Biden Press Secretary KARINE JEAN-PIERRE: “The American people are beginning to feel Bidenomics”

Prices are up 16.6% and real wages are down 3% since Biden took office.

Well, at least Jean-Pierre didn’t claim like her boss Joe Biden claimed that he “ended cancer as we know it.”

But getting back to Jean-Pierre’s claim that “The American people are beginning to feel Bidenomics.” She is right (for once). Americans are REALLY feeling Bidenomics. And it hurts SO BAD!!!

What hurts so bad? Food (CRB Foodstuffs) are up 56% under Bidenomics. Real weekly wage growth is down -90% since Biden assumed office. Regular gas prices are up 52%. And the 30Y mortgage rate is up a staggering 153%. Yes, Karine, this hurts so bad!

While real wages are down -3% under Biden and the real average weekly wage growth is down -90%. That REALLY hurts so good.

Jared Bernstein was VP Joe Biden’s former Chief Economist and is now chair of the United States Council of Economic Advisers. Pretty impressive! Except that Bernstein is not really an economist. He has a PhD in social welfare from Columbia University. In other words, Bernstein is a Progressive Marxist cheerleader, not a real economist. Perfect for The Biden Adminstration where they installed a small town Mayor with no experience (Buttigieg) as Transportation Secretary.

BERNSTEIN: “Yes, it depends on what your benchmark is.”

Bernstein’s answer reminds me of the infamous reply of President Clinton about having sex in the Oval Office with Monica Lewinsky: “It depends on what the definition of sex is.”

Well, Jared, here is the data.

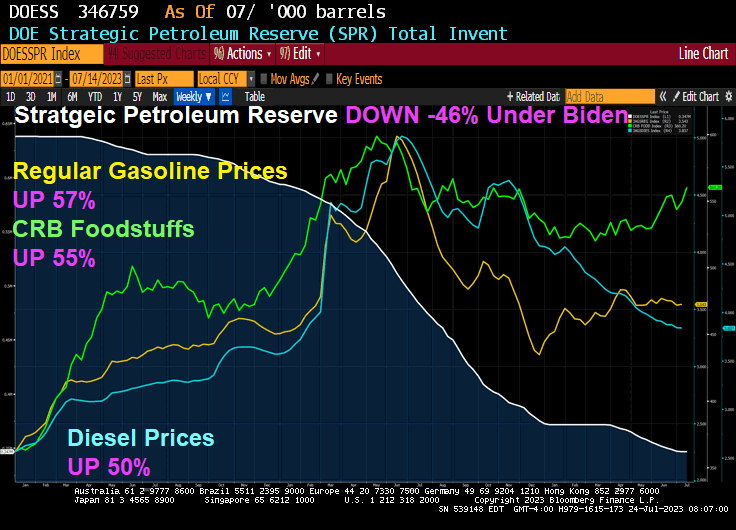

Since January 2021, regular gasoline prices are up 57% under Biden’s and Bernstein’s Reigns of Error. CRB Foodstuffs are up 55% under Clueless Joe and Diesel prices 50% under Bully Biden. Meanwhile, the Strategic Petroleum Reserves is DOWN -46% under Hidin’ Biden.

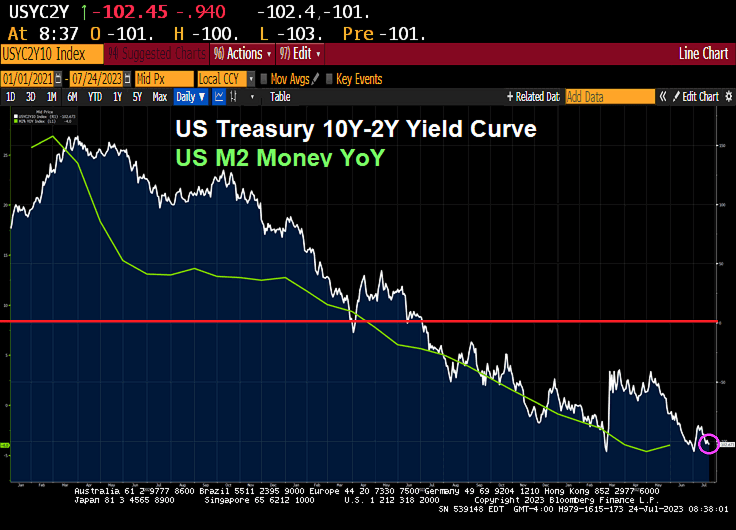

Meanwhile, the US Treasury 10Y-2Y yield curve has inverted to -102.45 as it does prior to a recession. I would love to hear “economist” Jared Bernstein explain that!

