James Carter (no, not Mr. Peanut, the smart one at America First Policy Institute’s Center for American Prosperity) had a nice op-ed on American Thinker entitled “The Biden Administration’s Budget Hypocrisy.”

The Biden administration’s claims of deficit reduction come in stark contrast to the president and his team, having added $4.8 trillion to the deficit through 2031.

You might call anyone uttering such claims a hypocrite. As Adlai Stevenson, the grandfather of the future Illinois governor and two-time presidential candidate of the same name, reportedly quipped: “A hypocrite is the kind of politician who would cut down a redwood tree, then mount the stump and make a speech for conservation.” Sounds about right.

Why does this matter? It matters because President Joe Biden fancies himself a champion of deficit reduction. As he bragged in a “60 Minutes” interview last month, “By the way, we’ve also … reduced the deficit by $350 billion my first year. This year, it’s going to be over $1.5 trillion, reduced the debt.”

But the president’s attempts to redefine his reckless spending as deficit reduction don’t end there. According to The Washington Post, “Just in the week before the 60 Minutes interview, the president mentioned having reduced the budget deficit by $350 billion six times, sometimes saying he wants to counter accusations that he’s running up the federal tab.” (emphasis added)

What the president fails to mention, however, is that this near-term deficit reduction has nothing to do with him or his administration. Instead, it’s the result of emergency COVID-19 spending that is now ending as planned.

Maya MacGuineas, president of the nonpartisan Committee for a Responsible Federal Budget, points out what the Biden administration is loath to admit:

“The White House has been trying to paint President Biden as the champion of prudent economic stewardship. Biden’s ‘record on fiscal responsibility is second to none,’ it asserts. As temporary covid measures end — and record-high deficits predictably decline — the administration is congratulating itself for that supposed achievement.

But the administration’s record is, sadly, the opposite of what it argues. Since entering office, the president has approved policies adding $4.8 trillion to the deficit over the next decade. This is an extraordinary sum, which makes it all the more astonishing that the administration would try to pull off this claim.”

According to the Office of Management and Budget, even if the 117th Congress had enacted the Biden administration’s fiscal year 2023 budget in its entirety, net interest costs would more than triple from $352 billion in 2021 to $1.1 trillion by 2032. Is a tripling of future net interest costs something typically associated with an administration committed to tackling the federal budget deficit? No.

President Biden’s rhetoric aside, his mid-session budget review forecasts endless $1 trillion-plus annual deficits totaling more than $14 trillion over the coming decade. Even adjusted for inflation, these deficits would be among the largest ever generated by the federal government. Is that “fiscally responsible?” No.

President Biden is not serious about reducing the deficit. He claims progress on the deficit but obscures the facts that every American should know.

Not only does President Biden fail to try to balance the budget, but he actively pursues policies that he must know will balloon federal spending and deficits.

No, but Biden and Congress are serious about bankrupting the US Treasury and moving to a Socialist model.

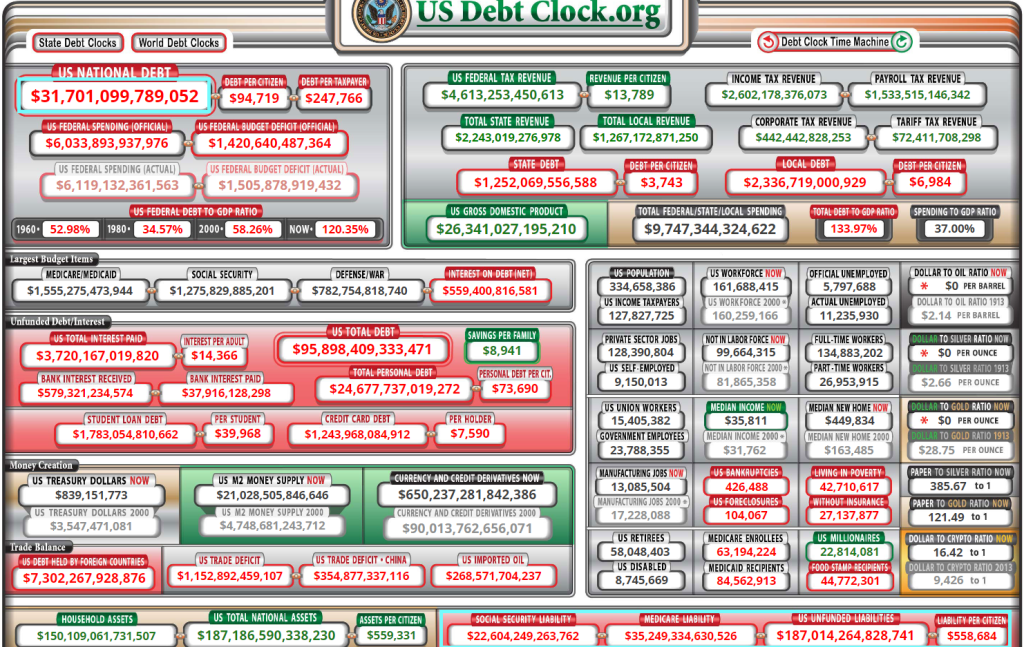

And what even James Carter doesn’t mention is the staggering levels of UNFUNDED LIABILITIES of $187 TRILLION. The question for Biden is …. how are deficits and the massive debt going to play out when we are on the hook for $187 TRILLION?

I am sure that Bernie Sanders, Elizabeth Warren and The Squad will suggest much higher taxes to cover it. And remember, Biden was the idiot that helped taxed Social Security for seniors. And he has also worked towards cutting Social Security and Medicare in the past.

The only out is 1) default on the US debt which would be catestophic and 2) renegging on the massive unfunded liability load. Remember, France is rioting over raising their retirement age by 2 years. Let’s see if Americans riot over inevitable cuts to Social Security, Medicare and Medicaid.

Cut mandatory spending without riots? Please.

The theme song of Biden’s insane, economy destroying, inflation creating budget should be “Keep on printing!”

Yes, this is Government Gone Wild! But no pics or videos of ancient Congress members like Warren or President Biden, please.

You must be logged in to post a comment.