Well, the Fed’s talking heads have been saying a 50 basis point hike was coming in May … and it appeared!

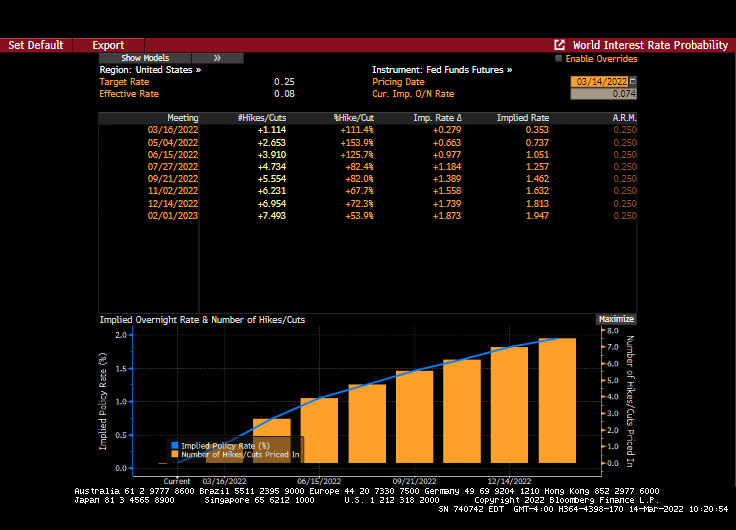

And it looks like 9 rate hikes are a comin’ by February 2023.

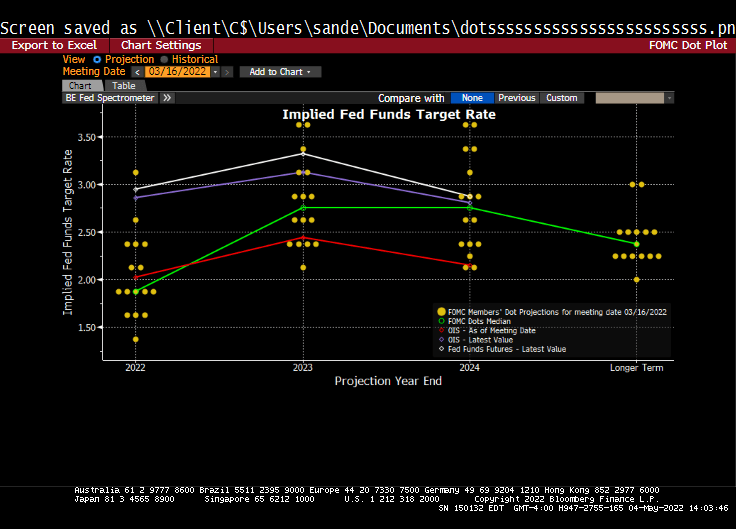

The Fed’s Dot Plots shows a cooling of Fed rate hikes by 2024 and beyond.

Here is the path of Balance Sheet peel-off.

The US Treasury actives curve is up by 14 bps at the 10-year tenor and up 17 bps at the 2-year tenor.

The plan will see $30 billion of Treasuries and $17.5 billion on mortgage-backed securities roll off. After three months, the cap for Treasuries will increase to $60 billion and $35 billion for mortgages.

I could read the Fed’s speech on their decision, but since The Fed has been so highly politicized, I don’t really care what they say. Only what they do.

The U.S. Treasury market is showing signs of stress that may have implications for whether the curve keeps steepening.

Over the past month the curve has retraced from an inversion to a steepening driven by a surge in yields on benchmark 10-year bonds. That has led to interesting outlier indications, as traders weigh the outlook for Federal Reserve interest rate increases and inflation.

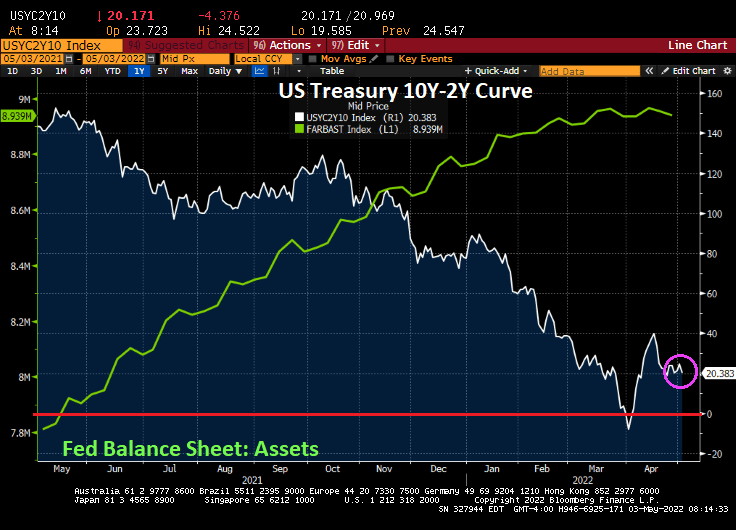

The US Treasury yield curve has settled-in at 20.383 bps (effectively zero) as The Fed continues its war on inflation.

On the SOFR front, we see SOFR Coupons being slow to benefits from Fed rate hikes. So, SOFR Coupons are behaving like Stouffer’s lasagna, frozen and tasteless.

