We really are committed to using our tools to get 2% inflation back,” he said, referring to the Fed’s target for annual price increases.

Central bankers are grappling with some of the highest inflation rates since the 1980s that are being further pressured as Russia’s invasion of Ukraine boosts food and energy prices and China’s coronavirus lockdowns tangles supply chains anew.

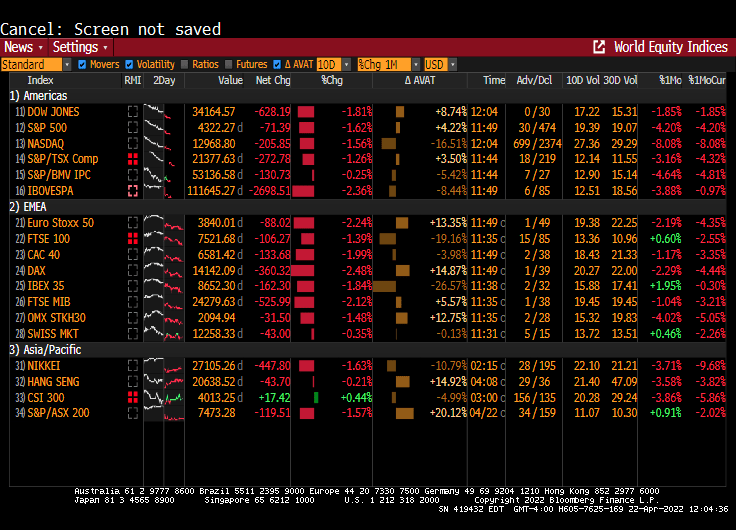

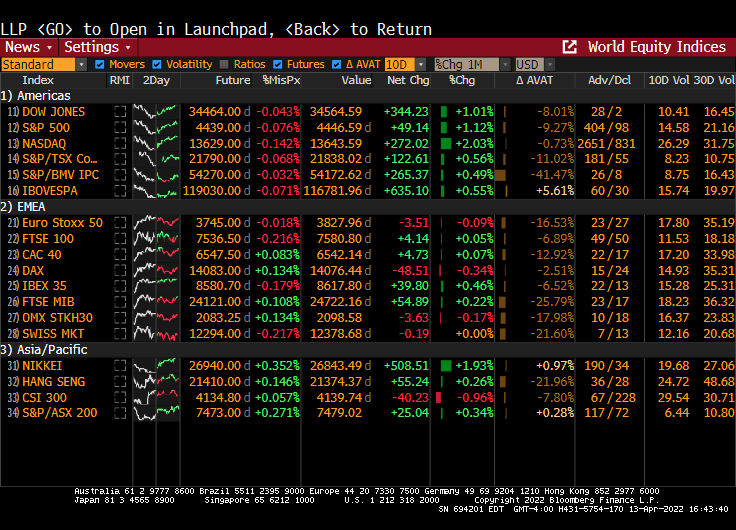

Equity markets in the USA and Europe are getting “Powell’d” and “Lagarde’d” today. As of noon today, the Dow is down 628 points (or -1.81%). Euro Stoxx 50 is down -2.24%.

I remember appearing on Fox Business’ Stuart Varney and Company where he asked me what will happen when The Fed starts to raise rates in a serious fashion. I made a ka-boom gesture at which he laughed. Stuart, I wasn’t joking!

US President Biden went green and signed executive orders on his first day to limit oil and natural gas exploration of Federal lands and offshore (also, killed the Keystone Pipeline), helping to drive up energy prices and food prices. These orders begat inflation (also caused by the massive Covid relief by the Federal government). The highest inflation in 40 years begat The Federal Reserve signalling a tightening of Fed monetary policy … to fight the problem caused by The Fed in the first place … too much monetary stimulus for too long. Fiscal and monetary fanaticism and ignorance is forever busy and needs feeding

There was an interesting article on MarketWatch entitled “Bond rout exposes Social Security’s insanity.” The headline was “Every dollar of yours that’s invested in the Social Security trust fund is invested in low-yielding government bonds.”

Yes, another disastrous consequence of The Fed’s lax monetary policy since 2008, helping to push Treasury yields extremely low. And REAL Treasury yields into negative territory.

