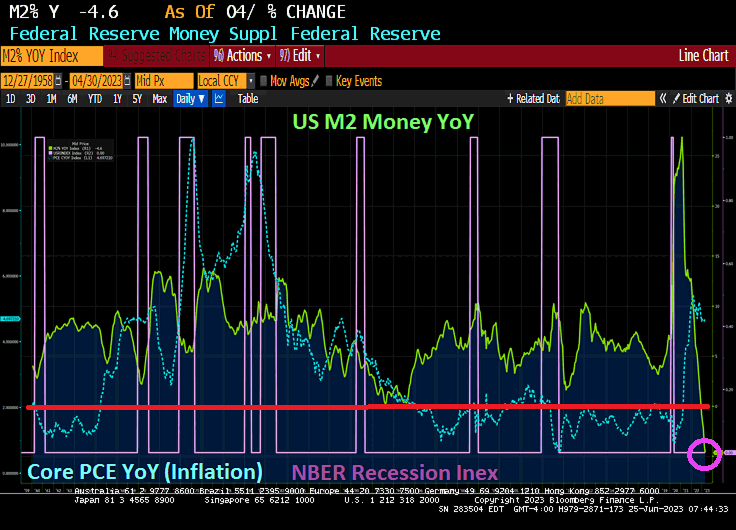

Money supply growth fell again in April from Jerome Powell And The Fed, plummeting further into negative territory after turning negative in November 2022 for the first time in twenty-eight years. April’s drop continues a steep downward trend from the unprecedented highs experienced during much of the past two years.

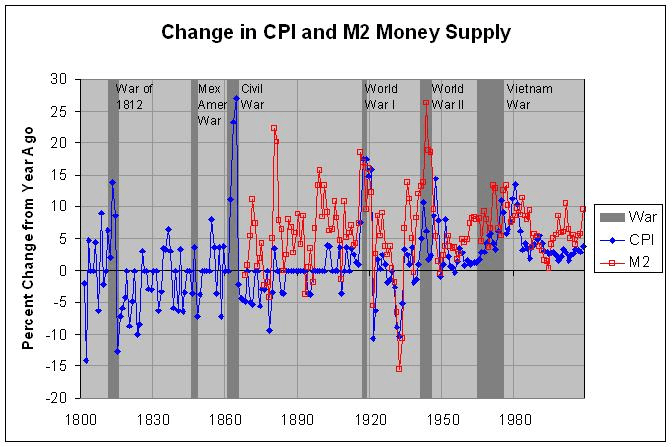

Yes, The Fed is printing money like it is going out of style! The war on Covid was similar to other wars fought where the US printed boatloads of money to pay for WWI. WWII, Korea and Vietnam wars. And the war against the middle class (known as The Best Depression). Apparently, The Fed is still waging war against the middle class.

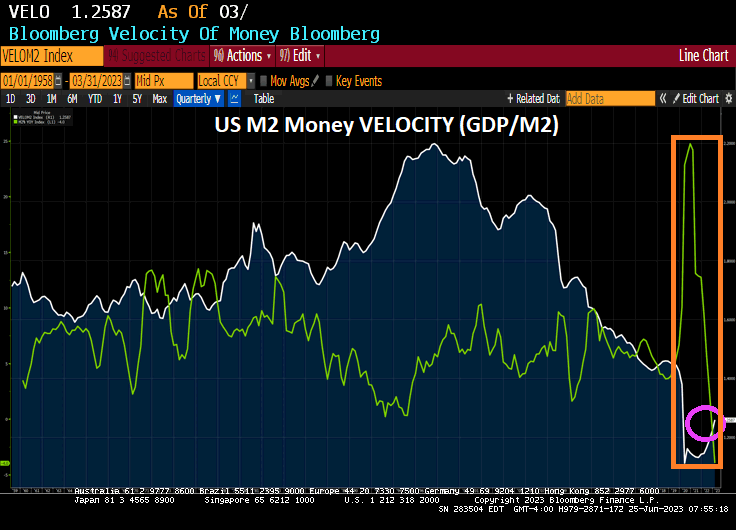

US M2 Money VELOCITY (GDP/M2) is near an all-time low after The Fed went berserk with money printing to combat the Covid economic and school shutdowns.

