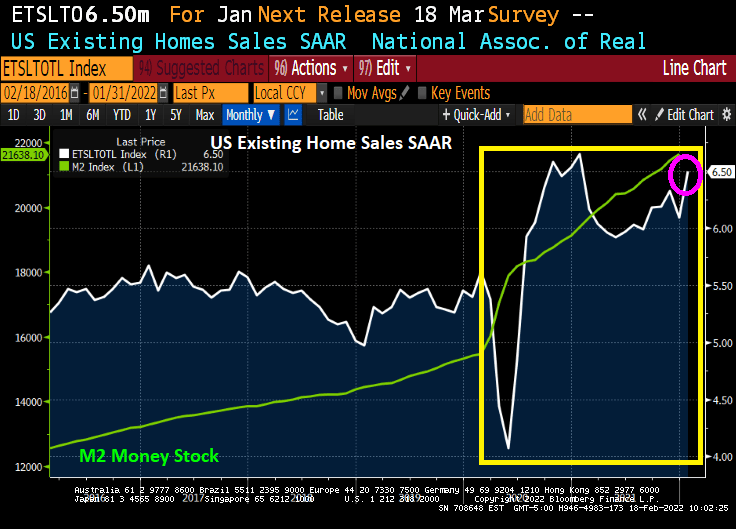

Surprise! US existing home sales in January rose to 6.50 million units SAAR versus the expected 6.10 million units. That is a 6.7% increase over December.

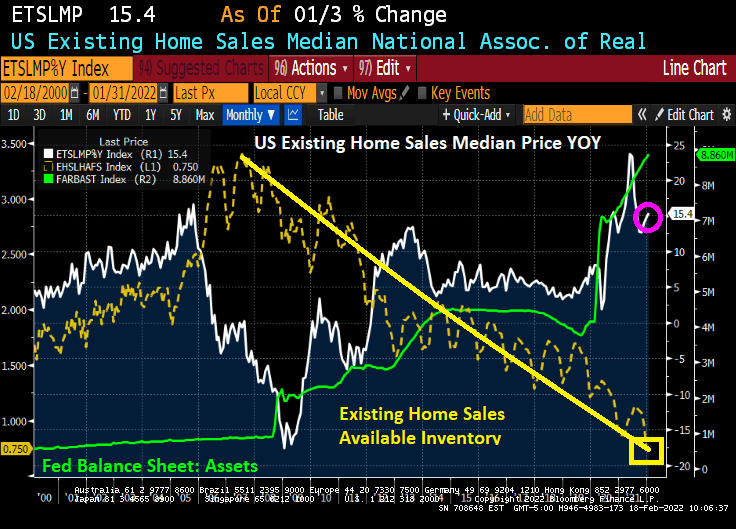

The disturbing news is the continued lack of available inventory that peaked in Q4 2007 and has continued its decline to today … the lowest level of available inventory since 1981. Despite the Fed’s massive stimulus that they allegedly will take away. Median price of existing home sales rose to 15.4% YoY. Making homes affordable should NOT be a slogan for The Federal Reserve, the Biden Administration or Congress.

The massive Federal stimulypto (fiscal and monetary) has helped push existing home sales to 6.50 million units SAAR in January. What will happen after The Fed withdraws it stimulus??

What is surprising is that with declining REAL wage growth, we saw a surge in home buying in January.