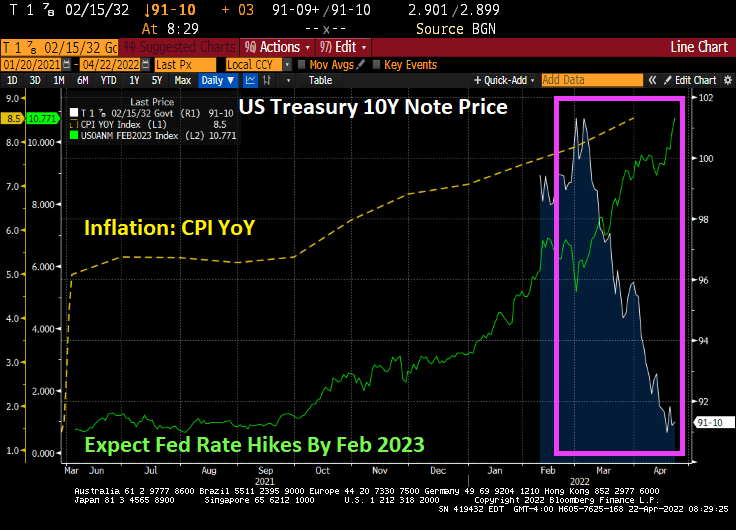

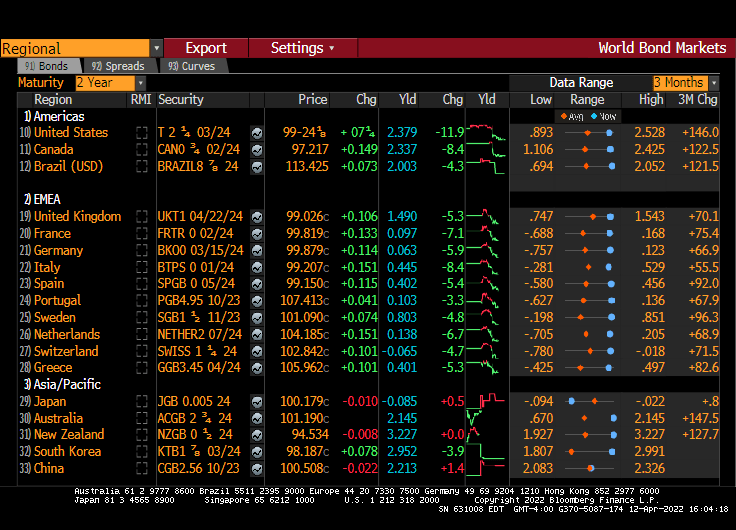

But here we sit today with The Fed threatening to trim their balance sheet and raise rates … to combat the inflation they helped create in the first place. Now we have the 10-year Treasury Note price falling like a paralyzed falcon with expected hate hikes going above rate hikes by February 2023 (based on Fed Funds Futures prices).

Most pension funds also invest heaving in US Treasuries, along with agency Mortgage-backed Securities (AgencyMBS).

The Covid epidemic was bad enough with the government shutdowns and deaths. But was even worse is that all the Fed monetary stimulus and Federal government stimulus “relief” led to a reversal of fortune. In that, the share of net worth held by the top 1% grew and the gap between the 1% and bottom 50% hit an all-time high.

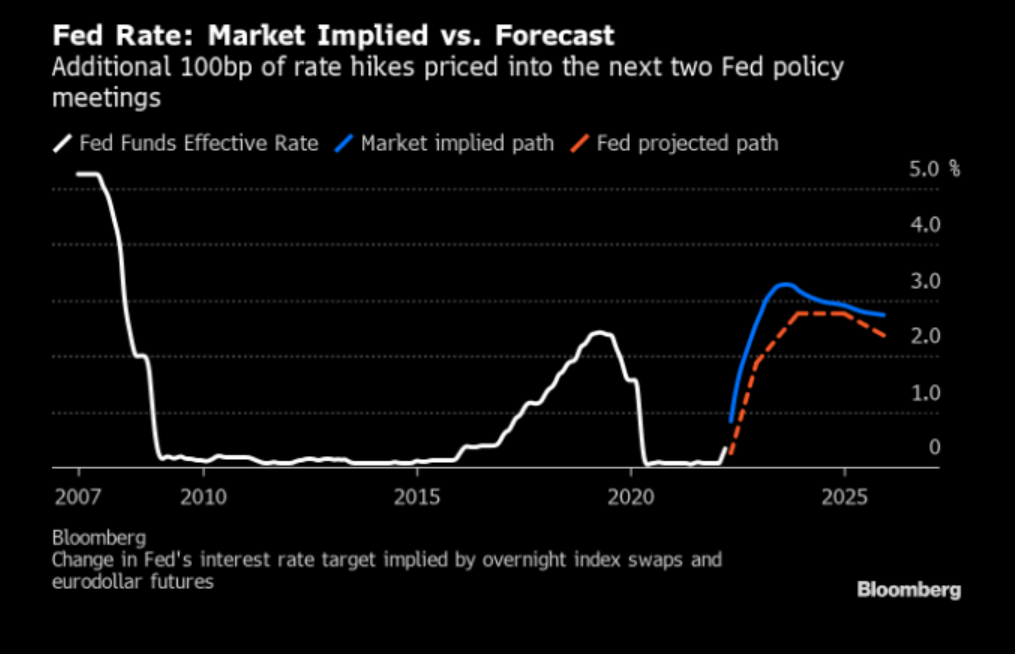

Now that the 1% have fed at the Federal trough, The Fed is anticipated to raise rates by 100 basis points at the next two meetings.