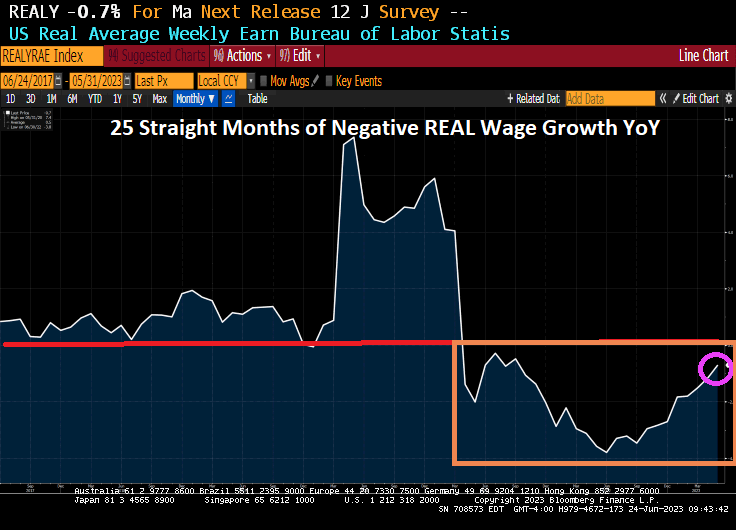

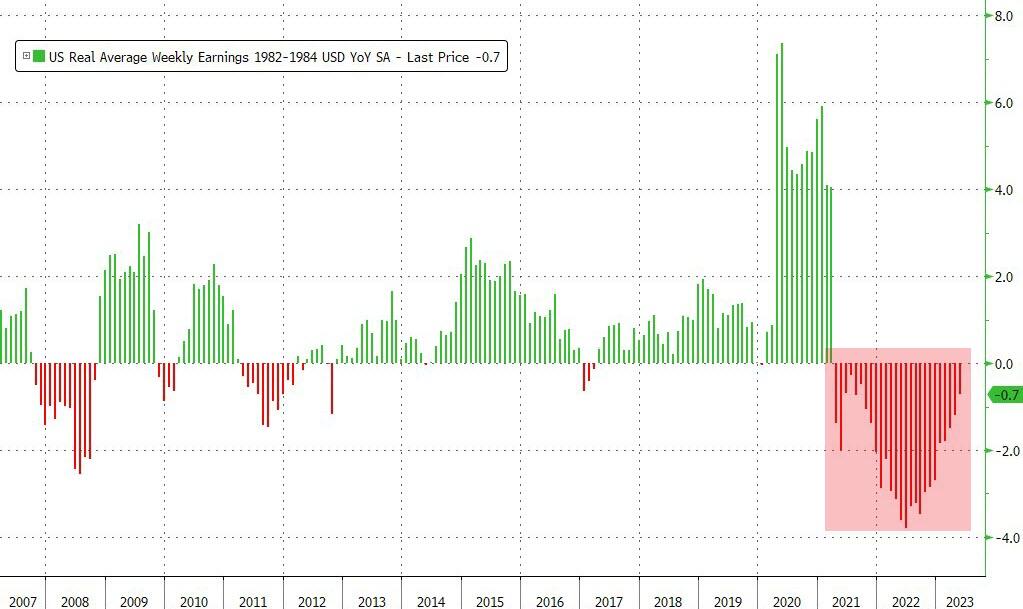

Then with The Fed’s massive monetary expansion and sudden contraction, we have REAL average weekly earnings growth YoY in negative territory for 25 straight months.

The Walking Dead’s Negan, the poster child for The Federal Reserve.

The US is Living La Vida Biden (living the Biden life!) Which means you are making millions if you are a political elite, but suffering if you live on Main Street.

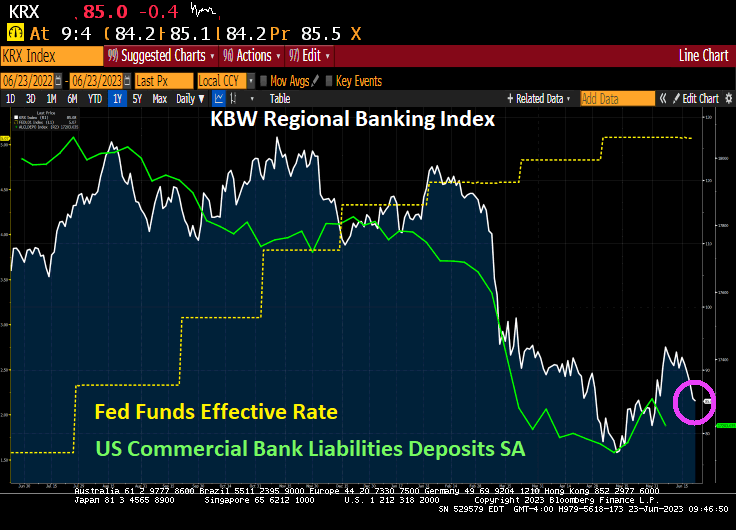

And regional banks (not the TBTF national banks) continue to suffer. The Bank Term Funding Program (1 of 2) is skyrocketing as The Fed cranks up rates to fight BidenFedflation (a combination of excessive monetary stimulus by The Fed and Biden’s lousy economic policies) and M2 Money growth crashes.

The regional banking index continues to fall as bank deposits shrink (like me when I used to jump in the Pacific Ocean in Santa Cruz).

Cryptos down this morning. But Bitcoin is above $30,000 … again.

Oil is down this morning but gold and silver are up slightly.

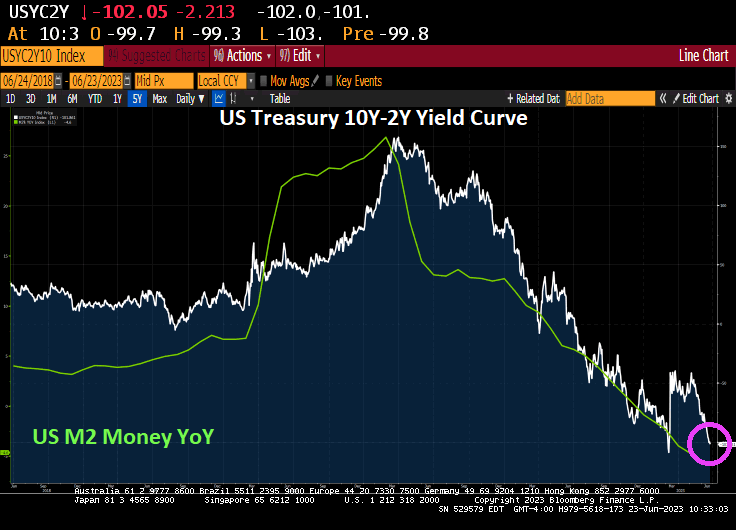

The 10Y-2Y US Treasury yield curve just dipped below -100 basis points (steep inversion) as M2 Money growth crashed and burned.

