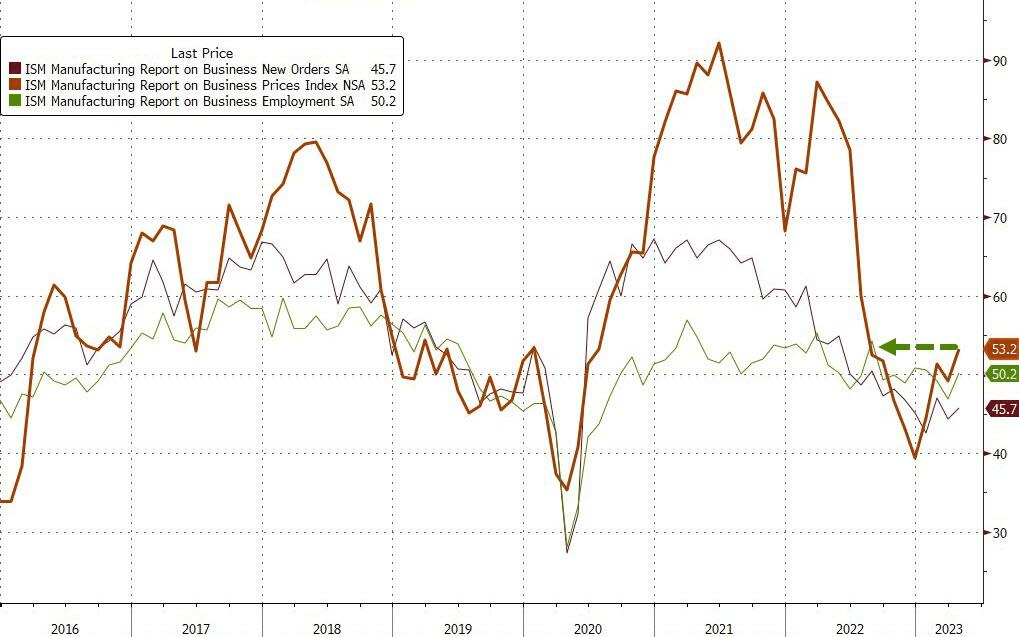

Ah, that wonderful economy O’Biden talks about. It is actually shrinking.

The ISM Manufacturing index screams stagflation, as it continues to contract. With “reigniting inflationary pressures.

And prices are beginning to take off again.

Confounded Interest – Anthony B. Sanders

Financial Markets And Real Estate

Ah, that wonderful economy O’Biden talks about. It is actually shrinking.

The ISM Manufacturing index screams stagflation, as it continues to contract. With “reigniting inflationary pressures.

And prices are beginning to take off again.

Thanks to O’Biden (Obama/Biden) and Senate Majority Leader Chuck Schumer’s failure to negotiate a debt ceiling increase, the US has officially become a banana republic. Crazy government, lawless censoring and arrest of opposing political candidates.

The US CDS 1Y SR Eur just hit a staggering 176.53. That is the price of insuring against a debt default by O’Biden and Treasury Secretary Janet Yellen.

Is a US debt default likely? It shouldn’t be. But you never know with the circus clowns in the White House and nasty Chuck Schumer. But arresting the leading Republican Presidential candidate before the elections is pure Chavez/Maduro Banana Republic politics.

2 year Treasury yield up over 11 basis points today.

From ZeroHedge, here is a tantalizing story … behind a pay wall. But here is the gist of what I think the article says. Or at least my spin on it.

Here is a chart of US office vacancies nationally (yellow), New York (white), San Franciso (green) and Los Angeles (orange). Note the rapid decline in office vacancies just prior to the financial crisis (often mislabeled as the subprime mortgage crisis). Then look at office vacancies after The Fed’s massive monetary experiment of setting rates to near zero and buying a ton of Treasuries, Agency MBS. etc. While San Francisco returned to pre-financial crisis levels of office vacancy, in general the office market never fully recovered.

And then “the slammer” struck: the COVID economic shutdowns. After 2020 shutdowns, office vacancy rates rose dramatically. Two complicating factors: 1) the US moved to working at home rather than commuting to an office and largely remains that way. 2) crime is going bonkers in American cities, particularly New York, Los Angeles and San Francisco (don’t worry, I haven’t forgotten about other gang nests like Chicago and Detroit). I saw that California’s woke governor Gavin “Nancy Pelosi’s nephew” Newsom said the word “gang” then apologized and replaced it with “organized groups.” No wonder Newsom can’t fix anything, but he is running for President of the US! (insert Edvard Munch’s “The Scream” painting here,)

The Fed responded to the financial crisis by lower rates to 25 basis points and printing a boat load of money. Unfortunately, office vacancies rose to a peak in October 2010 then began falling again. Only to start rising again after Trump took office in 2017. Alas, Covid struck in 2020, The Fed and Federal government panicked. States and local governments (not to mention teacher’s unions) shut down economies and schools. Office vacancies are now higher than at peak of the Covid shutdowns!!!

