We are living in a banker’s paradise. Where a top administrative official pushes to change forecasts of the economy. Hey, it’s a Presidential election year and literally anything goes.

The disagreement was over forecasts for 10-year Treasury yields in the budget, a linchpin estimate that is intertwined with other measures, like debt service costs.

Forecasts in the president’s budget proposal — scheduled for release Monday — are typically set by Treasury Secretary Janet Yellen, Office of Management and Budget Director Shalanda Young and the chair of the Council of Economic Advisers, Jared Bernstein. The group is known in fiscal circles as the troika.

An October meeting, however, included a fourth invited principal: Brainard, who directs the National Economic Council. Brainard at one point disagreed with Yellen, Young and Bernstein on the 10-year interest rate projections and predicted a slightly lower rate, the people said, speaking on condition of anonymity to detail the discussions.

The difference between the forecasts was modest and both were well within range of private-sector estimates, the people said. The exact scope of Brainard’s changes aren’t clear.

Brainard’s forecast painted a modestly better picture for Biden. A lower interest-rate forecast would have the effect of an improved overall outlook by offering more support for growth and suggesting less concern about inflation. It also would lower borrowing cost projections at a time of rising worries about the US deficit and debt.

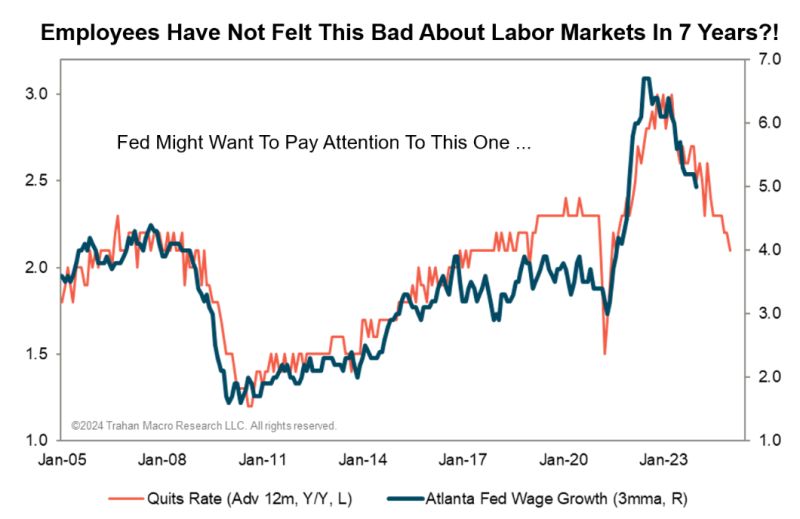

Let’s see what the Troika have to say about the quits rate.

Yes, it is the Ides of March. No, not Nikki Haley trying to sabotage Donald Trump’s campaign after Nikki got clobbered in all but two state primaries. So in a sour grapes move, Haley didn’t endorse Trump. But the Ides of March refers to the stabbing of Julius Caesar (led by Brutus).

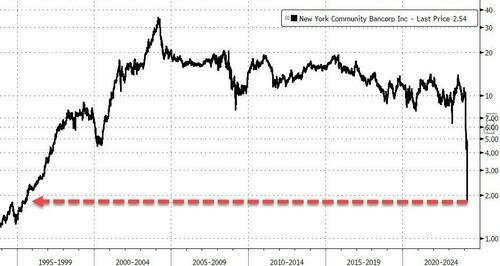

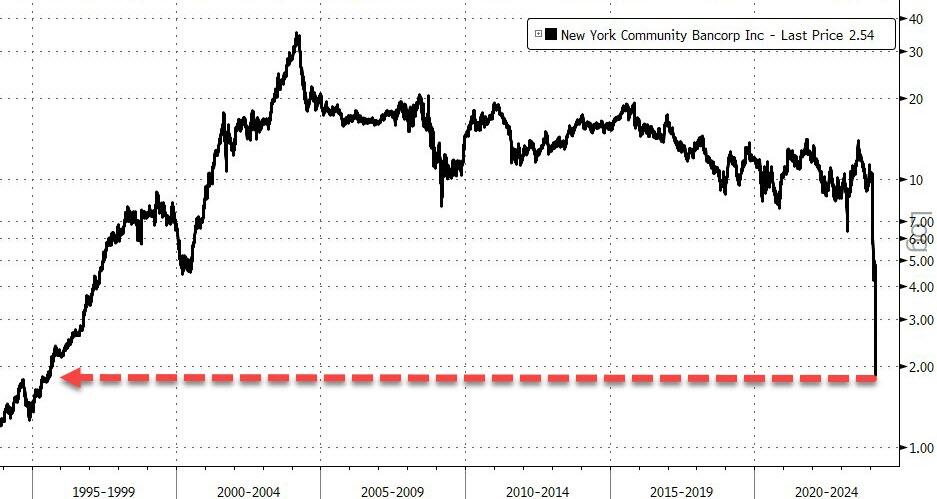

Once the darling of the small banking crisis comeback, New York Community Bancorp has crashed 45% to fresh 30 year lows after The Wall Street Journal reportsthe bank is seeking to raise equity capital in a bid to shore up confidence in the troubled regional lender.

According to people familiar with the matter, NYCB has dispatched bankers to gauge investors’ interest in buying stock in the company.

There’s no guarantee there will be a deal, or that one would succeed in addressing the bank’s challenges, which as of Wednesday morning had led to a roughly 80% decline in its stock price since January.

This is not a good picture for a bank… Would you hold your deposits there?

Last month, DiNello laid out a series of options the bank could explore to bolster its balance sheet, including selling assets from certain non-core businesses. The bank has also considered turning to newfangled financial instruments that would share the risks of those loans with outside investors, people familiar with the matter said.

As WSJ reports, finding takers for those assets, at least at prices that would make a deal worthwhile, has been challenging and U.S. officials have expressed reservations with banks pursuing credit-risk transfers that would shift the burden of potential losses to entities outside of the regulated banking system.

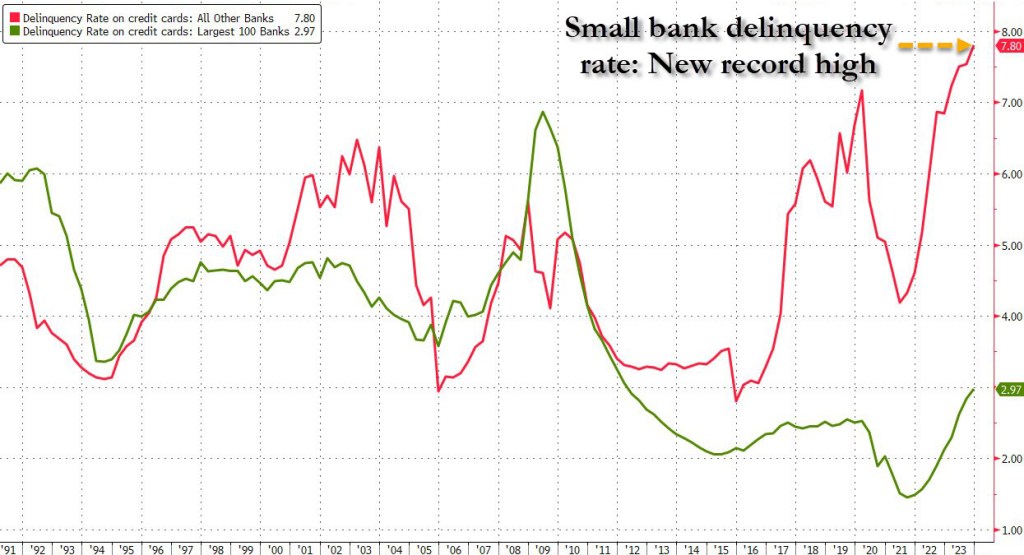

Finally, as a reminder, NYCB is not alone. The red line below shows ‘small banks’ are in trouble absent The Fed’s BTFP facility…

