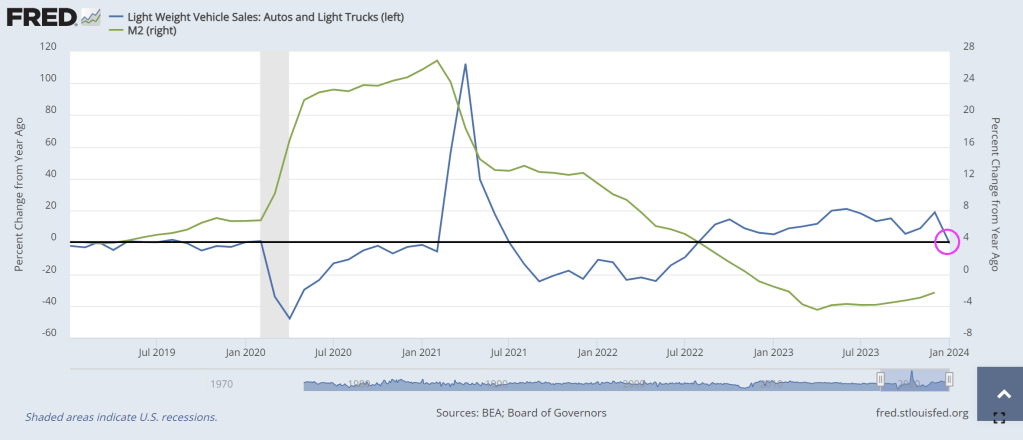

Cars and light trucks are seeing declining YoY sales in January (-0.7%) as M2 Money growth remains negative.

Automotive News was the first to report Ford Motor Co. halted shipments of all 2024 F-150 Lightning electric pickup trucks for an undisclosed quality control issue just weeks after slashing production volumes for the EV model due to sliding demand.

“We expect to ramp up shipments in the coming weeks as we complete thorough launch quality checks to ensure these new F-150s meet our high standards and delight customers,” company spokeswoman Emma Bergg wrote in a statement.

Last month, Ford announced plans to slash the Lightning production in April “to achieve the optimal balance of production, sales growth and profitability.”

The automaker (and many others, like Mercedes Benz) is recalibrating its electric vehicle strategy as the Biden administration plans to downshift the EV transition as demand plummets.

Thousands of auto dealers nationwide recently warned the ‘climate change warriors’ in the White House: the 2030 EV push is backfiring.

“Currently, there are many excellent battery electric vehicles available for consumers to purchase. These vehicles are ideal for many people, and we believe their appeal will grow over time. The reality, however, is that electric vehicle demand today is not keeping up with the large influx of BEVs arriving at our dealerships prompted by the current regulations. BEVs are stacking up on our lots,” the dealers said.

They warned: “Already, electric vehicles are stacking up on our lots which is our best indicator of customer demand in the marketplace.”

“Key takeaways thus far from earnings season are that the EV slowdown is not showing any evidence of an inflection, Level 4 autonomy headwinds continue to persist, and fears over supplier inventory overbuild are likely overblown.

The Hollies said it best: Stop, stop, stop. FIAT Money Printing that is.

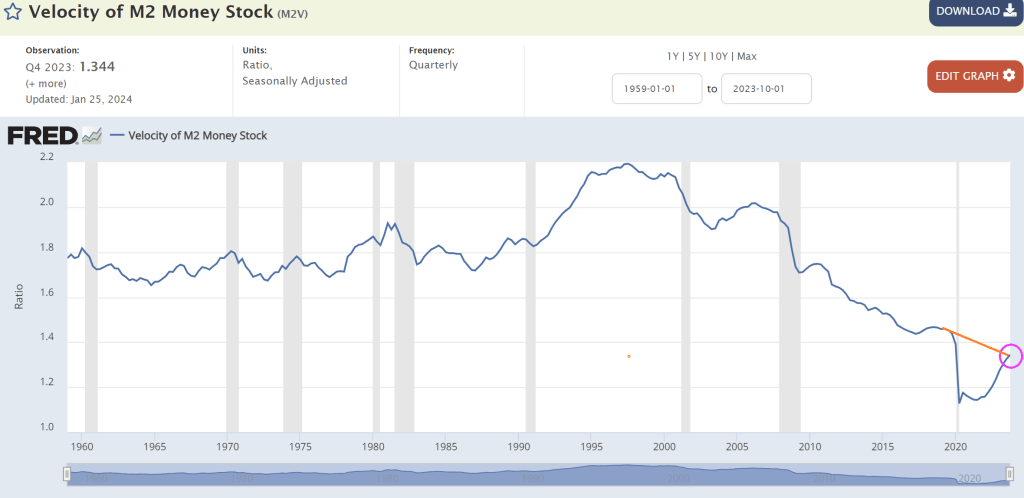

Typically, we look at M2 Money Velocity (GDP/M2) as a measure of how much the economy grows by expanding the money supply.

M2 Money Velocity is currently at 1.344, and still below where we were under Trump prior to Covid. After Powell printing palooza after Covid, M2 Money Velocity collapsed and is slowly rising, but remains low by historic standards.

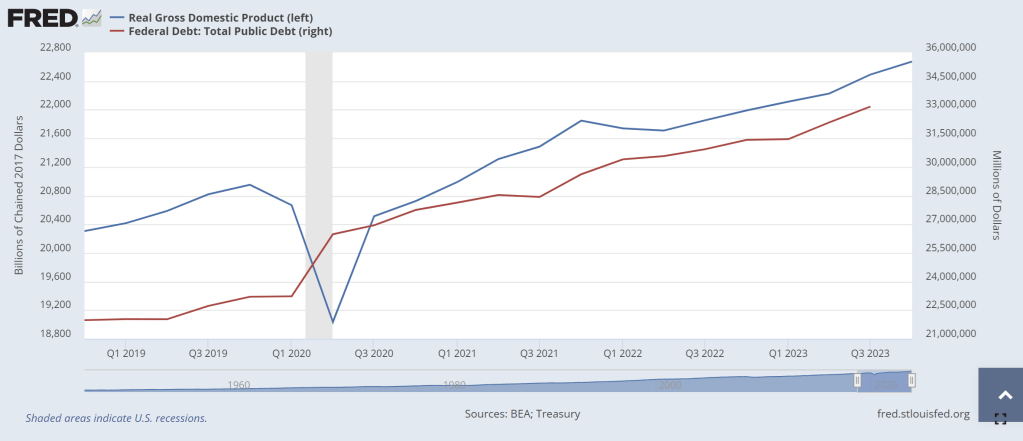

Perhaps a more interest velocity is DEBT velocity (GDP/DEBT). Under Biden’s Reign of Error, Federal debt has increased by $6,539,359 million while real GDP has increased by only $1,948.731 billion (or roughly $2 trillion in GDP growth after $6.54 trillion in debt). Or a DEBT velocity of 0.3. Yikes! No wonder China is bailing on US debt!

This chart makes debt issuance look better than it really is. Again, the DEBT VELOCITY of 0.3 is terrible meaning that for every $1 of Federal debt, we get 30 cents in Real GDP under Biden. One of my macroeconomics textbooks stated that debt growth is fine as long as real GDP growth rises faster than debt growth. Apparently, Treasury Secretary Janet Yellen didn’t read that textbook! Real GDP has grown by 9.43% under Biden while Federal debt has grown by … gulp .. 24%.

Yes, the US is borrowing like the proverbial drunken sailor while they “invest” in green energy, wars in Ukraine and the Middle East, and massive social welfare programs (like the old breads and circuses from the dying Roman Empire). When watching the media’s obsession with Taylor Swift and Chief’s Tight End Travis Kelce at The Super Bowl, it reminded me of “Breads and Circuses” as our nation is collapsing like a dying star. (That is why I Iike Gold, Silver and Bitcoin!)

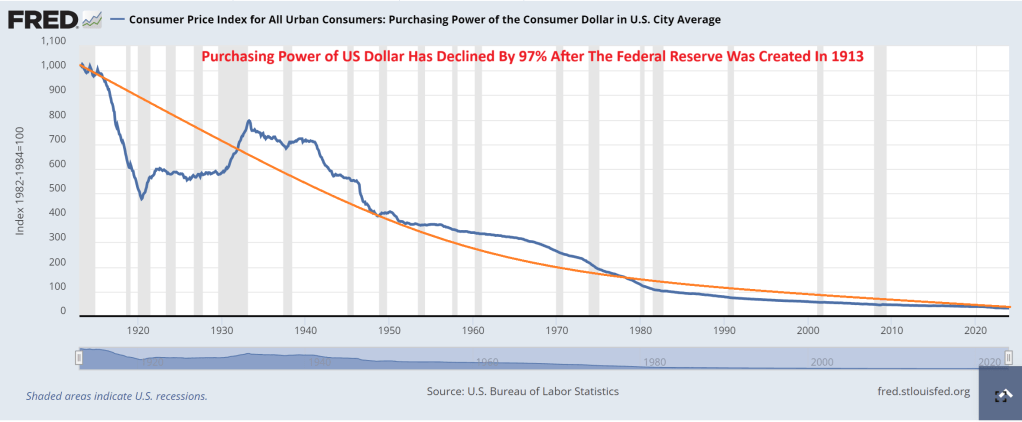

What about The Federal Reserve? It was created in 1913 after signed into existence by President Woodrow Wilson. Since The Fed’s inception, consumer purchasing power has declined by 97%.

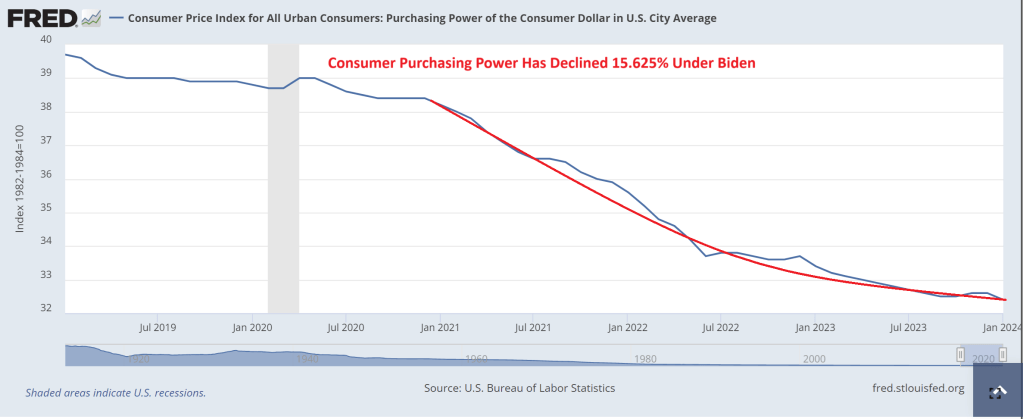

And under Biden, inflation has been so bad that consumer purchasing power is down 16%.

In summary, The Federal Reserve has been printing like crazy (I would say Batshit Crazy, but I actually think bats are adorable). And Treasury (under former Fed Chair Janet Yellen) has been borrowing like crazy too. While politicians claim the economy is in great shape, it is really because The Fed is printing wildly, Yellen is borrowing wildly, and much of US GDP is not due to the private sector, but Federal government spending … to the donor class. This is NOT a sustainable and will eventually crash into a ravine.

Silence is not golden. Particularly when it comes to a silent DEPRESSION. Talking is cheap, people follow like sheep. Particularly when are told by Biden, Press Secretary Karine Jean-Pierre and NY Times economic spinster Paul Krugman say its the best economy in decades. It isn’t. In fact, the US is in a silent depression.

Typically, a recession is defined as two consecutive quarters of negative GDP growth. If we use 2 consecutive quarter of negative GDP growth, we are not in a recession. But ….

Why these results? Bidenomics is based on costly Keynesian boom-and-bust policies. With so much whiplash, it’s no wonder people are conflicted about the economy.

In the latest jobs report for January, a net increase of 353,000 nonfarm jobs from the establishment survey appears robust, as it was well above the consensus estimate of 185,000 new jobs. But let’s dig deeper.

Last month, household employment declined by 31,000, contradicting the headlines. The divergence of jobs added between the household survey and the establishment survey has widened since March 2022. This period coincides with declining real gross domestic product in the first and second quarters of 2022 (usually that’s deemed a recession, but it hasn’t been yet). Indexing these two employment levels to 100 in January 2021, they were essentially the same until March 2022, but nonfarm employment was 2.5 percent higher in January 2024.

While this divergence mystifies some, a primary reason is how the surveys are conducted.

