Fed Governor Christopher Waller said Friday headline inflation has been “cut in half” since peaking last year, but prices excluding food and energy (aka, CORE inflation) has barely budged over the last eight or nine months.

“That’s the disturbing thing to me,” Waller said during a question-and-answer session following a speech in Oslo, Norway. “We’re seeing policy rates having some effects on parts of the economy. The labor market is still strong, but core inflation is just not moving, and that’s going to require probably some more tightening to try to get that going down.”

At a separate event Friday, Richmond Fed President Thomas Barkin said inflation remained “too high” and was “stubbornly persistent.”

“I want to reiterate that 2% inflation is our target, and that I am still looking to be convinced of the plausible story that slowing demand returns inflation relatively quickly to that target,” Barkin said in a speech in Ocean City, Maryland. “If coming data doesn’t support that story, I’m comfortable doing more.”

The Federal Open Market Committee paused its series of interest-rate hikes Wednesday, but policymakers projected rates would move higher than previously expected in response to surprisingly persistent price pressures and labor-market strength.

The consumer price index this week showed headline inflation slowed, but core prices excluding food and energy continued to rise at a pace that’s concerning for Fed officials. Employers continued adding jobs at a rapid clip in May, and job openings climbed in April, recent data showed.

Barkin warned that prematurely loosening policy would be a costly mistake.

“I recognize that creates the risk of a more significant slowdown, but the experience of the ’70s provides a clear lesson: If you back off inflation too soon, inflation comes back stronger, requiring the Fed to do even more, with even more damage,” he said. “That’s not a risk I want to take.”

Policy Report

Separately, the Fed released a new report Friday that said tighter US credit conditions following bank failures in March may weigh on growth, and that the extent of additional policy tightening will depend on incoming data.

“The FOMC will determine meeting by meeting the extent of additional policy firming that may be appropriate to return inflation to 2% over time, based on the totality of incoming data and their implications for the outlook for economic activity and inflation,” the Fed said in in its semi-annual report to Congress.

Read More: Fed Says Tighter Credit Conditions to Weigh on US Growth

The Fed report, which provides lawmakers with an update on economic and financial developments and monetary policy, was published on the central bank’s website ahead of Chair Jerome Powell’s testimony before the House Financial Services Committee on June 21. He will appear before the Senate banking panel the following day.

“Evidence suggests that the recent banking-sector stress and related concerns about deposit outflows and funding costs contributed to tightening and expected tightening in lending standards and terms at some banks beyond what these banks would have reported absent the banking-sector stress,” the report said.

Between work at home, Bidenflation and The Feral Reserve, commercial real estate and regional banks are suffering … and it could get a lot worse. And Joe Biden (aka, Negan) in general. Living in Negan Country!

The work-from-home trend has been taking its toll on office landlords and is now making its way through to banks’ commercial loan portfolios, leading some analysts to predict that more trauma could be on the way for regional banks this year.

And in the current climate of bank failures, short sellers, and nervous depositors, banks with large exposures to commercial real estate (CRE) loans are racing to clean up and sell down their loan portfolios in hopes that they will not fall victim to another round of bank runs.

“There is an estimated $1.5 trillion of commercial property debt that will be due for repayment in about 18 months,” Peter Earle, an economist at the American Institute for Economic Research, told The Epoch Times. “It’s not improbable that even if interest rates have fallen by that time, some of that real estate debt will nevertheless be impaired and have an adverse impact on regional banks.”

In step with a recent trend in the CRE market, tech giant Google announced in May that it was attempting to sublease 1.4 million square feet of vacant office space in its Silicon Valley home base in order to “match the needs of our hybrid workforce.” Despite more employees returning to their offices this year, average office occupancy rates across the United States are still below 50 percent.

According to a report by Bank of America, 68 percent of CRE loans are held by regional banks. Approximately $450 billion in CRE loans will mature in 2023. JPMorgan Chase estimated that CRE loans comprise, on average 28.7 percent of the assets of small and regional banks, and projected that 21 percent of CRE loans will ultimately default, costing banks about $38 billion in losses.

Double Hit (of Biden’s Policies) Commercial mortgages are getting hit on two fronts: first, by the lack of demand for office space, leading to credit concerns regarding landlords, and second, by interest rate hikes that make it significantly more expensive for borrowers to refinance.