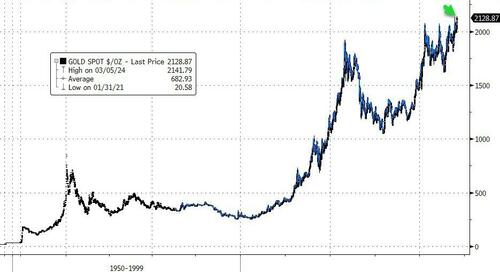

Let’s start with gold. Extending their run of the last few days, spot gold prices just exceeded their all-time highs, topping $2140 for the first time in history…

Source: Bloomberg

A longer view.

Source: Bloomberg

What is gold pricing in about future Fed action? Real rates dramatically negative? As Luke Gromen noted on X:

“When gold rises in your currency DESPITE positive real rates, the gold market is saying ‘Your government will have a debt spiral if real rates remain positive’.“

Source: Bloomberg

Bitcoin just hit $68,567.57, also an all-time high.

The Alt-Assets (gold, silver, Bitcoin) have counterattacked!!

Or as Bonnie Beecher almost sang in a Twilight Zone episode, “Come wander with China Joe Biden.” On The White House lawn. Or wander with The Federal Reserve!

The USA is a runaway train with a dead man (China Joe is about as dead as one can be) in the engineer’s seat.The conductor goes through the cars assuring the passengers that everything is fine. . . never mind the screeching wheels on the curves. . . or the blinding strobe effect of low sunlight passing through the trees out the window at a hundred and forty mph. . . or the bump that made half the stuff in the overhead luggage rack jump out. More than half the people on-board are at tachycardia levels of fright — some are screeching — but the other less than half just remain fixed on their phones and laptop screens. They can’t be bothered to look out the window…

Okay, that’s a metaphor.

But if you’re a citizen of our country and care about it, these are the matters you’d better pay attention to, because they are all going off the rails.

The war in Ukraine. We started it in 2014 to mess with Russia and Russia is going to finish it. Who knows what our real motives were. A resource grab? A desperate ploy to erase our national debt by creating a global fiasco? Sheer psychopathic hatred of this Putin fellow? We can’t bring ourselves to acknowledge the failure of this ill-conceived venture. Instead, our feckless allies in Europe are foolishly rattling their sabers, apparently forgetting that you don’t bring a sword to a nuclear missile fight.

Mr. Macron in France affects to offer up his army for slaughter on the blood-soaked plains of Ukraine, just as the Ukrainians offered up a half a million of their young men so that Victoria Nuland could feel good about herself. Mr. Macron is insane, but the society he presides over is collectively insane, so perhaps he represents them well. Similarly, Olaf Scholz in Germany, whose top generals were caught on a leaked recording last week discussing their plan to blow up the Kerch Bridge that connects Crimea to Russia. Do you understand that this would be a direct attack on Russia, an act of War by NATO? And what the obvious consequence would be?

The phantom government of “Joe Biden” is too weak and mindless to join any negotiation. Ukraine and Russia are up to some kind of cross-talk down in Riyadh with Prince MBS. Even Mr. Zelensky went down for a day, though video appears to show him coked-up, sniffling and snarfling, not a good sign. If ever there was a time to end this stupid conflict, it’s now, before the Russian election. After that, terms will only be more difficult for Ukraine, up to direct custodial supervision instead of remaining a nation. It was never any of our business (though the Biden family, BlackRock, and the CIA saw fabulous opportunity to profit there).

Next is the border. You saw last year how the blob elite greeted the transfer of illegal immigrants to their happy little island of Martha’s Vineyard. (They were not amused by Governor DeSantis’s prank, and off-loaded the mutts post-haste.) But that same smug demographic doesn’t care if hundreds of thousands are distributed to the big cities, which are now fiscally destabilized by them to an extreme, probably to bankruptcy.

Of course, that is not the main thing to worry about with what altogether amounts to millions of border-jumpers flooding our land. The main reason to worry is what the blob that invited them here intends for them to do, which, you may suspect, is to unleash mayhem in the streets, malls, stadiums, and upon our infrastructure just in time to derail the election — perhaps even to make war on us right in our homeland. The US government is paying for this whole operation, you understand, funneling our tax money to international cut-out orgs who set up the transfer camps in Panama, and buy the plane tickets for the mutts to cross the ocean, and coordinate with the Mexican cartels to shuttle this horde of mystery people among us to work their juju for the Democratic Party. The pissed-off-ness of the public has passed the red line on this.

A third FUBAR is the lawfare campaign of the Democratic Party and its regime in power against the citizens of this land. This folder includes overt and obvious political prosecutions by DA’s and AG’s who make election promises to “go after” individuals without such niceties as probable cause. It includes the gigantic new scaffold of inter-agency censorship and propaganda. It includes the psychopathic struggle sessions mandated by “diversity and inclusion” policy. It includes election-rigging directed by the likes of Marc Elias and Norm Eisen, getting states to fiddle laws on voter ID and mail-in ballots. It includes the political protection of rogue groups ranging from looter flash-mobs to Antifa anarchists who bust up things and people and burn buildings down. It includes state officials who peremptorily kick candidates off the ballot. It includes a nakedly biased judiciary, and especially the use of the DC federal district court to punish people extralegally, unjustly, extravagantly, and cruelly. In short, lawfare is the complete perversion of law, and we-the -people are entreated by reprobate officials such as Merrick Garland and Letitia James to accept it.

A fourth item on this list is the US economy which has been overwhelmed by maladministration of an overgrown monster bureaucracy, and the gross (perhaps fatal) mismanagement of the government’s money. The people of this land are not being allowed to do business, to find a livelihood, to transact fairly. “Joe Biden’s” shadow string-pullers are messing as badly with the oil and gas producers as they have messed with Ukraine. And they are doing it in pursuit of a laughable mirage: their “green new deal.”