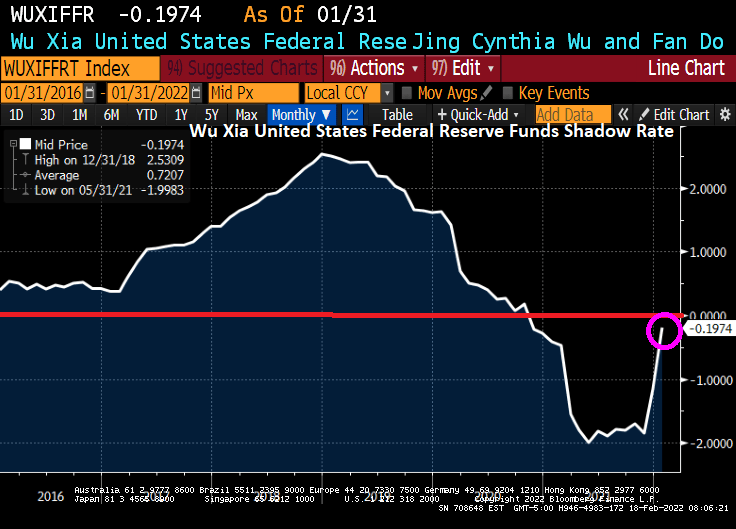

Wu-Xia employs an approximation that makes a nonlinear term structure model extremely tractable for analysis of an economy operating near the zero lower bound for interest rates. It can be used to summarize the macroeconomic effects of unconventional monetary policy (ZIRP + QE). The Shadow Rate is now -0.1974%.

The good news? The Atlanta Fed Wage Growth tracker is showing a 5.1% wage growth. The bad news? Inflation is ruining that growth at a whopping 7.5% rate leaving REAL wage growth at -2.4%.

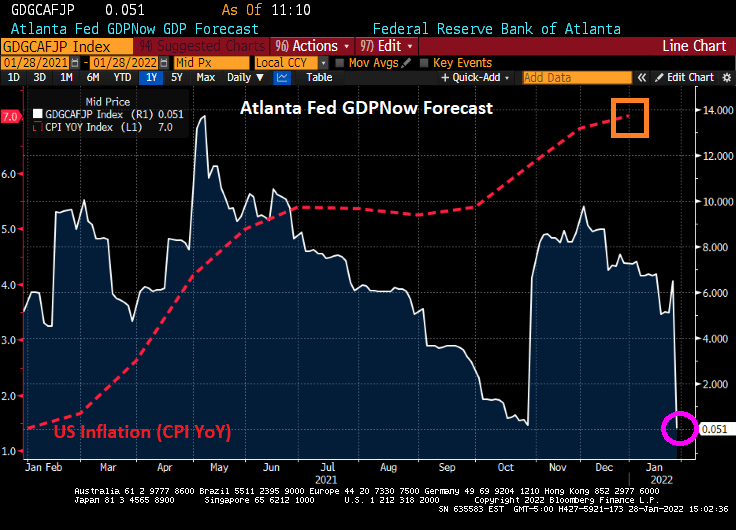

And the Atlanta Fed’s GDPNow Q1 forecast is a measly 1.285%. Apparently, the fiscal and monetary stimulypto has worn out.

And liquidity in the equity market has seemingly vanished.

The Biden Administration and Congress need a distraction from the awful inflation news caused by Biden’s energy policies, sheer wasteful spending and Federal Reserve policy errors (too much monetary stimulus for too long).

Jay “The Revelator” Powell has told us in The Fed minutes that The Fed is ready to raise rates and shrink the balance “soon.” Sort of like saying “Shock and Awe” is coming.