According to a June 12 report by Trepp, a CRE analytics firm, CRE loans that were originated a decade ago, when average mortgage rates were 4.58 percent, are now coming due, and in today’s market, fixed-rate CRE loan rates are averaging around 6.5 percent.

Banks that make CRE loans consider factors like debt service coverage ratios (DSCRs), which measure a property’s income relative to cash payments due on loans. Simulating mortgage interest rates from 5.5 percent to 7.5 percent, Trepp projected that between 28 percent and 44 percent, respectively, of currently outstanding CRE loans would fail to meet the 1.25 DSCR ratio today, and thus be ineligible for refinancing.

These calculations were done assuming current cash flows from properties stay the same and that loans are interest-only, but with vacancies rising, many landlords may have substantially less cash flow available. In addition, whereas interest-only CRE loans were 88 percent of the market in 2021, lenders are now switching to amortizing mortgages to reduce risk, which significantly increases debt service payments.

Refinancing Issues Fitch, a rating agency, projected that approximately one-third of commercial mortgages coming due between April and December of this year will be unable to refinance, given current interest rates and rental income.

“It’s a very different world now from the one in which the majority of these loans were made,” Earle said. “In a zero-interest-rate environment, before the COVID lockdowns saw many businesses shift to a remote work basis, many of these loan portfolios full of office properties looked great. Now, a substantial portion of them look quite vulnerable.”

The Trepp report highlighted several regional markets, such as San Francisco, where office sublease offers jumped 140 percent since 2020, and Los Angeles, where office vacancies hit a historic high of 22 percent. Available office space in Washington D.C. increased to 21.7 percent in the first quarter of 2023.

New York has been hit hard, as well. Office occupancy rates in New York City plummeted from 90 percent to 10 percent in 2020 during the COVID pandemic, but only recovered to 48 percent this year. Revenue from office leases fell by 18.5 percent between December 2019 and December 2022.

Vacancy Rates at 30-Year High Overall, according to a report by analysts at New York University and Columbia Business School, office vacancy rates are at a 30-year high in many American cities.

The report found that “remote work led to large drops in lease revenues, occupancy, lease renewal rates, and market rents in the commercial office sector.”

The authors predict that, even if office occupancy returns to pre-pandemic levels, “we revalue New York City office buildings, taking into account both the cash flow and discount rate implications of these shocks, and find a 44% decline in long run value. For the U.S., we find a $506.3 billion value destruction.”

As predicted, delinquencies in commercial mortgage loans are now creeping up. Missed payments in commercial mortgage-backed securities (CMBS) increased half a percent in May over the prior month to 3.62 percent, Trepp reports. The worst component of the CMBS market, which includes multi-unit rental buildings, medical facilities, malls, warehouses, and hotels, was offices, where delinquencies increased 125 basis points to more than 4 percent.

To put this in perspective, however, CMBS delinquencies exceeded 10 percent in 2012 and 2020. And analysts say that lending criteria for CRE have been more conservative than they were before the mortgage crisis of 2008, leaving more cushion on ratios relative to a decade ago.

All the same, the credit crunch at regional banks has created a vicious circle, where banks race to pare down their CRE portfolios, and the dearth of financing leaves more landlords facing default as outstanding loans mature. To make matters worse, commercial property values, which provide collateral for the loans, appear to be taking a hit as well.

In an effort to rapidly clean up their CRE loan portfolios and avoid the fate of failed banks like Silicon Valley Bank, Signature Bank, and First Republic Bank, banks are now attempting to sell off the loans, often taking a loss in the process.

In May, PacWest, a regional bank, sold $2.6 billion of construction loans at a loss. Citizens Bank reportedly has put $1.8 billion of its CRE loans up for sale during the first quarter of this year. Customers Bancorp reduced its CRE lending by $25 million and put $16 million of its existing portfolio up for sale.

Wells Fargo, one of the top four largest U.S. banks, is also downsizing its CRE portfolio, and in announcing the move CEO Charlie Scharf stated, “we will see losses, no question about it.”