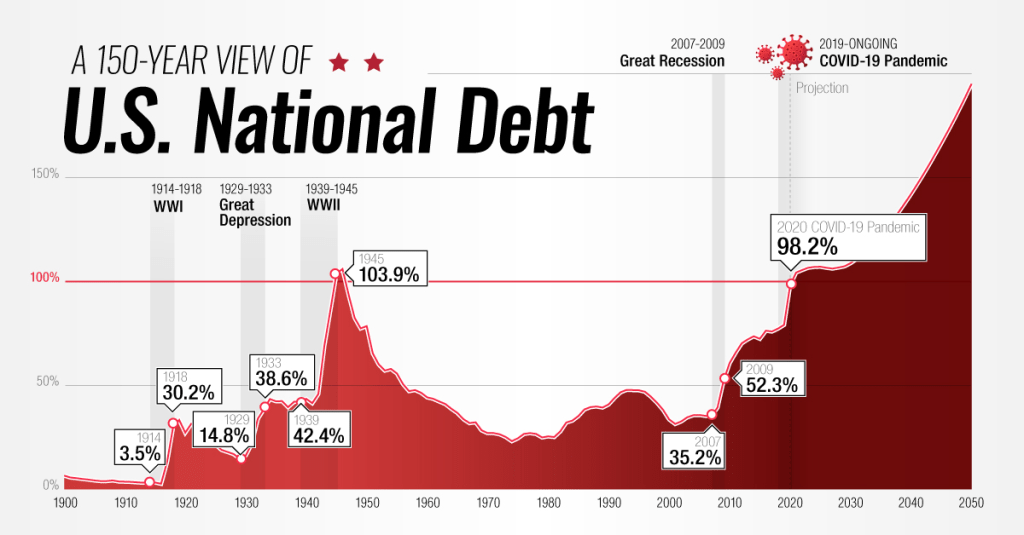

John Podesta, the “clean energy czar” who replaced the Haircut-in-search-of-a-brain called John Kerry, sits on a $370-billion slush fund that can be used to just dole out to anyone and everyone a political patronage payoff, especially to janky “community” orgs and NGOs with fake agendas. This really just amounts to an asset-stripping operation that will leave the American people busted and with broken supply chains for everything. Instead of annual budgets, Congress raises the US debt ceiling by “continuing resolutions” to keep the government from shutting down. The national debt races to the $35-trillion mark. As interest rates on debt rise, our debt payments now exceed our military spending. You can be sure that our country will break down financially very soon.

The capper on today’s list is the nation’s health, the racketeering system we’ve set up to care for it, and the public health agencies of the government that enabled the Covid-19 operation to happen. The CDC continues to push vaccines that have killed millions of Americans and more millions around the world, and has probably compromised the well-being of millions more going forward. Corporate medicine — that is, your doctor, and your hospitals — is a sinking Titanic of grift and chaos. Try to get an appointment to even see a doctor for an emergency. Try to avoid being bankrupted by your treatment. Try to get out of a hospital alive. Yeah, it’s that bad.

The doctors have surrendered your trust in them with their lying and their bullshit. The current director of the CDC, Mandy Cohen and her predecessor, Rochelle Walensky, have knowingly presided over the mass killing and injuries imposed on the mRNA vaccinated. Hundreds of their deputies should be liable for prosecution, and so should many of the other prominent characters in the Covid Saga: Fauci, Birx, Collins, Baric, Bourla, Daszak, Califf, Woodcock, Hahn, and many more.

What are we going to do about any of this? Return to the metaphor. The runaway train is still picking up speed. You can’t just jump off at 150 mph. If you’re one of the passengers watching this in horror, maybe you can decouple your car, or get the conductor to do it by any means necessary. Let’s say that each car behind the engine of this train is a state of the United States. Let the engine up front with the dead man at the controls ride that runaway to its terrible conclusion. Cut loose the cars behind it to take care of themselves, to slow down, get a grip on their situation, and make plans to find a better engine to pull the train. Decouple. Cut loose. It’s the only way.

First, online shopping has crushed retail commercial space. Second, crime is rampant in The Big Apple. A slowing economy is contributing to the malaise in commercial real estate (CRE).

According to Bloomberg, Canadian pension funds – which until recently had been among the world’s most prolific buyers of real estate, starting a revolution that inspired retirement plans around the globe to emulate them because, in the immortal words of Ben Bernanke, Canadian real estate prices never go down…

Canada Pension Plan Investment Board has recently done three deals at deeply discounted prices, selling its interests in a pair of Vancouver towers, and a business park in Southern California, but it was its Manhattan office tower redevelopment project that shocked the industry: the Canadian asset manager sold its stake for just $1. The worry now is that such firesales will set an example for other major investors seeking a way out of the turmoil too, forcing a wholesale crash in the Manhattan real estate market which until now had managed to avoid real price discovery.

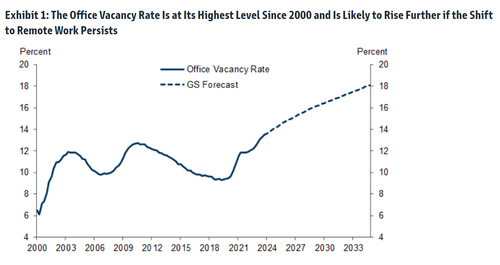

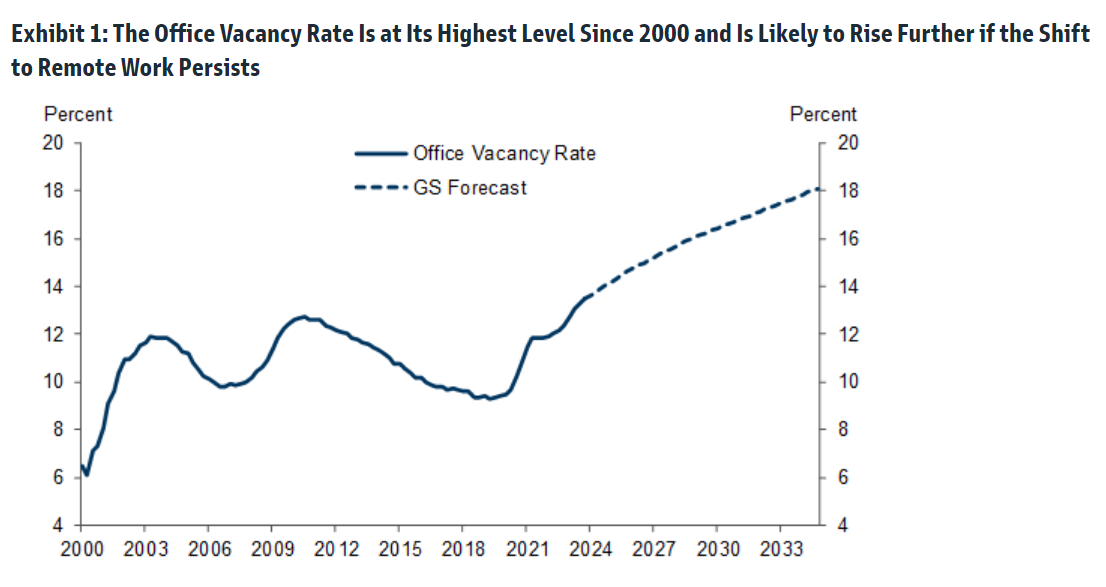

Indeed, as Goldman wrote earlier this week, while office vacancy rates are expected to keep rising well into the next decade..

… the average price of many nonviable offices has fallen only 11% to $307/sqft since 2019 (left side of Exhibit 6). The bank goes on to note that in the hardest-hit cities, as many as 14-16% of offices may no longer be viable, and their average transaction prices have already declined by 15-35%. However, because of lack of liquidity in this market, these recent transaction prices have not yet started to reflect the current values of many existing offices. Goldman ominously concludes that “alternative valuation methods, like those that are based on repeat-sales and appraisal values, suggest that actual office values may be far lower than the average transaction price.” Well, a $1 dollar price would certainly confirm that actual office values are far, far lower (more in the full Goldman note available to professional subscribers).