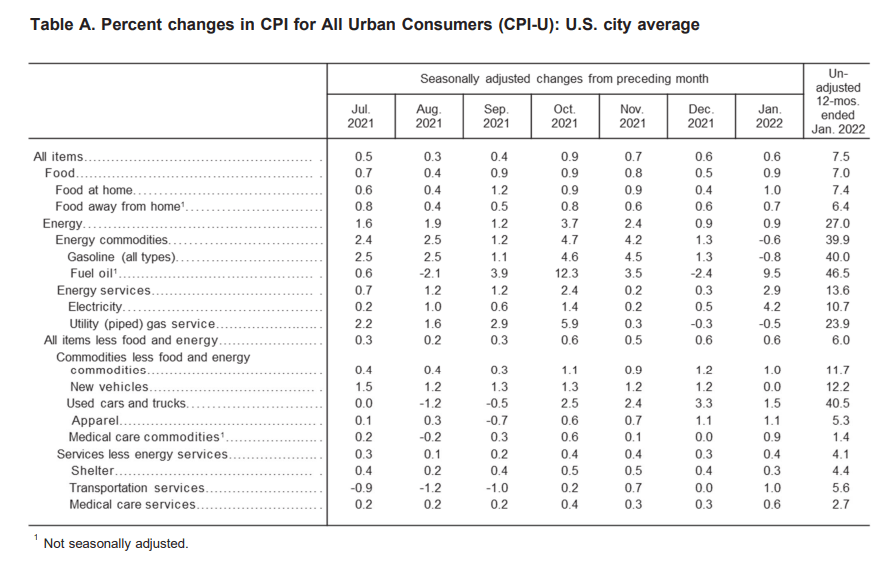

As expected, US inflation surged from 7.0% in December to 7.5% in January.

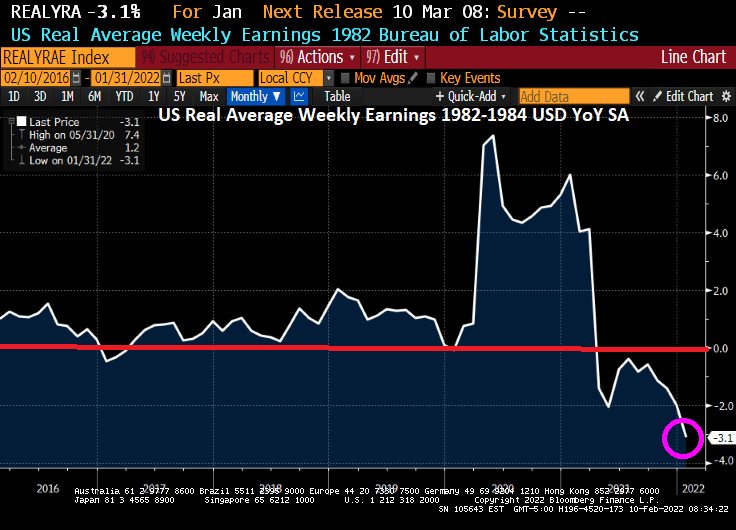

REAL average weekly earnings growth YoY fell to -3.1%.

Energy prices YoY lead the wage (fuel oil UP 46.5% YoY). Used cars and trucks UP 40.5%. At least food is up “only” 7%.

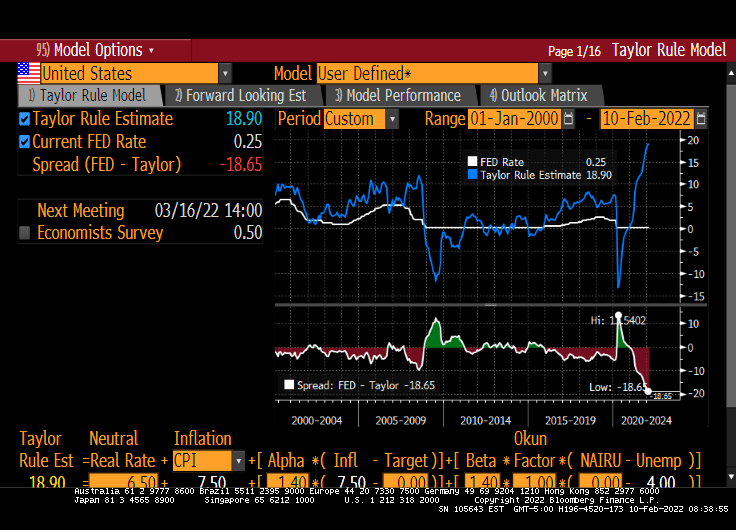

At 7.5% CPI, the Taylor Rule suggests that The Federal Reserve should have their target rate be 18.90%.

At least CORE inflation is “only” 6% YoY.