“Between the Fed’s 500+ basis point hikes over the past 16 months and the failure of Silicon Valley Bank, and others, earlier this year, a credit tightening is already underway,” Earle said. “That has put a lot of pressure on regional lenders.”

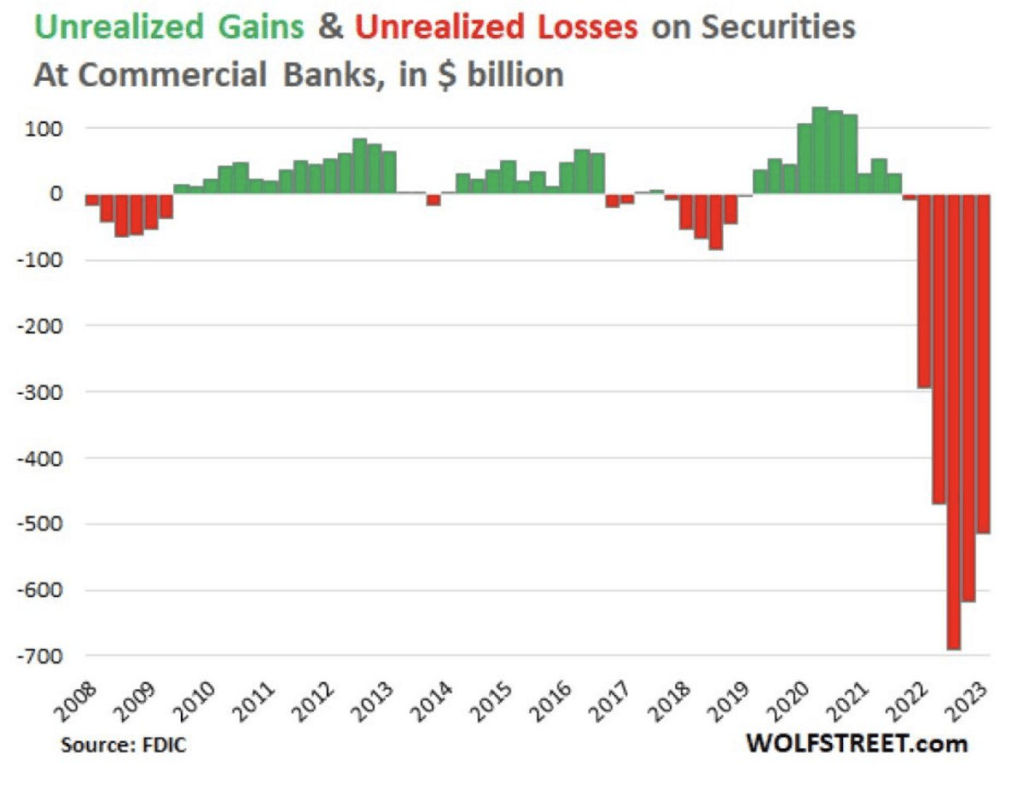

A March academic study titled “Monetary Tightening and U.S. Bank Fragility in 2023” stated that the market value of assets held by U.S. banks is $2.2 trillion lower than what is reported in terms of their book value. This represents an average 10 percent decline in the market value of assets across the U.S. banking industry, and much of this decline came from commercial real estate loans.

Consequently, the authors wrote, “even if only half of uninsured depositors decide to withdraw, almost 190 banks with assets of $300 billion are at a potential risk of impairment, meaning that the mark-to-market value of their remaining assets after these withdrawals will be insufficient to repay all insured deposits.”