And going back to the historic firesale, at the end of last year the Canadian fund sold its 29% stake in Manhattan’s 360 Park Avenue South for $1 to one of its partners, Boston Properties, which also agreed to assume CPPIB’s share of the project’s debt. The investors, along with Singapore sovereign wealth fund GIC Pte., bought the 20-story building in 2021 with plans to redevelop it into a modern workspace.

360 Park Avenue South

“It’s the opposite of a vote of confidence for office,” said John Kim, an analyst tracking real estate companies for BMO Capital Markets. “My question is, who could be next?”

As office building anxiety has swept the financial world, as the persistence of both remote work and higher borrowing costs undercuts the economic fundamentals that made the properties good investments in the first place, a wave of banks from New York to Tokyo recently conceded that loans they made against offices may never be fully repaid, sending their share prices plunging and prompting fears of a broader credit crunch.

But the real test will be what price office buildings actually trade for – especially once the hundreds of billions of loan backing the properties mature….

…. and until now there have been precious few examples since interest rates started rising. That’s why industry-watchers see such shocking liquidations like CPPIB’s as a very ominous sign for the market.

The Manhattan firesale isn’t the pension fund’s first sale: last month, CPPIB sold its 45% stake in Santa Monica Business Park, which the fund also owned with Boston Properties, for $38 million. That’s a discount of almost 75% to what CPPIB paid for its share of the property in 2018. The deal came just after the landlords signed a lease with social media company Snap that required they spend additional capital to improve the campus, Boston Properties Chief Executive Officer Owen Thomas said on a conference call.

Peter Ballon, CPPIB’s global head of real estate, declined to comment on the recent deals, but said the fund has continued to invest in office buildings, including a recently completed, 37-story tower in Vancouver.

“Selling is an integral part of our investment process,” Ballon said in an emailed statement. “We exit when the asset has maximized its value and we are able to redeploy proceeds into higher and better returns in other assets, sectors and markets, including office buildings.”

As Bloomberg notes, the pension fund isn’t actively backing away from offices, but it’s not looking to increase its office holdings either. And where a property requires additional investment, CPPIB might simply look to sell so it can put that cash somewhere it can get higher returns instead, said the person, who asked not to be identified discussing a private matter.

CPPIB’s C$590.8 billion ($436.9 billion) fund is one of the world’s largest pools of capital, and its C$41.4 billion portfolio of real estate — stretching from Stockholm to Bengaluru — includes almost every property type, from warehouses, to life sciences complexes, to apartment blocks.

While that scale would mitigate any potential losses from individual transactions, it also means even a small shift in CPPIB’s office appetite has the power to cause ripple effects in the market.

While the 360 Park liquidation may be shocking, it’s just the first of many: with hybrid work schedules set to depress demand for office space in the long term, and higher interest rates increasing the cost of the constant upgrades needed to attract and keep tenants, even the best office buildings may not be able to compete with investment opportunities elsewhere.

“To get even better returns in your office investment you’re going to have to modernize, you’re going to have to put a lot more money into that office,” said Matt Hershey, a partner at real estate capital advisory firm Hodes Weill & Associates. “Sometimes it’s better to just take your losses and reinvest in something that’s going to perform much better.”

Robin Hood is a legendary heroic outlaw originally depicted in English folklore and subsequently featured in literature, theatre, and cinema. Traditionally depicted dressed in Lincoln green, he is said to have stolen from the rich to give to the poor. Politicians have created the new “Forgotten Man” by Amity Shlaes.

However, politicians like Joe Biden, Chuck Schumer, Mitch McConnell are “reverse Robin Hoods” dressed in business suits (although Jamie Raskin D-MD is often seen wearing a bandana and John Fetterman D-PA is often seen in a hoodie and shorts). They instead enact policies that steal from the middle class and give to themselves and the donor class. How do you think that politicians like the Bidens, Obama, Clintons and AOC go in broke and emerge as multi-millionaires?

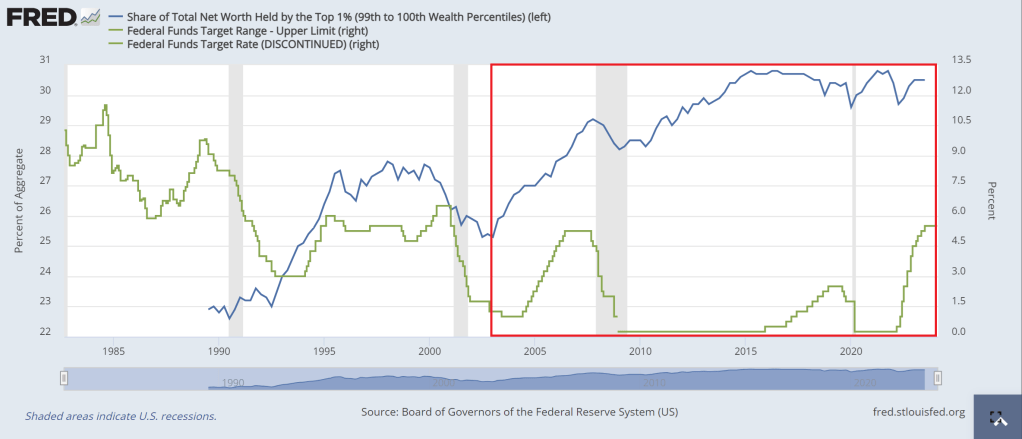

Part of the problem with the reverse Robin Hood model is the Federal Reserve itself. They helped punish the 99% with inflation due to excessive money printing. The share of total net worth held by the top 1% has exploded since The Fed’s rate cuts following the 2001 recession. The Fed has never lowered rates since to levels we saw prior to the 2001 recession, although The Fed is getting close.

Then we have the green energy hysteria (which like pornography excites the brain and distorts logical thinking). Wealthy donors have received a massive windfall (along with China) from Biden/Congress’s green energy spending (scam). The middle class and low-wage workers are now playing higher utility bills (sacrificial lambs on the altar of global warming … or cooling) along with seeing gasoline and diesel prices far higher than before Biden was elected. Gasoline prices are up 46.25% under Biden and diesel prices are up 55.6%.

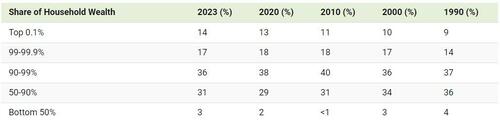

I like this chart of the distribution of household wealth by income group. The top 1% (the elite Pelosi class, are getting wealthier and wealthier. The 90-99% group are doing well, but not as well as the top 1%. The bottom 50% (who the Washington DC elite class seems to have forgotten about)

Here is a table of the same data.

Then we have the exploding mortgage rates under Biden. Rates are up over 155% under Old Grandad Joe Biden. Another shot through the heart of the middle class. And Washington DC is to blame.

Speaking of Washington DC millionaire elites, I want to share this picture with you. Hillary Clinton is NOT Robin Hood but an example of a REVERSE Robin Hood.

Director John Carpenter had two films, “Escape From New York” and the less popular “Escape From LA.” Carpenter’s vision of a dystopian future with Manhattan as a prison island, filled with criminals and Los Angeles as a just a weird, dystopian area filled with gangs and sleazebags. Apparently, Carpenter read George Orwell with a splash of Franz Kafka in writing these films which are sadly becoming a reality. With Biden’s immigration “policy” (let everyone in without checking who they are) is a blueprint for a new film “Escape From The USA!” I wonder if Kurt Russell is available to reprise his role as Snake Plisken?