The establishment survey reports the answers from businesses and the household survey from individual citizens. The establishment survey often counts the same person working in multiple jobs, while the household survey counts each person employed. This likely explains much of the divergence, as many people work multiple jobs to make ends meet. The surge in part-time employment and more discouraged workers underscores

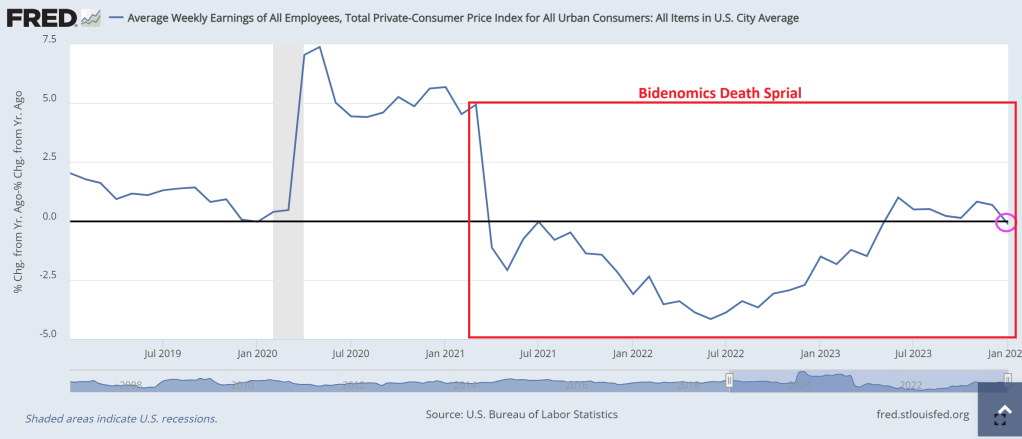

Though average weekly earnings increased by 3 percent in January over a year prior, this is below inflation of 3.1 percent. Real average weekly earnings had increased for seven months before falling last month. And there had been declines in year-over-year average weekly earnings for 24 of the prior 25 months before June 2023. These real wages are down 4.4 percent since Biden took office in January 2021.

As purchasing power declines, mounting debts become more urgent.

Total US household debt has reached unprecedented levels, with credit card debt soaring by 14.5 percent over the last year to a staggering $1.13 trillion in the fourth quarter of 2023. Such substantial growth in debt raises concerns about the current (unsustainable?) consumption trends, business investment, and a looming financial crisis.

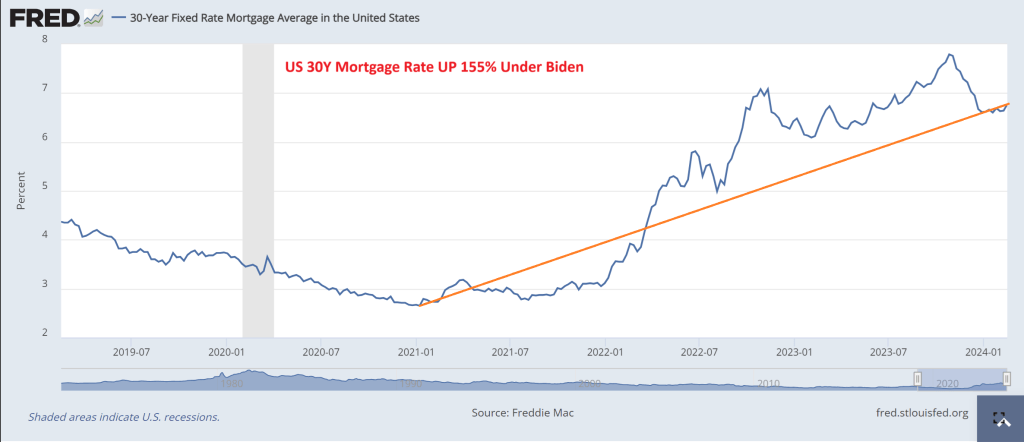

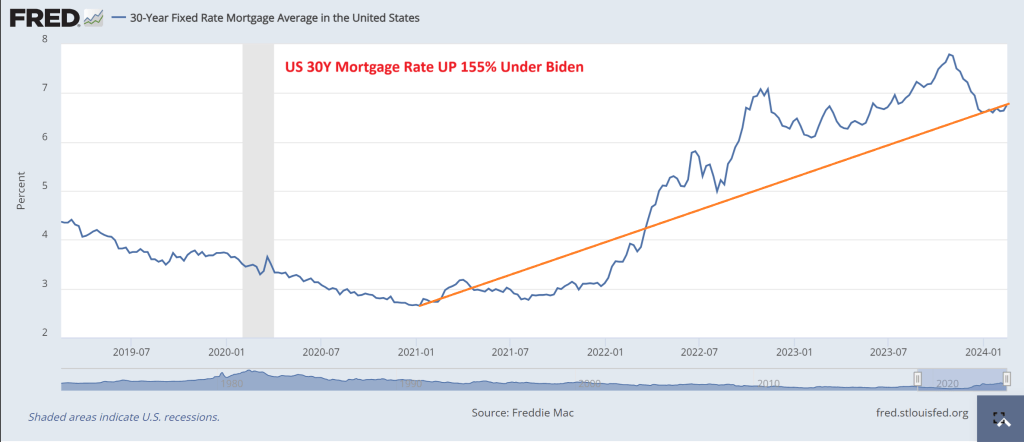

The surge in mortgage rates to over seven percent for the first time since December and rising home prices exacerbate housing affordability challenges, particularly for aspiring homeowners. An integral component of what some consider the “American Dream,” housing affordability is a major factor discouraging Americans. Remember, Bidenomics has seen a 155% increase in mortgage rates.

The euphoria surrounding the January 2024 jobs report is misplaced. Policymakers should heed these warning signs and enact meaningful reforms to address root causes.

Biden’s policy approach undergirds most of these difficulties. Bidenomics focuses on his Build Back Better agenda that picks winners and losers by redistributing taxpayer money for supposed economic gains through large deficit spending (and most of the gains went to political donors).

We haven’t seen an agenda of this magnitude since LBJ’s Great Society in the 1960s or possibly since FDR’s New Deal in the 1930s. Both were damaging, as the Great Society dramatically expanded the size and scope of government, contributing to the Great Inflation in the 1970s, and the New Deal contributed to a longer and harsher Great Depression.

These four bills will add nearly $4.3 trillion to the national debt. But at least another $2.5 trillion will be added to the national debt for student loan forgiveness schemes, SNAP expansions, net interest increases, Ukraine funding, PACT Act, and more. In total over the past three years, excessive spending will lead to more than $7 trillion added to the national debt, which now totals $34 trillion — a 21 percent increase since 2021. There seems to be no end to soaring debt with the recent discussions of more taxpayer money to Ukraine, Israel, the border, and the “bipartisan tax deal,” collectively adding at least another $700 billion to the debt over a decade.

Record debts accrued by households and by the federal government (paid by households) are not signs of a robust economy. This will likely worsen before it improves, as household savings dry up. And with interest rates likely to stay higher for longer because of persistent inflation, debts will crowd out household finances and the federal budget.

The Federal Reserve has monetized much of this increased national debt over the last few years by ballooning its balance sheet from $4 trillion to $9 trillion and back down to a still-bloated $7.6 trillion. This helps explain persistent inflation, massive misallocation of resources, and costly malinvestments across the economy, keeping the economy afloat yet fragile.

Excessive deficit spending weighs heavily on future generations, saddling them with unsustainable debt levels they have no voice in. Today, everyone owes about $100,000, and taxpayers owe $165,000, toward the national debt. Of course, these amounts don’t include the hundreds of trillions of dollars in unfunded liabilities for the quickly-going-bankruptwelfare programs of Social Security and Medicare.

Future generations will be on the hook for even more national debt if Bidenomics continues and Congress doesn’t reduce government spending now. This is why the national debt is the biggest national crisis for America. We’re robbing current and future generations of their hopes and dreams.

Fortunately, there’s a better path forward if politicians have the willpower. This path should be chosen before we reap the major costs of a bigger crisis. Look at Argentina’s president Javier Milei who managed to balance the budget in 60 days and generate a whopping SURPLUS of $589,000,000. How? By cutting massive government waste and closing agencies and programs.

In short, we need a fiscal rule of a spending limit covering the entire budget based on a maximum rate of population growth plus inflation. There should also be a monetary rule that ideally reduces and caps the Fed’s current balance sheet to at least where it was before the lockdowns. My work with Americans for Tax Reform shows that had the federal government used this spending limit over the last 20 years, the debt would have increased by just $700 billion instead of the actual $20.2 trillion. That’s much more manageable and would point us in a more sustainable fiscal and monetary direction.

Together, fiscal and monetary rules that rein in government will help reduce the roles that politicians and bureaucrats have in our lives so we can achieve our unique American dreams. If not, we will have wasted many dreams on Bidenomics that can make things look good on the surface, but cause rot underneath.

Clarification: When Biden and various members of Congress tout Biden as having created more jobs that previous Presidents, that is the ultimate gaslighting of the American people. Trump actually saw more job creation than Biden until Covid struck and politicians shut down the economy (and schools closed). Then like magic, after Biden was elected, many jobs returned. Biden and his lackies take credit for the incredible job market, but NEW jobs (rather than simply old jobs returning) had nothing to do with Biden’s Keynesian policies. Rather, Biden’s policies have helped destroy the jobs market.

And yes, the US is under invasion by the United Nations who are helping millions of migrants ILLEGALLY cross the US border, creating horrible stress on the economy and helping keep inflation high. Not to mention soaring crime. Its as if Biden (and his master Obama) are using the Cloward-Piven strategy of overwhelming the economy so it breaks.

All we hear about from Biden and Schumer (and their ilk) is about spending billions MORE on Ukraine and their oligarchs to “protect their borders” while Biden and Mayorkas (Cuba Pete) leave American borders over to invasion.

Yes, Democrats like The Clintons, Obamas and Bidens LOVE the Cloward-Piven strategy. Hey, they are all multi-millionaires and are insulated from all the damage they inflict on the middle class and low wage workers.

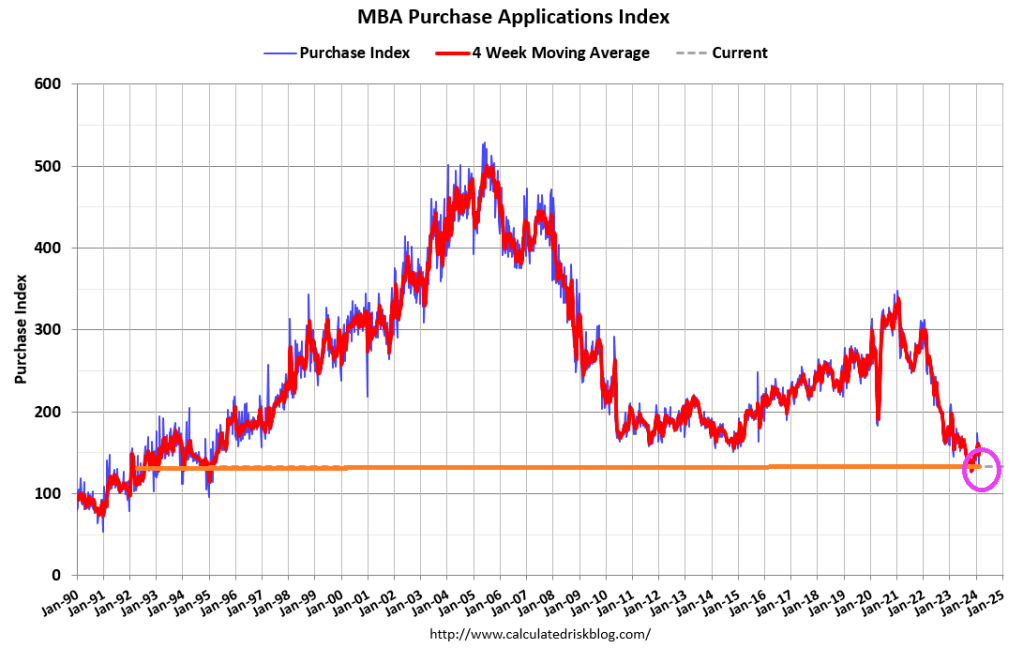

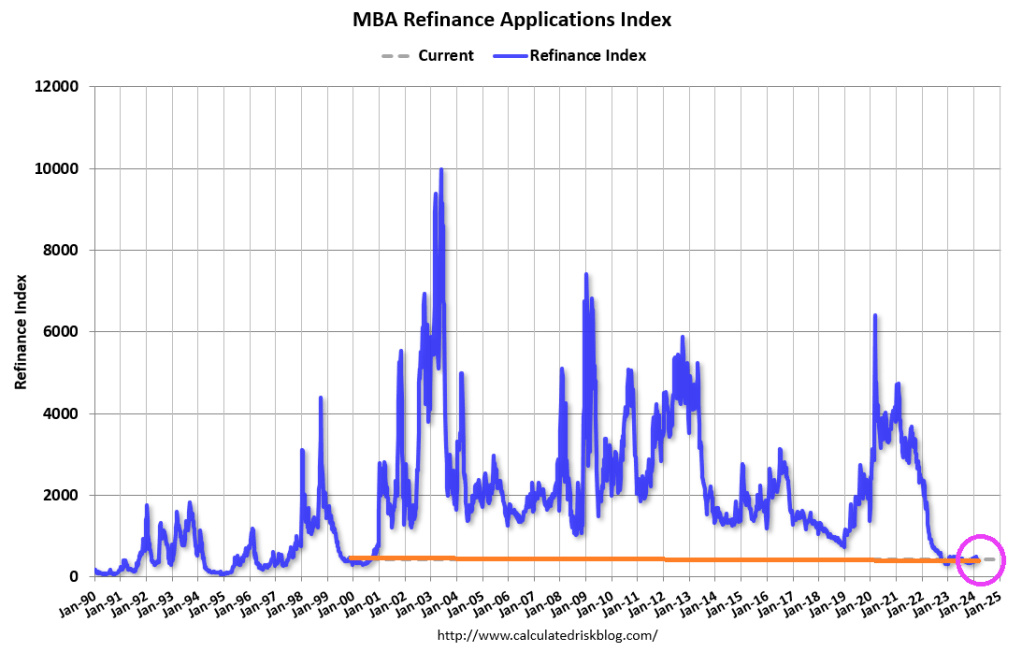

Mortgage applications decreased 10.6 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending February 16, 2024.