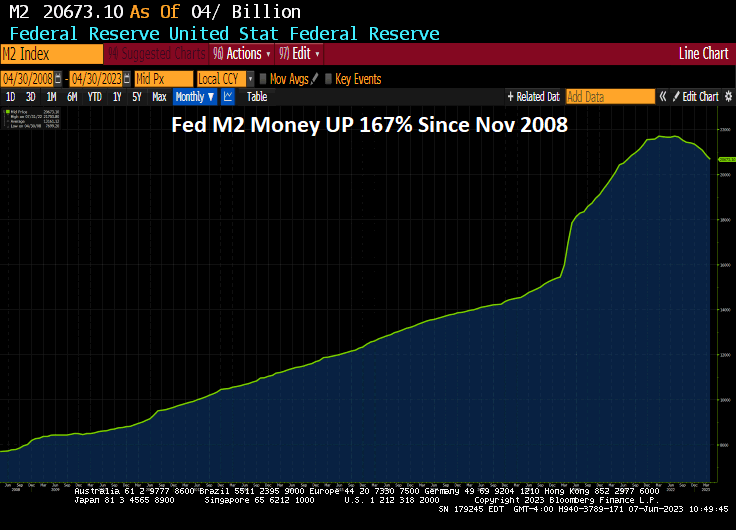

One has to wonder about The Feral Reserve. Since The Great Recession of 2008, The Federal Reserve has printed a staggering amount of money (know as QE). There is still about $8.3 TRILLION in monetary stimulus sloshing around the economy.

And M2 Money printing is up 167% since November 2008.

So, despite the talking heads from The Fed and CNBC, etc blathering about Fed tightening, there remains over $8 TRILLION in monetary stimulus chasing asset prices.

Is The Fed ACTUALLY the US economy? Or is The Fed the financing arm of the Democrat party?

Yes, The Fed looks like they are pausing .. rate hikes.

As Connor MacLeod said in the film Highlander, “There can only be one!” The US banking system under Joe Biden’s Reign of Error is like the film Highlander: apparently, there can only be one bank. And it is likely JP Morgan Chase.

Take the JP Morgan Chase (JPMC) acquisition of First Republic Bank:

In Acquiring First Republic Bank, JP Morgan Has:

Bypassed laws against acquiring bank while controlling 10%+ of US deposits

Shared $13 billion in losses with the FDIC

Received a $50 billion loan from the FDIC

Effectively bought back its own deposits

Expects to profit $5 billion+ over the next 5 years

This crisis has taught us that rules don’t matter in times of panic, particularly to regulators.

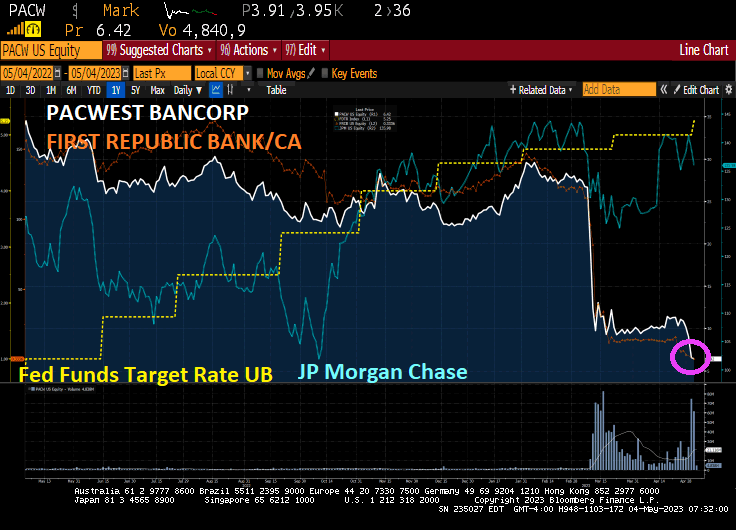

And now we have PacWest Bancorp. Lender says it’s been approached by potential investors. Bill Ackman warns US regional banking system at risk.

The turmoil at PacWest shows how investor angst still remains elevated after a string of failures and deposit outflows in the sector despite Federal Reserve Chair Jerome Powell’s assurance Wednesday that authorities were closer to containing the crisis. It’s reignited the debate over whether more US regional lenders will fall after this year’s collapse of SVB Financial Group’s Silicon Valley Bank, Silvergate Capital Corp., Signature Bank and most recently First Republic Bank.

Smaller banks are under pressure after a year of interest-rate hikes hammered the value of their bond holdings and drove unrealized losses to an estimated $1.84 trillion. Trouble in commercial real estate is adding to the pain, while depositors take their money out to seek better returns elsewhere. These stresses have put the spotlight on these lenders, which typically have fewer resources to defend themselves.

We are seeing a consolidation of the banking system .. again as smaller and regional banks fail and get gobbled up by the Too-Big-To-Fail (TBTF) banks like … JP Morgan Chase.