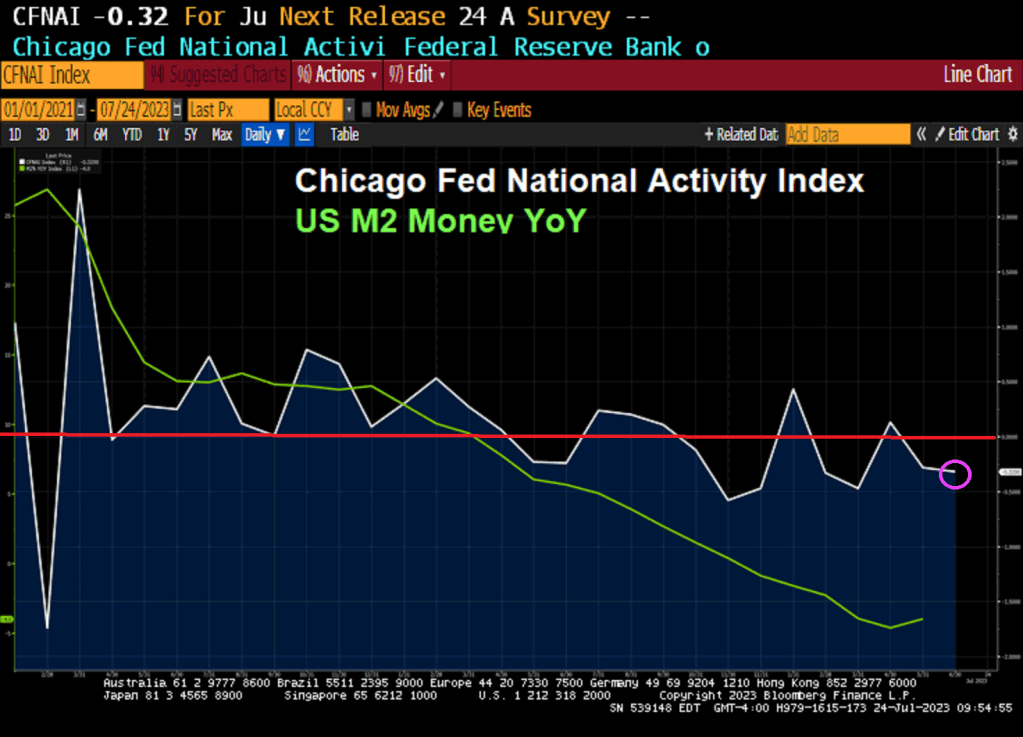

The Chicago Fed’s National Activity index fell to -0.32 in June. That is negative readings for 6 of the last 8 months.

The Fed still hasn’t removed its monetary stimulypto from the market.