The Market Composite Index, a measure of mortgage loan application volume, decreased 10.6 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 8 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 10 percent from one week earlier. The unadjusted Purchase Index decreased 6 percent compared with the previous week and was13 percent lower than the same week one year ago.

The Refinance Index decreased 11 percent from the previous week and was 0.1 percent higher than the same week one year ago.

One reason why mortgage demand is so low is that mortgage rates are up 155% under Biden.

Is it sundown for the US mortgage market? And when will it improve?? Probably won’t improve in New York City after Judge Engmoron’s idiotic fine of Donald Trump and family for non-crimes.

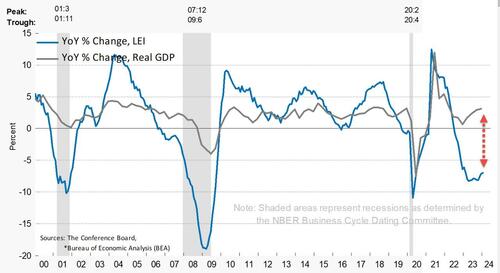

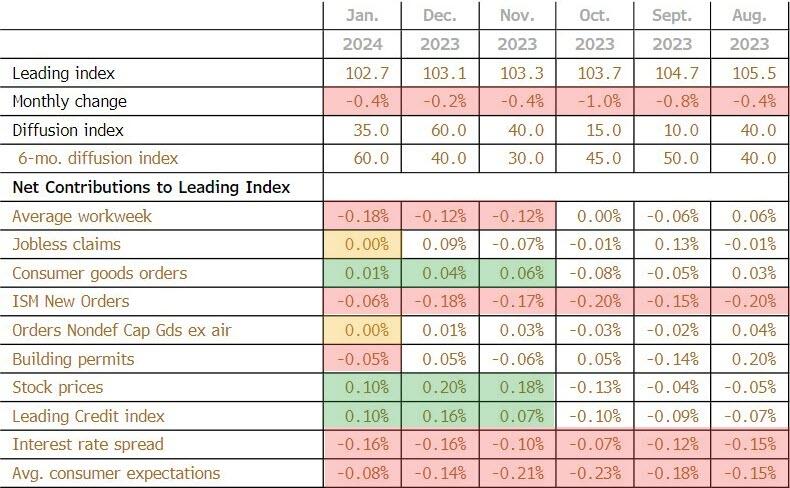

The biggest positive contributor to the leading index was stock prices (again)at +0.10

The biggest negative contributor was average workweek at -0.18

This is the 22nd straight MoM decline in the LEI (and 23rd month of 25) – equaling the longest streak of declines since ‘Lehman’ (22 straight months of declines from June 2007 to April 2008)

“While the declining LEI continues to signal headwinds to economic activity, for the first time in the past two years, six out of its ten components were positive contributors over the past six-month period (ending in January 2024).

As a result, the leading index currently does not signal recession ahead.

While no longer forecasting a recession in 2024, we do expect real GDP growth to slow to near zero percent over Q2 and Q3.”

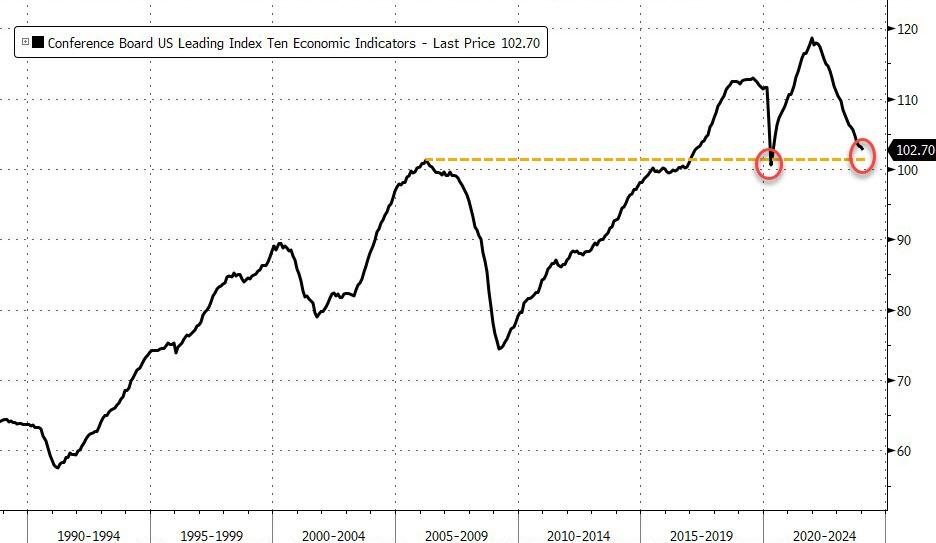

While the Conference Board seems optimistic, we are struggling to see any signs of hope! tumbling back below the peak in March 2006…

And on a year-over-year basis, the LEI is down 7.0% (down YoY for 19 straight months) – still close to its biggest YoY drop since 2008 (Lehman) outside of the COVID lockdown-enforced collapse (but starting to inflect)…

The annual growth rate of the LEI remains deeply negative and decoupled from Real GDP…..

Finally, the massive easing of financial conditions in the last few months suggests a turn in LEI is imminent…

And hence the ‘soft landing’ mission is accomplished… so no need for rate-cuts? (Except for the banking crisis that looms in March).

This headline from Zero Hedge makes me so glad I have eaten heart-healthy Quaker Oats and Cheerios every morning for the last 20 years! Study Finds 80% Of Americans Exposed To Fertility-Lowering Chemicals In Cheerios, Quaker Oats. The chemical (chlormequat chloride) was detected in “92 percent of oat-based foods purchased in May 2023, including Quaker Oats and Cheerios.” But that was nothing compared to this Zero Hedge headline: EU “Suicide Pact” Threatens To Flood Continent With 75 Million More Migrants. Makes me wonder if Biden/Mayorkas are under orders from the UN/WEF/Soros to let immigrants pour across our southern border (including 20,000+ Chinese military age males). But back to the economy.

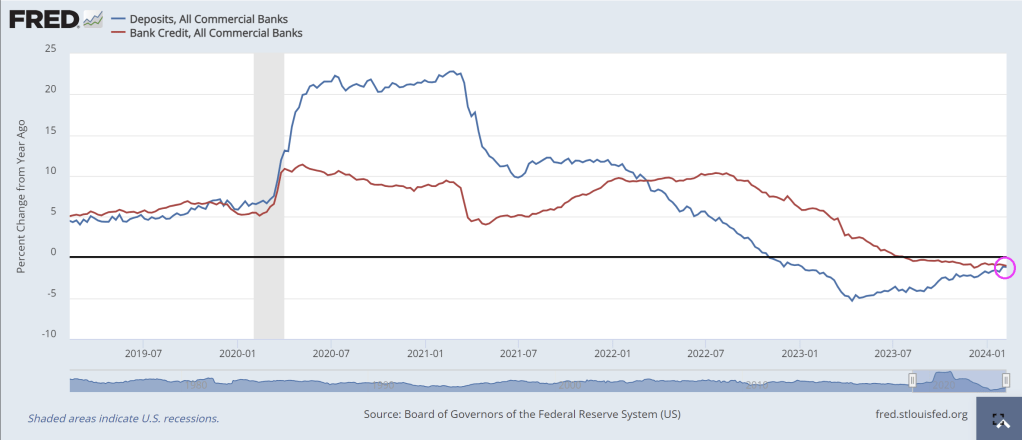

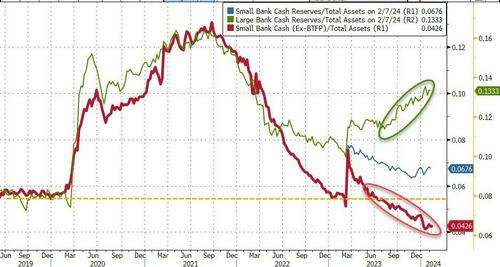

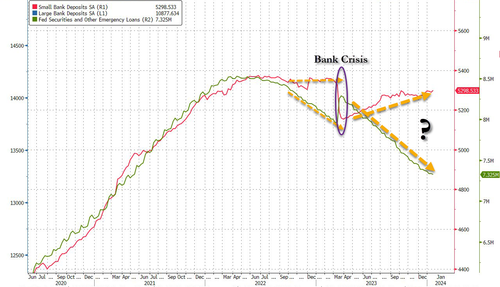

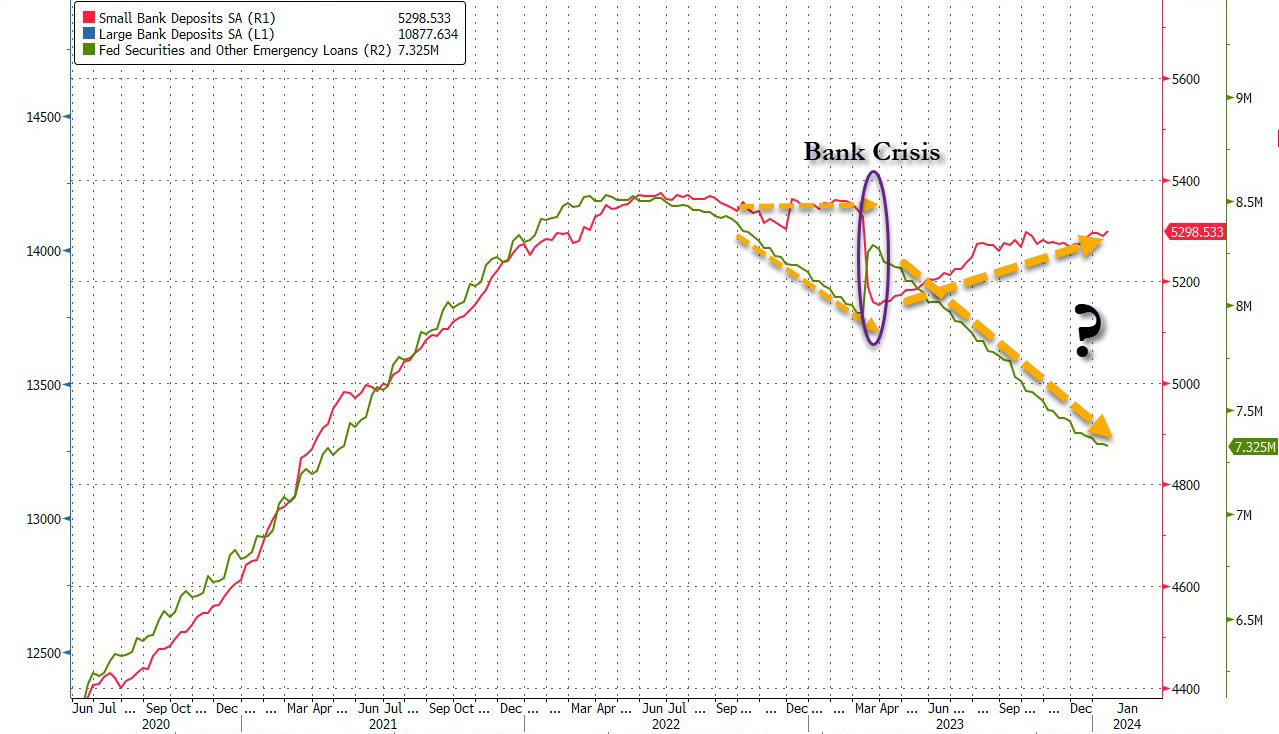

Both bank credit growth year-over-year (YoY) and bank deposit growth (YoY) are NEGATIVE. Covid resulted in massive Federal government stimulus spending (and Federal Reserve hyper stimulus) in 2020, but as the stimulus wears out, so does bank lending and deposits.