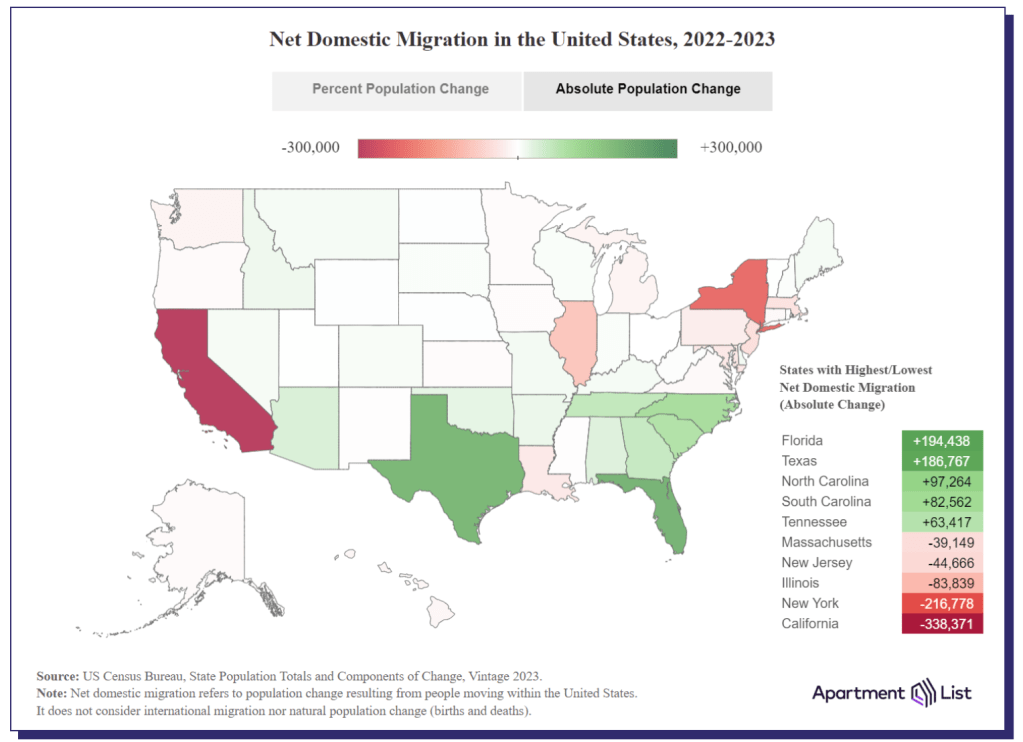

Like John Carpenter foretold, both California and New York are leading the nation in outmigration. BAD crime, high taxes, insane politicians and droves of illegal immigrants are making living in those state very difficult. Throw in the NY AG Letisha James and Judge Engmoron’s Marxist show trials of Donald Trump for doing absolutely nothing wrong and many people are are plain fed up. Illinois under the “leadership” of Chicago Fats (Governor J.B. Pritzker) and horrendous Chicago mayor Brandon Johnson (who makes former Chicago Mayor Lori Lightfoot almost look reasonable) is third in the nation for outmigration. Once again, high taxes, high crime, lots of illegal immigrants, and inane policies are causing people and businesses to flee. John Carpenter should do a film “Escape From Chicago.”

Where are people fleeing to? Florida leads followed by Texas, then the Carolinas, and Tennessee. Generally, these states have lower taxes, lower crime, and less intrusive politicians. E.g., no Gavin Newsom (CA), no Kathy Hochul (NY) and no J.B. Pritzker (IL).