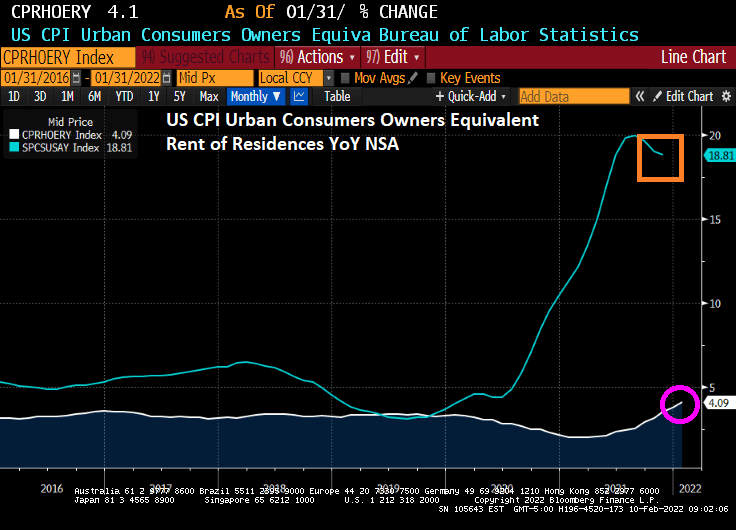

How about rent CPI? The owner’s equivalent rent of residences rose to 4.09% YoY. Seems a little misleading since home prices nationally are growing at 18.81% YoY.

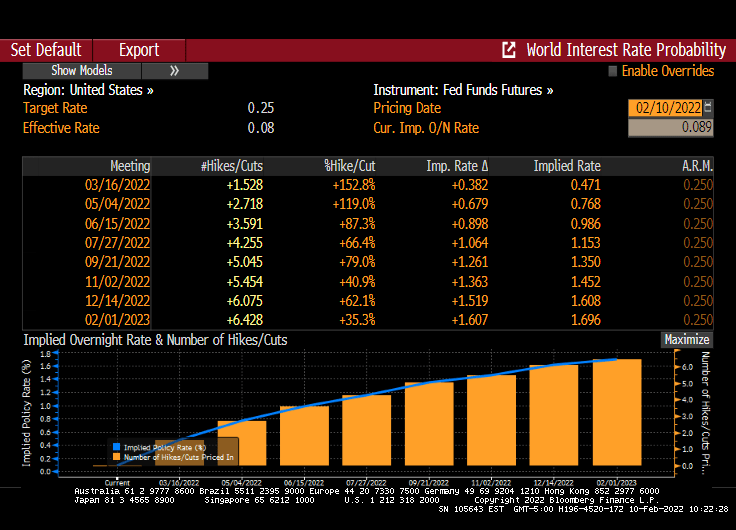

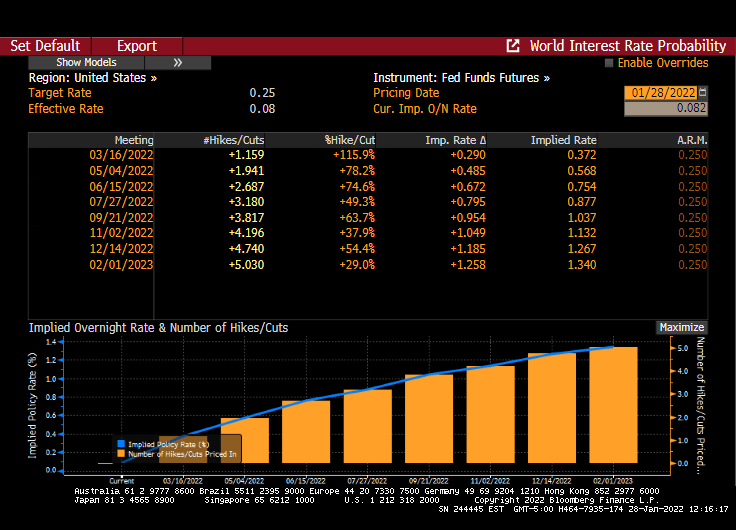

Fed Funds Futures data points to 6-7 rate HIKES over the coming year. BRACE FOR IMPACT!!

Yes, this is Powell’s famous chili recipe if The Fed actually starts to raise rates and pare back the balance sheet stimulus.