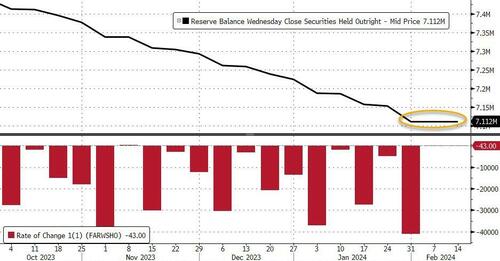

And after the prior week’s miraculous surge in deposits (again, according to The Fed), last week saw total bank deposits (seasonally-adjusted) drop $57BN – the biggest weekly drop since October…

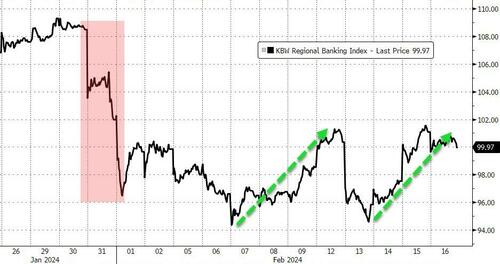

This data is from the week when Regional bank shares shit the bed thanks to NYCB…

Interestingly, on a non-seasonally-adjusted basis, total bank deposits declined about the same as SA -$58BN (and are down $180BN YTD)…

And, excluding foreign banks, domestic deposits dropped $52BN SA (Large Banks -$40BN, Small Banks -$12BN), and tumbled $65BN NSA (Large Banks -$57BN, Small Banks -$$8BN)

As the chart above shows, on an NSA basis, domestic banks have only seen one week of inflows in 2024.

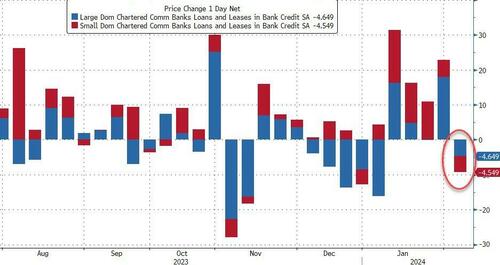

As one might expect, loan volumes shrank during that week by just over $9BN (Large banks -$4.6BN, Small banks -$4.4BN)…

And finally, as a reminder – despite the rebound off the lows again this week in regional bank shares, which must mean everything is awesome, right? – the regional bank crisis is still very much alive as evidenced by the red line below (without The Fed’s imminently expiring BTFP facility)…

…what else are big banks (green line) going to do with all that cash burning a hole in their pockets?

The bottom line is – this looks a lot like a ‘Small Bank’ crisis. The last time this happened, the crisis sparked a sudden $300BN ‘run’ in small bank deposits…

Is The Fed ‘hoping’ for a controlled bank-run this time – so as many small bank deposits are drained voluntarily, before they are drained all at once in a panic (and the Reverse Repo facility is empty, unable to provide any cushion)?

It is looking like a recession in mid-2024 as Covid Stimulypto has run its course. Is the US economy so lame that is requires constant Federal government and Federal Reserve manipulation??

Joe Biden (President of the top 1% of Americans) and his likely replacement “Greasy Gavin” Newsom, wrecker of the California economy. Two economy wreckers on the same stage.

Remember when Democrats were the party of the working man and Republicans (like George HW Bush) were called “Country Club Republicans”? Now Biden and Democrats represent the elitist top 1% of wealth and Trump/Republicans (that Biden snidely calls “Maga Republicans”) represent the bottom 99%. Who woulda thunk??

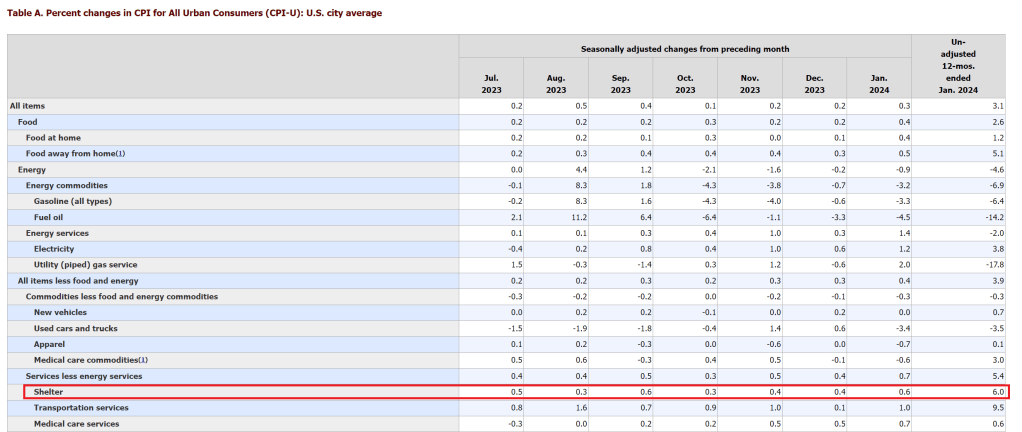

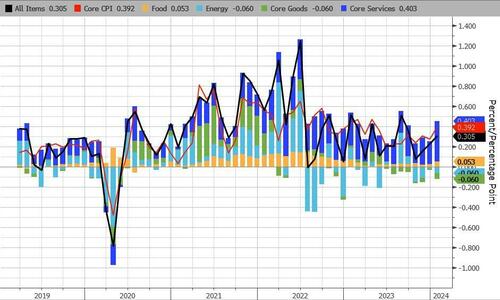

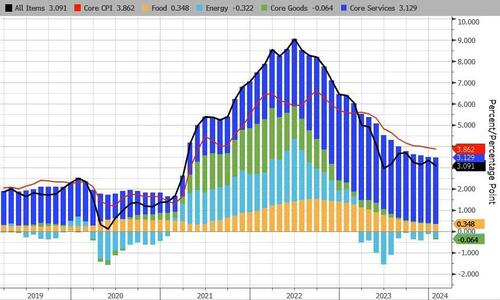

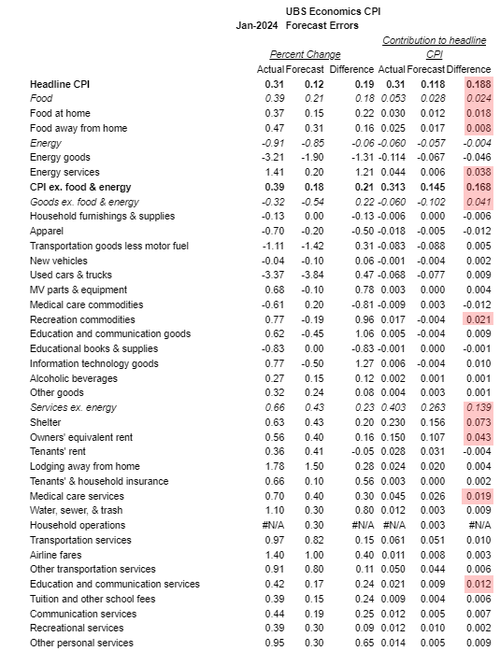

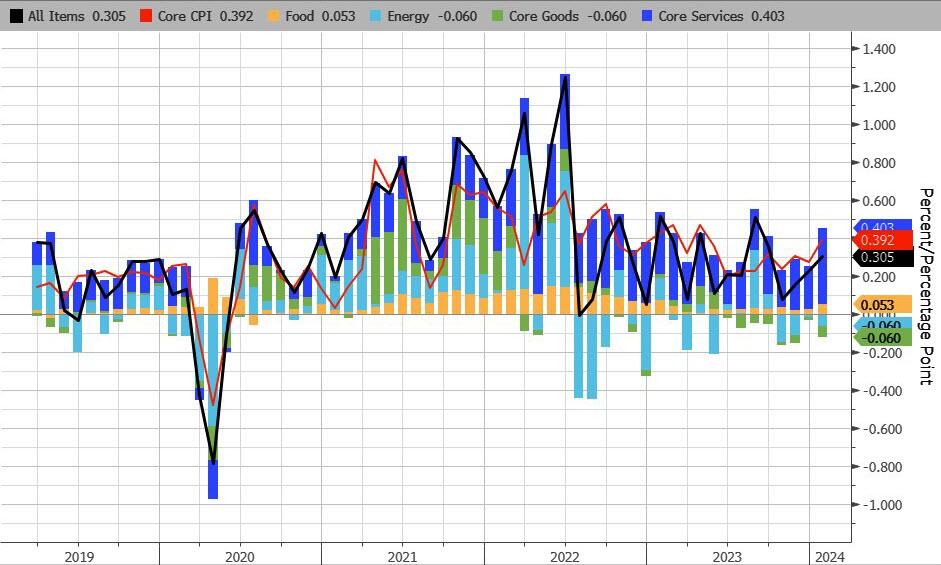

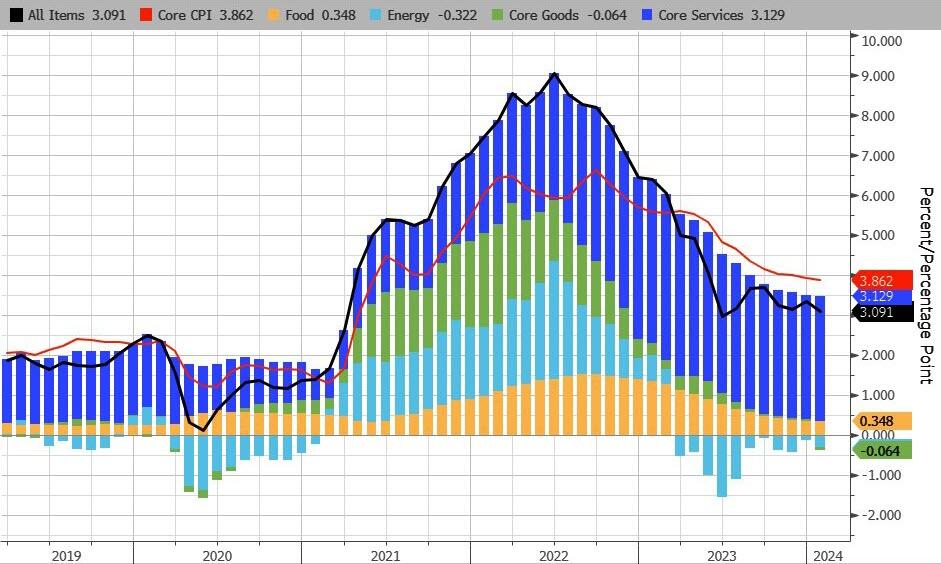

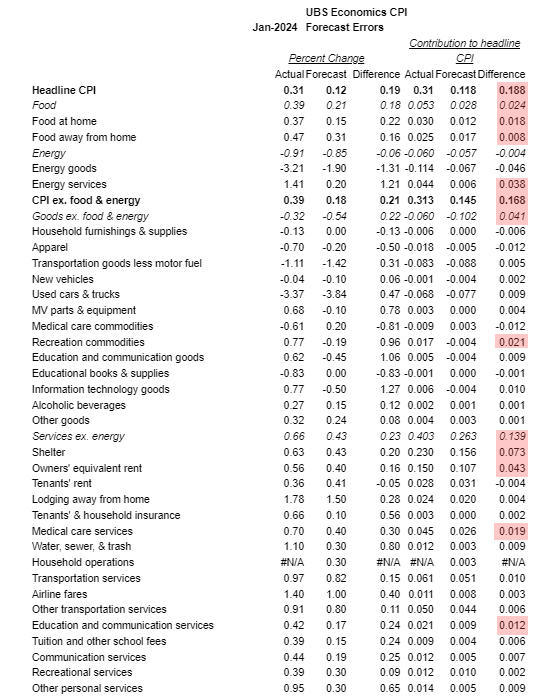

Core CPI fell below 4.00% YoY for the first time since May 2021, but the +3.86% YoY print was hitter than the 3.7% exp (with prices rising 0.4% MoM – the biggest jump since April 2023)…

Source: Bloomberg

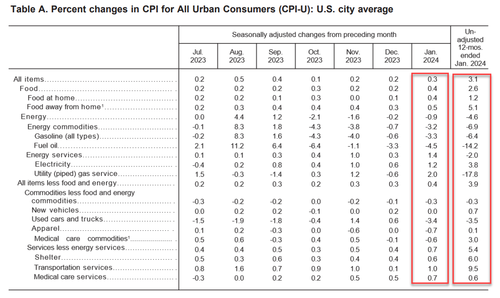

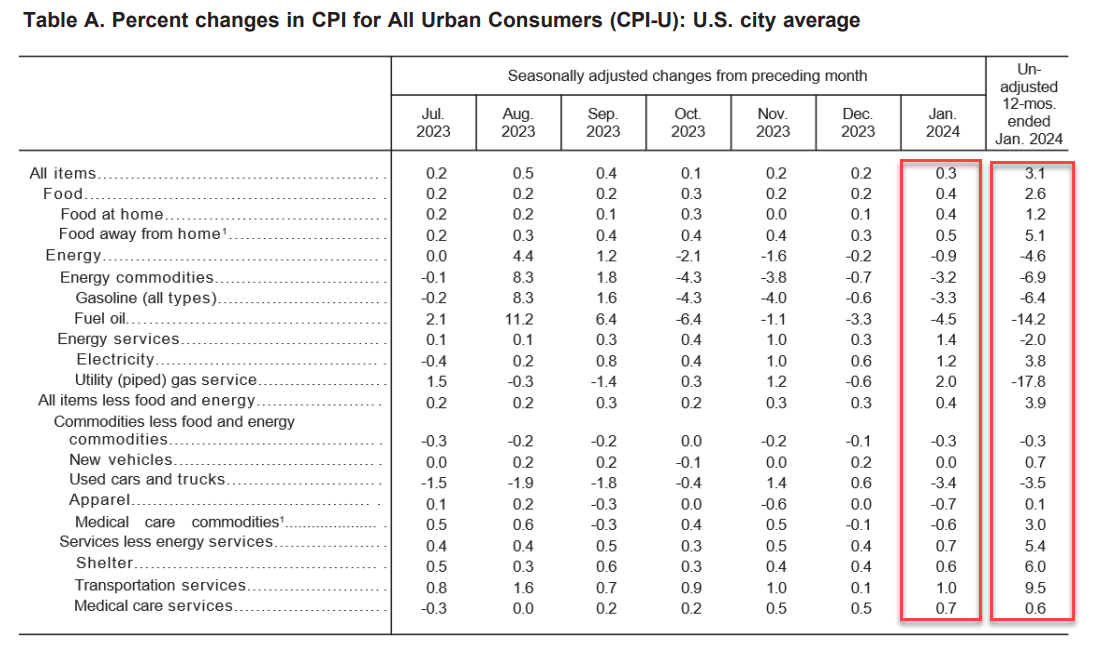

CPI Core: The index for all items less food and energy rose 0.4 percent in January.