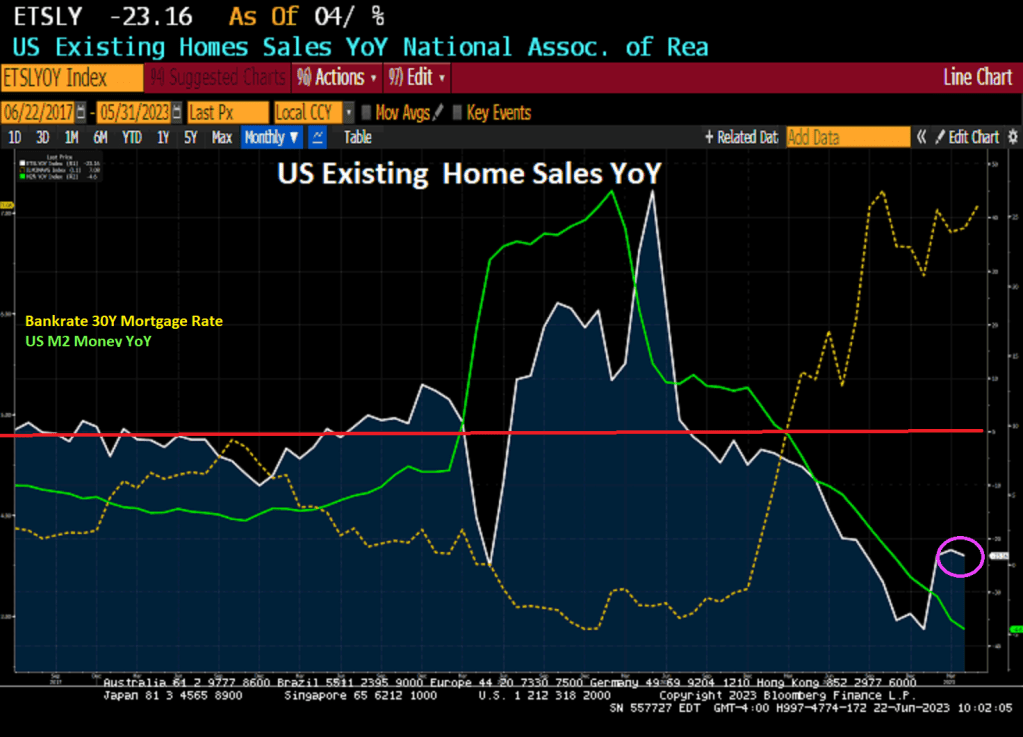

Like a bad good news, bad news joke, the good news is that US existing home sales ROSE 0.2% in May. The bad news? Existing home sales are DOWN -23.16% on a year-over-year basis.

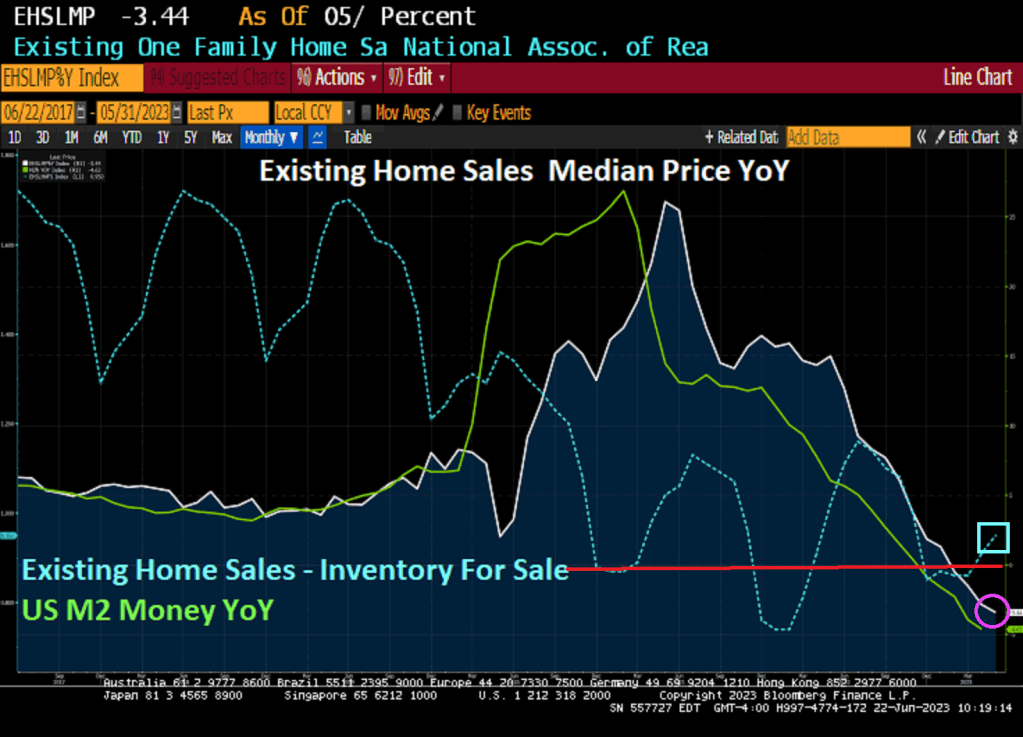

And the median price of existing home sales fell -3.44% YoY as inventory for sales remains missing in action (like Biden debating Democrat challengers).

Expect a hawkish Fed Chairman Jerome Powell to double down on the Fed’s commitment to vanquish inflation at his semiannual testimony before Congress on June 21-22. While the immediate audience will be lawmakers, the message will be aimed at markets, which remain unconvinced the Fed will hike by another 50 basis points, as indicated in the dot plot from the June FOMC meeting. Powell may raise his hawkish tone to push back against such views.

Even as Powell is putting on a hawkish performance, confirmation hearings for World Bank Executive Director Adriana Kugler — as well as to extend Fed Governor Lisa Cook’s term — could reinforce the dovish faction on the Fed, somewhat diluting Powell’s message.

What we expect at the June 21-22 hearings:

The updated dot plot from the June FOMC meeting shows a majority of FOMC participants anticipate at least 50 bps more of rate hikes this year. Markets aren’t convinced – as of the time of writing, futures point to a 74% chance of rate hike in July and only a 10% chance of an additional rate hike in 2023.

Powell’s main task at the testimony will be to convince markets that officials stand behind the dot plot and anticipate multiple hikes.

Powell will likely be asked why the FOMC didn’t hike in June if inflation remains a threat. He’ll say that 500 bps of hikes to date allow the central bank to moderate its pace while gauging economic conditions, and will appeal to the Fed’s dual mandate as warranting a cautious approach. That will be music to the ears of Democrat lawmakers.

Powell said a decision on whether to hike at the July FOMC meeting will be “live.” We take that to mean the bar not to hike will be high, but it’s not a done deal. Powell will likely clarify that comment at his testimony.

The published semiannual monetary policy report offers a preview of how Powell will make the hawkish case:

While the labor market is still “very tight,” it has been softening gradually — and by some measures, labor-market tightness has eased “more substantially over the past year.”

Some outside studies are arguing that wages did not contribute to or lead inflation, but the monetary-policy report notes that “prospects for slowing inflation may depend in part on a further easing of tight labor-market conditions.” Thus, the Fed still stands by the conventional economic wisdom that the Phillips Curve is well and alive – and that a tradeoff exists between inflation and the unemployment rate.

Powell will probably reiterate that low inflation is a necessary condition for achieving the Fed’s mandate, as he has many times before: “Restoring price stability is essential to set the stage for achieving maximum employment and stable prices over the longer run.”

