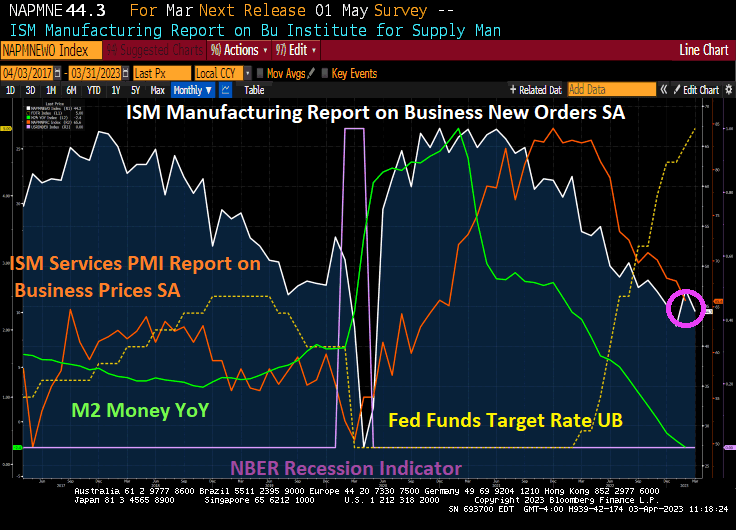

Not only did the ISM Manfacturimng Report on New Business Order fall to 44.3, but price PAID also fell as The Fed hikes rates (yellow line) and slowing M2 Money growth (green line).

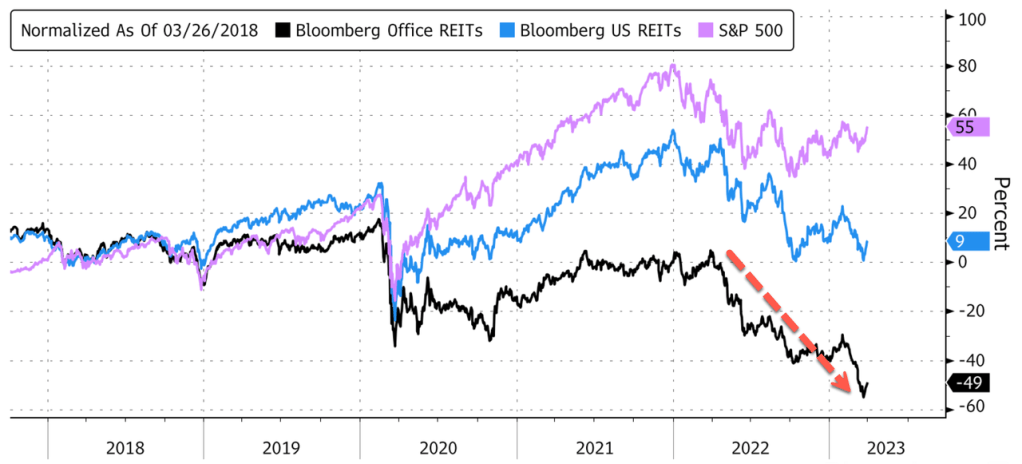

Office REITs are really hurting as Count Powellula sucks the blood (liquidity) from the market.

Count Powellula. “I vant to suck the blood from your economy.”

Well, the University of Michigan consumer sentiment indices are out for March … and they are ugly.

As a baseline, consumer confidence in February 2020 (just before Covid) was 101. After Covid and massive Fed stimulus and Federal government spending spree, consumer confidence in March fell to 62.0, a far cry from 101 under Trump.

Even worse, the UMich buying conditions for housing hit 142 in February 2020 but has declined to 47 in March 2023.

Why would ANYONE have confidence in the US economy under a complete fool with dementia like “China Joe” Biden??