The shelter index increased 0.6 percent in January, and was the largest factor in the monthly increase in the index for all items less food and energy.

The index for owners’ equivalent rent rose 0.6 percent over the month, while the index for rent increased 0.4 percent.

The lodging away from home index increased 1.8 percent in January. The motor vehicle insurance index increased 1.4 percent in January, and the recreation index rose 0.5 percent in January.

Among other indexes that rose in January were communication, personal care, airline fares, and education.

The medical care index rose 0.5 percent in January.

The index for hospital services increased 1.6 percent over the month and the index for physicians’ services increased 0.6 percent.

The prescription drugs index fell 0.8 percent in January.

The index for used cars and trucks fell 3.4 percent in January.

The index for new vehicles was unchanged in January.

The apparel index also decreased, falling 0.7 percent over the month.

Core Service inflation picked up MoM…

..and accelerated YoY

Source: Bloomberg

Under the hood, food and Energy services costs jumped MoM along with transportation services…

Here’s the biggest component upside surprises…

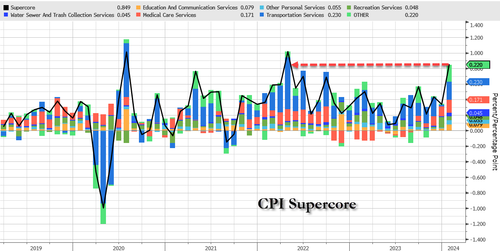

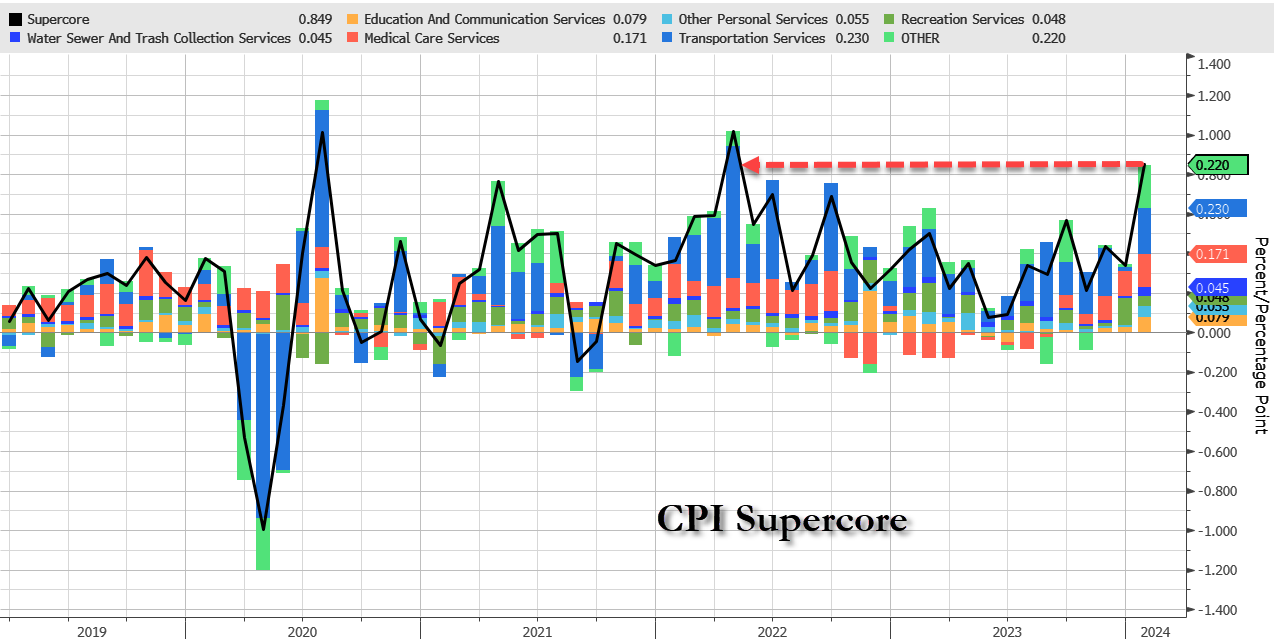

And one step deeper – the so-called SuperCore: Core CPI Services Ex-Shelter index – soared 0.7% MoM (the biggest jump since Sept 2022…

… driving the YoY change up to +4.4% – the hottest since May 2023….

Source: Bloomberg

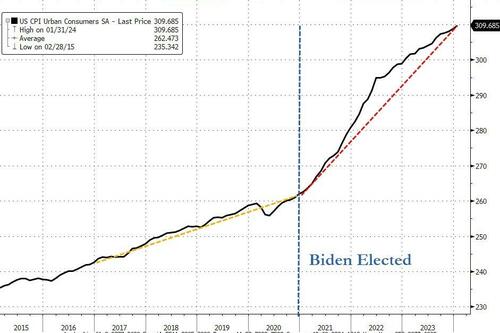

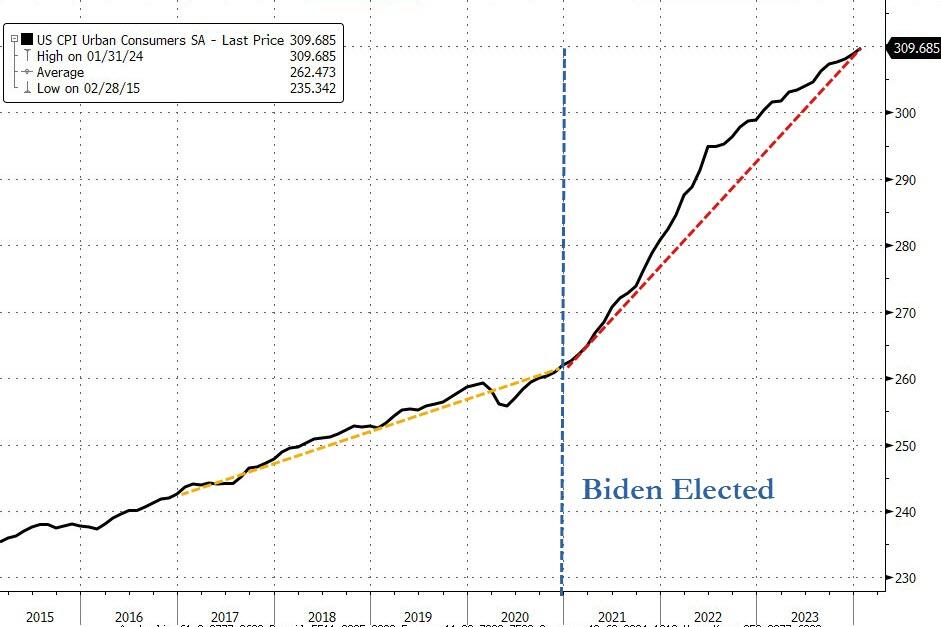

Finally, as a reminder, lower inflation does not mean lower prices.

Source: Bloomberg

The actual index of consumer prices hit a new record high this month – and is up over 18% since President Biden’s term began(it was up 8% over President Trump’s full four year term).

And it gets worse…

Source: Bloomberg

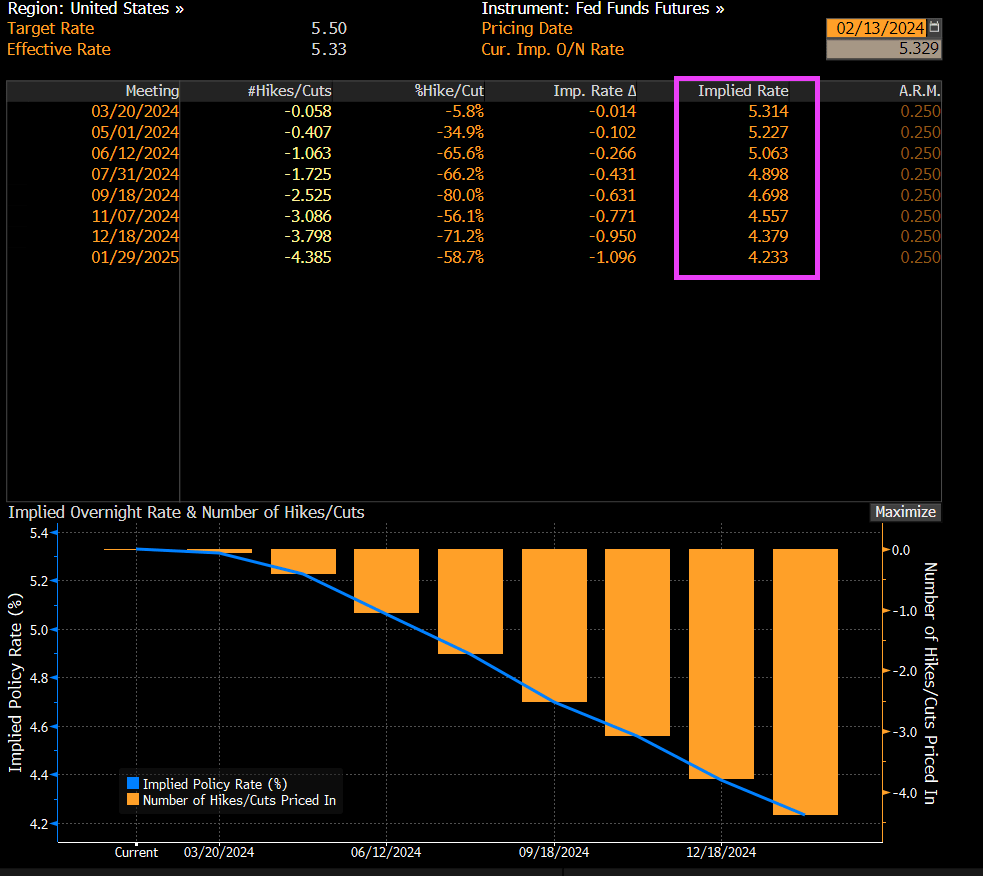

And on the higher than expected inflation report, we are still seeing bets on Fed Funds rate falling from 5.50% to 4.233% over the coming year.

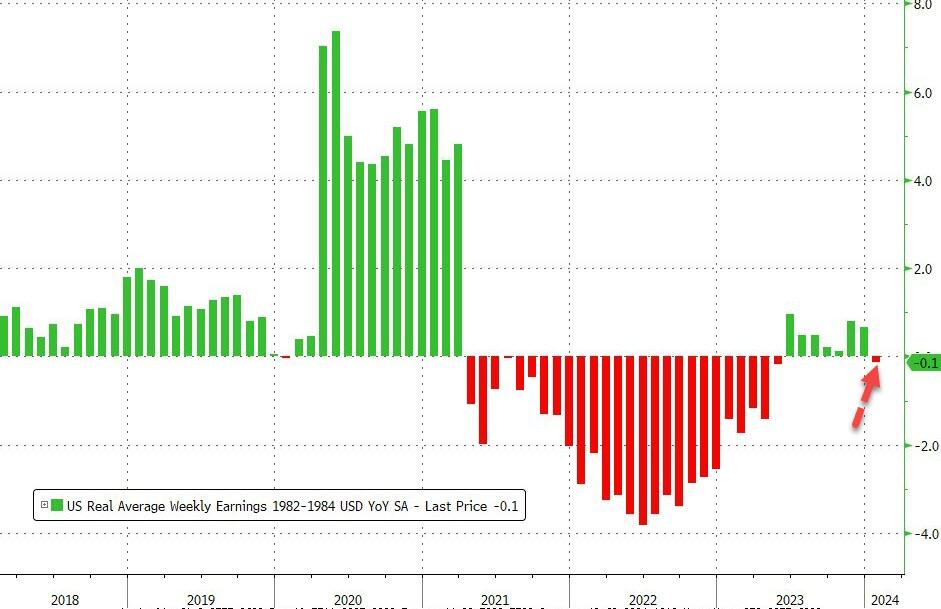

The re-accleration of inflation means wage growth is back in the red relative to prices.