On the other hand, mortgage rates continue to soar on EXPECTATIONS of Fed rate hikes.

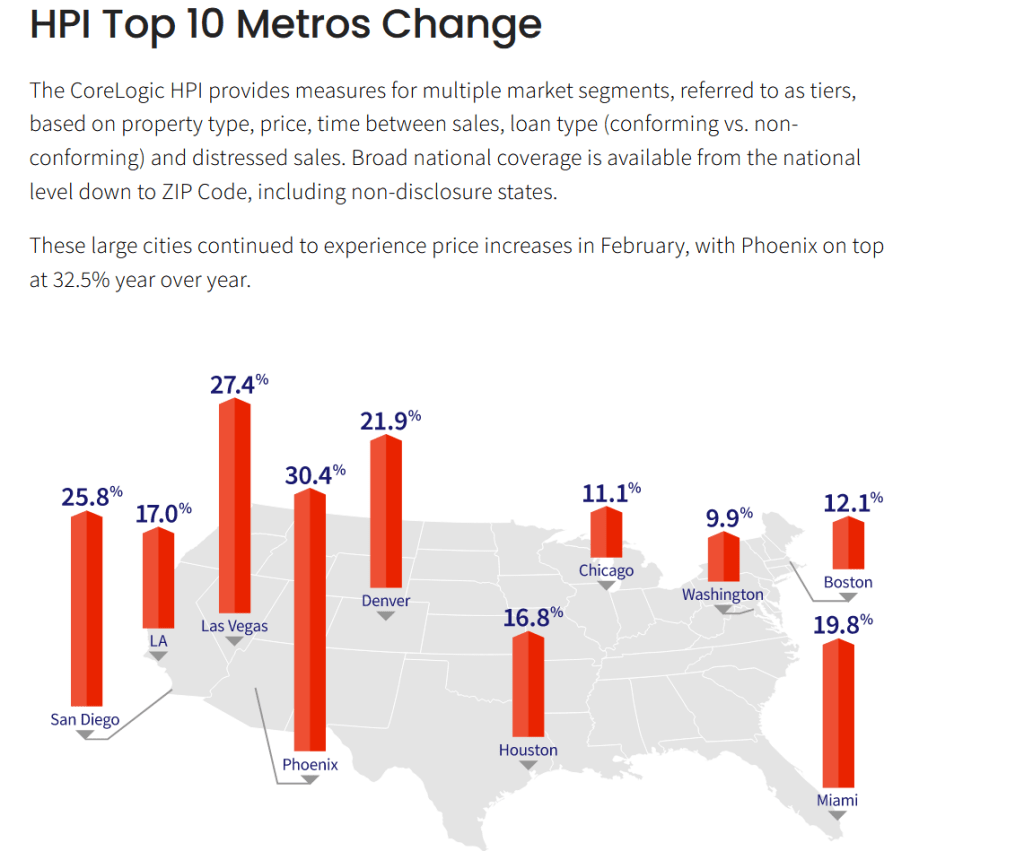

Phoenix AZ leads the top ten at 30.4% with Washington DC lagging at 9.9%.

So, its official. The Federal Reserve is best exemplified by former Yankee/Mets first baseman “Marvelous” Marv Throneberry. When players presented Mets’ manager Casey Stengel with a birthday cake but neglected to give piece of cake to Throneberry, Stengel replied to Throneberry when asked why no cake, “Because I was afraid your were going to drop it.”

Just like The Federal Reserve, the honorary Marv Throneberry of the the global economy.

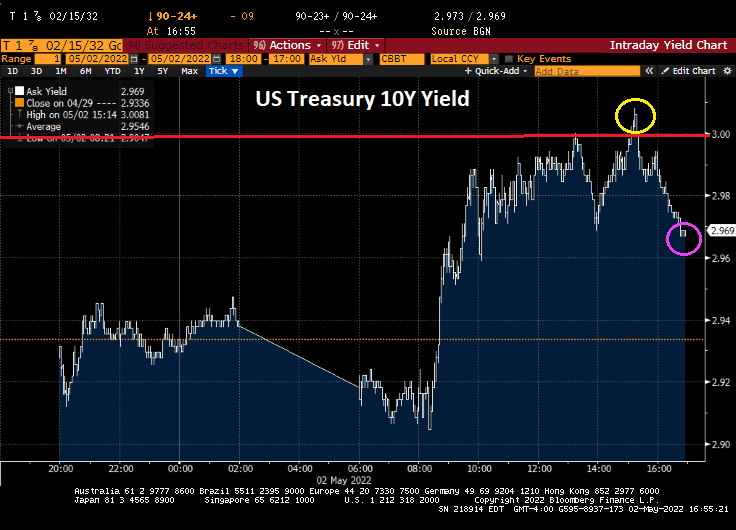

Today we saw the 10-year Treasury Note yield break through the 3% barrier, then retreat as is there was a reflecting barrier at 3%.

And in Europe, we saw a flash crash allegedly caused by Citi’s trading desk.