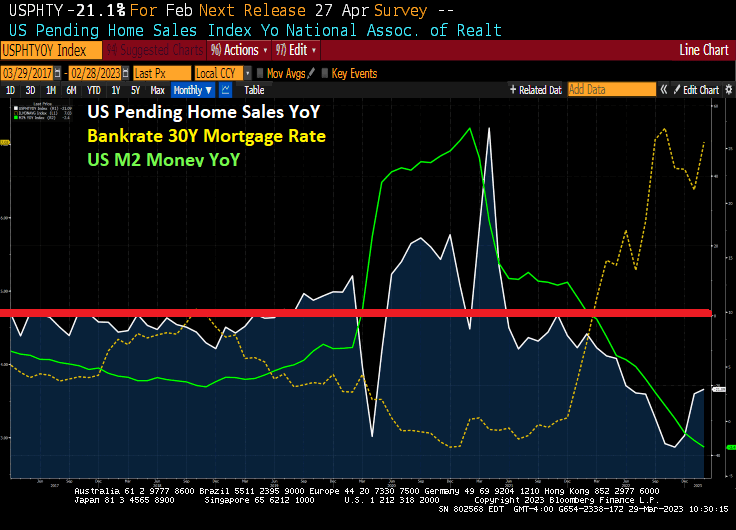

Pending home sales grew in February for the third consecutive month, according to the National Association of REALTORS®. Three U.S. regions posted monthly gains, while the West declined. All four regions saw year-over-year decreases in transactions.

The Pending Home Sales Index (PHSI)* — a forward-looking indicator of home sales based on contract signings — improved 0.8% to 83.2 in February. Year-over-year, pending transactions dropped by 21.1%. An index of 100 is equal to the level of contract activity in 2001.

More notably, the YoY growth rate has been NEGATIVE for 20 of the last 21 months. And 15 straight months.

Biden’s energy policies + insane Federal spending = inflation = Fed slowing M2 Money growth. Hence, pending home sales YoY is down -21.1%.

Consumer considence (according to the Conference Board) remains below pre-Covid levels despite the massive Federal spending spree and Fed money printing).

The US economy got beaten to a pulp by the Chinese Wuhan Covid virus outbreak in early 2020. The Fed intervened with massive money printing along with massive spending by Congress and the Administration. Result? 40-year highs in inflation and a Fed counterattack in terms of rate hikes.

The result of Fed rate hikes? Failing regional banks trying to cope with duration extention and scared depositors. And then we have the St Louis Fed Financial Stress index reaching its highest level since the Covid outbreak of early 2020. And with that, bond volatility is higher than that found during the Covid crisis.

With the expectation of MORE rate hikes, the 10-year Treasury yield jumped 12 basis points.

The architect of The Fed’s “too long for too long” is also the US Treasury Secretary, Janet Yellen.

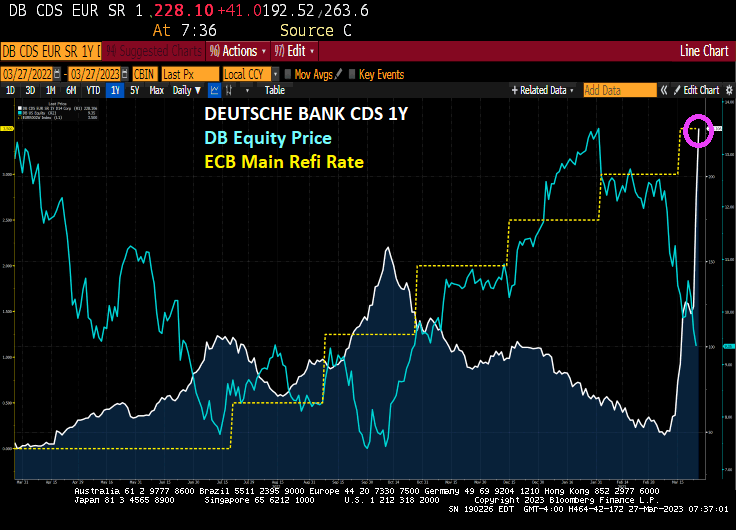

Are central banks like The Federal Reserve and European Central Bank ({ECB) sinking the banks?