Our view is that if inflation remains as high as the FOMC projects, it would be appropriate for the Fed to hike by at least 50 bps more. But the latest batch of indicators show some encouraging progress on goods and housing disinflation; as a result, our baseline is for inflation to fall short of the median FOMC participant’s forecast.

The Senate Banking Committee hearing on the nominations of Cook, Kugler and Vice Chair Philip Jefferson will likely be less eventful. During this period of high inflation, nominees will need to lean more hawkish in their public statements than they otherwise would.

Nevertheless, if the full slate of nominees is confirmed, it will add one more dove to the board of governors, heightening discord on the FOMC.

Jefferson’s nomination to the vice-chair post vacated by Lael Brainard won’t affect policy direction, as he’s already serving on the board. He previously was confirmed by a vote of 91-7, and we expect his confirmation as vice chair to be similarly easy.

Though we have yet to hear much from Kugler on her monetary-policy outlook, her research focus on labor markets creates a likely bias toward the maximum-employment element of the Fed’s dual mandate.

In addition to Jefferson and Kugler’s nominations, Cook — whose term is slated to end in January 2024 — would see her governorship extended for the full 14-year term. If confirmed, it would keep her dovish voice on the FOMC longer than before.

Cook, who is perceived as more dovish and more political than the other nominees — she’s a former adviser to the Biden transition team – saw her previous nomination barely confirmed 51-50, with Vice President Kamala Harris casting the tie-breaking vote. It’s unclear if she’ll have enough support this time to clear the confirmation hurdle.

Bottom line: The hearings present an opportunity for Powell to bring market pricing in line with what has been put forth in the FOMC’s Summary of Economic Projections. We are doubtful that he will succeed.

The most recent Fed dots plot suggests rate declines in future years.

Cryptos are up this morning.

Commodities are down this AM.

So, like in the film Blue Velvet, we have the choice between Michelob or Pabst Blue Ribbon. Powell is choosing …. PBR!!

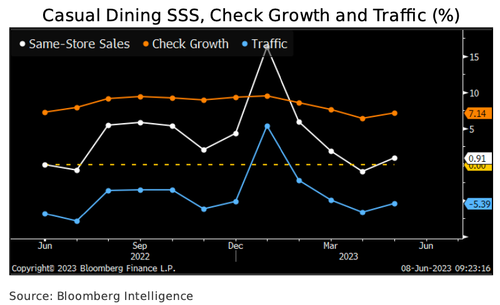

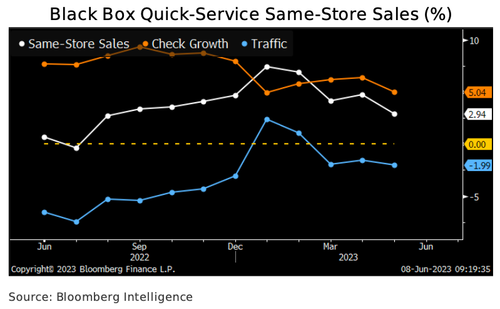

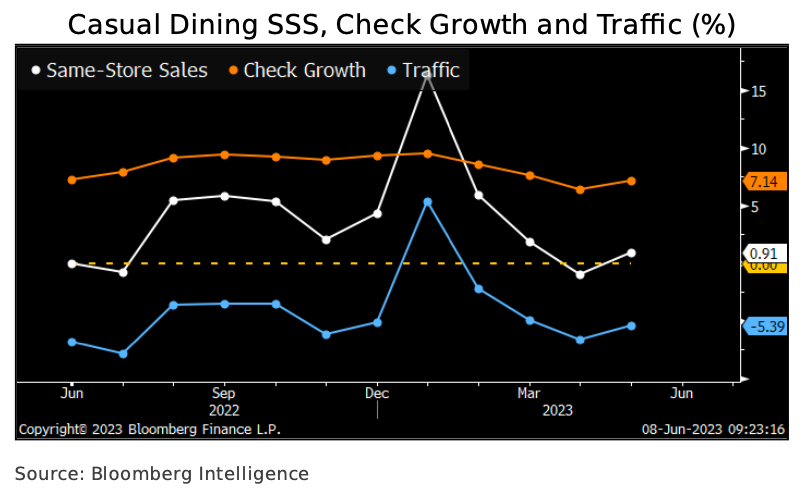

Bloomberg Intelligence’s Michael Halen penned a new note titled “2H Restaurant Sales: Inflation Killing Appetites.” It outlines, “Consumer spending finally buckles under more than two years of inflation and price hikes,” and the likely result is a trade-down of casual-dining chains like Brinker and Cheesecake Factory for quick-service chains like McDonald’s and Wendy’s.

The trade-down, which could start as early as this summer, is expected to dent consumer spending in restaurants such as Cheesecake Factory, Texas Roadhouse, and at brands operated by Brinker and Darden, Halen said.

Casual-dining industry same-store sales rose just 0.9% in May, according to Black Box Intelligence, as traffic dropped 5.4%. We expect cash-strapped low- and middle-income diners to cut restaurant visits and checks through year-end due to more than two years of real income declines and ballooning credit-card balances.

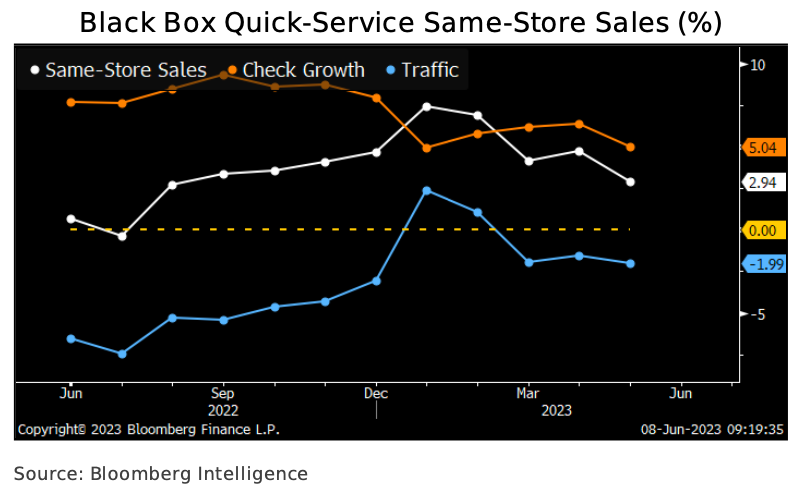

Halen provides more details about quick-service restaurants to fare better than causal-dining ones as “consumer spending finally buckles.”