The selloff was triggered by a large erroneous transaction made by the U.S. bank’s London trading desk, according to people with knowledge of the matter who asked not to be identified discussing private information. A knee-jerk selloff in OMX Stockholm 30 Index in five minutes wreaked havoc in bourses stretching from Paris to Warsaw toppling the main European index by as much as 3% and wiping out 300 billion euros ($315 billion) at one point.

The US Dollar rose again as expectations of Fed monetary tightening due to inflation become a reality.

A measure of U.S. manufacturing activity unexpectedly dropped in April to the lowest level since 2020 as growth in orders, production and employment softened.

The Institute for Supply Management’s gauge of factory activity fell to 55.4 last month from 57.1, according to data released Monday. The Manufacturing Prices index remained elevated.

As the 10-year Treasury yield tries to breech the 3% barrier.

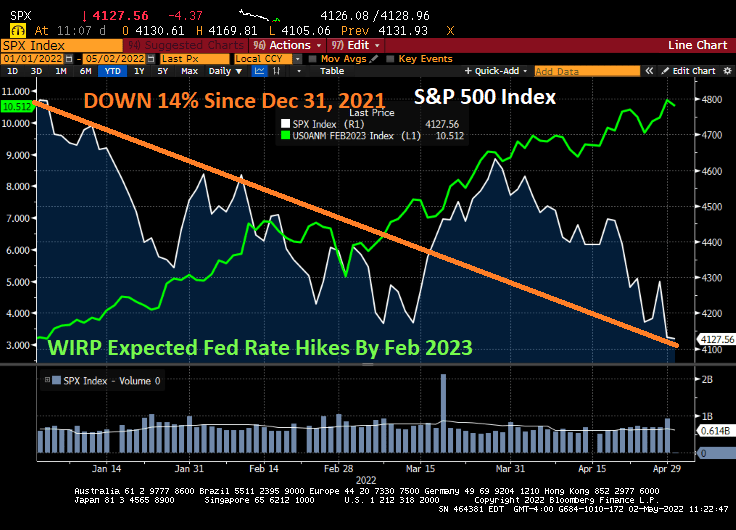

And as The Fed continues to threaten tightening of their monetary follicies, the S&P 500 index is down 14% since Dec 31, 2021.

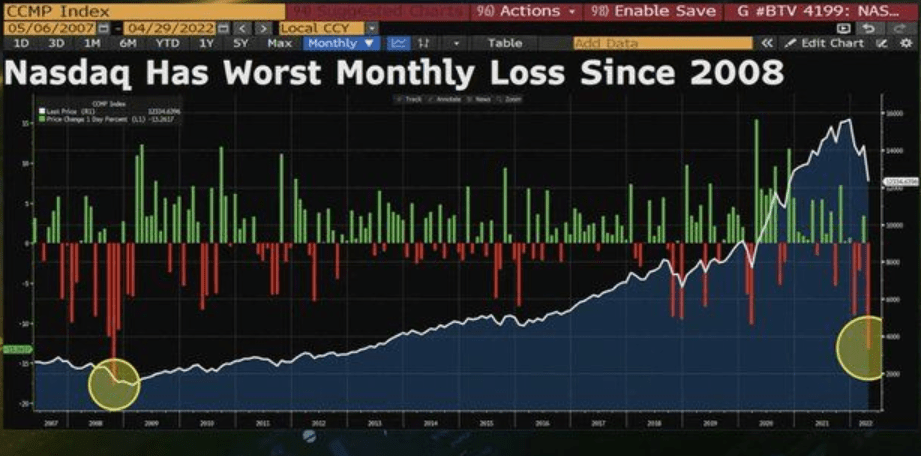

And the NASDAQ had it worst monthly loss since 2008.

Well, the US have gone from “fastest economic recovery in history” to real GDP growth of less than 1% (Atlanta Fed GDPNow for Q1). In addition, the flexible price CPI less food and energy is a whopping 20%.

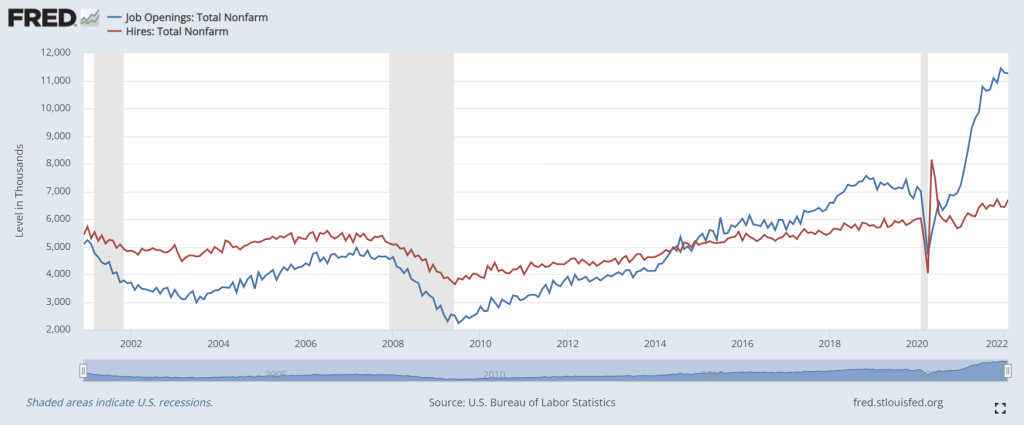

You can see “The Biden Miracle!” in the following chart. Hires (red line) dropped with Covid shutdowns, then spiked when governments opened economies again. Throw in the trillions of Federal government Covid stimulus and trillions in Fed monetary support, the Biden Miracle sees less like a miracle and more like an extremely expensive way to add jobs. But the interesting problem facing the Administration is the massive spike in job openings relative to hires (again, governments opening-up plus Federal Stimulypto).