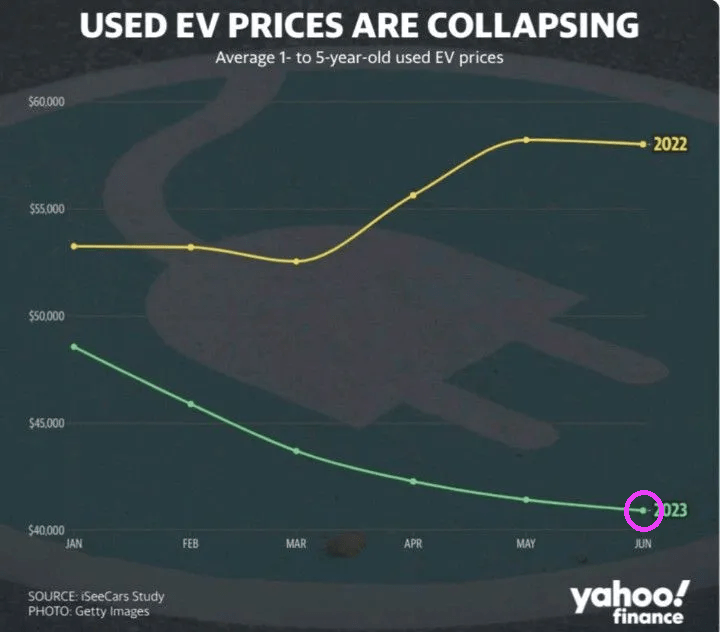

Yes, one of the cornerstones of Bidenomics is the massive expansion of (impractical) electric vehicles (or EVs). You know, those mondo expensive cars that run out of power after a couple of hundred miles requiring a lengthy recharge (kind of makes long distance trips the domain of Internal Combustion Engine (ICE) cars.

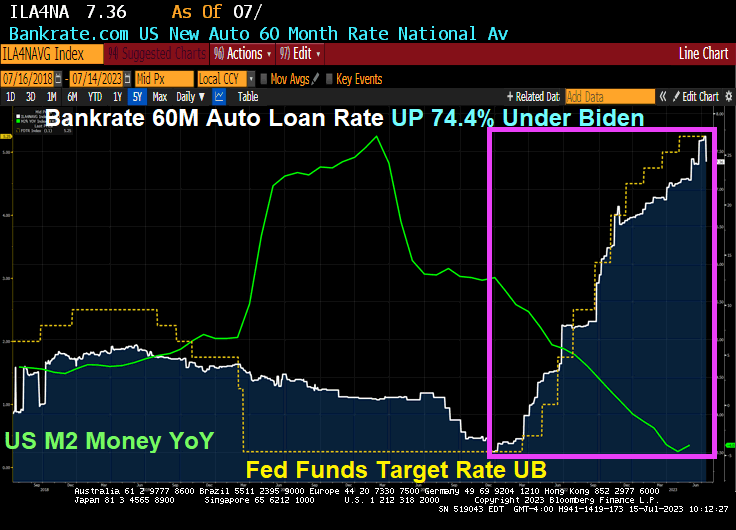

But as Biden/Congress spent trillions on green energy (massive subsidies for anything green), we noticed that 1) inflation hit 40 year highs and 2) The Fed intervened to raise rates. So, now we see that 60-month auto loan rates are now around 7.36%, up 74.4% under “Middle Class Joe.”

And we see used EV prices collapsing like a week-old soufflé.

Speaking of green energy fraud, here is the leader of the green energy fraud movement, John F’ing Kerry. Aka, Heinz Planes Grifter.

I could have used 3 shades of Joe, but 50 shades of Joe sounds better!

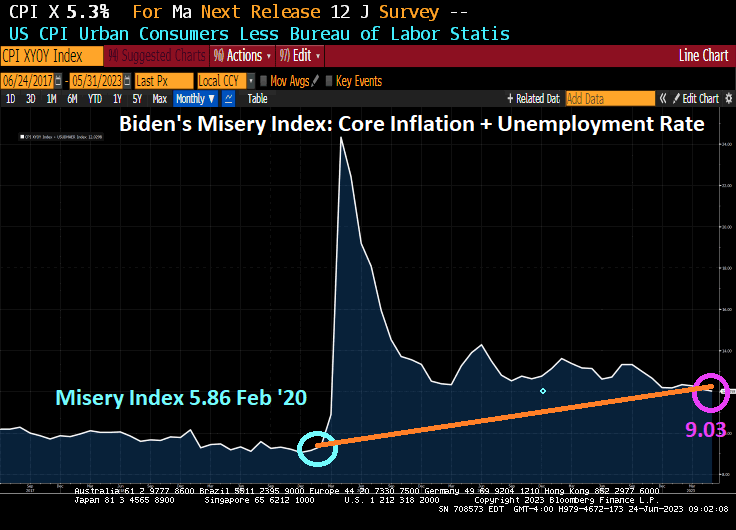

But the fact remains that Americans are far more miserable under Biden than they were under Trump before the Chinese Wuhan Covid virus was unleashed. 9.03 today (Core CPI YoY + U-3 Unemployment) than it was in February 2020 under Trump (5.86). While not twice as bad, inflation is continues to cause serious problems for America’s middle class and low-wage workers.