Quick-service restaurants’ same-store sales could moderate with consumer spending in 2H but should fare better than their full-service competitors. Results rose 2.9% in May, according to Black Box data, as a 5% average-check increase was partly offset by a 2% guest-count decline. Check- driven comp-store sales gains are unsustainable, and we think inflation and menu price hikes will motivate low- and middle-income diners to reduce restaurant visits and manage their spending in 2H. On Domino’s 1Q earnings call, management said lower-income consumers shifted delivery occasions to cooking at home. Still, a trade-down from full-service dining due to cheaper price points may cushion the blow.

McDonald’s, Burger King, Wendy’s, and Jack in the Box are among the quick-service chains in Black Box’s index.

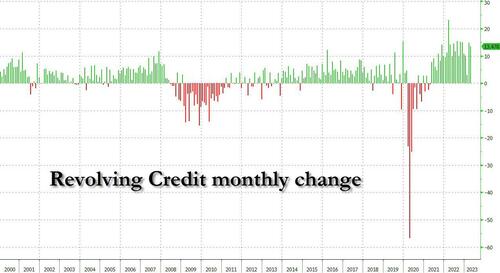

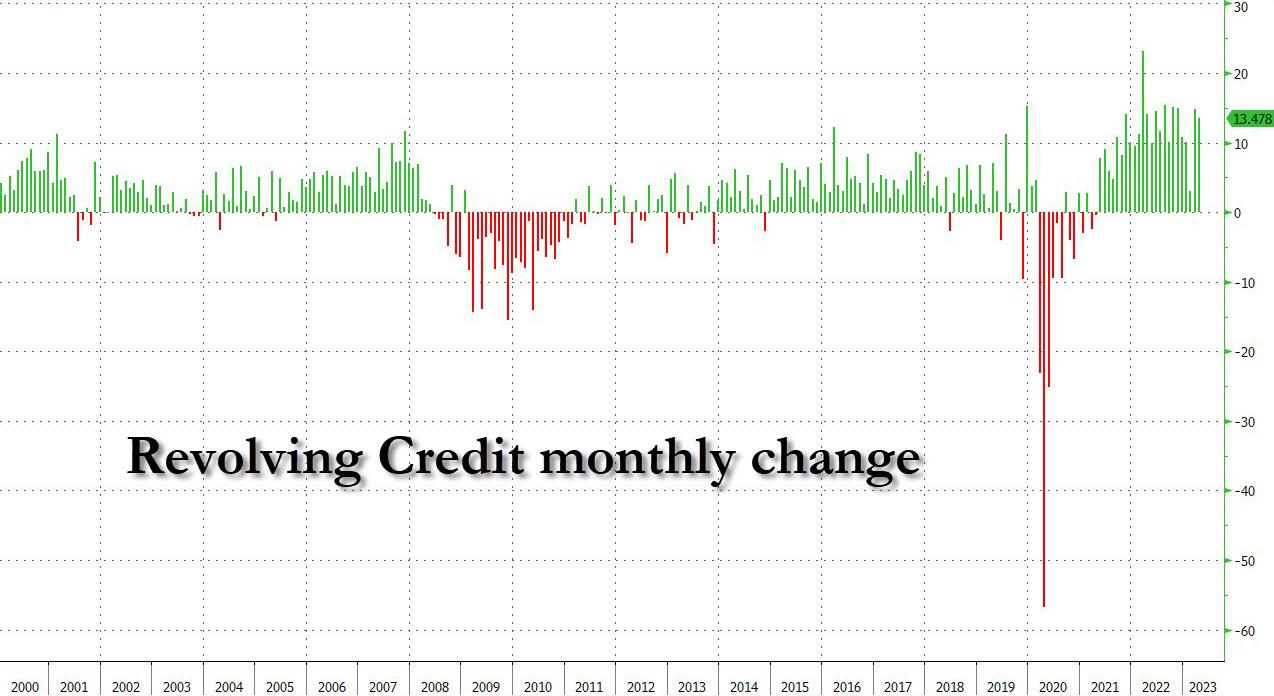

The latest inflation data shows consumers have endured the 26th straight month of negative real wage growth. What this means is that inflation is outpacing wage gains. And bad news for household finances, hence why many have resorted to record credit card usage.