Biden’s Reign of Error is not over yet. His campaign slogan (which was also Bill Clinton’s campaign reelection slogan) is “Finish the job!” With Biden’s idiotic mortgage idea of punishing borrowers with good credit and giving subsidies to those with bad credit, Biden is trying to finish off the US economy and banking system.

James Carter (no, not Mr. Peanut, the smart one at America First Policy Institute’s Center for American Prosperity) had a nice op-ed on American Thinker entitled “The Biden Administration’s Budget Hypocrisy.”

The Biden administration’s claims of deficit reduction come in stark contrast to the president and his team, having added $4.8 trillion to the deficit through 2031.

You might call anyone uttering such claims a hypocrite. As Adlai Stevenson, the grandfather of the future Illinois governor and two-time presidential candidate of the same name, reportedly quipped: “A hypocrite is the kind of politician who would cut down a redwood tree, then mount the stump and make a speech for conservation.” Sounds about right.

Why does this matter? It matters because President Joe Biden fancies himself a champion of deficit reduction. As he bragged in a “60 Minutes” interview last month, “By the way, we’ve also … reduced the deficit by $350 billion my first year. This year, it’s going to be over $1.5 trillion, reduced the debt.”

But the president’s attempts to redefine his reckless spending as deficit reduction don’t end there. According to The Washington Post, “Just in the week before the 60 Minutes interview, the president mentioned having reduced the budget deficit by $350 billion six times, sometimes saying he wants to counter accusations that he’s running up the federal tab.” (emphasis added)

What the president fails to mention, however, is that this near-term deficit reduction has nothing to do with him or his administration. Instead, it’s the result of emergency COVID-19 spending that is now ending as planned.

Maya MacGuineas, president of the nonpartisan Committee for a Responsible Federal Budget, points out what the Biden administration is loath to admit:

“The White House has been trying to paint President Biden as the champion of prudent economic stewardship. Biden’s ‘record on fiscal responsibility is second to none,’ it asserts. As temporary covid measures end — and record-high deficits predictably decline — the administration is congratulating itself for that supposed achievement.

But the administration’s record is, sadly, the opposite of what it argues. Since entering office, the president has approved policies adding $4.8 trillion to the deficit over the next decade. This is an extraordinary sum, which makes it all the more astonishing that the administration would try to pull off this claim.”

According to the Office of Management and Budget, even if the 117th Congress had enacted the Biden administration’s fiscal year 2023 budget in its entirety, net interest costs would more than triple from $352 billion in 2021 to $1.1 trillion by 2032. Is a tripling of future net interest costs something typically associated with an administration committed to tackling the federal budget deficit? No.

President Biden’s rhetoric aside, his mid-session budget review forecasts endless $1 trillion-plus annual deficits totaling more than $14 trillion over the coming decade. Even adjusted for inflation, these deficits would be among the largest ever generated by the federal government. Is that “fiscally responsible?” No.

President Biden is not serious about reducing the deficit. He claims progress on the deficit but obscures the facts that every American should know.

Not only does President Biden fail to try to balance the budget, but he actively pursues policies that he must know will balloon federal spending and deficits.

No, but Biden and Congress are serious about bankrupting the US Treasury and moving to a Socialist model.