But never fear! Too low for too long (TLFTL) Fed Chair Janet Yellen is back as Biden’s Treasury Secretary. To royally screw things up even more.

Consumer considence (according to the Conference Board) remains below pre-Covid levels despite the massive Federal spending spree and Fed money printing).

I feel like I am watching the Star Trek original series episode “The Doomsday Machine” as former Fed Chair and current US Treasury Secretary effectively just guaranteed ALL US bank deposits. Aka, a massive bank bailout. The episode was about a robot space vehicle that destroy planets … and anything in its path. And if it changed course to destroy something, it gradually returned to its original destructive path. Like The Federal Reseve.

But after a few days of declining Treasury yields because of the mess created by Bernanke/Yellen’s too low for too long policies, and the Biden/Congress insane spending, the US Treasury 2-year yield is up 16.1 basis points.

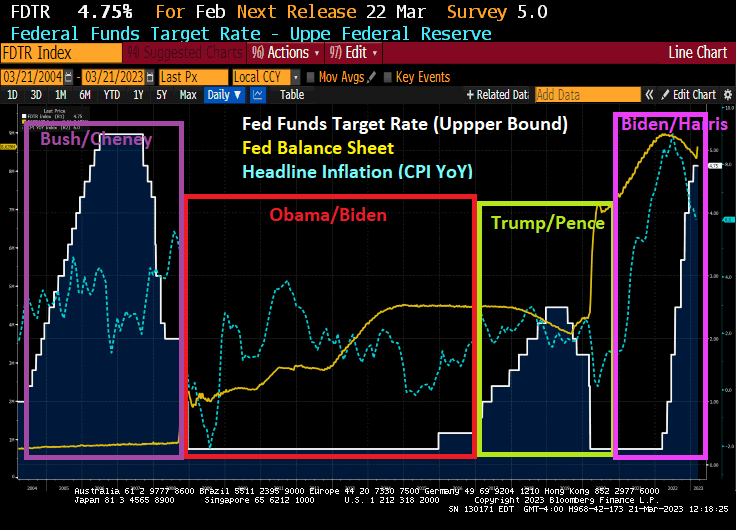

Whether it was politcally motivated to protect Obama/Biden or Obama/Biden’s economic recovery was terrible, The Fed only raised their target rate once before Trump’s election. And then Yellen raised rates like crazy. Only to hand her mess off to Powell who had to drop rates like a rock and massively expand the balance sheet … again … to fight Covid.

The Federal Reserve from a car on Constitution Avenue in Washington DC.