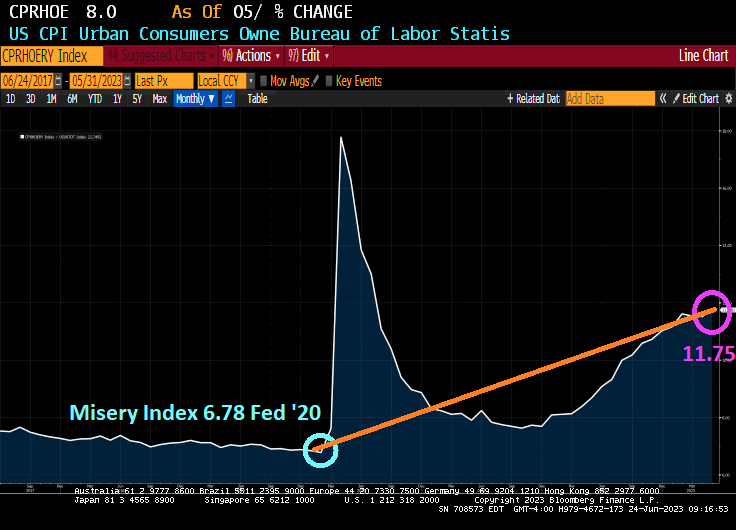

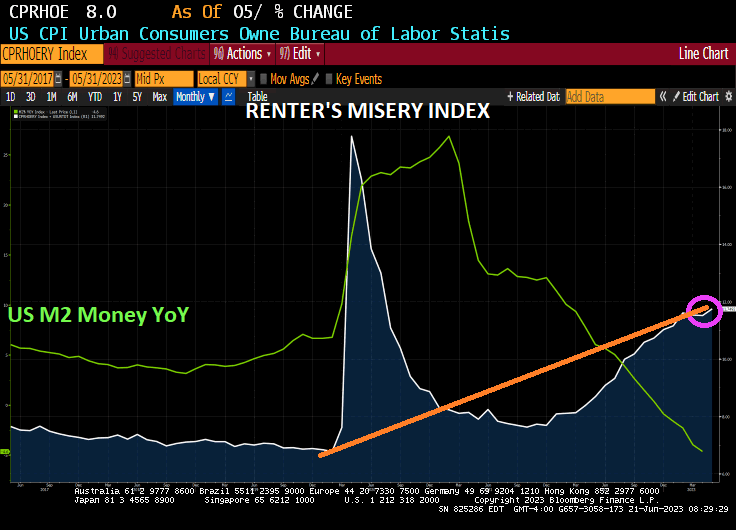

Speaking of the middle class and low wage workers, let’s look at the Renter’s Misery index (CPI Owner’s equivalent rent YoY + Unemployment rate). It was 6.78% in February 2020 under Trump and before Covid struck and is now 11.75% under Inflation Joe.

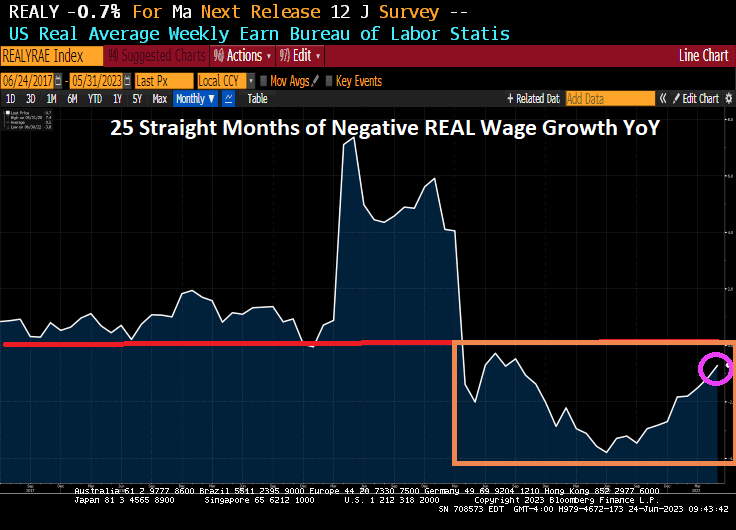

Speaking of misery, how 25 straight months of negative REAL wage growth? Real weekly wage growth went negative in April 2021, just a few months after Biden was installed as President.