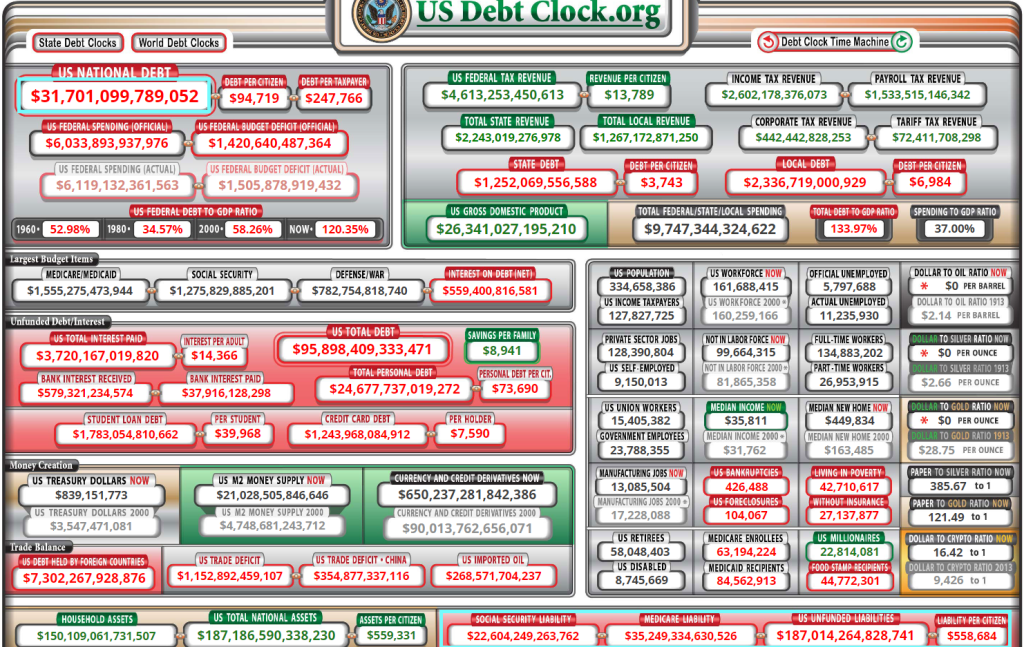

And what even James Carter doesn’t mention is the staggering levels of UNFUNDED LIABILITIES of $187 TRILLION. The question for Biden is …. how are deficits and the massive debt going to play out when we are on the hook for $187 TRILLION?

I am sure that Bernie Sanders, Elizabeth Warren and The Squad will suggest much higher taxes to cover it. And remember, Biden was the idiot that helped taxed Social Security for seniors. And he has also worked towards cutting Social Security and Medicare in the past.

The only out is 1) default on the US debt which would be catestophic and 2) renegging on the massive unfunded liability load. Remember, France is rioting over raising their retirement age by 2 years. Let’s see if Americans riot over inevitable cuts to Social Security, Medicare and Medicaid.

Cut mandatory spending without riots? Please.

The theme song of Biden’s insane, economy destroying, inflation creating budget should be “Keep on printing!”

Yes, this is Government Gone Wild! But no pics or videos of ancient Congress members like Warren or President Biden, please.

Here is a chart of US office vacancies nationally (yellow), New York (white), San Franciso (green) and Los Angeles (orange). Note the rapid decline in office vacancies just prior to the financial crisis (often mislabeled as the subprime mortgage crisis). Then look at office vacancies after The Fed’s massive monetary experiment of setting rates to near zero and buying a ton of Treasuries, Agency MBS. etc. While San Francisco returned to pre-financial crisis levels of office vacancy, in general the office market never fully recovered.

And then “the slammer” struck: the COVID economic shutdowns. After 2020 shutdowns, office vacancy rates rose dramatically. Two complicating factors: 1) the US moved to working at home rather than commuting to an office and largely remains that way. 2) crime is going bonkers in American cities, particularly New York, Los Angeles and San Francisco (don’t worry, I haven’t forgotten about other gang nests like Chicago and Detroit). I saw that California’s woke governor Gavin “Nancy Pelosi’s nephew” Newsom said the word “gang” then apologized and replaced it with “organized groups.” No wonder Newsom can’t fix anything, but he is running for President of the US! (insert Edvard Munch’s “The Scream” painting here,)

The Fed responded to the financial crisis by lower rates to 25 basis points and printing a boat load of money. Unfortunately, office vacancies rose to a peak in October 2010 then began falling again. Only to start rising again after Trump took office in 2017. Alas, Covid struck in 2020, The Fed and Federal government panicked. States and local governments (not to mention teacher’s unions) shut down economies and schools. Office vacancies are now higher than at peak of the Covid shutdowns!!!

Consumer considence (according to the Conference Board) remains below pre-Covid levels despite the massive Federal spending spree and Fed money printing).

The Federal Reserve never died. In fact, The Fed is growing its balance sheet again. Why? A slowing economy and weakness in the banking sector (thanks to inflation and the Fed trying to get inflation back to 2%.

And the banking fiasco keeps rolling, particularly in Europe where Credit Suisse has been in the news for failing and now my former employer, Deutsche Bank (aka, The Teutonic Titanic).