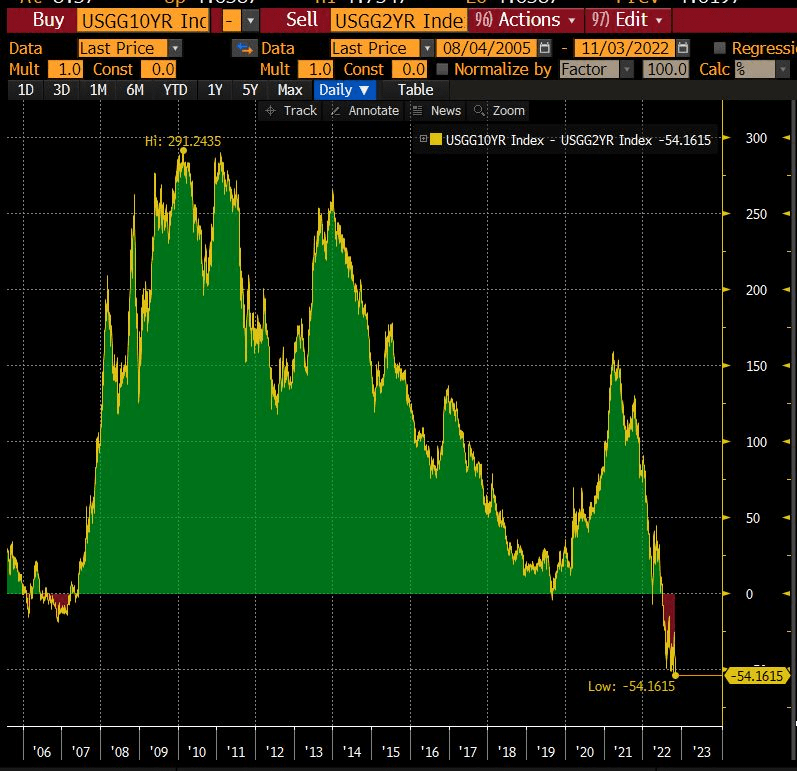

The US Treasury 10y-2y yield curve descended further into inversion at -82 basis point, the worst since 1981.

This is not a good sign, since the 10Y-2Y curve typically inverts just prior to a recession.

The current US Treasury curve is currently humped at 1 year, then declining rapidly. The swaps curve is peaking at 9 months, then declining rapidly.

The Fed Funds Futures market is pointing to a peak Fed Funds rate of 5% at the May 3rd FOMC meeting.

Yes, a recession is headed our way.

Even Joe Biden’s hate speech towards Republicans can’t mask the horrid inflation on his watch. As if Biden watches anything other than ice cream cones.

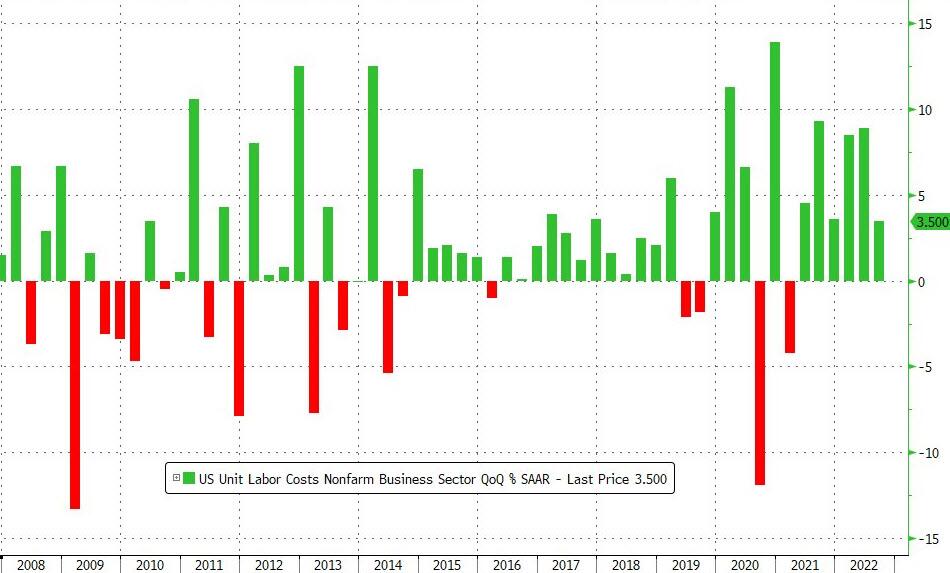

On a YoY basis, US Productivity is down for the 3rd straight quarter (and 4th quarter of the last 5).

On the mirror image of productivity, unit labor costs rose 3.5% QoQ (a notable slowing from the 8.9% QoQ growth in Q2). This was the 6th quarter in a row of rising unit labor costs (but was less than the +4.0% QoQ expected)…

However, on a YoY basis, that is the fastest growth since Q3 1982.

Yikes! The 2s10s Yield Curve Inversion Is the worst since the 1980s.

One of my friends on Wall Street wrote my yesterday claiming “The 10-year Treasury yield is set to crash. Brace for impact!” Then I logged into Bloomberg this AM and saw the 10-year Treasury yield up almost 10 basis points (although it is down -2 BPS at 10:20am). Did markets not read his comments?? Maybe they did!

Well, The Fed is doing the Tighten Up. That is, The Fed is FINALLY removing their excessive monetary stimulus left over from the Bernanke Blowout (2008 adopting Japan’s print ’till you drop model).

But as The Fed removes their monetary stimulus (rate increases), we are seeing negative effects in the housing market. I call this chart “The X Factor.”

The US Treasury 10-year yield is up to 4.3% this morning, a far cry from 1.804% when Biden was crowned as President on January 20, 2021. The 30-year mortgage rate is up from 3.67% on Coronation Day to 7.32% yesterday, an increase of … 100% (that is, the 30-year mortgage rate has doubled under Biden). At the same time, Existing Home Sales YoY have gone from -2.41% in January 2021 to -23.79% in September 2022. THAT is a HUGE decline!