Deutsche Bank, Germany’s largest bank (eerily like Germany’s World War II battleship The Bismarck) is seeing a blow out in its 1-year credit default swaps (CDS) as the ECB cranks up it main refinancing rate to fight inflation.

And then we have Deutsche’s Banks gross notional derivatives exposure (Euro 55.6 TRILLLION) dwarfing German GDP (Euro 2.7 Trillion). By a factor of greater than 20! Now, THAT’S a lot of derivatives exposure.

On the bond front (the NEW eastern front), we see the US Treasury 2-year yield rising 17.1 basis points. But European sovereign yields are up double digits as well (except for Italy).

As The Fed attempts to fight inflation, rates are rising. Consequently, deposits are all commercial banks are falling.

The Fed just released its weekly commercial bank data dump showing deposit inflows/outflows.

Two things to note:

1) This is for the week up to 3/15/23 (which includes the SVB collapse but nothing more)

2) ‘Large Banks’ includes the top 25 banks (which means SVB was among that group, hence, we get no indication of SVB rotation flows)

The overall data shows that domestic commercial banks saw over $98 billion in deposit outflows (seasonally-adjusted) that week to just over $17.5 trillion (8th straight week of aggregate outflows).

Source: Bloomberg

That is the largest (seasonally-adjusted) outflow since April 2022 (tax-related?) as we suspect much of that flowed into money-markets. Deposits have been on a steady decline over the past year or so, falling $582.4 billion since February 2022.

There was a notable rotation however with the large banks seeing deposit inflows of $117.9 billion on a non-seasonally-adjusted basis (the biggest weekly inflow since Dec 2021).

Small banks, on the hand, saw a massive $111 billion outflow (non-seasonally-adjusted)…

Source: Bloomberg (note different scales)

That is the largest weekly outflow ever (by multiples) and drops ‘small bank’ total deposits to the lowest since Sept 2021…

Source: Bloomberg

Bear in mind this data does not include the last 10 days, where we have US regional banks all tumbling further and Yellen offering no guaranteed deposits, FRC stock collapse amid bailouts (though that will skew the data due to that $30bn infusion), and the fear of Credit Suisse’s collapse.

Will banks start to compete for deposits? (Well not the biggest ones, for sure)…

I feel like I am watching the Star Trek original series episode “The Doomsday Machine” as former Fed Chair and current US Treasury Secretary effectively just guaranteed ALL US bank deposits. Aka, a massive bank bailout. The episode was about a robot space vehicle that destroy planets … and anything in its path. And if it changed course to destroy something, it gradually returned to its original destructive path. Like The Federal Reseve.

But after a few days of declining Treasury yields because of the mess created by Bernanke/Yellen’s too low for too long policies, and the Biden/Congress insane spending, the US Treasury 2-year yield is up 16.1 basis points.