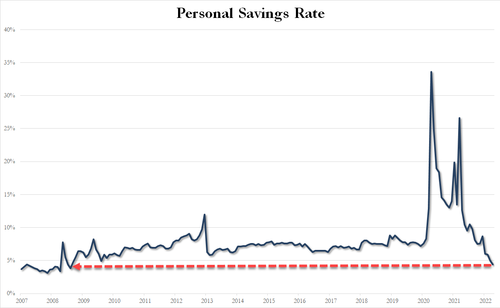

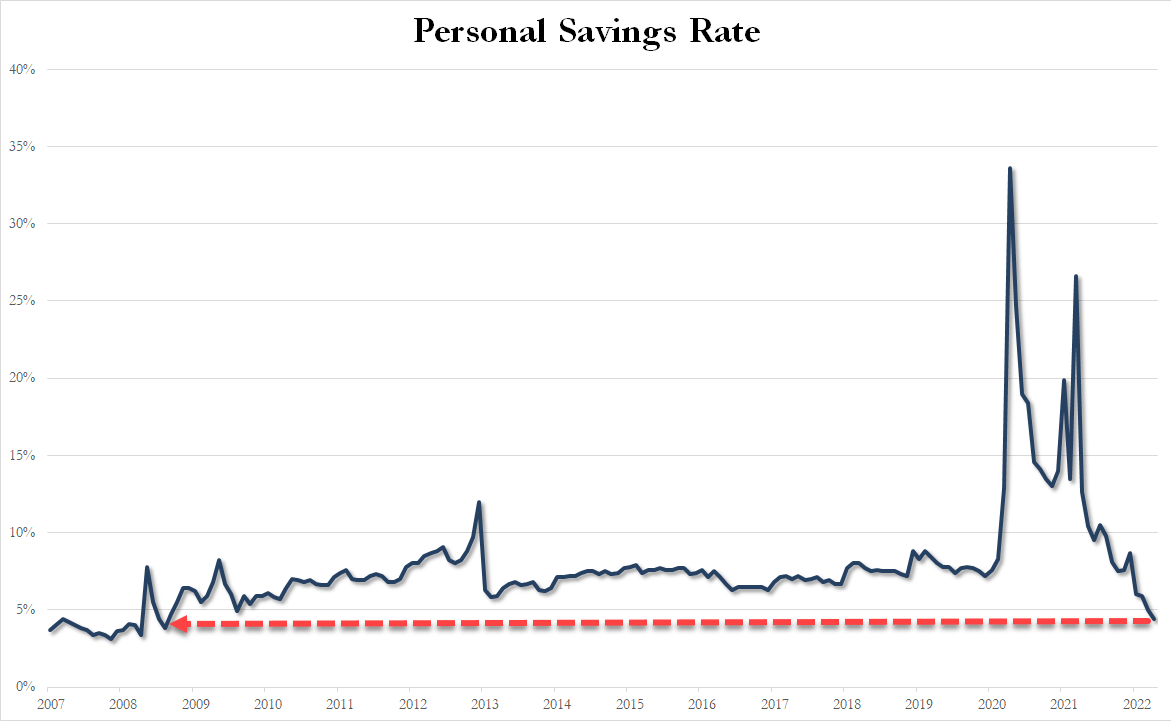

And the personal savings rate has collapsed to just 4.4%, its lowest level since Sept. 2008 (the dark days of Lehman). And why is this? To afford shelter, gas, and food, consumers are drawing from emergency funds due to the worst inflation storm in a generation.

As revolving consumer credit has exploded higher and the last two months have seen a near-record increase…

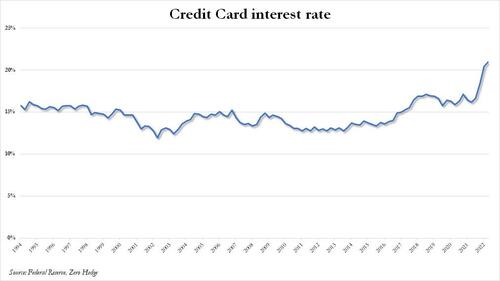

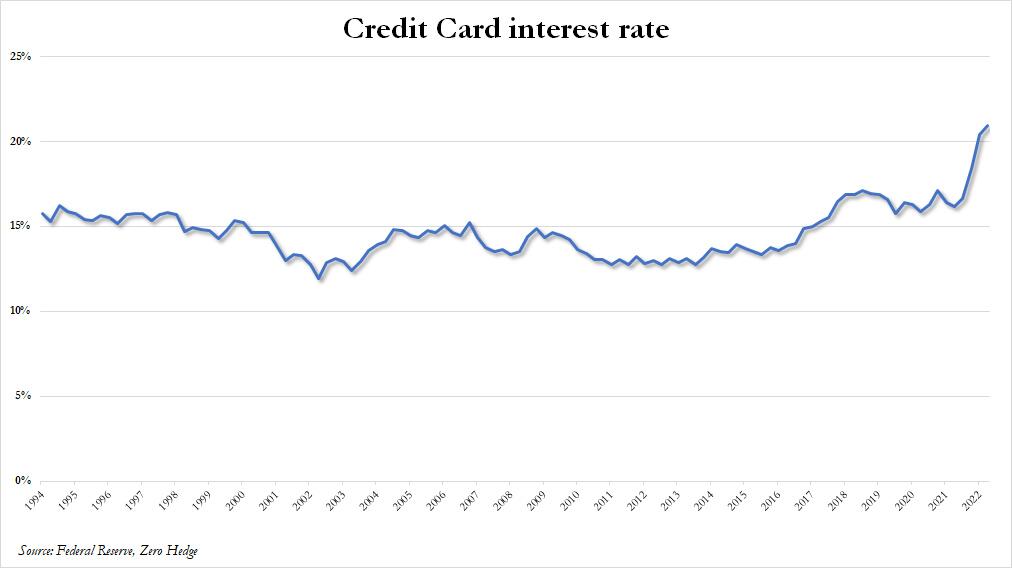

… even as the interest rate on credit cards has jumped to the highest on record.

With record credit card debt load and highest interest payments in years, plus depleted savings, oh yeah, and we forgot, the restart of student loan payments later this year, this all may signal a consumer spending slowdown at causal diners while many trade down for McDonald’s value menu. Even then, we’ve reported consumers have shown that menu items at the fast-food chain have become too expensive.