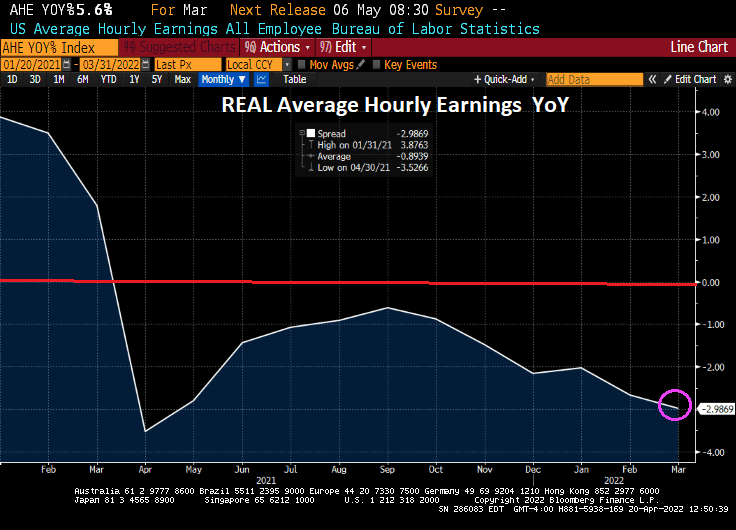

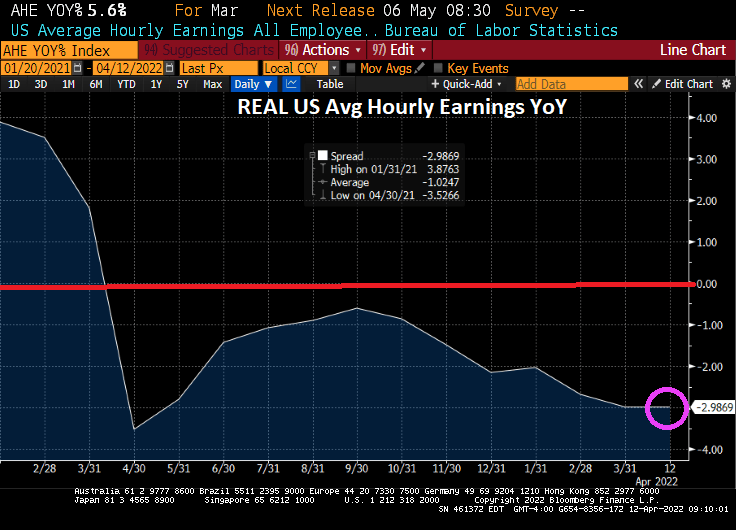

Remember, REAL average hourly earnings are getting crushed under Biden and his pro-1% policies.

This is a nightmare for the American middle-class and lower-wage households.

There is one song that sums up the mortgage banking industry with proposed tightening of Fed monetary stimulypto: T-R-O-U-B-L-E.

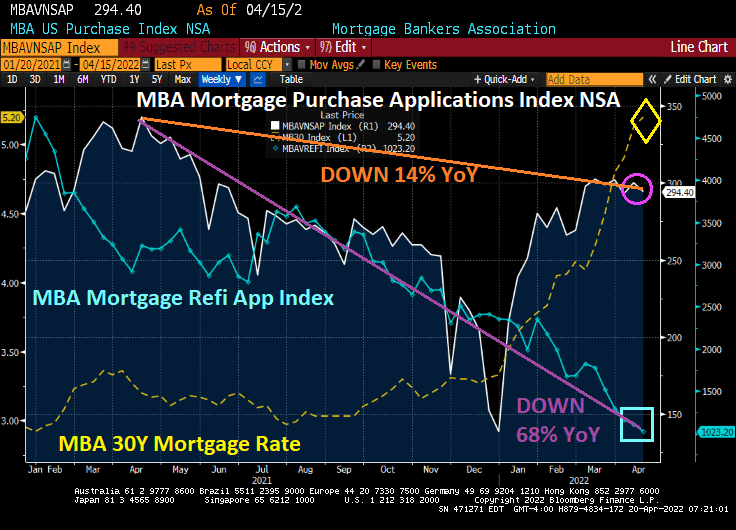

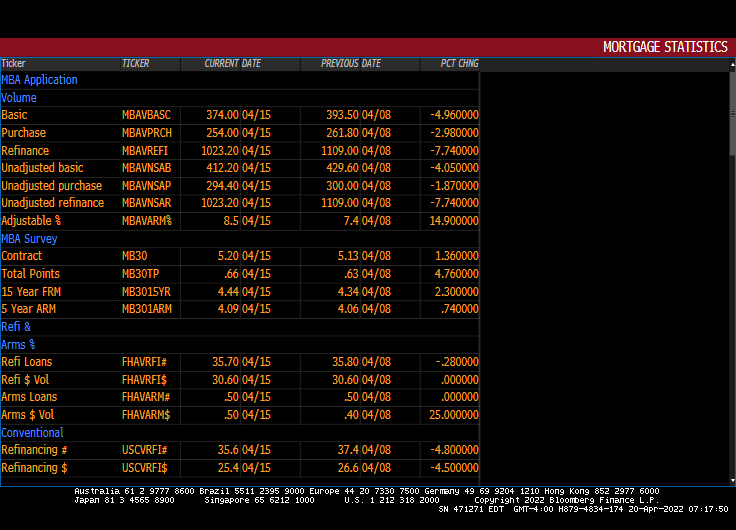

Mortgage applications decreased 5.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 15, 2022.

The Refinance Index decreased 8 percent from the previous week and was 68 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 3 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 14 percent lower than the same week one year ago.

All together now, mortgage rates are up 76% under Biden.