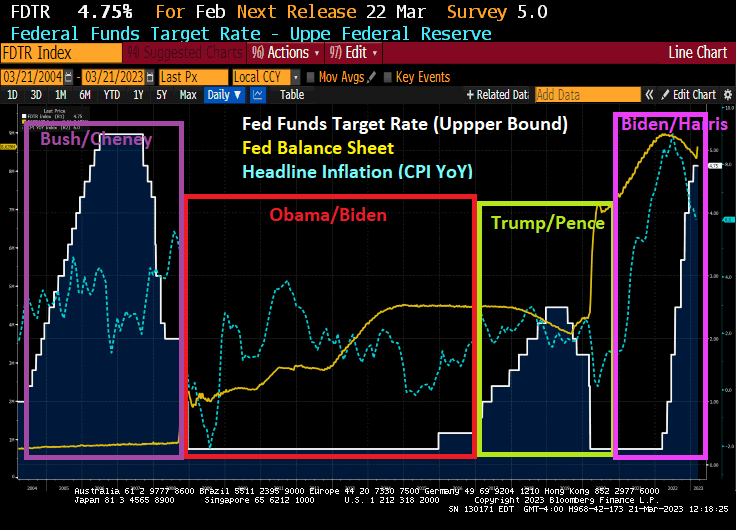

Whether it was politcally motivated to protect Obama/Biden or Obama/Biden’s economic recovery was terrible, The Fed only raised their target rate once before Trump’s election. And then Yellen raised rates like crazy. Only to hand her mess off to Powell who had to drop rates like a rock and massively expand the balance sheet … again … to fight Covid.

For all the focus on whether the Federal Reserve is about to pause its interest-rate hikes, there’s another critical policy decision sure to draw plenty of attention come Wednesday: What the central bank does with its massive pile of bond holdings.

The banking-sector turmoil that has only appeared to deepen, combined with a previous increase in funding pressures, has left financial markets keenly attuned to what the Fed will say about its $8.6 trillion balance sheet.

Until this month the stash had been shrinking as part of the Fed’s efforts to return it back to pre-pandemic levels. But now it has started to expand again as the Fed acts to bolster the banking system through a slate of emergency lending programs. Its latest step came Sunday, when it moved with other central banks to boost US dollar liquidity.

Some say financial-stability concern may spur policymakers to dial back the runoff of its bond portfolio, a process known as quantitative tightening that’s designed to drain reserves from the system. Still, others argue that even if the Fed does pause its rate increases, the central bank’s overarching goal of taming inflation means it’s unlikely it will signal any shift this week in efforts to shrink the holdings of Treasuries and mortgage-backed debt. The one exception, they note, would be if stress in the banking sector were to become much more severe.

The Fed’s move to backstop US banks “clearly expands the Fed’s balance sheet,” said Subadra Rajappa, head of US rates strategy at Societe Generale SA. If usage of the Fed’s liquidity facilities is “small and contained they probably continue QT, but if the take-up is large then they probably stop as it then starts to raise concerns over reserve scarcity.”

The fate of the Fed’s portfolio is a subject of debate after the collapse of several US lenders led the central bank to create a new emergency backstop, known as the Bank Term Funding Program, which it announced March 12. Banks borrowed $153 billion from the Fed’s discount window — lenders’ traditional liquidity backstop — in the week ended March 15, Fed data show, a record that eclipsed the previous all-time high set during the 2008 financial crisis. They also tapped the new program for $11.9 billion.

The central bank’s various liquidity programs added about $300 billion to the Fed’s balance sheet last week, reversing about half of the reduction the Fed has achieved since the runoff began last June. But some economists say the two programs can work in tandem, with the banking efforts targeting financial stability and QT remaining a steady part of the Fed’s plan to remove the support it provided during the pandemic.

It looks like a 25 basis point increase at the next meeting, then cuts in The Fed Funds Target Rate to 3.820% by January 2024.

The labor market is still tight. So tight, we get this!!