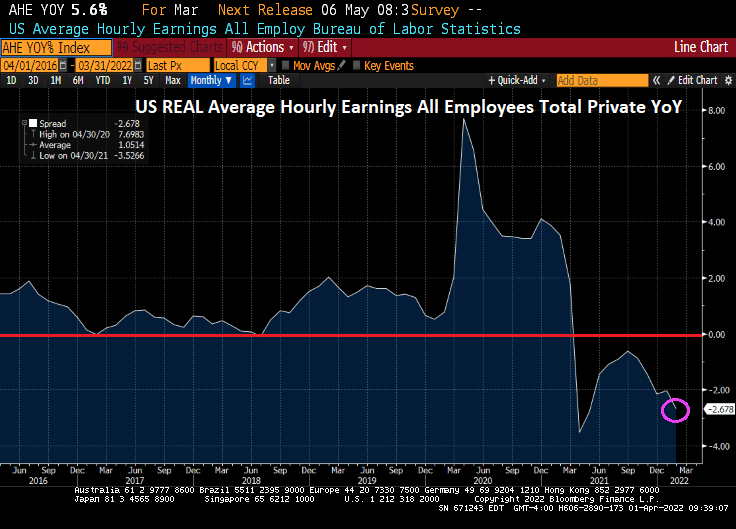

Now for a real downer of a chart. Inflation is so toxic that REAL average hourly earnings YoY is down -2.72%. Hardly the best economic growth in history.

Now we have Jerome Powell and The Blackhearts threatening quantitative tightening starting in May. Here is The Fed’s theme song “We love printing money.”

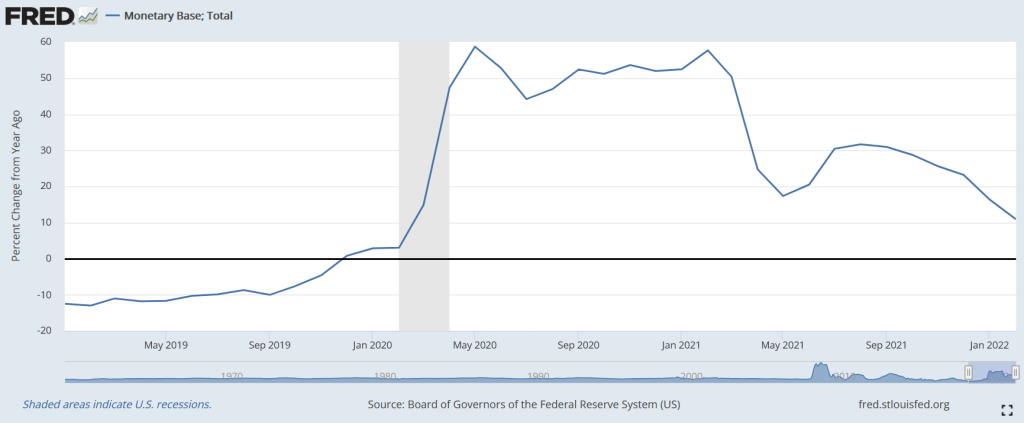

But The Fed is already slowing the growth of monetary base, although this Fed Stimulypto is still growing much faster than pre-Covid.

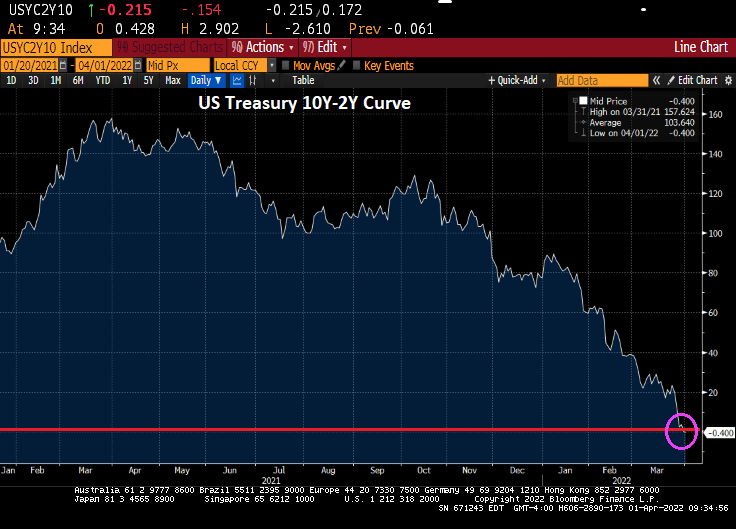

At least the 10Y-2Y Treasury curve is back above 0 bps as the Atlanta Fed’s GDPNow Q1 forecast falls to under 1%.