Remember the Chicago Bears’ “Super Bowl Shuffle”? Well, Joe Biden is thedemented (according to Hur) shuffler so a Super Bowl shuffle video featuring Biden talking about how he is reducing prices.

A week out from kickoff, rooms at five-star hotels like the Bellagio, Aria, and The Venetian started at $1,500 or more per night for Super Bowl weekend, according to Expedia. Travelers seeking an affordable stay on the Las Vegas Strip, such as at Excalibur, can find an average nightly rate of $88 on Priceline for this weekend. That jumps to $486 during Super Bowl weekend, an increase of 426 percent. Prices do dip a bit if Super Bowl fans want to stay away from the Strip’s hotels and casinos. Downtown and hotels away from the main drag do offer some cheaper options, with some hotels charging around $200 per night on Fremont Street. Circa, which contains one of the most popular sportsbooks in Las Vegas, is an exception. Rooms this weekend are going for $179 per night on Priceline. That shoots up to $1,232 per night, with only a few rooms remaining at that price, for Super Bowl weekend.

And then, of course, there are the costs of getting there and subsisting. Intrepid drivers looking to travel from San Francisco to Los Angeles (a trip of between 8 and 9 hours) will do so with gasoline prices at $3.66/gallon. That’s down markedly from the mid-2022 spike, but still vastly above levels before the pandemic. Like hotel and ticket prices, airfare into and out of Las Vegas around the big game has alsovaulted in price, although a number of carriers have increased capacity to meet surging demand.

Celebrating at Home Of course, the vast majority of Super Bowl LVIII viewers will not be in Allegiant Stadium, which holds 65,000 spectators. The remainder of viewers, averaging north of 100 million people, will be watching at home or in their hometown sports bars and restaurants. But the persistent inflation of the past three years extended the financial burden into that seemingly more affordable alternative: hosting or attending Super Bowl parties at home. What was once a casual affair of chips, dips, and budget-friendly beverages has transformed into a costly endeavor, as the price of groceries, alcoholic beverages, and even party supplies have surged, affecting the way fans plan to experience one of America’s most iconic sporting events.

The top Super Bowl snacks and dishes include chicken wings, guacamole, potato skins, and deviled eggs, so a look at the recent price trends in chicken, beef, pork, avocados, eggs, beans, potatoes, eggs and condiments is relevant. Pizza, alcoholic beverages, and soft drinks are other popular choices prices have been creeping up.

Below are the prices of a handful of foodstuffs and ingredients which feature prominently in Super Bowl festivities, as well as the price changes from the pre-pandemic period to the most recent data (December 2019 to December 2023). The prices are provided by the US Bureau of Labor Statistics Average Prices by Product series, not seasonally adjusted:

Dec-19 to

Dec 2019

Dec 2023

Dec-23

Grade A Large Eggs

$1.54

$2.51

63.30%

White Sugar All Sizes

$0.59

$0.96

62.30%

Price Frozen Concentrate OJ

$2.34

$3.72

59.10%

Coffee

$4.05

$6.09

50.30%

White Bread

$1.36

$2.02

48.50%

All Ham Ex Canned and Slices

$3.04

$4.40

45.00%

Chocolate Chip Cookies

$3.58

$5.12

42.80%

Grapefruits

$1.25

$1.78

41.90%

Potato Chips

$4.53

$6.41

41.40%

Long Grain White Rice

$0.71

$0.99

38.70%

All Uncooked Beef Steaks

$7.71

$10.65

38.10%

Sirloin Steak Boneless

$8.48

$11.69

37.80%

All Other Uncooked Beef ExVeal

$5.05

$6.91

36.70%

Round Roast Choice Boneless

$5.07

$6.89

35.80%

Boneless Ham Excluding Canned

$4.07

$5.50

35.10%

Ground Beef 100% Beef

$3.86

$5.21

34.90%

Fresh Whole Chicken

$1.45

$1.96

34.80%

Whole Wheat Bread

$1.96

$2.65

34.80%

Round Steak Boneless

$5.98

$7.99

33.70%

All Uncooked Beef Roasts

$5.54

$7.35

32.70%

All Other Pork Ex Can/Sliced

$2.76

$3.64

31.80%

Boneless Chicken Breast

$3.11

$4.08

31.10%

Chuck Roast Choice Boneless

$5.65

$7.38

30.70%

All Uncooked Ground Beef

$4.30

$5.57

29.40%

Ice Cream

$4.74

$6.02

26.90%

Processed American Cheese

$3.91

$4.96

26.80%

Ground Chuck

$4.07

$5.12

25.90%

Fresh Fortified Whole Milk

$3.19

$4.01

25.70%

All Pork Chops

$3.39

$4.26

25.50%

All Purpose White Flour

$0.43

$0.54

25.40%

Sliced Bacon

$5.47

$6.77

23.70%

Chicken Legs Bone In

$1.51

$1.86

23.30%

Romaine Lettuce

$2.18

$2.68

23.30%

White Potatoes

$0.78

$0.96

23.20%

Malt Beverages

$1.42

$1.75

23.00%

Boneless Beef for Stew

$5.75

$7.03

22.20%

Lean Ground Beef

$5.52

$6.67

20.90%

Navel Orange

$1.33

$1.60

20.60%

Boneless Chops

$3.81

$4.56

19.80%

Iceberg Lettuce

$1.30

$1.53

17.30%

Spaghetti and Macaroni

$1.19

$1.38

15.80%

Dry Pint Fresh Strawberries

$3.10

$3.57

15.40%

Center Cut Bone In Chops

$3.77

$4.33

14.70%

Dried Beans

$1.40

$1.59

13.60%

Red and White Table Wine

$12.04

$13.32

10.60%

Bananas

$0.57

$0.63

9.10%

Natural Cheddar Cheese

$5.30

$5.55

4.60%

Lemon

$2.00

$2.07

3.60%

Field Grown Tomatoes

$1.95

$2.00

2.10%

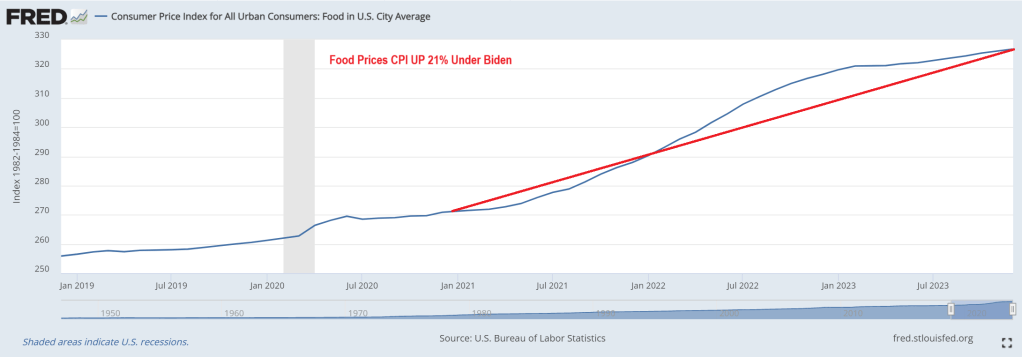

And although disinflation has proceeded, by their nature the various indices (Consumer Price Index, Personal Consumption Expenditure Price Index) obscure individual price changes. For example: the US CPI Urban Consumers Food-at-Home index, in December 2023, showed a year-over-year change of 1.31 percent (from 299.089 to 303.005). Below are the actual December 2022 to December 2023 changes in individual food items which are prominent in Super Bowl celebrations.

Dec-22 to

Dec 2022

Dec 2023

Dec-23

Price Frozen Concentrate OJ

$2.72

$3.72

36.80%

Sirloin Steak Boneless

$10.17

$11.69

15.00%

White Sugar All Sizes

$0.84

$0.96

13.30%

Round Steak Boneless

$7.06

$7.99

13.20%

All Uncooked Beef Steaks

$9.46

$10.65

12.50%

Round Roast Choice Boneless

$6.22

$6.89

10.70%

Whole Wheat Bread

$2.42

$2.65

9.40%

All Uncooked Beef Roasts

$6.72

$7.35

9.30%

All Ham Ex Canned and Slices

$4.05

$4.40

8.70%

Ground Beef 100% Beef

$4.80

$5.21

8.50%

Ice Cream

$5.56

$6.02

8.20%

White Bread

$1.87

$2.02

8.10%

Navel Orange

$1.49

$1.60

7.80%

Chuck Roast Choice Boneless

$6.86

$7.38

7.60%

Ground Chuck

$4.76

$5.12

7.60%

All Uncooked Ground Beef

$5.19

$5.57

7.30%

Fresh Whole Chicken

$1.83

$1.96

6.80%

Processed American Cheese

$4.66

$4.96

6.30%

All Other Uncooked Beef ExVeal

$6.59

$6.91

4.80%

Lean Ground Beef

$6.39

$6.67

4.50%

All Purpose White Flour

$0.52

$0.54

3.10%

Chocolate Chip Cookies

$4.97

$5.12

2.90%

Boneless Ham Excluding Canned

$5.37

$5.50

2.40%

Boneless Beef for Stew

$6.87

$7.03

2.20%

Potato Chips

$6.28

$6.41

2.00%

Long Grain White Rice

$0.97

$0.99

2.00%

White Potatoes

$0.95

$0.96

1.40%

Malt Beverages

$1.74

$1.75

0.70%

Boneless Chops

$4.56

$4.56

0.00%

All Other Pork Ex Can/Sliced

$3.64

$3.64

0.00%

Bananas

$0.63

$0.63

-0.50%

Lemon

$2.09

$2.07

-0.90%

All Pork Chops

$4.31

$4.26

-1.30%

Red and White Table Wine

$13.66

$13.32

-2.50%

Sliced Bacon

$6.96

$6.77

-2.60%

Spaghetti and Macaroni

$1.43

$1.38

-4.00%

Chicken Legs Bone In

$1.95

$1.86

-4.60%

Fresh Fortified Whole Milk

$4.21

$4.01

-4.80%

Coffee

$6.47

$6.09

-5.80%

Boneless Chicken Breast

$4.35

$4.08

-6.10%

Dried Beans

$1.70

$1.59

-6.40%

Dry Pint Fresh Strawberries

$3.86

$3.57

-7.30%

Center Cut Bone In Chops

$4.67

$4.33

-7.40%

Natural Cheddar Cheese

$6.00

$5.55

-7.50%

Field Grown Tomatoes

$2.23

$2.00

-10.50%

Romaine Lettuce

$3.57

$2.68

-24.80%

Grade A Large Eggs

$4.25

$2.51

-41.00%

Avocado prices, according to the Mexico Products CPI, have risen 27.2 percent from December 2019 (83.80) to December 2023 (106.554). From December 2022 (95.922) to December 2023, they rose 11.1 percent.

Determining the average price of a delivery pizza is more difficult. In local contexts, the price of a slice of pizza can act as an inflationary benchmark of sorts, but estimates indicate that from February 2023 to February 2024 the price of an average delivery pizza has increased from $17.81 to $18.33, or 2.9 percent.

Comparing these numbers with the year-over-year headline and core CPI numbers (3.4 percent and 3.9 percent, respectively), two significant insights emerge. The individual price changes above, over a four- and one-year period, frequently underscore how price indices obscure trends in prices which, at specific times can be considerably graver than the headline figures suggest. Second, that one needn’t be anywhere near Las Vegas to feel the damage of expansionary monetary policies acutely. Well over a year after the lies about Vladimir Putin, gas station owners, ocean shippers, and corporate profits have been told and forgotten, and despite the cynical political impudence of calling a massive green spending bill an “Inflation Reduction Act,” spending Super Bowl Sunday at home in 2024 will be much more expensive than it was in 2023, and vastly more than it was four short years ago.