Now, there was winners under Biden. Green energy donors, the big banks, big pharma, big tech, but media … essentially any big donors from big entities got massive payoffs. The middle class and low-wage workers? As Jerry Reid once sang, “They got the coal mine and we got the shaft.”

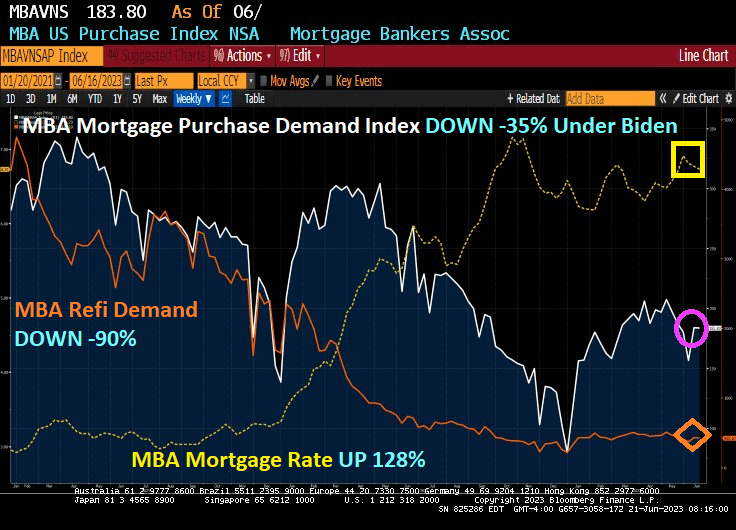

The good news? Mortgage purchase demand fell only -0.05% from last week. The bad news? Mortgage purchase demand is down -35% since Resident Biden was sworn in. And mortgage refinancing demand is down a whopping -90%. Reason? Mortgage rates are up 128% under Clueless Joe.

Mortgage applications increased 0.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 16, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 0.5 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 1 percent compared with the previous week. The Refinance Index decreased 2 percent from the previous week and was 40 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index decreased 0.1 percent compared with the previous week and was 32 percent lower than the same week one year ago.

And as Paul Harvey used to say, here is the rest of the story.

And the renter’s misery index, CPI for owner’s equivalent rent YoY + U-3 unemployment rate, is now a staggering 11.75% verus 6.78% in February 2020, the last month before the Chinese Wuhan virus led to economic and school shutdowns. And we have Donald Trump as President instead of this corrupt clown.

What is the difference between baseball legend Shoeless Joe Jackson and Clueless Joe Biden? While both sold out their teams for personal wealth, at least Shoeless Joe was good at baseball. Clueless Joe is a corrupt bully. Shoeless Joe was allegedly stupid, but so is Clueless Joe.