Remember, The Fed is planning on shrinking the balance sheet by $95 billion. The Fed’s balance sheet is just shy of $9 trillion. Which is around 1% per month.

With rising expectations of Fed quantitative tightening (QT), residential mortgage rates keep climbing.

Despite a slowing economy teetering on recession and a war raging in Europe, The Fed is tightening monetary policy. Allegedly to fight red-hot inflation.

(Forbes) – Credit Suisse’s Zoltan Pozsar argues Bretton Woods II crumbled when the G7 countries seized Russia’s foreign exchange reserves. Keeping money inside financial institutions like the IMF was considered risk free. That is clearly no longer the case. Similarly, Bretton Woods I collapsed when Nixon took the US of the gold standard back in 1971 when dollars were convertible to gold at a fixed exchange rate of $35 an ounce. This led to Bretton Woods II, backed by “inside money” or the dollar, which itself is not linked to gold or any other commodity.

Now the basis of this system, which has operated for the past 50 years, is being called into question. The sanctions on Russia, which showed that reserves accumulated by central banks can simply be taken away, raised the question of “what is money?”

That question may explain why Pozsar believes a huge shift in the way the world organizes money and reserves is now underway, “creating a “Bretton Woods III backed by outside money,” (gold and other commodities). Including crude oil and bitcoin.

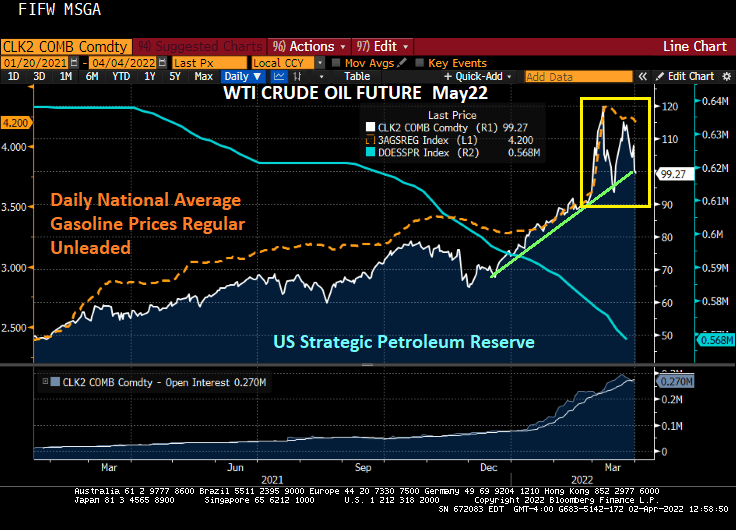

At least crude oil has fallen below $100 as Biden merrily drains the Strategic Petroleum Reserve (SPR). Gasoline prices have fallen slightly as this is being done before the midterm elections with political, not economic, intent. Once the midterms pass, will Biden continue draining the SPR until there is little left forcing the US to convert to “green energy”?

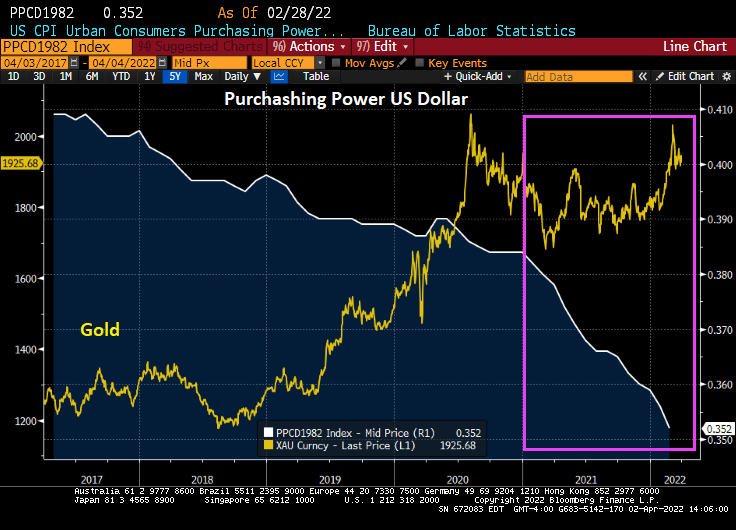

The purchasing power of the consumer dollar took a plunge under Biden as other commodities such as Bitcoin and crude oil soared.

An alternative asset, gold, have generally risen under Biden’s Reign of Error, but particularly after the Russian invasion of Ukraine.

Wasting away again in Biden/Pelosiville, looking for my lost inexpensive gasoline and food. Some people say that Putin is to blame, but we know its Biden/Pelosi’s fault.

The US Treasury 10Y-2Y yield curve just inverted, generally a precursor to a recession. Called it, nothing but net!