And yes, The Federal Reserve STILL has its enormous foot on the monetary gas pedal (with hints that they will remove it “soon.”

The number of ARMs increased 14.9% from the previous week.

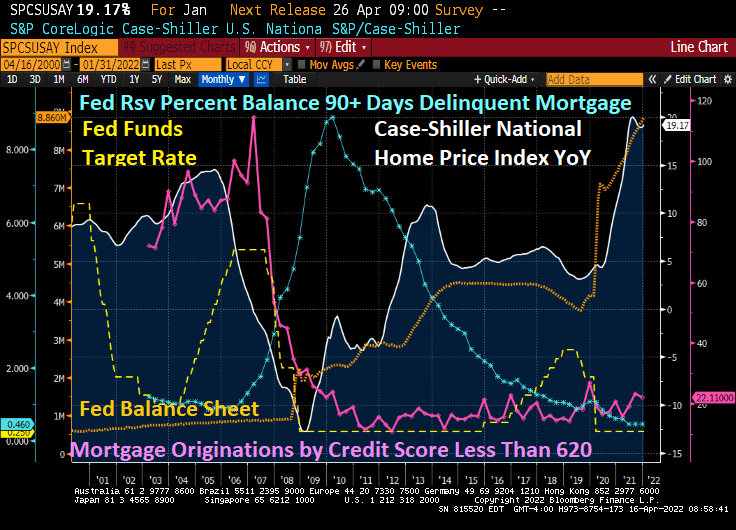

The book and movie “The Big Short” revolved around the 2005-2007 housing bubble driven by lending to borrowers with subprime credit (and little or no underwriting). As we know, Bear Stearns, Lehman Brothers and other investment banks too large positions in subprime asset-backed securities (SABS) that became highly toxic once the demand for high-yield subprime ABS dried up. The decline in US home prices coupled with soaring 90-day mortgage delinquencies led to the failure of Bear Stearns and Lehman Brothers along with Fannie Mae and Freddie Mac being put into conservatorship by their regulator.

Fast forward to today. Mortgage originations by credit scores of 620 or less have shriveled while home price growth YoY is even higher than the subprime mortgage crisis of 2005-2007. So, is the US facing another “Big Short” scenario? Yes and no.

The answer is no in that lenders have tightened their credit box sufficiently so that investment banks are no longer buying large quantities of subprime credit paper. The answer is yes if we consider that the current housing bubble is fueled by extraordinary monetary stimulus due to Covid (as well as rampant Federal government stimulus spending).

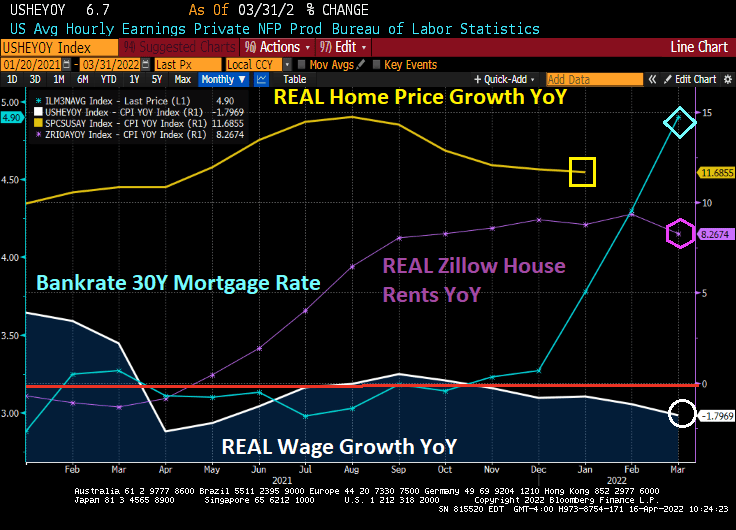

Following the Federal Reserve of Dallas’ lead, here is a chart of REAL home price growth YoY against REAL average hourly earnings YoY. I added REAL Zillow house rents YoY as well.

Look at the affordability gap during the Subprime Bubble of 2004-2006 and then the Fed Bubble of 2020 to today. Both bubbles show a disconnect between REAL home prices and REAL wages. REAL Zillow home rents are not as high as REAL home price growth, but still how a huge gap in rent affordability.

So, what can upset the apple cart? How about Jay and The Gang jacking up mortgage rates making home affordability even worse (unless it slows home price growth).

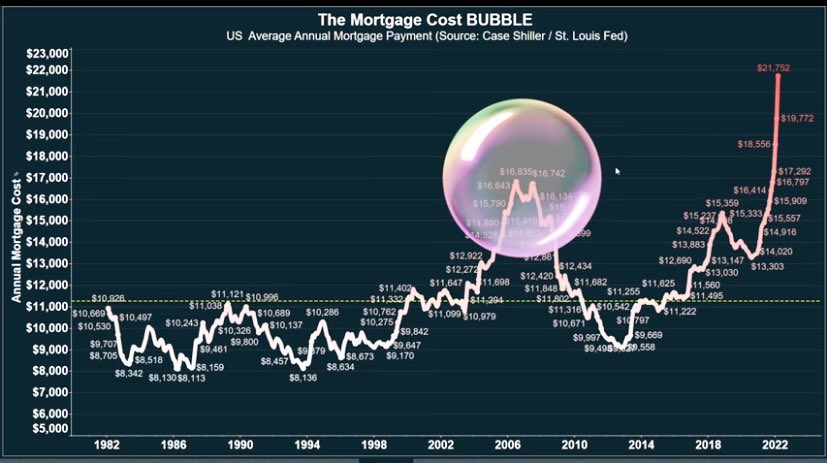

Thanks to The Fed’s propose quantitative tightening, mortgage rates are soaring and mortgage costs along with them. Mortgage costs, thanks to The Fed driving up housing prices AND mortgage rates, are substantially higher than during the subprime mortgage housing bubble.