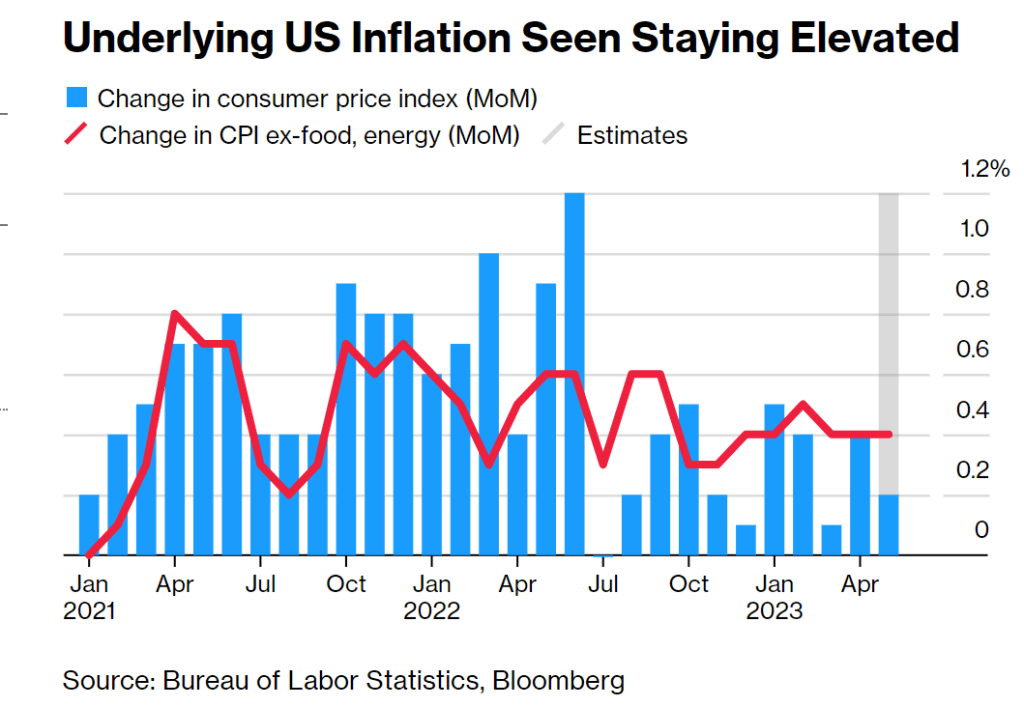

Federal Reserve policymakers are about to take their first break from an interest-rate hiking campaign that started 15 months ago, even as they confront a resilient US economy and persistent inflation.

The Federal Open Market Committee on Wednesday is expected to maintain its benchmark lending rate at the 5%-5.25% range, marking the first skip after 10 consecutive increases going back to March of last year. While officials’ efforts have helped to reduce price pressures in the US economy, inflation remains well above their goal.

Source: Bureau of Labor Statistics, Bloomberg

Investors’ focus will be on the Fed’s quarterly dot plot in its Summary of Economic Projections, which is expected to show the policy benchmark rate at 5.1% at the end of 2023.

By contrast, markets are pricing in the possibility of a quarter-point hike in July followed by a similar-sized cut by December, and some Fed policymakers have emphasized that a pause in the hiking cycle shouldn’t be seen as the final increase.

Fed Chair Jerome Powell, who’ll hold a press conference after the meeting, has suggested he favors a break from hiking to assess the impact both of past moves and of recent banking failures on credit conditions and the economy. His commentary will be scrutinized for hints of the committee.

Remember, there is still over $8 TRILLION in Fed assets held sloshing around the economy. The Fed never really removed the excess liquidity and it continues to stoke asset bubbles.

Bear in mind that The Fed is pausing at 5.25% Fed Target Rate, while the Taylor Rule suggests rate hikes to 10.12%. So, Foul Powell is pausing at just over the half way mark.

Of course, Biden’s and Congress’ massive spending spree is causing inflation, and The Fed has no control over Biden/Congress irresponsible spending.

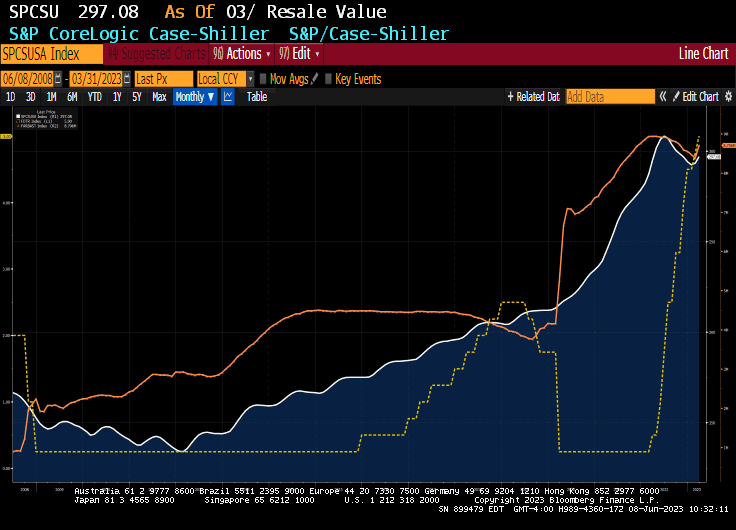

But it isn’t just San Francisco. Phil Hall reports that Fitch Ratings reduced its 2023 outlook for the U.S. real estate investment trust (REIT) sector outlook from “Neutral” to “Deteriorating,” citing the tumult in the commercial real estate space.

While Fitch noted that most of its rated REITs “have the capacity to withstand such a slowdown within rating sensitivities [and] those with ample dry powder could capitalize on distressed property sales by weaker capitalized players.” But at the same time, the ratings agency warned that banks – which account for nearly half of the $5.5 trillion commercial mortgage market – saw their lending levels drop by 20% between February and April, with more tightening expected.

“At minimum, this will lead to further contractions in CRE credit, further limiting conditions for property transactions,” Fitch added in its announcement of the outlook reduction, adding that “CRE transaction volume has steadily declined since early 2022 due to the confluence of operating fundamentals pressure, higher interest and capitalization rates, limited buyer financing, and looming recession risk. The rapid jump in rates has resulted in unusually wide value discrepancies between buyers and sellers across most property types and markets, particularly in the struggling office sector. Our forward-looking U.S. equity REIT ratings incorporate assumptions about future property disposition volumes and valuations.”

Fitch predicted the U.S. economy will go into a recession, most likely late in the year – a previous forecast put the downturn at mid-year – and forecasted property performances will vary by sector over the next two years.

“Sectors experiencing strong fundamentals, such as industrial and shopping centers, will likely see some cooling in demand, with tenants showing greater reluctance to lease space, including delaying decisions, resulting in less pricing power for landlords,” Fitch continued. “Tighter lending conditions and weaker economic growth will add to the secular pressures facing some property formats (e.g. office, enclosed malls). The office REIT sector has met, or modestly underperformed, our low expectations during 2023. Leasing volumes have generally underperformed as occupiers add the business cycle to the list concerns and reasons for conservatism, along with secular pressure from remote work. Conversely, the industrial sector, although no longer white hot, continues to deliver above average occupancies and outsized rent growth that have modestly exceeded our projections.”

While Fitch stressed that REITs were “unlikely to directly encounter meaningful stress” based on the recent problems in the banking industry, although it also acknowledged that it did not expect “REITs’ access to unsecured revolvers will be impeded, although facilities up for renewal will likely see higher pricing and some banks have reduced appetites for traditional bank syndicate activities, such as making funded term loans – particularly in hard hit sectors, such as office. We also do not expect meaningful portfolio vacancies caused by bank tenant failures, which are unlikely to be widespread.”