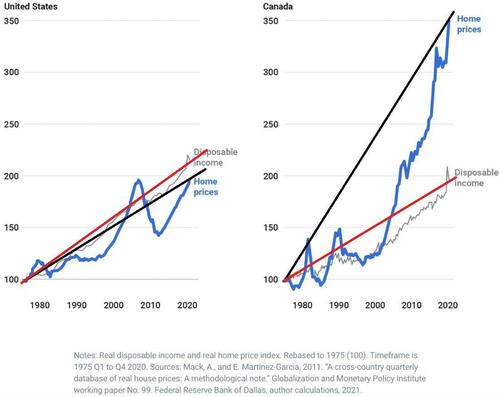

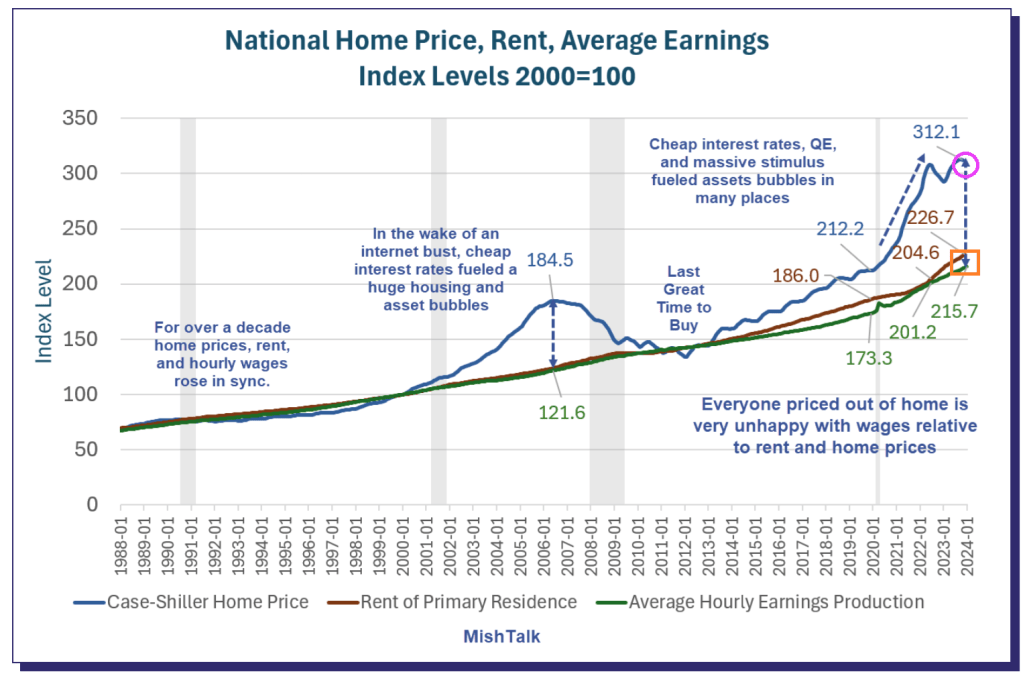

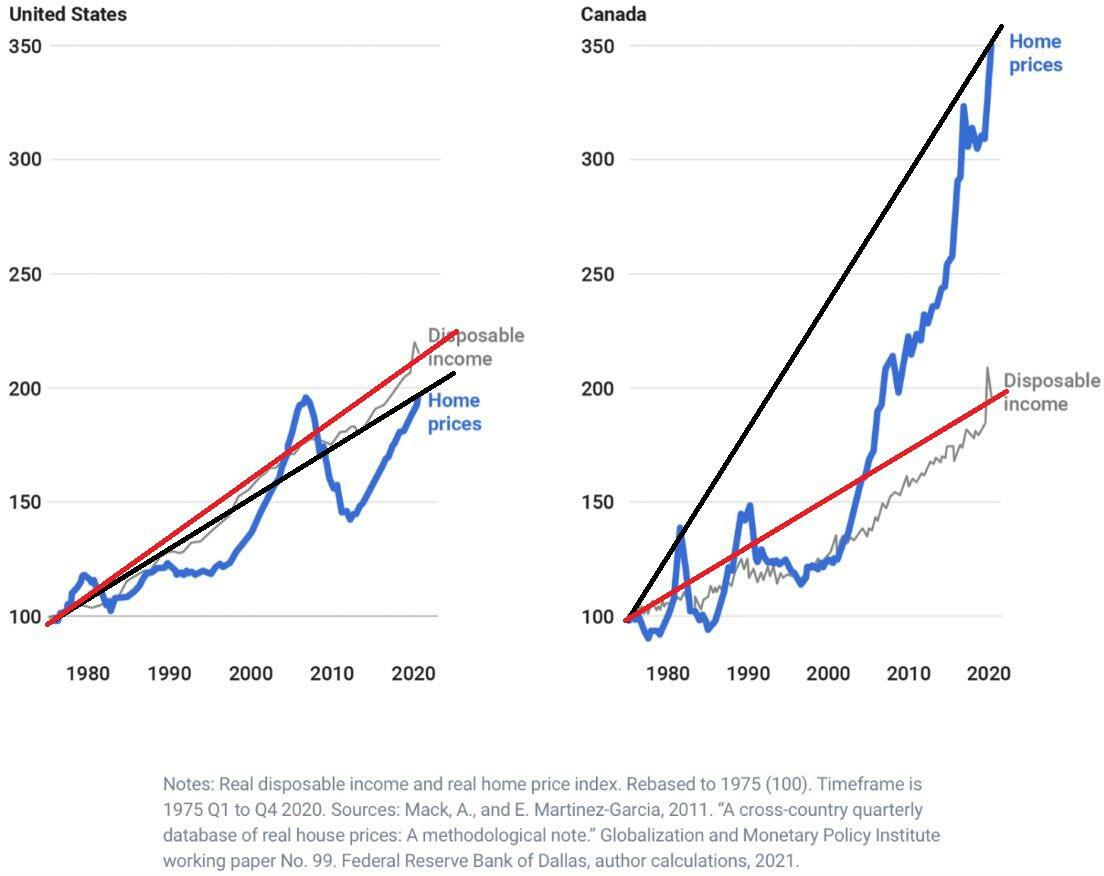

Another reason that people are fleeing New York and California is cost of living. To be sure, Bidenomics (an insidious malinvestment plan, aka, donor-nomics) has made matters worse. Home prices (blue line) and rents (red line) has soared and are far higher than the grow in average earnings (green line). Los Angeles is wonderful if you are a celebrity like Steve Spielberg, Tom Hanks and The Office’s Jenna Fischer where you live in a mansion and are protected by the police force. But other parts of Los Angeles are filled with the homeless, illegal immigrants, rampant crime, and is simply unlivable.

Escape From New York is appropriate for today’s situation. An idiot Mayor and Governor, illegals crowding the streets and hotels, crime through the roof, illegals attacking police. And Joe Biden acting like The Duke of New York, A number One! I guess the closest person we have to Snake Plisken is Donald Trump.

On a related note, Georgia is still seeing positive net in-migration. But as the Fani Willis corruption scandals unfolds and their weak-kneed Governor Kemp does nothing, we have yet another film John Carpenter could make “Escape From Atlanta.” Or a computer game like “Call of Booty.”

I remember the joke made by Jay Leno about Obama. Go to a McDonalds and order whatever you want and give the bill to the person behind you. Unfortunately, that is the Democrat playbook under Obama/Biden (hereafter termed “O’Biden”). For example, Biden is bragging about forgiving student loan debt relief in the amount of $1.2 Billion in student debt for roughly 153,000 borrowers. And bragging that he is ignoring the US Supreme Court like a banana republic dictator. Like the Jay Leno “joke,” SOMEONE has to pay for this election year vote pandering. But that is the beauty/tragedy of BIG government. It is so big and the numbers so monstrous that many kind of shrug and go “eh.” But someone pays and its the middle class in the form of taxes and inflation.

Who is going to pay for the 10 million illegal immigrants that have crossed the southern border under Biden? While Paul Krugman points to a higher GDP from immigration (illegals still buy goods and services), but mostly are a deadweight drag on social services such as welfare, Medicare, schools, healthcare system, etc.). And of course migrant crime is going off the charts. Who pays for Biden’s border fiasco? The middle class and low wage workers, of course. Elites benefit from uncontrolled immigration, generally live in compounds with private security that the rest of us can’t afford. Remember President Carter and the Cuban Mariel boat lift where Fidel Castro emptied his prisons and sent them to Florida creating absolute mayhem and a huge spike in crime? Biden and Cuba Pete Mayorkas turning up the heat on immigration and its accompanied crime wave.

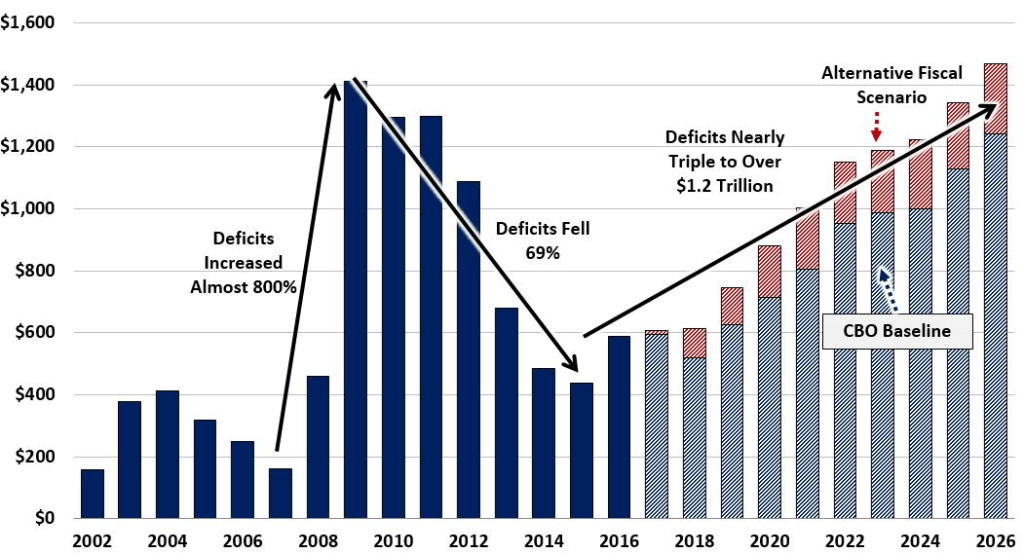

O’Biden loves to spend other people’s money. Aka, OUR money. Case in point. According to the CBO, net interest on the exploding Federal debt under O’Biden now exceeds our defense spending and that gap is expected to explode. To be sure, the US is funding billions in the middle east, handing over billions to Zelensky and Ukrainian oligarchs, and we have China. What a mess!