The Fed’s whipsaw approach helped crash home prices during the subprime mortgage crisis by dropping rates too fast at first (helping to ignite a housing bubble) then raising rates too fast (helping to crash housing prices).

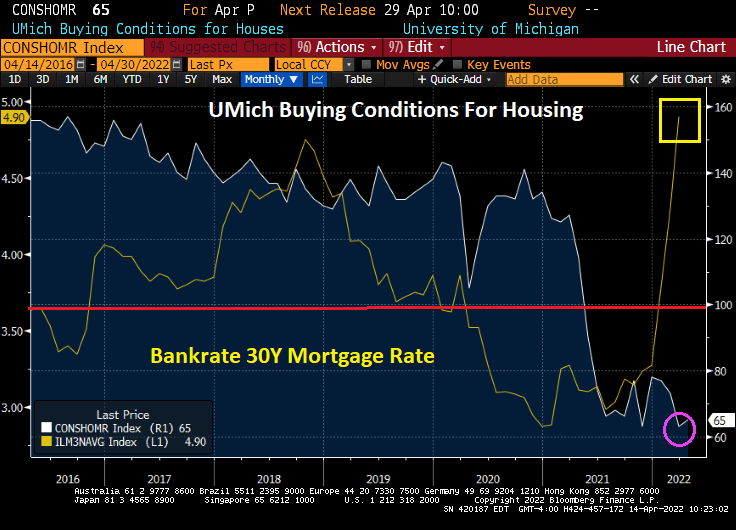

Mortgage interest rates continue their meteoric rise (along with home prices), the result of which is a tanking of consumer confidence in home buying.

The University of Michigan survey of consumers about buying conditions for housing remains depressed due to rising mortgage rates and surging home prices.

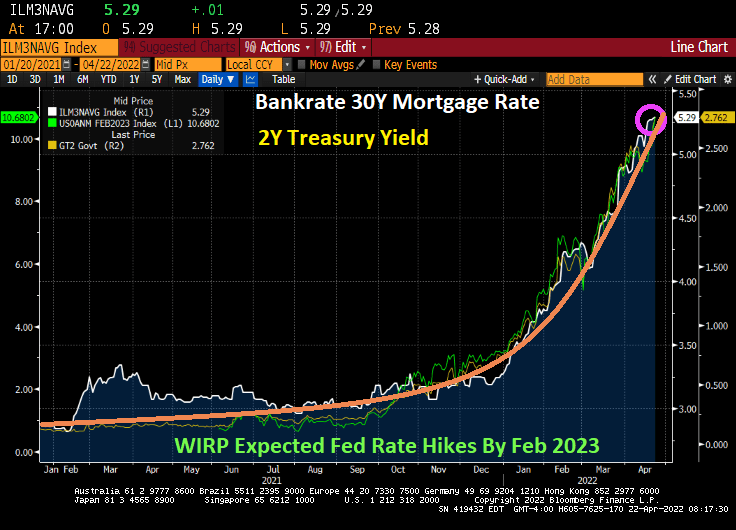

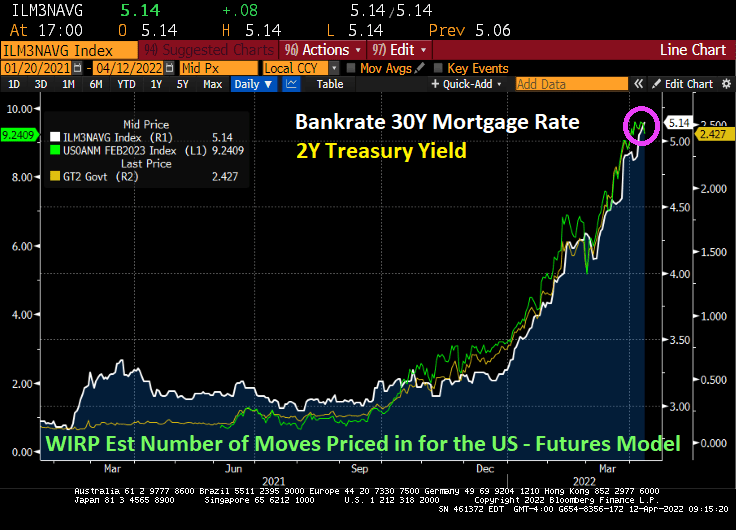

Bankrate’s 30Y mortgage rate is down slightly today to 5.06% as the 2-year Treasury yield declines and the anticipated rate hikes have fallen to 9.19.

As I mentioned earlier, mortgage credit availability hasn’t recovered from the “Covid Correction.”