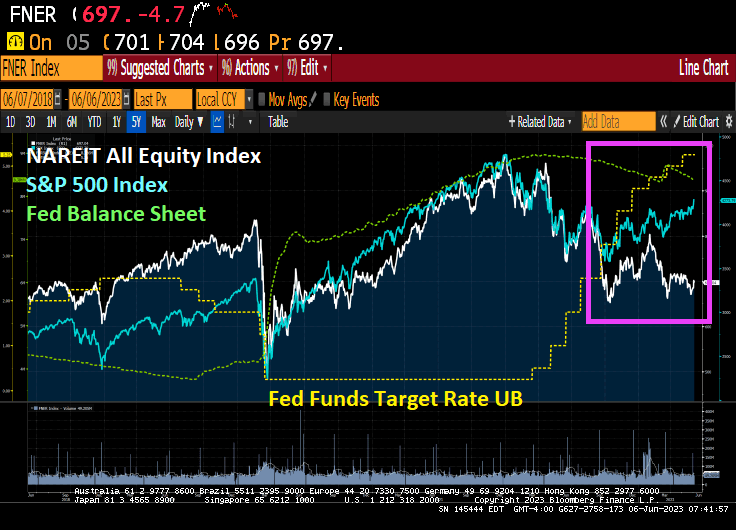

The NAREIT All-equity index has gotten pummelled by the S&P 500 index since The Fed started tightening monetary policy to fight inflation …. that The Fed helped cause in the first place.

Under Biden, the US is beginning to morph into a lawless Socialist sewer like Venezuela. Joe Maduro??

It is not a surprise that the ill-advised COVID economic shutdowns would harm small businesses that large corporations.

Yes, The Fed’s M2 Money printing press went wild with COVID emergency refief. And so did the discrepancy between the top 1% and the bottom 50% in terms of “Share of Total Net Worth Held.” The top 1% is in blue and the bottom 50% is in red. M2 Money is in green.

Compared to pre-COVID, the top 1% increased their share of total net worth from 29.7% to 31.9%, an increase of 7.4% since January 2020. The bottom 50% fell from 30% to 28.5%, a -5% decline. An elitist wonderland!

And The Biden family keeps raking in the money far about Joe’s salary.

And I assume Fed Chair Jerome Powell and Treasury Secretary Janet Yellen also made fortunes from COVID relief.

Well, Biden and McCarthy have agreed in principle to a budget revision, raise the debt ceiling and avoid a US debt default. The Uniparty strikes again! No restraint of reckless Federal spending t speak of . The big donor class wins and middle class Americans lose.

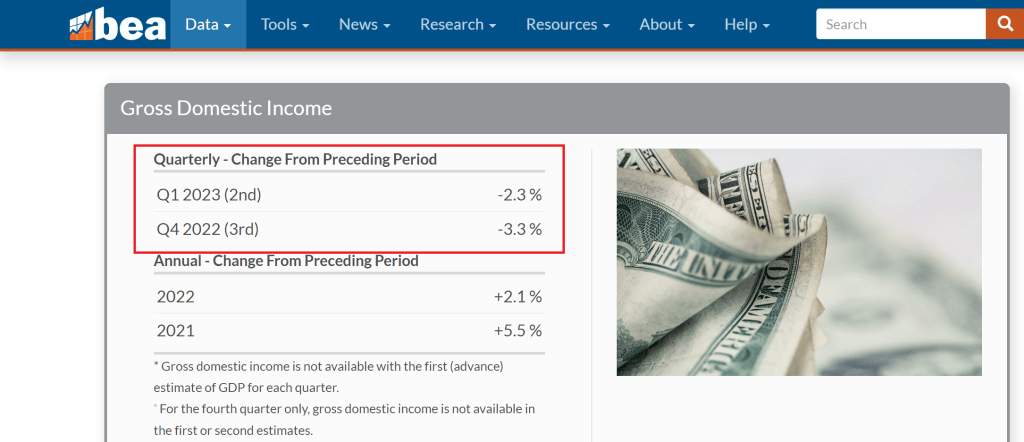

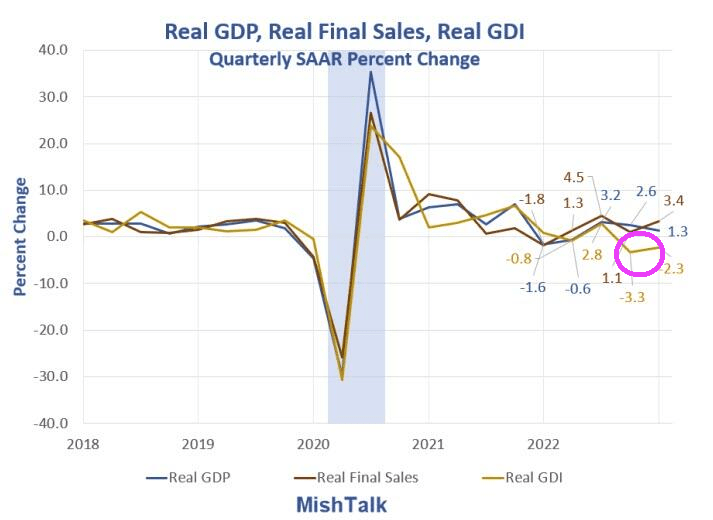

Mike Shedlock (aka, Mish) makes a good point: the US is already in recession if we look at GDI (gross domestic income) rather than GDP (gross domestic product). The US has already declined two consecutive quarters in terms of negative GDI growth.

First, Biden didn’t “balance the budget” liked he claimed at Hiroshima. In fact, the Federal budget deficit, while improving, is still worse than it was before the 2020 Covid economic shutdown.

Biden, Schumer and Yellen are ignoring the $187 TRILLION in UNFUNDED entitlements promised America, even though Biden keeps threatening to halt Social Security payments if Biden and Yellen default on the debt. No discussion of the runaway train of entitlemennts.

I love this Bloomberg headline: “(ECB’s) Lagarde Trusts in US Common Sense to Avert Catastrophic Default.” Has Lagarde actually talked to Biden, Harris or Yellen? America’s REAL 3 Stooges??

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.