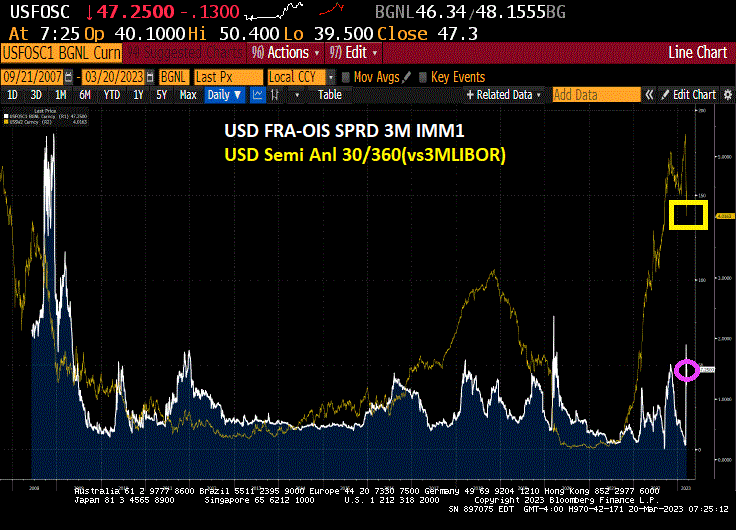

Its the start of a new week after the closure of several US banks (SVP, Signature) and the failure of Credit Suisse. But swaps spreads have calmed down a bit and are no where near the credit crisis highs of late 2008. Or the plain vanilla swap between fixed and variable contracts (white line) has simmered down a bit. BUT was never as high as it was during the financial crisis. Panic by The Fed and FDIC much?

And the 2-year Treasury yield dropped -10 basis points … again.

The Bank of Canada, the Bank of England, the Bank of Japan, the European Central Bank, the Federal Reserve, and the Swiss National Bank are today announcing a coordinated action to enhance the provision of liquidity via the standing U.S. dollar liquidity swap line arrangements.

To improve the swap lines’ effectiveness in providing U.S. dollar funding, the central banks currently offering U.S. dollar operations have agreed to increase the frequency of 7-day maturity operations from weekly to daily. These daily operations will commence on Monday, March 20, 2023, and will continue at least through the end of April.

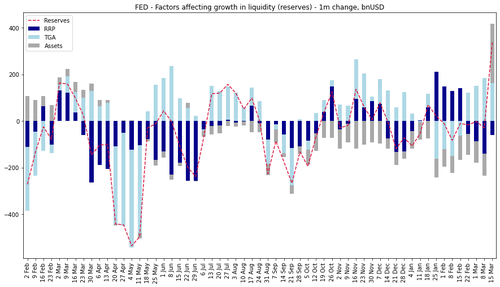

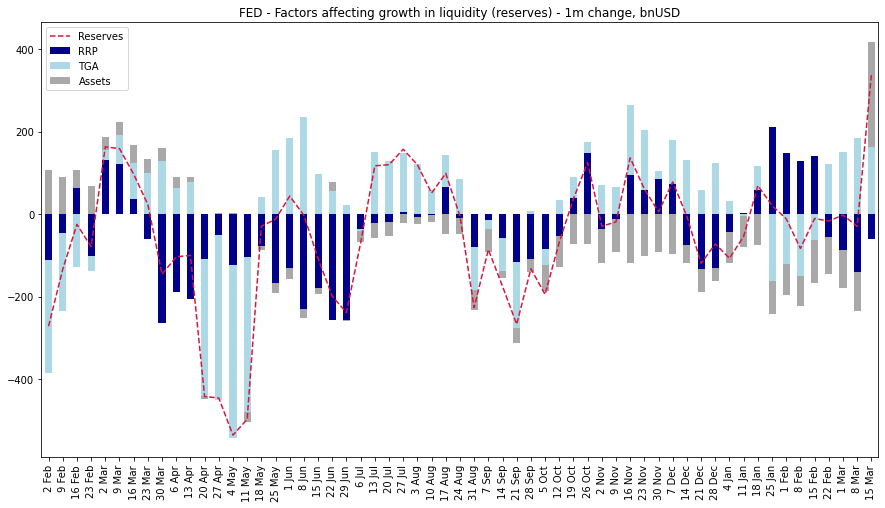

And once the USD swap lines are reopened, the rest of the cavalry follows: rate cuts, QE (the real stuff, not that Discount Window nonsense), etc, etc. In fact, we have already seen a near record surge in reserve injections:

The Fed may as well formalize it now and at least preserve some confidence in the banking sector, even if it means destroying all confidence left in the “inflation fighting” Fed, with all those whose were in charge handing in their resignation for their catastrophic handling of this bank crisis.

{kind=link}

You must be logged in to post a comment.