Harry Truman once uttered the phrase “The buck stops here.” Joe Biden’s catchphrase should be “It’s Russia’s fault!”

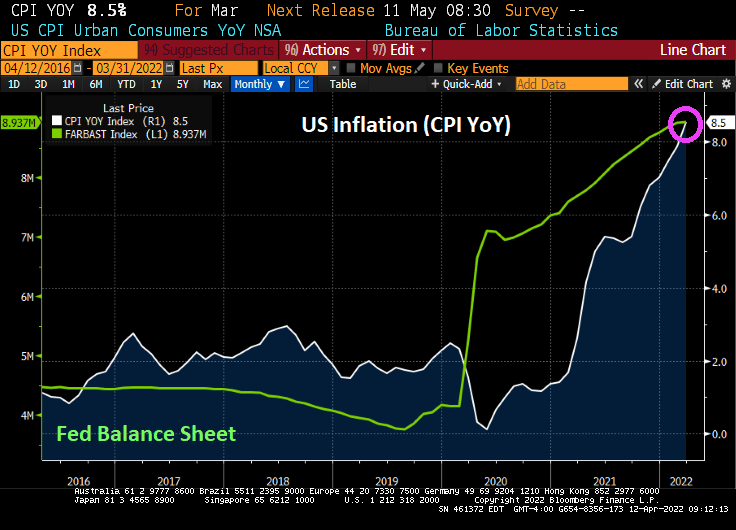

Well, all roads led to Joe and Jay. Here is a chart of Producer Price Index (Final Goods) prices YoY, now the highest in history. At least, gasoline prices are declining to $4.083 (they were $2.40 when Biden was installed as President). But inflation is out of control and the 30-year mortgage rate is now 5.14% (mortgage rates were 2.82% in February 2021 just after Biden took control).

Just in case you wonder why I follow Fed Funds Futures data so closely.

Equity markets are up strongly today as markets sense a weakening in resolve by The Federal Reserve (number of expected rate hikes dropped at 10AM EST).

It appears that we have a “Powell in the headlights” problem.

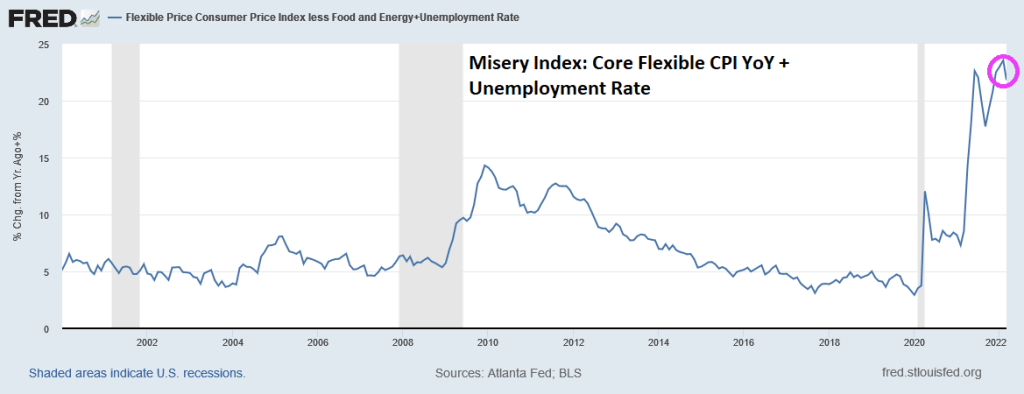

The Federal Reserve’s two goals of price stability and maximum sustainable employment are known collectively as the “dual mandate.” Unfortunately, inflation is running away (bad) from employment gains (good). Sort of like “The Good, The Bad and The Ugly.” But just the Good and The Ugly combine to create the Misery Index.

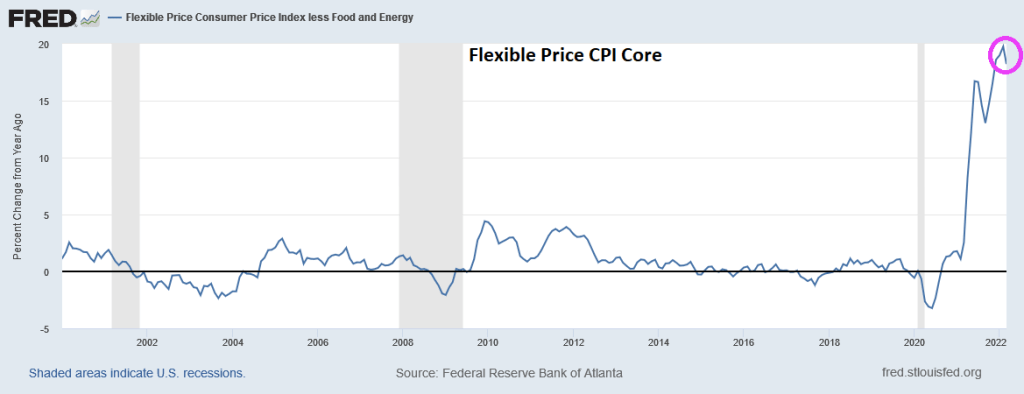

Here is the Atlanta Fed’s CORE flexible CPI YoY for March. The good news? Flexible Core CPI YoY was a little lower than the historic high reading in February. The bad news? We are still talking about 21.82%+ rise in prices (down from 23.56% in February).