So, when will “Billions Biden” stop spending other people’s money? Well, only a barely-held Republican House can stop Biden. Meanwhile I will focus on soaring food prices and eat cheap cabbage rolls and drink coffee. Until Biden kills off those pleasures.

But don’t worry! We might get Gavin Newsom, the ultimate used car salesman, to replace Biden against Trump. But Biden’s ego is so massive (why I have no idea) that he won’t go down without a fight. And what about Cacklin’ Kamala?

When Arnold Schwarzenegger was Governor California, his budget chief, a former high school pal of mine, called me to look at California’s budget. He sent me his spreadsheets with forecasts and asked me what I thought. Even back then, I called back and said “California is on an unsustainable fiscal path and seems to be committing suicide.” He agreed, but noted that Schwarzenegger would not like that conclusion. I told him to blame me for the report, as an unpaid consultant to The Golden State. But even back then, I could foresee the absolute mess that the California State legislature would make, particularly if they elected a Democrat governor.

California’s budget deficits look a lot like Biden’s (call him Newsom’s elderly intellectual grandpa) budget deficits where Biden and Congress went on a spending spree from “the honey pot” (US Treasury) and borrowed funds.

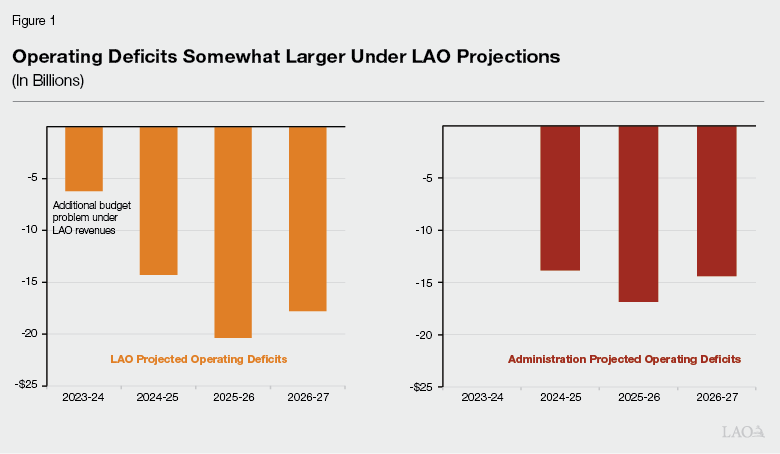

California’s budget crisis is projected to expand more than previously thought and could hit a record deficit of $73 billion, according to a new report from the state’s nonpartisan Legislative Analyst’s Office (LAO).Her

“The actual increase in the state’s budget problem will depend on a number of factors, including formula-driven spending changes, most notably Proposition 98 spending requirements for schools and community colleges,” the report said.

H.D. Palmer, the deputy director of the California Department of Finance and Newom’s spokesperson on budget matters, responded to the new LAO report by telling Fox News Digital that their budget shortfall differs from the $38 million they estimate.

“From now through April, more than $51 billion in income and corporate tax receipts are forecast to come in,” Palmer said. “No one can say today with certainty how those numbers may change the budget estimate of a $38 billion shortfall.”

“A responsible step would be for the Legislature to act now on the early action budget measures needed for $8 billion in solutions to help close this gap,” he added.

The projected bad news comes as Newsom has worked to increase his profile nationwide. It also occurred as California experienced a mass exodus.

California saw its first-ever population decline in 2020 when the state imposed rigid lockdowns during the COVID-19 pandemic. From January 2020 to July 2022, the state lost well over half a million people, with the number of residents leaving surpassing those moving in by almost 700,000.

Census data has shown that Texas is the most popular destination for residents fleeing the state, followed by Arizona, Florida, and Washington. (Of course, Arizona where I used to live has flipped from a Red state to a Blue state with immigration and Democrats are working hard to flip Texas to a Blue state. Washington, has already flipped Blue. Florida remains a Red state under Ron DeSantis).

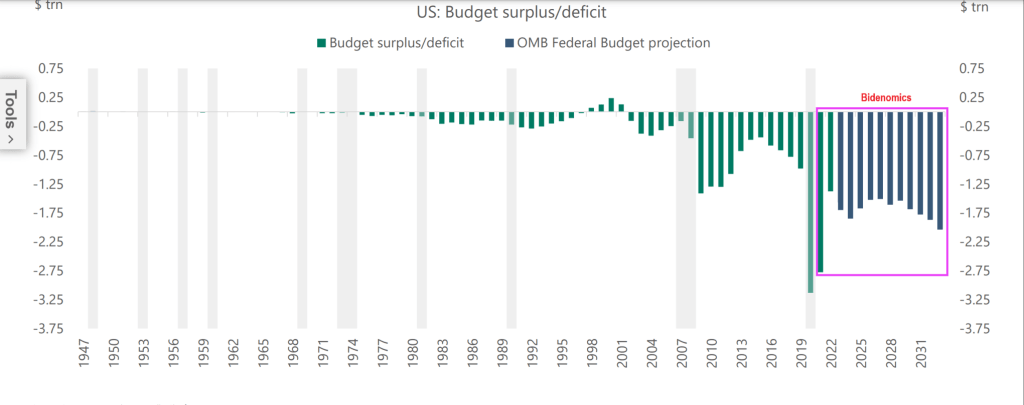

Here is Biden’s budget deficit chart under the hilariously termed “Bidenomics.” Ah, so maybe Governor Newsom is a perfect fit for the wild spenders in Washington DC.

Lest we forget, Biden/Congress can borrow endless funds and stick the bill to Gen Zers and the unborn.

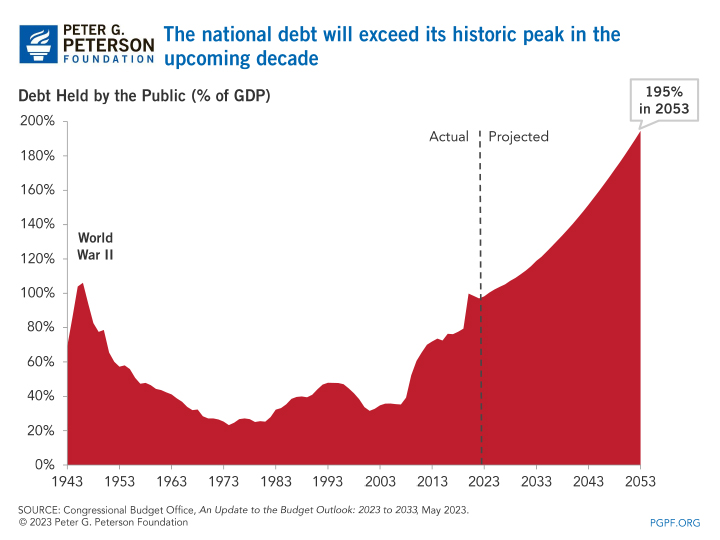

And remember, US politicians have promised $213 TRILLION in unfunded payments that will require cuts (LOL!) or a massive increase in Federal debt.

Biden and Newsom could sing “Fiscal inferno” together! “Here is my demented, doddering grandfather!”