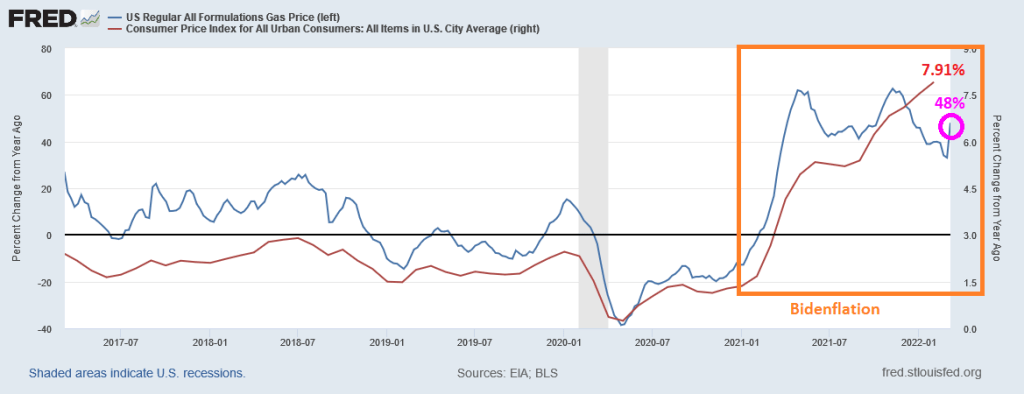

Meanwhile, today’s jobs report shows that Bidenflation is crushing America’s wage growth. While average hourly earnings grew to 5.6% YoY, we are still seeing inflation growing at 7.9% YoY meaning that inflation is reeling hurting the middle class and lower-income households.

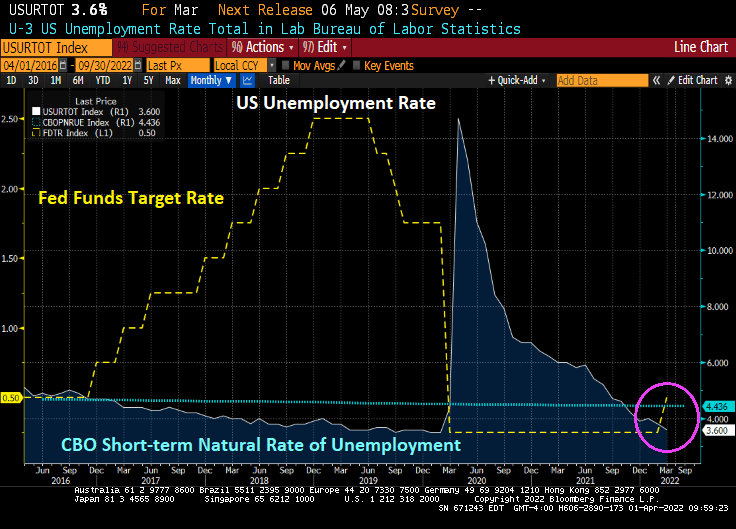

The good news is that the U-3 unemployment rate fell to 3.6%, almost back to the Trump-era unemployment rate of 3.5% prior to the Covid outbreak. And the unemployment rate remains below the CBO’s short-term natural rate of unemployment indicating that the labor market is OVERHEATED.

Today’s jobs report was pretty good, as we would expect from a recovery caused by governments shutting down economies, then reopening them. 431k jobs were added, but less than last month’s jobs added of 678k and less than the forecast 490k.

The number of people NOT in the labor force fell slightly, but it still around 100 million. The number of people holding multiple jobs to overcome Bidenflation rose to 7.5 million.

On the mortgage front, Bankrate’s 30-year mortgage rate rose to 4.90% as the 2-year Treasury rate (yellow) rises and the number of expected Fed rate hikes over the coming year is 9.26%.

According to Fed Funds Futures data, The Federal Reserve is now forecasting 9 rate increases over the next year.

Fed Funds Futures are pointing to 8.924 rate hikes by the Fed FOMC meeting on February 1, 2023.

The US Treasury 10Y-2Y curve flattened by 5.5 bps today with the entire curve downshifting.

The Federal Reserve reminds me of The Office episode “Malone’s Cones.” They can’t really explain why they kept rates so low for so long (policy error) and seem to risk collapsing the market with rapid rate hikes without much sensible explanation.

Yes, it is the much anticipated Fed Week! The Fed Open Market Committee (FOMC) will announce it decision (probably the first rate hike under Biden of 25 basis points).

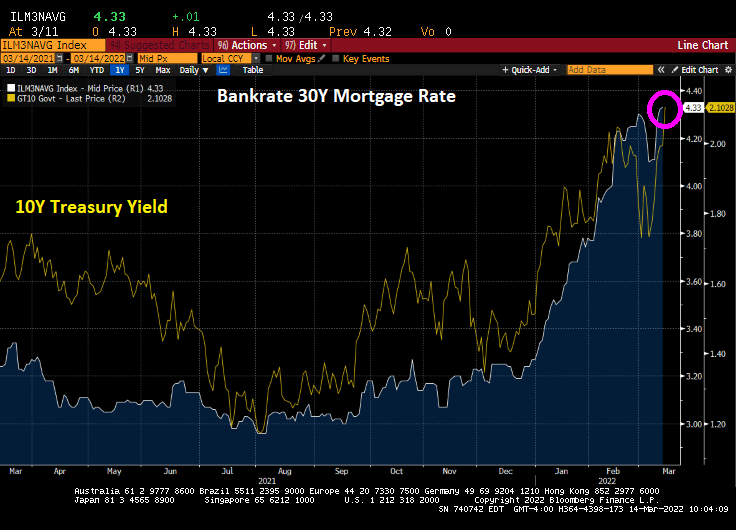

This morning, the 10-year Treasury yield rose by 11.1 basis points and the Bankrate 30Y mortgage rate rose to 4.33%.

