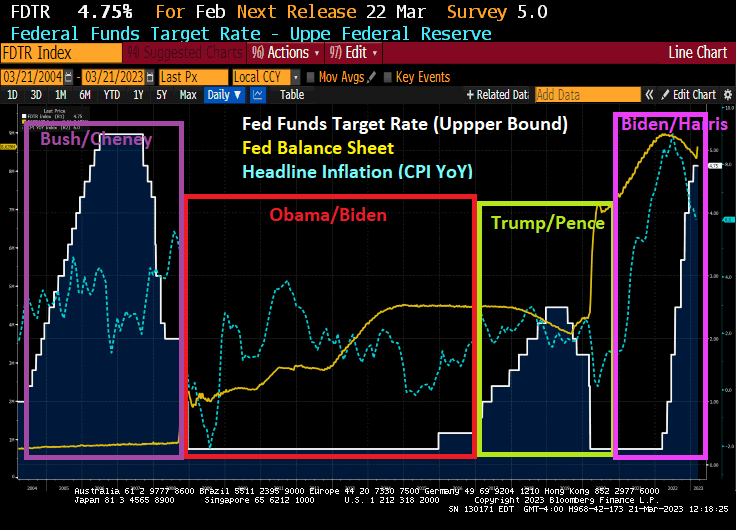

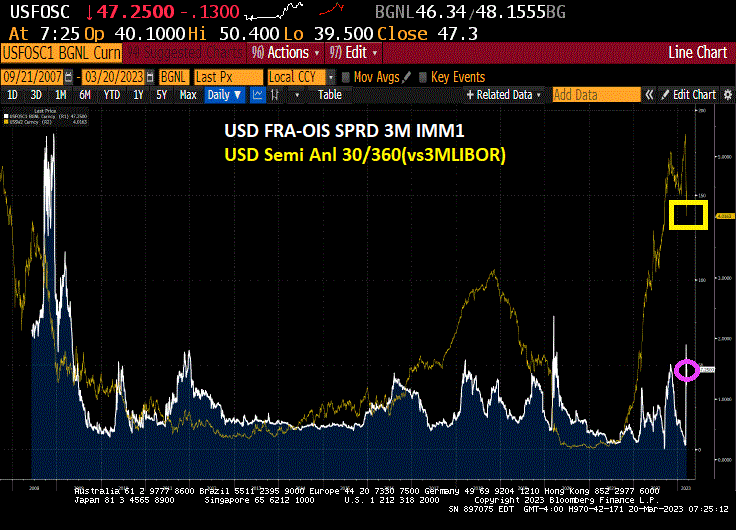

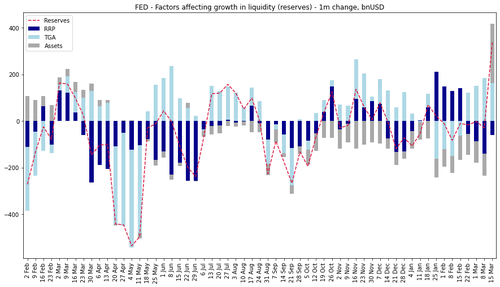

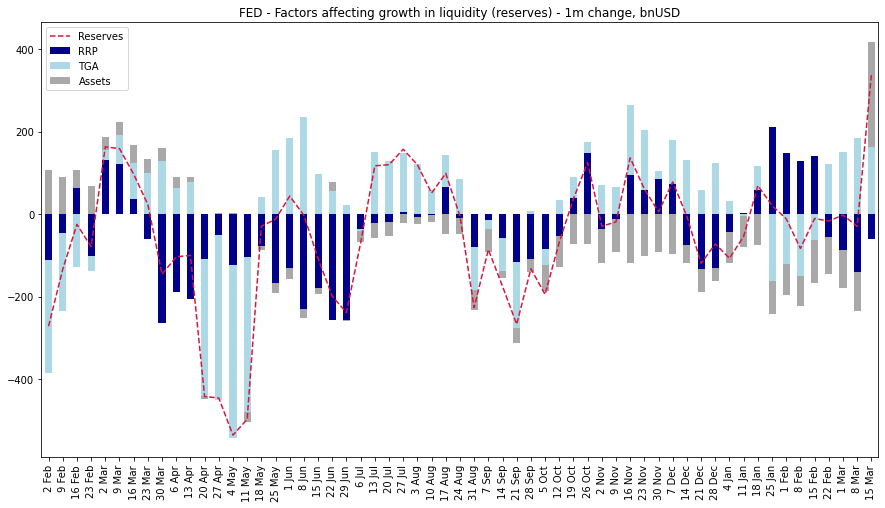

The Federal Reserve never died. In fact, The Fed is growing its balance sheet again. Why? A slowing economy and weakness in the banking sector (thanks to inflation and the Fed trying to get inflation back to 2%.

And the banking fiasco keeps rolling, particularly in Europe where Credit Suisse has been in the news for failing and now my former employer, Deutsche Bank (aka, The Teutonic Titanic).

Deutsche Bank AG became the latest focus of the banking turmoil in Europe as ongoing concern about the industry sent its shares slumping the most in three years and the cost of insuring against default rising.

The bank, which has staged a recovery in recent years after a series of crises, said Friday it will redeem a tier 2 subordinated bond early. Such moves are usually intended to give investors confidence in the strength of the balance sheet, though the share price reaction suggests the message isn’t getting through.

“It is a clear case of the market selling first and asking questions later,” said Paul de la Baume, senior market strategist at FlowBank SA. “Traders do not have the risk appetite to hold positions through the weekend, given the banking risk and what happened last week with Credit Suisse and regulators.”

Deutsche Bank slumped as much as 15%, the biggest decline since the early days of the pandemic in March 2020. It was the worst performer in an index of European bank stocks, which fell as much as 5.7%. Crosstown rival Commerzbank AG, Spain’s Banco de Sabadell SA and France’s Societe Generale SA also saw steep drops.

The widespread declines undermine hopes among authorities that the rescue of Credit Suisse Group AG last weekend would stabilize the broader sector. Central banks from the Federal Reserve to the Bank of England this week raised interest rates once again, keeping their focus on inflation amid hopes that the worst of the financial turmoil was past.

All week, regulators and company executives have sought to reassure traders about the health of the banking industry. Deutsche Bank management board member Fabrizio Campelli said Thursday that the government-brokered takeover of Credit Suisse by UBS is “no indication” of the state of European banks.

Standard Chartered Plc Chief Executive Bill Winters said Friday that while there are still some issues to be addressed, “it seems that the acute phase of the crisis is done.”

The latest moves in Europe follow losses in US banks, which tumbled Thursday even after Treasury Secretary Janet Yellen told lawmakers that regulators would be prepared for further steps to protect deposits if needed.

And apparently bank bailouts never died. They just got relabeled.

And on growing banking fears, the 10-year Treasury yield is down -11.7 basis points.

{kind=link}

You must be logged in to post a comment.