Inflation is literally burning a hole though the pockets of Americans. The Flexible Price CPI is raging at 18% YoY. The Dallas Fed has their preferred measure of inflation, the trimmed mean CPI, is growing at only 3.05% YoY. The classic measure of inflation, CPI YoY, is growing at 7.12%.

That is of course if you can find things to buy at the grocery store.

I remember when Fleetwood Mac played at Bill Clinton’s first inauguration party. Perhaps Fleetwood Mac can play at the midterm election party commemorating the rampant inflation under Biden’s “leadership”: Bare Shelves.

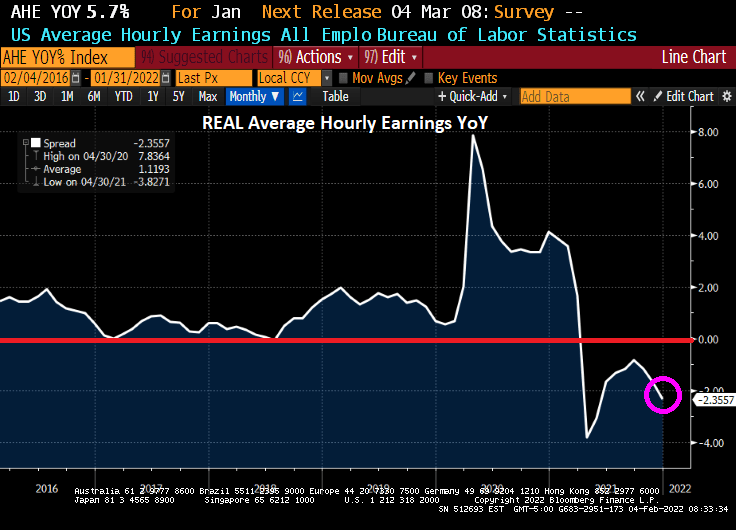

Well, the COVID hysteria from the Biden Administration and the media preparing us for a horrible jobs report was … incorrect. In fact, the January jobs report was “exceptional”. 467,000 jobs were added and average hourly earnings growth ROSE to 5.7% YoY.

The bad news? Thanks to surging inflation, REAL average hourly earnings growth YoY FELL to -2.36%.

Unemployment ROSE to 4.0% from 3.9% as more people dropped out of the labor force in January. On the bright side, labor force participation rate rose to 62.2% from 61.9%.

Leisure and hospitality employment (one of the most vulnerable to inflation) expanded by 151,000 in January, reflecting job gains in food services and drinking places (+108,000) and in the accommodation industry (+23,000).

