Things are getting interesting in DC, to say the least. The US is 100% likely to face a recession in the next 12 months while The Federal Reserve is on its crusade to fight inflation caused by … The Federal Reserve, Biden’s green energy shenanigans and massive, irresponsible Federal spending that even Former Obama economist Lawrence Summers warned would cause inflation. So what will The Fed do? Lower rates and expand their assets purchases to fight the impending recession OR keep tightening to fight Bidenflation? But where we are now is that the fixed-income market could be in big, big trouble.

According to MarketWatch, the world’s deepest and most liquid fixed-income market is in big, big trouble.

For months, traders, academics, and other analysts have fretted that the $23.7 trillion Treasuries market might be the source of the next financial crisis. Then last week, U.S. Treasury Secretary Janet Yellen acknowledged concerns about a potential breakdown in the trading of government debt and expressed worry about “a loss of adequate liquidity in the market.” Now, strategists at BofA Securities have identified a list of reasons why U.S. government bonds are exposed to the risk of “large scale forced selling or an external surprise” at a time when the bond market is in need of a reliable group of big buyers.

“We believe the UST market is fragile and potentially one shock away from functioning challenges” arising from either “large scale forced selling or an external surprise,” said BofA strategists Mark Cabana, Ralph Axel and Adarsh Sinha. “A UST breakdown is not our base case, but it is a building tail risk.”

In a note released Thursday, they said “we are unsure where this forced selling might come from,” though they have some ideas. The analysts said they see risks that could arise from mutual-fund outflows, the unwinding of positions held by hedge funds, and the deleveraging of risk-parity strategies that were put in place to help investors diversify risk across assets.

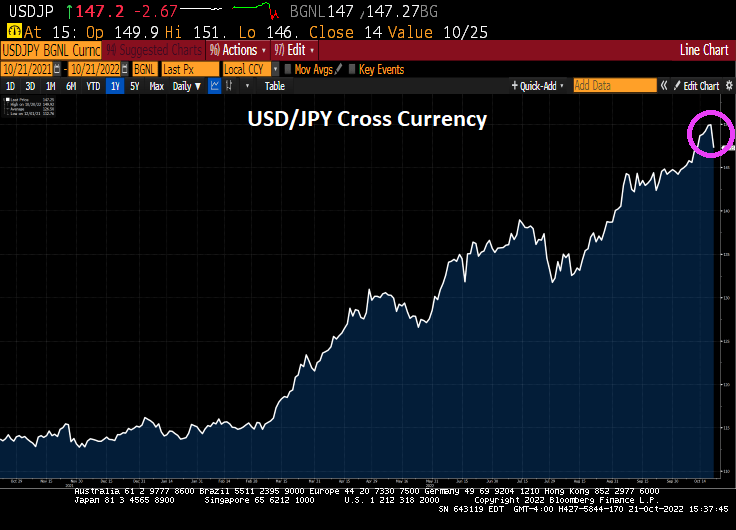

In addition, the events which could surprise bond investors include acute year-end funding stresses; a Democratic sweep of the midterm elections, which is not currently a consensus expectation; and even a shift in the Bank of Japan’s yield curve control policy, according to the BofA strategists.

The BOJ’s yield curve control policy, aimed at keeping the 10-year yield on the country’s government bonds at around zero, is being pushed to a breaking point.

Well. Bidenflation certainly isn’t helping, but Statist Economist and Cheerleader Janet Yellen can’t bring herself to blame green energy policies, rampant Federal spending or irresponsible Federal Reserve policies for the crisis.