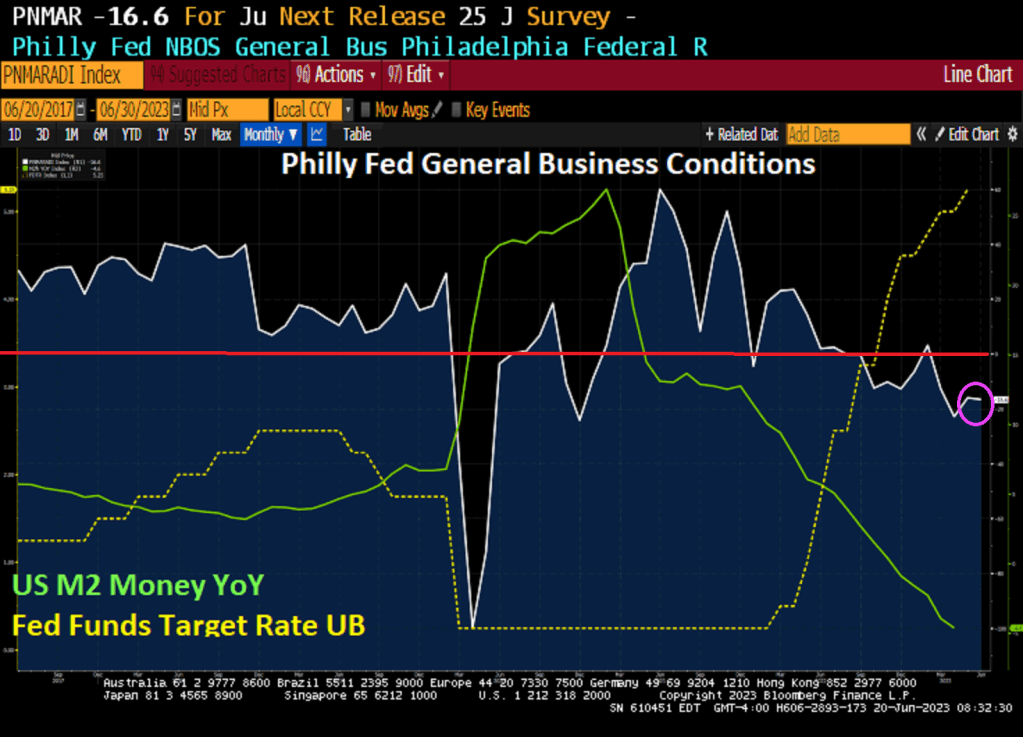

Now we have more evidence of an impending recession with the Philly Fed General Business Conditions index falling to -16.6 in June as Green Man (M2 Money growth) stalls.

Federal Reserve Chair Jerome Powell (aka, Green Man) will have an opportunity this week to clarify what many found a confusing message on the path of interest rates, with the added task of assuring Democrats and Republicans the economy is on track.

The Fed chief will face questions from lawmakers on Wednesday and Thursday, his first testimony on Capitol Hill since early March, before banking-sector turmoil prompted sharp criticism of the Fed and forced officials to rethink their policy strategy. Since then, the most acute financial strains have eased, but questions remain about the extent to which tighter credit will weigh on the economy, and what that means for the Fed.

Powell will need to reassure Republicans the Fed is not backing down from its campaign to contain price pressures, while pointing Democrats to the resilience of the economy as officials prepare to raise rates further this year.

“The Democrats are nervous because they would rather declare victory and move on,” said Stephen Myrow, a managing partner at Beacon Policy Advisors and a former George W. Bush Treasury official. “I think they’re going to try to caution this time against further increases. But Republicans are just going to hammer away and act like inflation hasn’t come down.”

Powell will be fresh off the Fed’s June 13-14 meeting, where he and his colleagues left rates unchanged for the first time in 15 months but signaled they may deliver two more hikes this year. Fed watchers and investors struggled to digest the message from Powell’s post-meeting press conference, and lawmakers last week said they planned to press him for an explanation.

“Right now there’s a lot of confusion about the next step,” Thom Tillis, a Republican senator from North Carolina, said Thursday.

Well, Senator Mel Tillis, there is no confusion. The DC Elites and Big Banks don’t want to disrupt the flow of money to the political donor class (including China and Ukraine payments to Biden’s family, now up to $30 million). The Fed may raise rates one more time and claim victory again their “War on Inflation!” then start cutting again as the Presidential election approaches.

While the children in Congress and the Administration argue about cutting the Fedcral budget (as if there isn’t trillions of dollars of wasteful spending in the budget), we saw an even dumber suggestion from Pramila Jayapal (WA-D), Adam (Shifty) Schiff (CA-D) and Sheila Jackson Lee (TX-D): a bill to eliminate the debt ceiling altogether to allow unlimited Federal spending. That reminds me of the Tom Arnold/Julie Ford film “The Stupids.” Yet these clowns keep getting re-elected.

In any case, The Federal Reserve’s quantitative-tightening program risks being propelled toward an early end as US politicians bicker in Washington over raising the national debt limit, according to some economists and bond-market participants. As of this morning, the US credit default swap (1-year CDS) remains elevated signaling a positive probability of a US debt default. (CDS represents the price of insuring against a default).

But notice that The Fed still has $8.5 TRILLION in assets (largely Treasuries and Agency MBS) on their balance sheet. But The Fed’s plans to continue shrinking their balance sheet will be put on hold (and if fact will be reversed) if Democrats and President (10% for the big guy) Biden don’t budget on cutting some of the enormous fat from the Federal budget.