If I use the Atlanta Fed’s flexible consumer price CORE index combined with the U-3 unemployment rate, we see that March’s inflation report plus U-3 unemployment is generating a misery index that was last seen in July 2008 during The Great Recession. Unless we consider the July 2021 reading of 31.3%, so we have seen two horrible misery index readings under Biden.

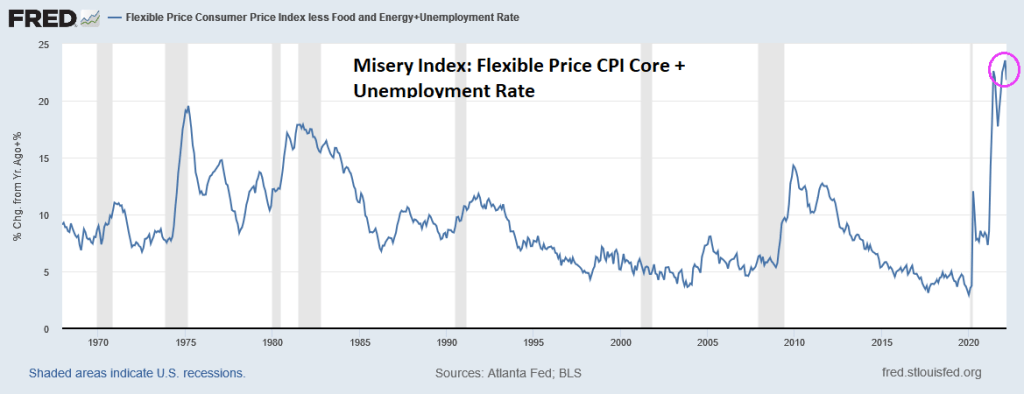

If we look at the Misery Index since 1967, we now have the GOAT (Greatest of All-time) Misery.

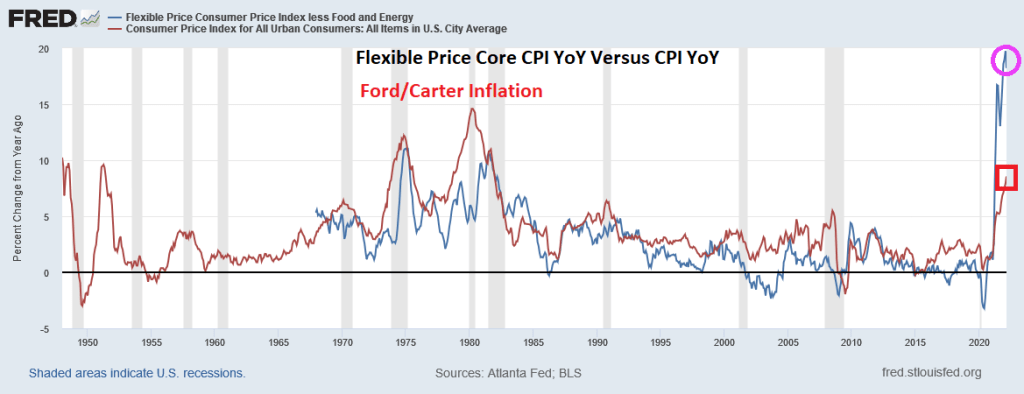

Now, inflation under Presidents Ford and Carter (red line) were higher than the flexible core price index (blue line) in the 1970s and 1980. But flexible core price CPI YoY is substantially higher than March’s CPI growth of 8.5%.

The bottom line is that inflation losses are far outweighing the employment gains, resulting in elevated misery.

US real average weekly earnings growth YoY is down to -3.60%. That is the lowest since 2007 and is worse than The Great Recession and financial crisis of 2008.