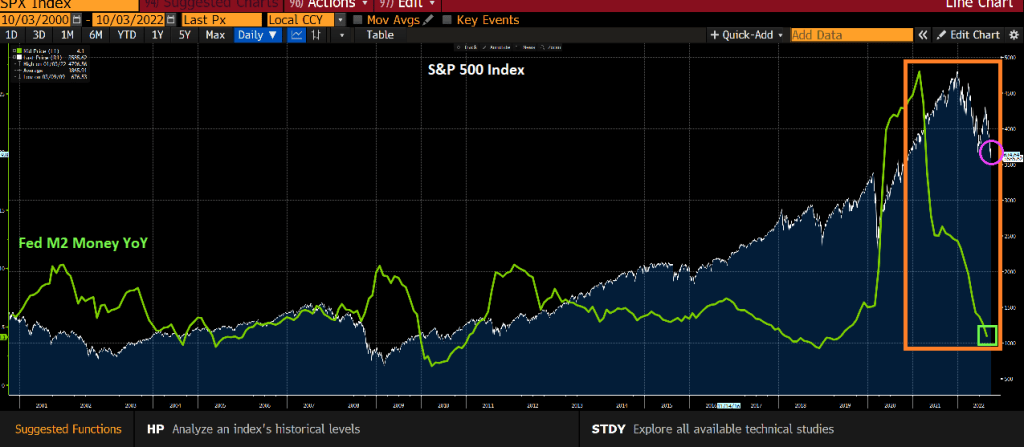

You will note the differences between today and the financial crisis of 2008-2009. The financial crisis gave us a massive surge in government securities liquidity thanks to then Fed Chair Ben Bernanke imitating Japan’s Central Bank and buying US government securities. Fast forward to today and the liquidity index hasn’t budged much since 2010 (except for a little blip around the Covid Fed intervention of early 2020), but we are now seeing near 40-year highs in inflation and a barely declining Fed balance sheet. And M2 Money YoY (mostly commercial bank deposits) are crashing.

I am guessing that The Fed will pivot given that stock futures are way up for Monday. The Dow Jones mini is up 770 points and the S&P 500 mini is up 88.75 points.

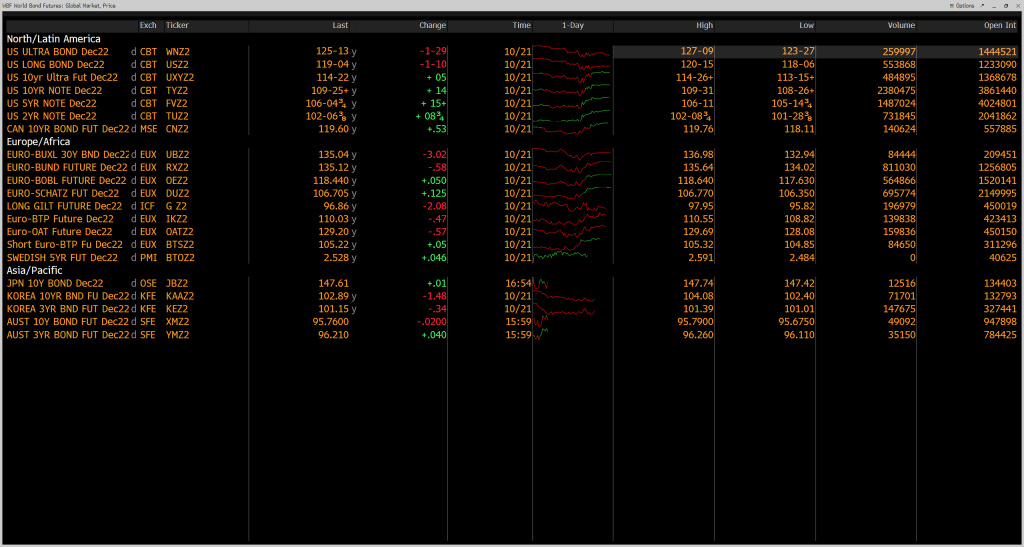

Bond market futures (specifically the US Ultra Bond) is down for Monday, meaning yields will be climbing.

While perusing MarketWatch, I noticed this headline from the uber-attention whore Nouriel Roubini: “New Yorkers are ‘stupid’ for moving to Texas, Florida: Wall Street’s ‘Dr. Doom’.” Seriously? Nouriel, you aren’t talking to friends in a Bleeker Street bar. Like Bernanke.

I remember giving a speech at The Brookings Institute in Washington DC. Talk about stranger in a strange land. One person who I was debating got frustrated and said “You are such a … Republican!!!” As if that was the worst slur he could throw at me.

You must be logged in to post a comment.