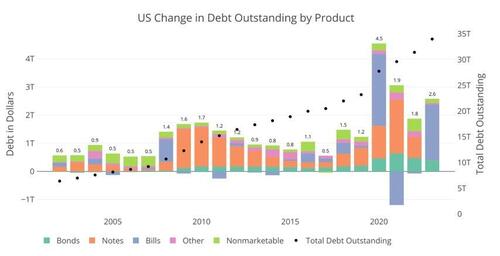

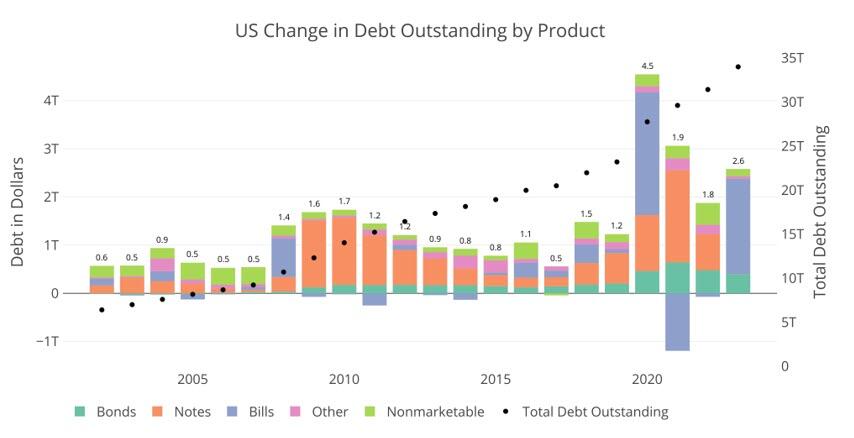

The only other times Bills were used as a primary funding source was in 2008 during the Great Financial Crisis and 2020 during Covid. Neither year came close to 77% of total new debt issuance. These were also emergency times, and specifically in 2021, almost half the short-term debt was retired in favor of Notes and Bonds to undo the 2020 Bill issuance.

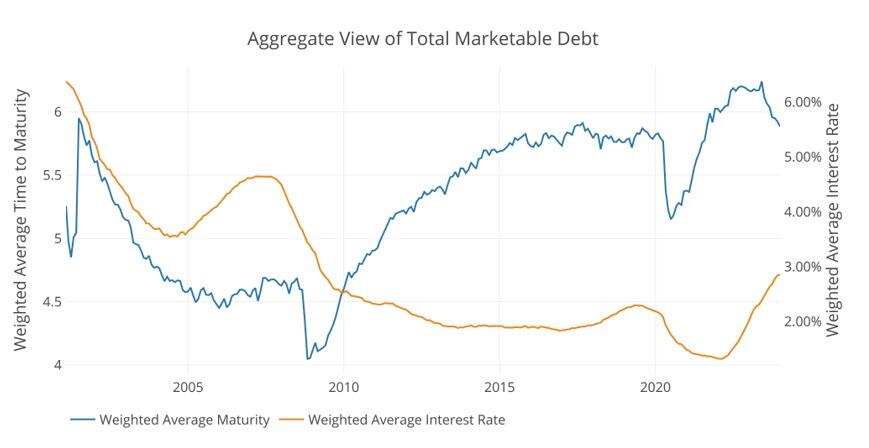

The Treasury has spent nearly two decades trying to extend the maturity of the debt. This can be seen in the blue line below that shows the average debt maturity. When the short term debt is issued in such a way, it drives down the average maturity, which causes the Treasury to have to roll-over more debt in shorter time periods. So why has the Treasury all of a sudden gone entirely to short-term debt in non-emergency times? The answer lies in the orange line, so let’s dig in.

Figure: 2 Weighted Averages

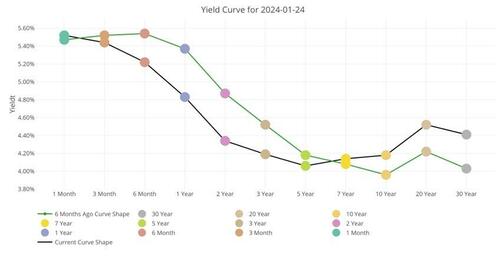

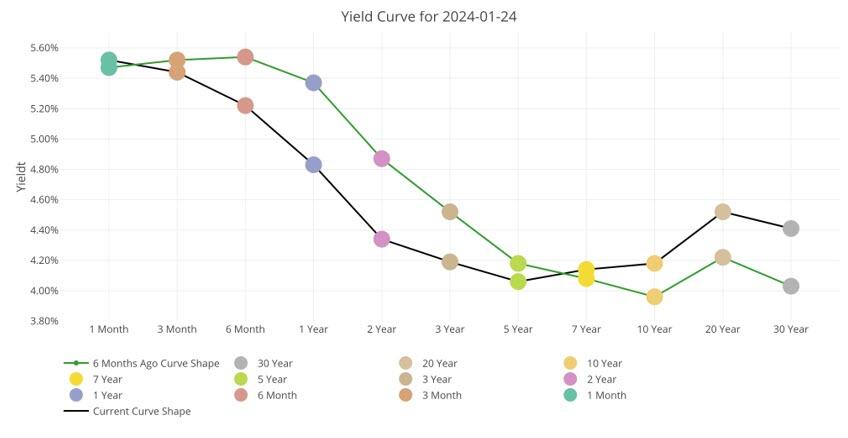

First, it is important to understand the interest rates the Treasury is facing. The chart below shows the current yield curve as it stands today and 6 months ago. As you can see, short-term rates are a full 1%-1.5% higher than medium-term. What?!? Didn’t we just see that the Treasury has specifically targeted short-term debt?

Why are they paying more than they have to? Had the Treasury financed the $2T with Notes, they would have saved $30B in interest this year alone!

Figure: 3 Tracking Yield Curve Inversion

So, why have they done this? Well, there are two potential possibilities.

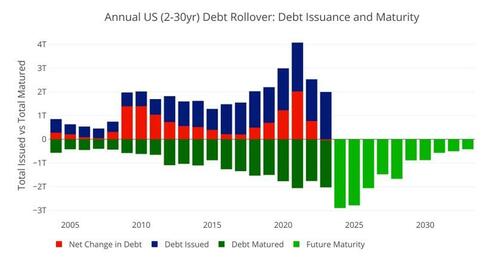

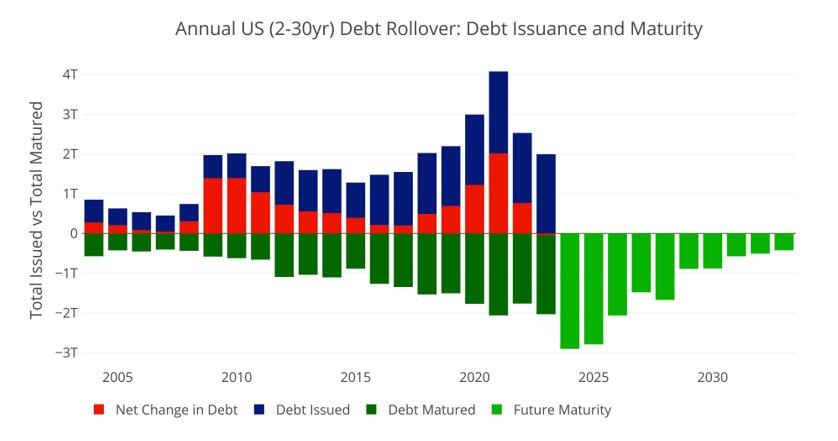

First, they may be nervous about the market’s ability to handle so much medium-term debt. The market typically digests short-term debt very easily, but it can become saturated with medium-term debt. The chart below shows the amount of medium-term debt that rolled over last year. This is not new issuance; this is debt maturing that needs to be rolled over.

As shown, nearly $2T rolled over last year. This means, had the Treasury issued Notes instead of Bills, the Market would have had to absorb a whopping $4T in new medium-term debt like they did in 2020. The difference this year is that back in 2020 the Fed bought nearly all of that debt, putting a floor under the market.

Compounding this problem further is that this year is set to be a record year in terms of debt rollover. Nearly $2.9T in Notes need to be rolled over.

Figure: 4 Treasury Rollover

Still, even with that massive amount of debt issuance, there must be more to the story. Why would Yellen specifically pay $30B more in interest just because she is concerned the about the volume of debt issuance. As Figure 1 above shows, this has never been a concern in the past except in emergency situations. Furthermore, why not issue at least some new debt as medium-term.

This lends to a second, and more probable conclusion. Long-term rates are set to fall in the very near term. The Treasury did not want to lock in for 2-7 years at 4% if it knows rates will fall. It will pay a premium ($30B this year), if it means it can lock in lower rates for longer and save the money on the back end.

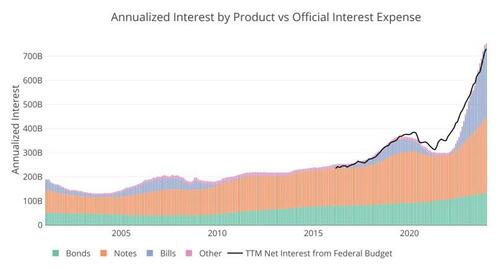

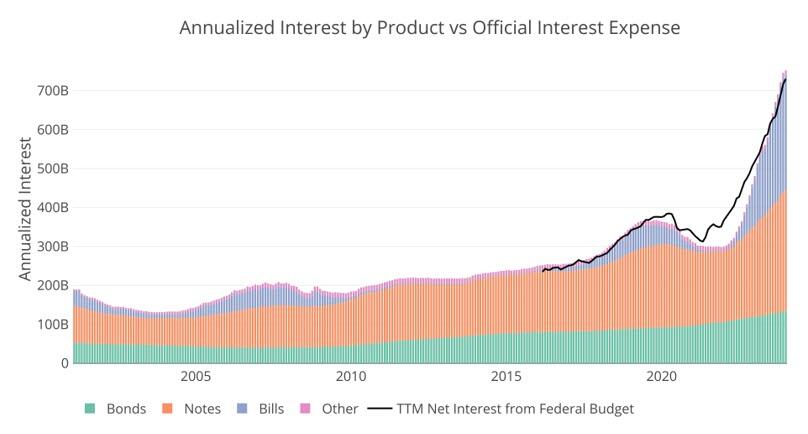

So, why are long-term rates, going to fall? Because they have to… the chart below shows the current interest owed on the national debt annualized. It’s not a pretty picture, and you can see how the interest from Bills has absolutely ballooned.

Figure: 5 Net Interest Expense

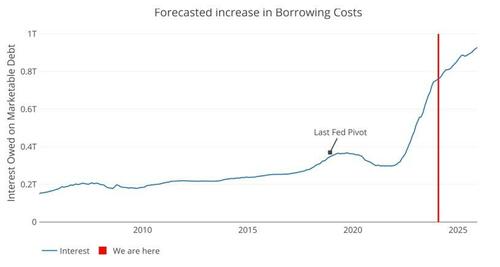

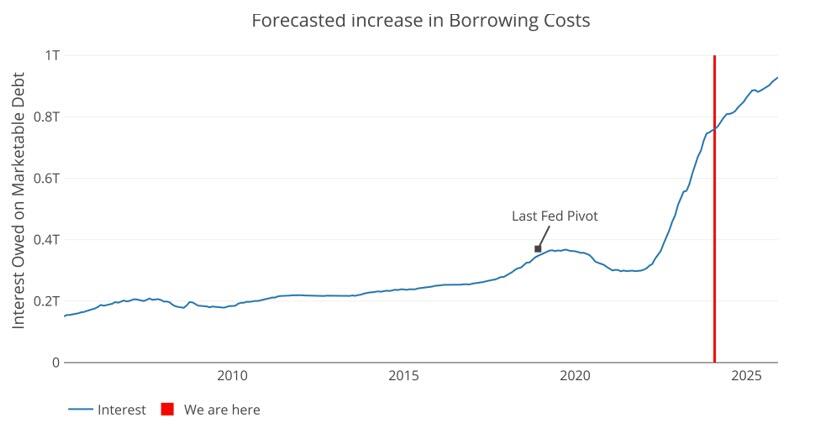

The Fed has come out with their dot plot that shows a calm glide path down. Well, we can take the debt maturity and push it forward at the projected rate of the Fed. Even given the current proposed 6 rate cuts, and getting back to 3.5% by early 2025, the trajectory for interest expense is not looking good.

Given current projections by the Fed, the Treasury will owe over $900B on interest by 2025. That is a debt death spiral. The Fed had to pivot back in 2018 when interest expense neared $400B. Next year, the cost will be more than double that!

Figure: 6 Projected Net Interest Expense

There is a potential third option. It’s an election year. Maybe Yellen is doing everything and anything to keep the financial system running smoothly. She has decided that the Treasury market must remain 100% stable and wants to take no chances. Thus, she issues tons of short-term debt, costing the tax payer an extra $30B this year and decides it’s a problem to be fixed at a later date.

While this would be wildly irresponsible and corrupt, the real argument against possibility 3 is the same as possibility 1, the market should be able to ingest at least some medium-term debt. This means the only logical conclusion is that she knows rates are coming down hard and fast. How does she know? Well, she used to be the head of the Fed.

There is no doubt, everyone in Washington can do the simple math above and recognize the Fed cannot take a glide path down. The only option is for rates to come down. Yellen just bet $2T on that outcome.