University of Michigan’s consumer sentiment for housing for 77 in January 2021 to 39 in November 2022. That is a -49% decline in consumer confidence. Also a big decline.

But going back to my pal’s email, he also said that The Fed is unwinding its balance sheet at a dangerously rapid rate (orange line). Relative to just increasing it, I would agree with him. But The Fed’s balance sheet is barely declining to my eyes. The troubling thing for housing is that inflation is so hot that REAL average hourly earnings YoY (yellow line) has fallen from +0.24% growth YoY on January 25, 2021 to a horrific -2.80% YoY rate in September 2022.

While I will not reveal my friend’s name (who works at a famous hedge fund), I will recommend Bill Carson, my former colleague at Deutsche Bank. While we might agree on everything, his site is worthy of a good read.

Bill’s point to me is that lending is still hot (at least commercial and industrial lending or C&I) while The Fed’s balance sheet remains in force (green line).

The Fed has a lot more work to do if they want to cool the commercial lending market. They have successfully slowed down the residential mortgage market.

The US is movin’ on up, to the dark side, while DC elites live in deluxe apartments in the sky. The US is movin’ on up to the dark side, we finally got a piece of the Banana Republic pie. … And its tastes horrible!

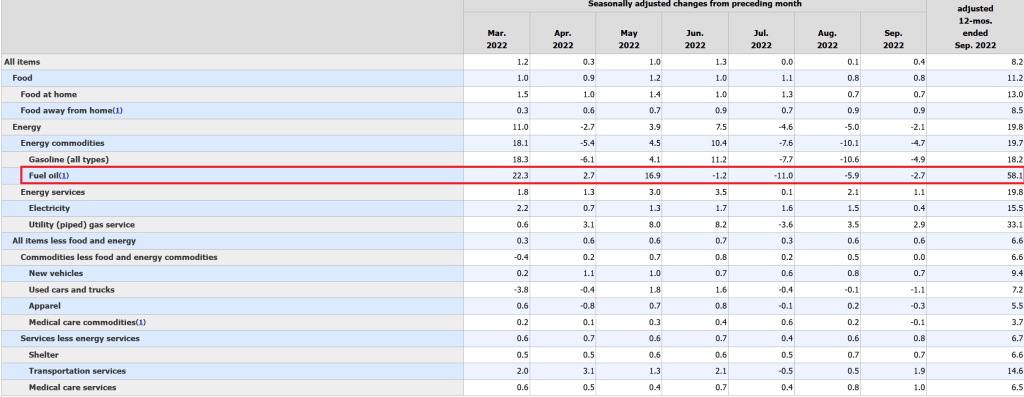

Today, the BLS released its inflation data. And it was terrible.

To begin with, headline inflation remains high at 8.2% YoY while CORE inflation (headline less food and energy) rose to 6.6% YoY.

Meanwhile, REAL average weekly earnings growth YoY further declined to -3.8% YoY.

On the bond front, the Bank of America ICE bond volatility index rose to Great Recession/banking crisis levels (also achieved during the Covid government shutdowns).

But back to the low-ball BLS inflation data. The biggest gain in price is … fuel oil at 33.1% YoY. Food at home rose 13.0% while gasoline rose 18.2%. Rent, according to the BLS, rose 6.6%.

Biden has probably been told by Ron Klain and Susan Rice that this is a good report.

‘‘We will keep at it until we are confident the job (i.e. killing inflation) is done.’’

Jerome Powell, Jackson Hole speech

Interviewer : What’s your prediction for the market?

Clubber Lang (Mr T) : My prediction?

Interviewer : Yes, your prediction.

Clubber Lang : Pain!

Of course, Friday was one of those “Black Fridays” for investors. And pension funds.

The Dow Jone Industrial Average fell -1008.38 points after Powell’s “Mr T” remarks on pain. That was a whopping -3%. The NASDAQ composite index fell almost -4%.

Equity markets struggled in Europe as well, particularly the German DAX index.

The UMich Buying conditions for houses rose slightly, but remains near the lowest level since 1982.

Clubber Powell, Federal Reserve Chairman.

The Case-Shiller house price numbers are due out Tuesday for June and it is expected that they will show a significant slowing in home prices. Biden and Clubber Powell could then take “credit” for slowing “inflation.”

{kind=link}

{kind=link}

You must be logged in to post a comment.