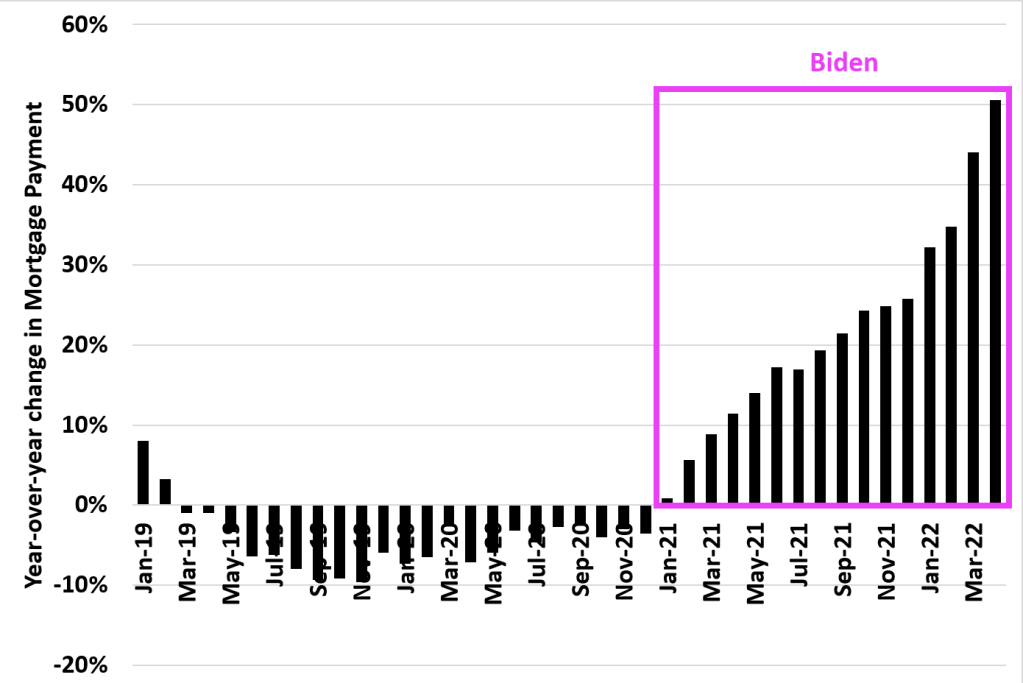

And look at this chart of mortgage payments under Biden. The US was actually experiencing DECLINING mortgage payments YoY in 2019 and 2020. But under Biden’s leadership, mortgage payments have increased by 50% making housing even MORE unaffordable for the middle class and lower-income households.

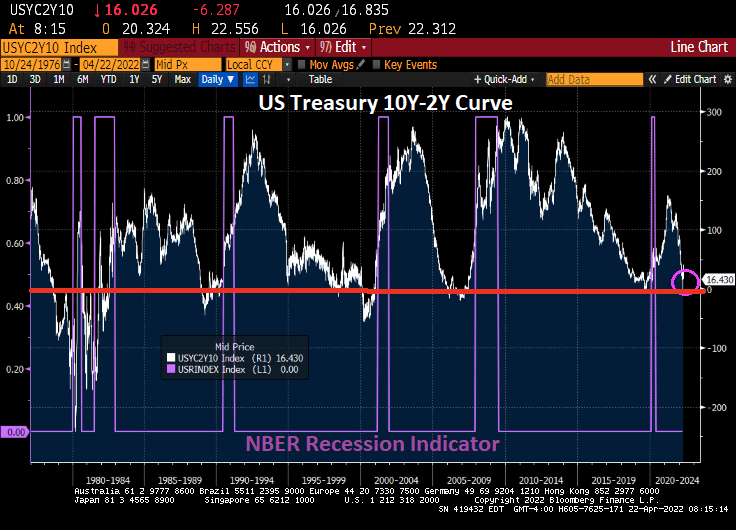

And now for something kind of scary. The US today suffered a 12 basis point decline in the 2-year Treasury yield, generally a bad sign for the economy. As if we needed more bad news for today.

Highest inflation in 40 years, worst wage growth since 2007 and rising mortgage payments. We will need all the luck we can get.

With 8.5% YoY inflation, REAL average hourly earnings growth fell to -3% YoY.

And with The Fed intent on extinguishing their part of the inflation, Bankrate’s 30Y mortgage rate rose to 5.14%.

Energy is the biggest culprit (fuel oil up 70.1% YoY) thanks to the double whammy of 1) Russia’s invasion of Ukraine and 2) Biden’s restrictions on oil and natural gas production. Food at home is up 10% YoY.

Here is a colorful chart of MoM growth in prices.

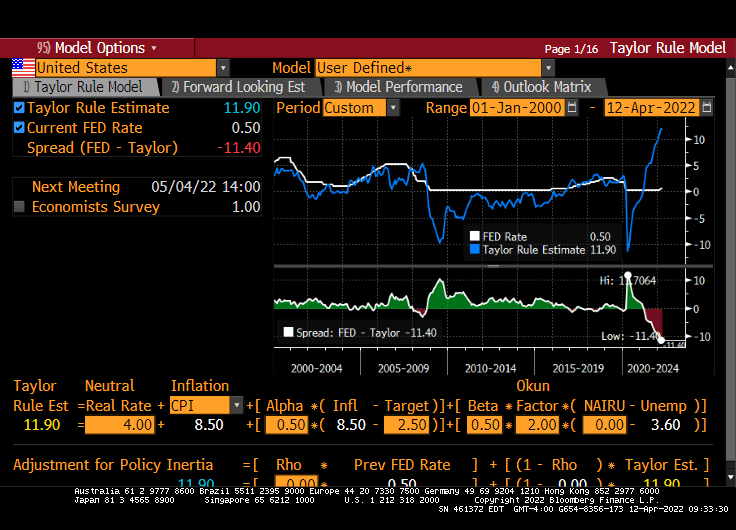

The Taylor Rule model now says that The Fed Funds Target Rate should be 11.90%. Hence, Fed Stimulypto is still in place with the signal that rates will increase.

How about WTI Crude and Brent Crude soaring over 4% today?

Once again, the Four Horsemen of the Inflation Apocalypse (Biden, Powell, Pelosi, Schumer) overstimulated the economy and financial markets with excessive monetary stimulus (Powell) and excessive Federal spending (Biden, Pelosi, Schumer) where demand soared for products and supply naturally hasn’t caught up.

You must be logged in to post a comment.