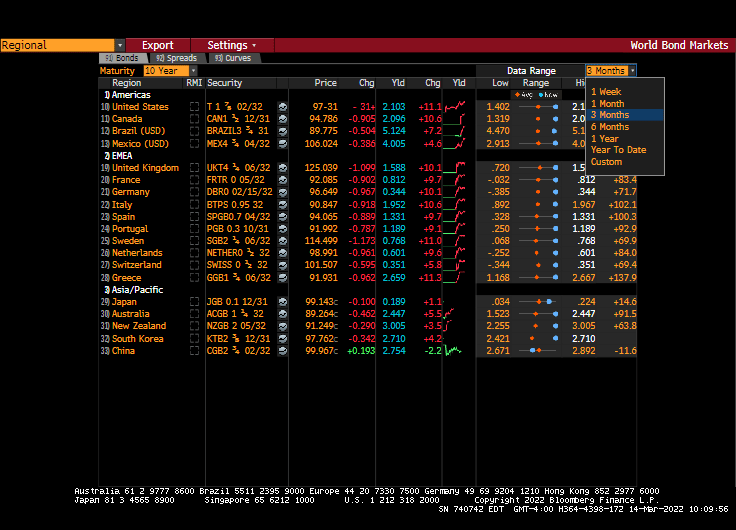

Actually, sovereign yields are up around 10 basis points in the US, Canada, and across the pond.

Fed Funds Futures are pointing to 7 rate hikes over the next year with 1.114 rate hikes on Wednesday. That means The FOMC may raise rates MORE than the 25 basis points expected my many (including me).

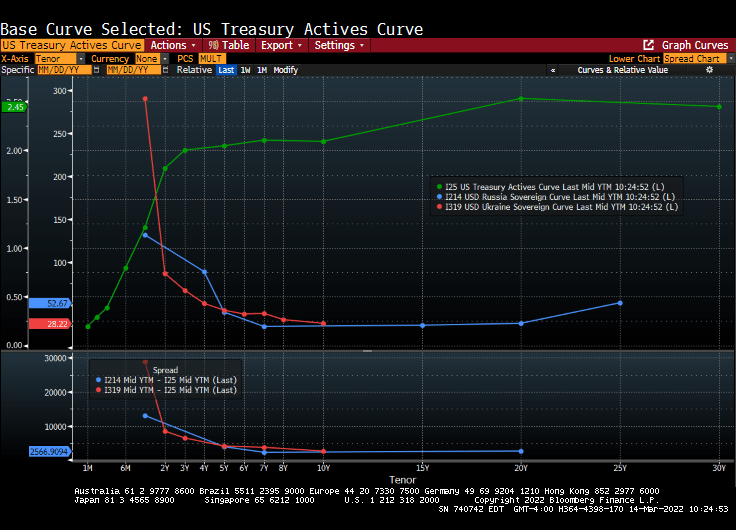

The US Treasury actives curve remains steeply upward sloping while both the Russian and Ukraine sovereign curves are steeply inverted and crashing.

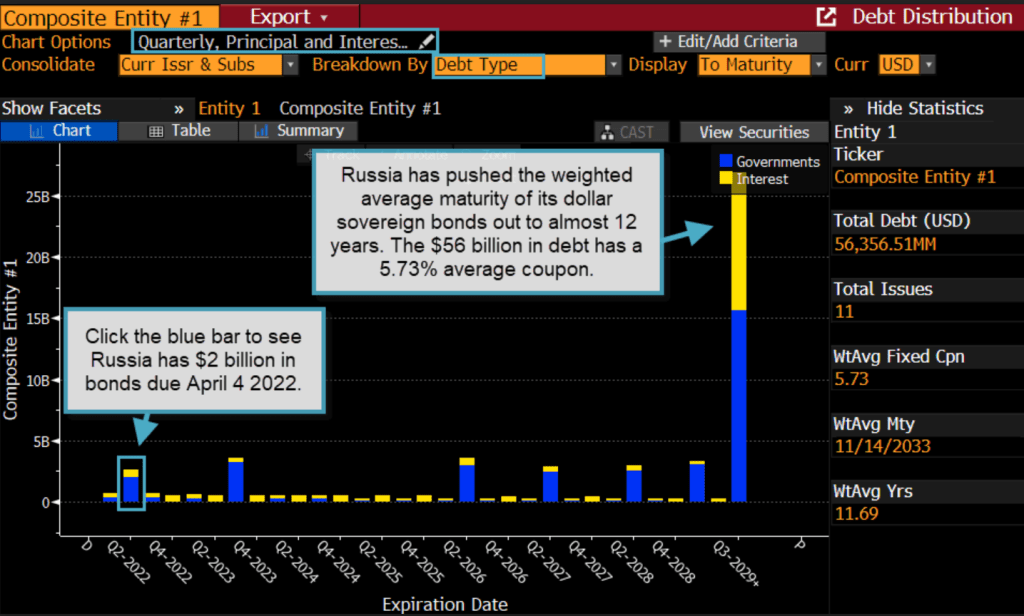

Russia has pushed the weighted average maturity of its dollar sovereign bonds out to almost 12 years.