Newly-minted US House Speaker Kevin McCarthy faces a daunting task: trying to avoid a US debt default. As I have discussed many times before, nothing has been the same since the US housing bubble and near-collapse of the banking system that produced an expensive bailout of seemingly all financial institutions. After 2008, Federal spending has gone out of control. The budgetary hawks (or pigeons) in the US House of Representatives (with Pelosi, Boehner, Ryan then Pelosi again) went on Federal spending sprees of epic proportions.

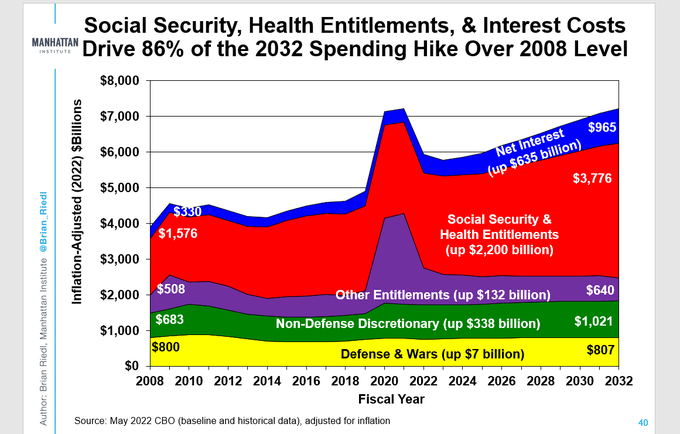

The Manhattan Institute has a nice chart showing the explosion in the Federal budget since 2008. Of particular note, interest payments on the Federal debt has increased by a staggering 192%. On the non-interest spending front, Social Security and Health Entitlements have increased by 140% while Nondefense Discretionary Spending has increased 76%.

The massive increase in Federal debt interest is due to both increased Federal spending and rising interest rates thanks to The Federal Reserve raising rates to fight inflation.

But what will McCarthy and House Republicans recommend cuts in? Tighter restrictions on who qualifies for Social Security and particularly Social Security Disability payments?

The odd factoid is that Defense and Wars budget is up less than 1% from 2008 to 2032. So, Ukraine military aid is coming from somewhere, but not from the Defense budget. Is Ukraine another entitlement program?

Rest assured that after debate, the House will pass a budget and, provided that virtually nothing was cut, the Senate will gleefully agree to more spending and “Top Secret Documents” Biden will sign it.

After he parks his gorgeous Corvette Sting Ray, that is.

The US Producer Price Index (PPI) final demand rose 10% YoY in February, further evidence of spiraling inflation under Biden/Pelosi/Schumer’s reign of error.

And speaking of Senate Majority Leader Chuck Schumer (D-NY), the Empire State Manufacturing Survey (General Business Conditions) crashed to -11.8.

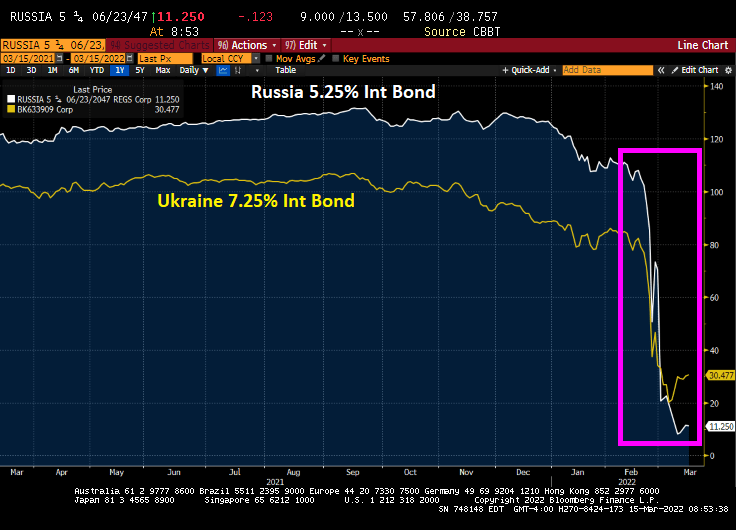

And Russia is losing the economic demolition derby with Ukraine (at least for sovereign debt).