Joe, are you kidding about the sizzling economy? Karine Jean Pierre is also guilty of comedy or gross propaganda.

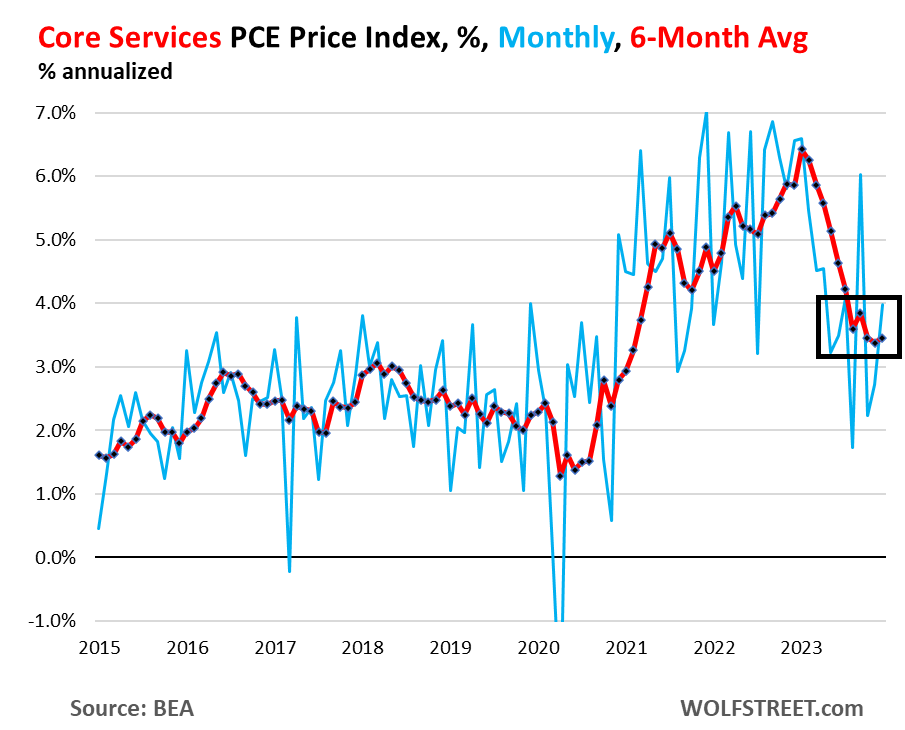

So right up front – and the Fed has been talking about this, though no one listens: The “core services” PCE price index has gotten stuck at 3.5% over the past six months annualized, and accelerated to 4.0% month-to-month annualized in December, with housing inflation stuck at about 6.7% over the past six months annualized, and with other core services components still red-hot.

The core services PCE price index rose by 0.33% in December from November, the second acceleration in a row, according to data from the Bureau of Economic Analysis today. This amounts to an increase of 4.0% annualized (blue).

The six-month moving average, which irons out the huge ups and downs of the month-to-month data, accelerated to 3.5%, and has been in this range since August, after the sharp deceleration in early 2023 (red).

Core services is where consumers spend the majority of their money, and they matter. Which is why Fed governors have said in near unison that they’re in no hurry to cut rates, but have taken a wait-and-see approach, with an eye on core services. And if it goes away, fine.

But on the surface, the PCE price index looks encouraging, and this has been the trend for months, with the overall PCE price index at +2.6% year-over-year in December, the lowest since March 2021; and with the core PCE price index at +2.9% year-over-year, also the lowest since March 2021, and aiming for the Fed’s 2% target.

The factors for the year-over-year cooling in these inflation measures have been the same for months: plunging energy prices, sharply dropping prices of durable goods after the huge spike in 2020 and 2021, cooling food inflation (with prices still rising from very high levels, but slowly), and favorable “base effects” when compared to a year ago.

But energy prices don’t plunge forever, so that will go away; durable goods prices don’t drop sharply forever either, though they can drop for a while longer to unwind some more of the price spike they’d been through in 2020 and 2021; and the base effects are going to get timed out this year, when the base of the year-over-year comparisons become the lower inflation figures of 2023.

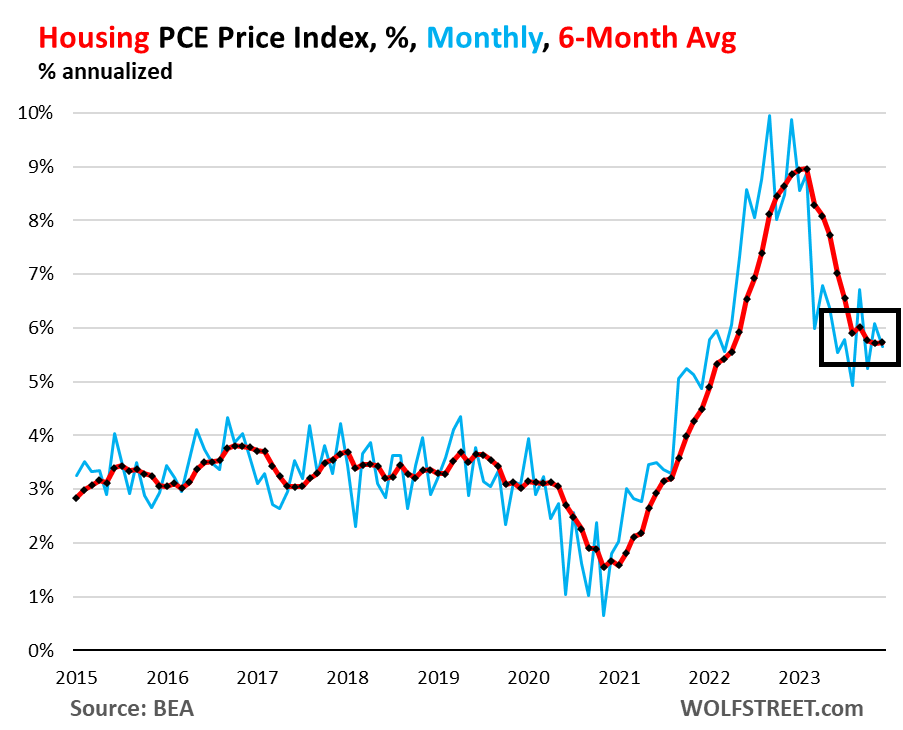

Housing inflation, still red hot and not cooling anymore. The PCE price index for housing rose by 0.46% in December from November and has been in this range since March, after the sharp slowdown early in 2023. This amounts to 5.7% annualized (blue in the chart below).

The housing index is broad-based and includes factors for rent in tenant-occupied dwellings; imputed rent for owner-occupied housing, group housing, and rental value of farm dwellings. It’s the largest component of core services.

The six-month moving average annualized, which shows the more recent trends, also rose by 5.7% in December, and has been in the same range since August (red).

So it looks like the PCE price index for housing has gotten stuck at 5.7%. This stubborn inflation in housing is a blow to theories trotted out for 18 months that housing was lagging, and that we know it will go away as an issue, etc., etc. The increases are less hot than they had been, but remain hot and have become persistent.

The major categories of core services in the PCE price index, as a six-month average of month-to-month changes, annualized:

Core services, major categories, 6-month average, annualized

Housing

5.7%

Description and chart above

Non-energy utilities

2.5%

Water, sewer, trash

Health care

2.5%

Physicians, outpatient, hospital, nursing care, dental, etc.

Transportation services

6.1%

Auto repair & maintenance, auto leasing & rentals, public transportation, airfares, etc.

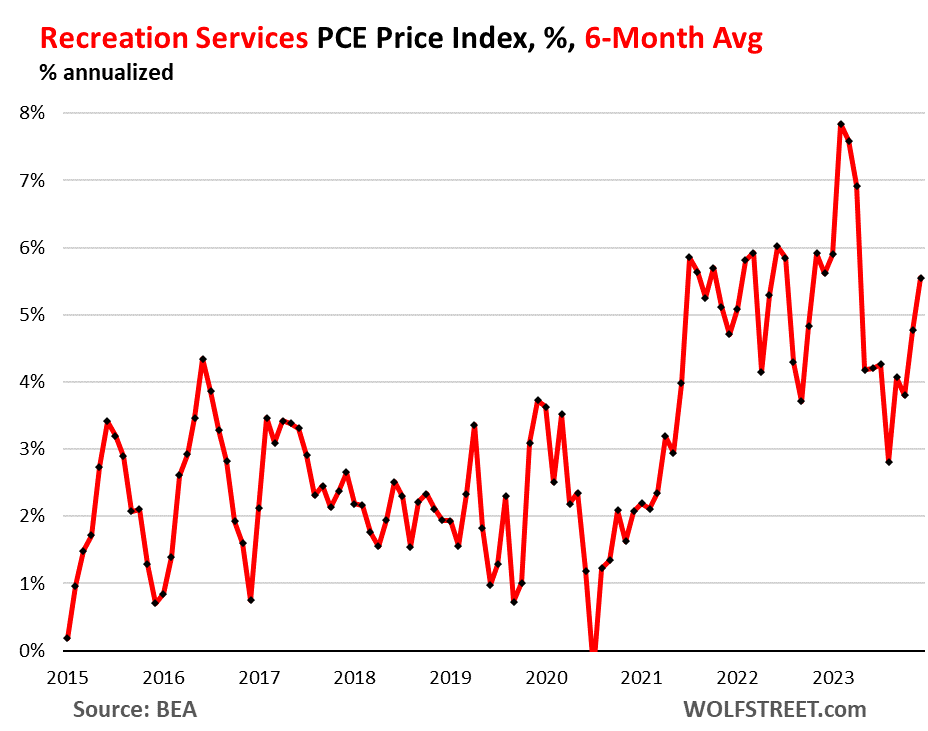

Recreation services

5.6%

Concerts, sports, movies, gambling, streaming, vet services, package tours, etc.

Food services, accommodation

2.8%

Meals & drinks at restaurants, bars, schools, cafeterias, etc.; accommodation at hotels, motels, schools, etc.

Financial services

3.5%

Fees & commissions at banks, brokers, funds, portfolio management, etc.

Insurance

2.8%

Insurance of all kinds, including health insurance

Other services

0.1%

Collection of other services

Inflation in Transportation services and Recreation services is accelerating on the basis of the 6-month moving average, with the PCE price index for Transportation services rising by 6.1%, and the index for Recreation services rising by 5.6%:

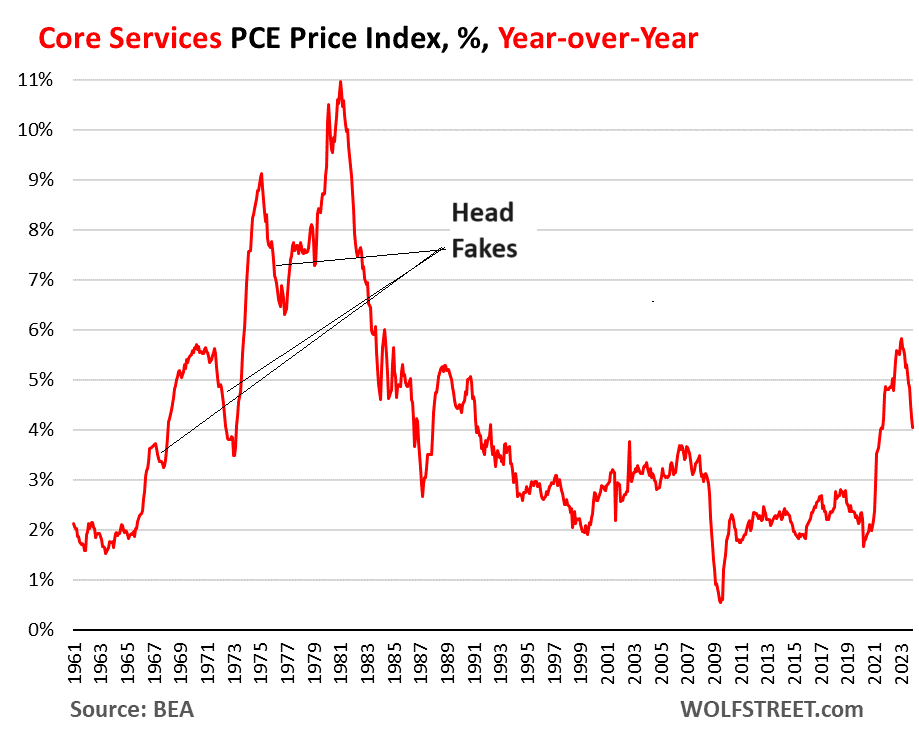

The head-fakes last time.

Inflation in services turns out to be tough to beat, and it can dish up big head-fakes. Last time we had this type of surge of inflation, so that was in the 1970s and 1980s, we thought repeatedly that we had inflation licked, only to find out that we’d fallen for an inflation head-fake. There were three head-fakes in core services on the way to the peak of 11% in 1981:

But Democrats are desperate to stay in power and rake in billons of dollars. Their strategy? Nobody But Joe. Well, except maybe Mike Obama.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.