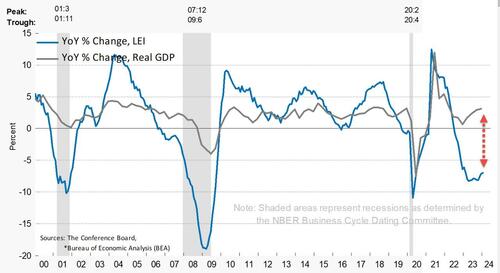

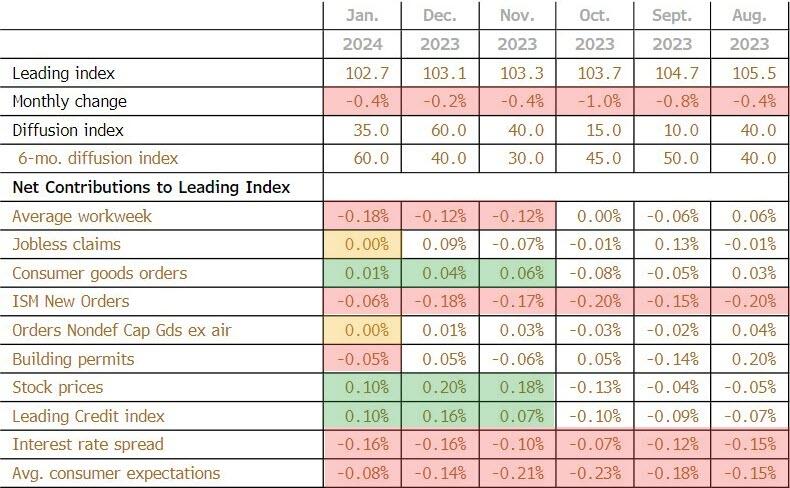

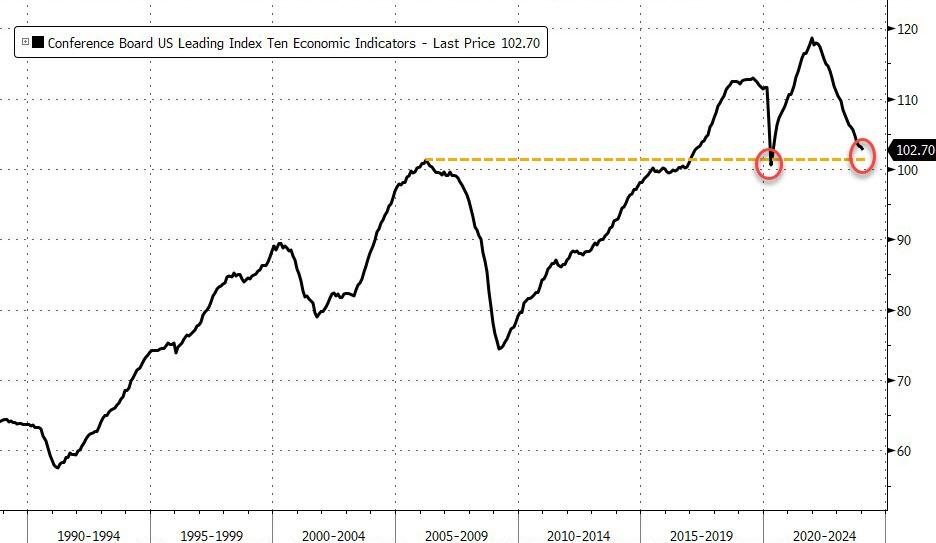

The biggest positive contributor to the leading index was stock prices (again)at +0.10

The biggest negative contributor was average workweek at -0.18

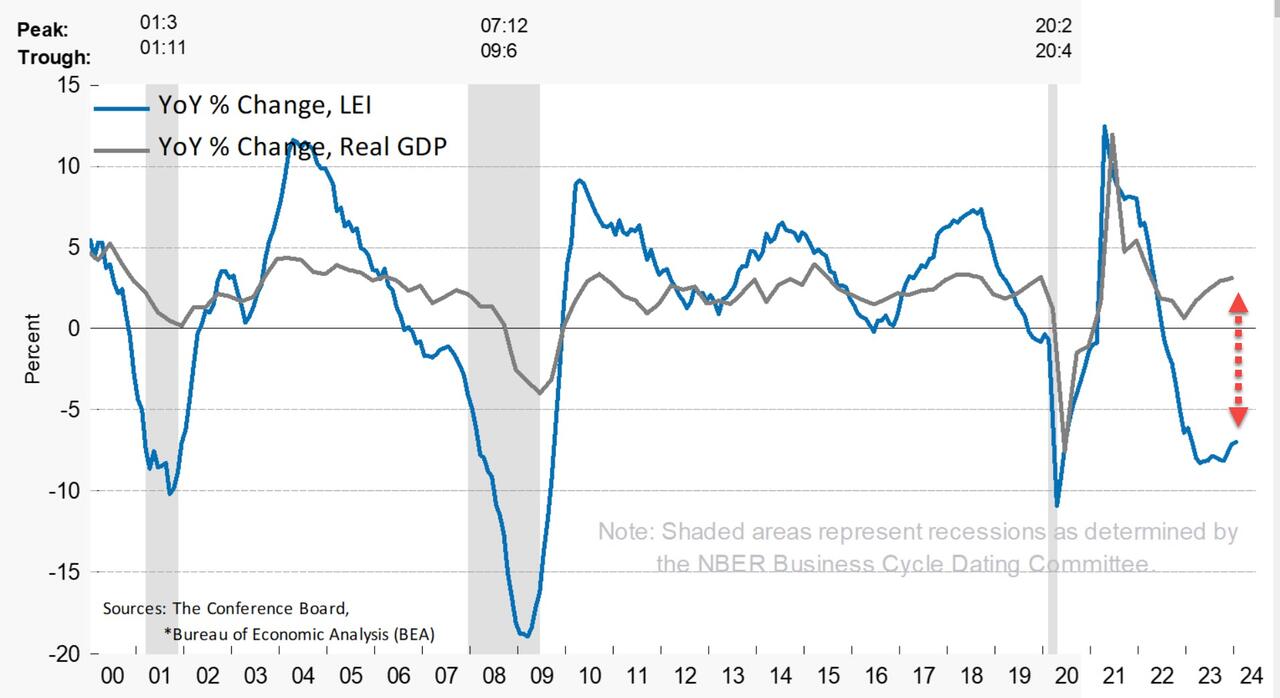

This is the 22nd straight MoM decline in the LEI (and 23rd month of 25) – equaling the longest streak of declines since ‘Lehman’ (22 straight months of declines from June 2007 to April 2008)

“While the declining LEI continues to signal headwinds to economic activity, for the first time in the past two years, six out of its ten components were positive contributors over the past six-month period (ending in January 2024).

As a result, the leading index currently does not signal recession ahead.

While no longer forecasting a recession in 2024, we do expect real GDP growth to slow to near zero percent over Q2 and Q3.”

While the Conference Board seems optimistic, we are struggling to see any signs of hope! tumbling back below the peak in March 2006…

And on a year-over-year basis, the LEI is down 7.0% (down YoY for 19 straight months) – still close to its biggest YoY drop since 2008 (Lehman) outside of the COVID lockdown-enforced collapse (but starting to inflect)…

The annual growth rate of the LEI remains deeply negative and decoupled from Real GDP…..

Finally, the massive easing of financial conditions in the last few months suggests a turn in LEI is imminent…

And hence the ‘soft landing’ mission is accomplished… so no need for rate-cuts? (Except for the banking crisis that looms in March).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.