I am still trying to figure out what House Speaker Nancy Pelosi (D-San Francisco) meant by “When we’re having this discussion, it’s important to dispel some of those who say, well it’s the government spending. No, it isn’t. The government spending is doing the exact reverse, reducing the national debt. It is not inflationary.”

Really Nancy?

Here is a chart of Federal government outlays and inflation. Massive expenditures and growth in Federal debt and the resulting inflation. Nancy?

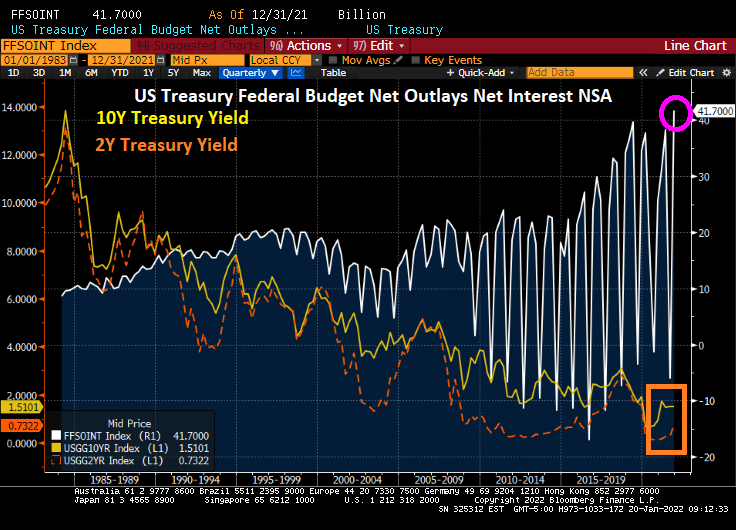

Treasury Secretary Janet Yellen is having trouble with the curve (yield curve, that is). It keeps inching up, meaning that Treasury’s cost of debt financing is inching up too.

As Treasury yields keep rising, so does the problem of financing the massive Federal debt load. Here is a chart showing the interest outlays in the Federal budget against the cost of Federal funding at the 10-year and 2-year tenors.

Now, The Fed is predicted to raise their target rate 4 times in 2022 (according to Fed Funds Futures data) and it looks like a whopping 100 basis points (or 1%). Holding the rest of the yield curve constant, this will considerably flatten the 10Y-3M Treasury curve. Resulting in a more expensive refinancing of the Federal Debt load.

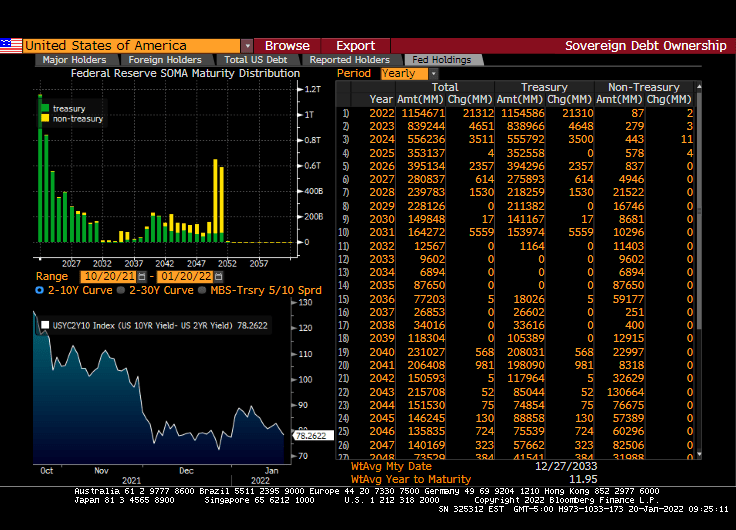

If we look at The Fed’s System Open Market Holdings (SOMH), we can see that The Fed’s holdings are primarily Treasuries with non-Treasuries (primarily agency mortgage-backed securities) not maturing (or running off) until 2050.

The majority of The Fed’s COVID expansion was picked-up by The Fed (light blue line).

How about the Treasury Inflation-protected Securities curve? Negative yields across the tenor range.

With Congress trying to spend trillions more (since Build Back Broke failed, Democrats are producing MORE spending legislation with the voting act included, of course), Treasury is going to have progressively more trouble with the (Treasury) curve.

You must be logged in to post a comment.