Deutsche Bank AG became the latest focus of the banking turmoil in Europe as ongoing concern about the industry sent its shares slumping the most in three years and the cost of insuring against default rising.

The bank, which has staged a recovery in recent years after a series of crises, said Friday it will redeem a tier 2 subordinated bond early. Such moves are usually intended to give investors confidence in the strength of the balance sheet, though the share price reaction suggests the message isn’t getting through.

“It is a clear case of the market selling first and asking questions later,” said Paul de la Baume, senior market strategist at FlowBank SA. “Traders do not have the risk appetite to hold positions through the weekend, given the banking risk and what happened last week with Credit Suisse and regulators.”

Deutsche Bank slumped as much as 15%, the biggest decline since the early days of the pandemic in March 2020. It was the worst performer in an index of European bank stocks, which fell as much as 5.7%. Crosstown rival Commerzbank AG, Spain’s Banco de Sabadell SA and France’s Societe Generale SA also saw steep drops.

The widespread declines undermine hopes among authorities that the rescue of Credit Suisse Group AG last weekend would stabilize the broader sector. Central banks from the Federal Reserve to the Bank of England this week raised interest rates once again, keeping their focus on inflation amid hopes that the worst of the financial turmoil was past.

All week, regulators and company executives have sought to reassure traders about the health of the banking industry. Deutsche Bank management board member Fabrizio Campelli said Thursday that the government-brokered takeover of Credit Suisse by UBS is “no indication” of the state of European banks.

Standard Chartered Plc Chief Executive Bill Winters said Friday that while there are still some issues to be addressed, “it seems that the acute phase of the crisis is done.”

The latest moves in Europe follow losses in US banks, which tumbled Thursday even after Treasury Secretary Janet Yellen told lawmakers that regulators would be prepared for further steps to protect deposits if needed.

And apparently bank bailouts never died. They just got relabeled.

And on growing banking fears, the 10-year Treasury yield is down -11.7 basis points.

I feel like I am watching the Star Trek original series episode “The Doomsday Machine” as former Fed Chair and current US Treasury Secretary effectively just guaranteed ALL US bank deposits. Aka, a massive bank bailout. The episode was about a robot space vehicle that destroy planets … and anything in its path. And if it changed course to destroy something, it gradually returned to its original destructive path. Like The Federal Reseve.

But after a few days of declining Treasury yields because of the mess created by Bernanke/Yellen’s too low for too long policies, and the Biden/Congress insane spending, the US Treasury 2-year yield is up 16.1 basis points.

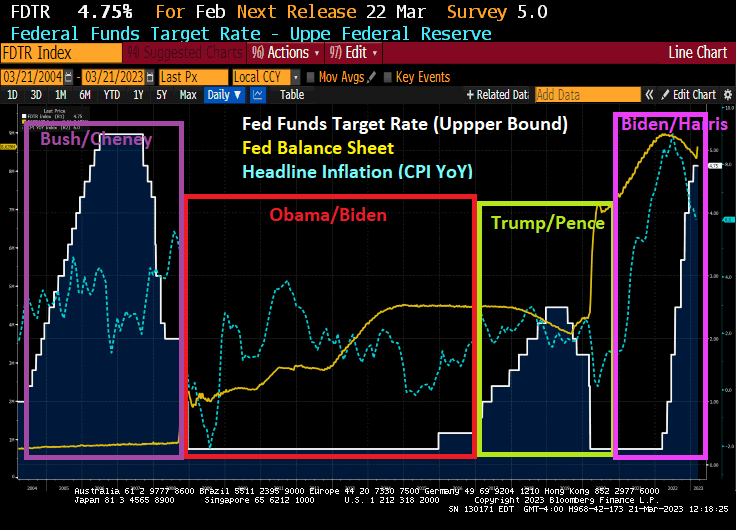

Whether it was politcally motivated to protect Obama/Biden or Obama/Biden’s economic recovery was terrible, The Fed only raised their target rate once before Trump’s election. And then Yellen raised rates like crazy. Only to hand her mess off to Powell who had to drop rates like a rock and massively expand the balance sheet … again … to fight Covid.

You must be logged in to post a comment.