The most hilarious headline of the day is a Bloomberg opinion piece: “Fighting Inflation May Require the Fed to Be Brutal: Clive Crook” How about the Biden Administration relaxing oil drilling and pipeline restraints? Otherwise, brutal translates into causing a recession. Great suggestion, Clive! … NOT!

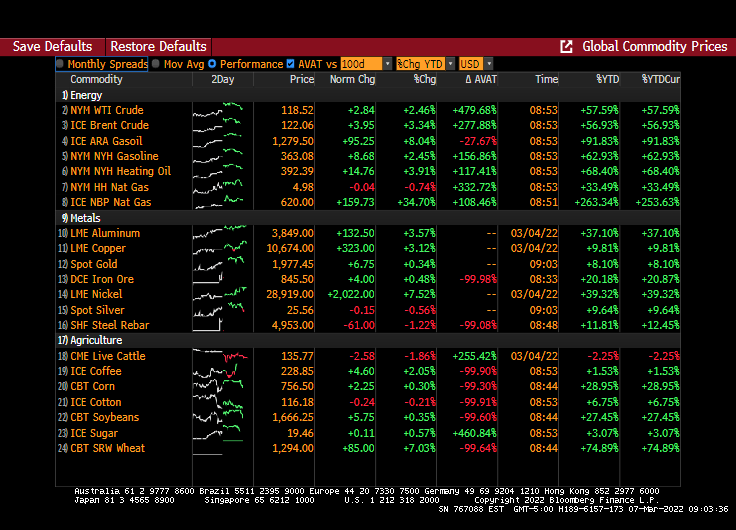

WTI Crude Oil spot price was up 91% from the beginning of 2021 to the Russian invasion of Ukraine. Now it is up 142% thanks to the invasion of Ukraine.

Energy prices are still soaring with UK Natural Gas prices up another 34.70% today with Brent Crude futures up 3.34%. Wheat futures are up 7.03%.

The US Treasury 10Y yield rose 6.8 bps this morning (UK takes the lead with a 10.3 bps increase).

The US Treasury 10Y-2Y yield curve slope continues to swoon to where it is now flatter than when President Biden entered office.

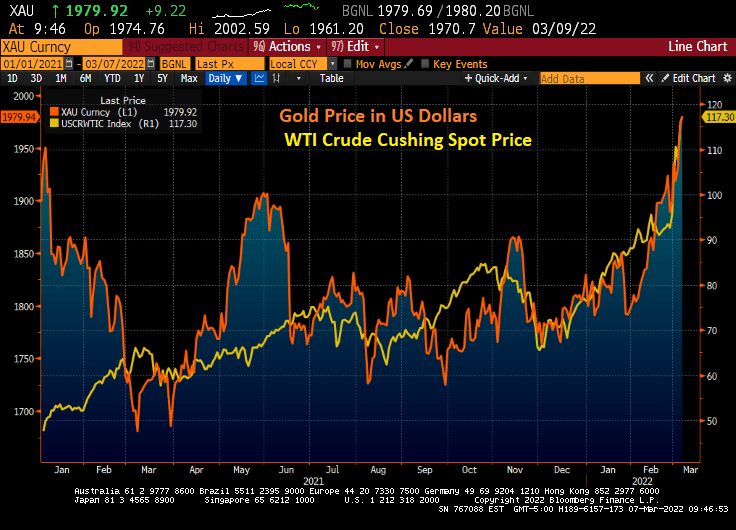

Gold is now at it highest level since before Biden was sworn-in as President as WTI Crude Oil soars.

Gold hit $2,000 before retreating back down.

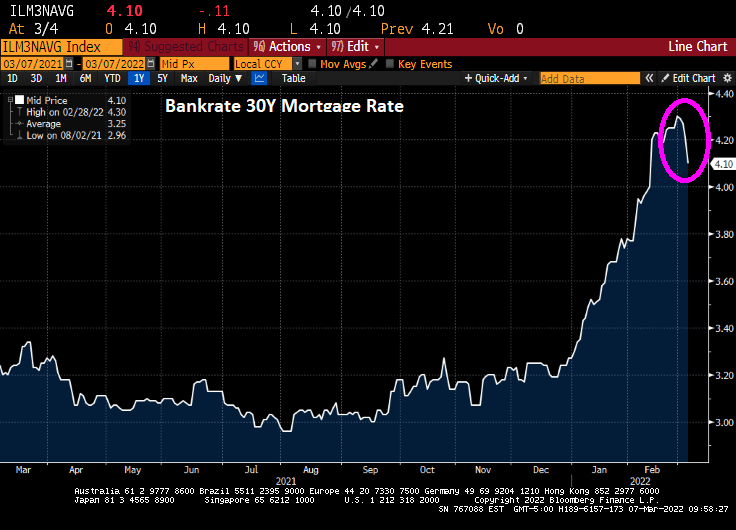

And Bankrate’s 30Y mortgage rate declined to 4.10%.

Russia is the world’s largest exporters of wheat and Ukraine is the 5th largest exporter.

You must be logged in to post a comment.