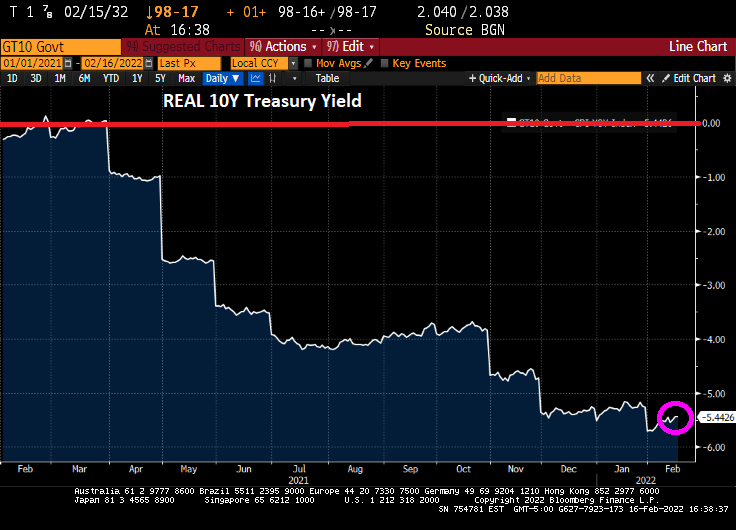

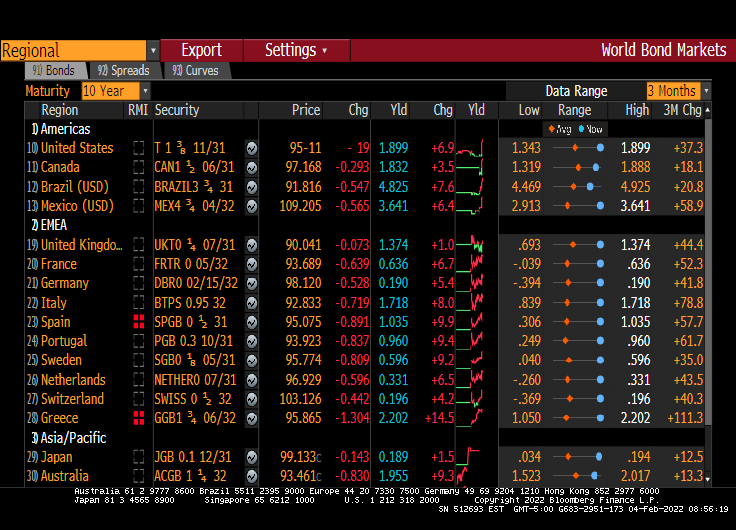

The reaction in the bond market? US 10-year yields are up 6.9 basis points as Eurozone is up across the board.

Energy prices are up (except natural gas futures).

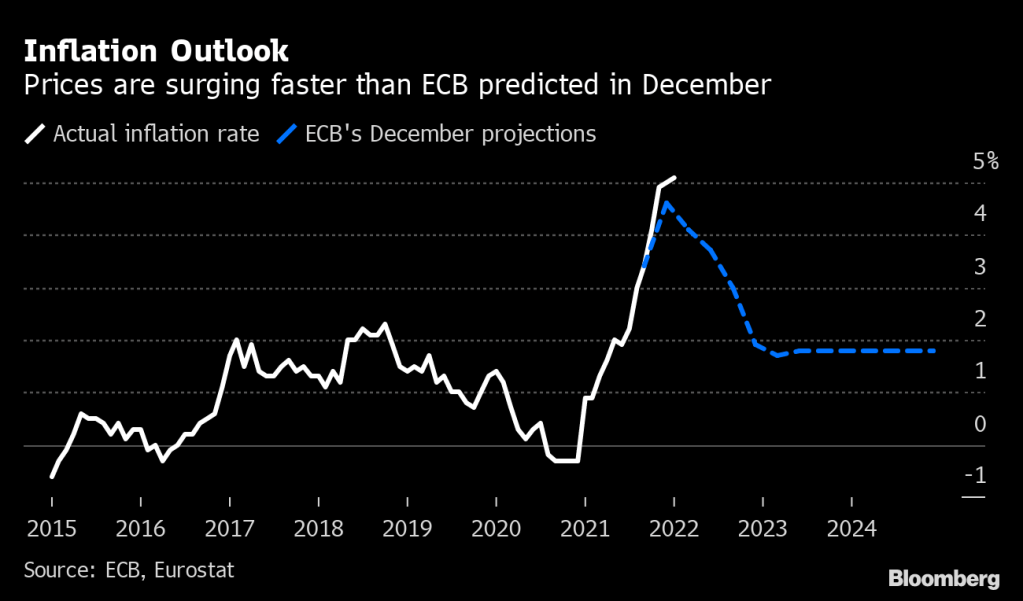

(Bloomberg) — European Central Bank President Christine Lagarde is no longer ruling out an interest-rate hike this year, a pivot toward the tightening stance of global peers that officials privately see materializing with a shift in policy guidance as soon as next month.

Investors brought forward bets on ECB action as the monetary chief delivered surprisingly hawkish comments citing unexpected record inflation data, contrasting with an earlier statement on Thursday that kept intact its formal view that price increases will ease.

She spoke after policy makers agreed that it’s sensible no longer to exclude a rate move in 2022, and that bond buying could end in the third quarter, according to officials familiar with their thinking who asked not to be identified because such discussions are confidential. An ECB spokesman declined to comment.

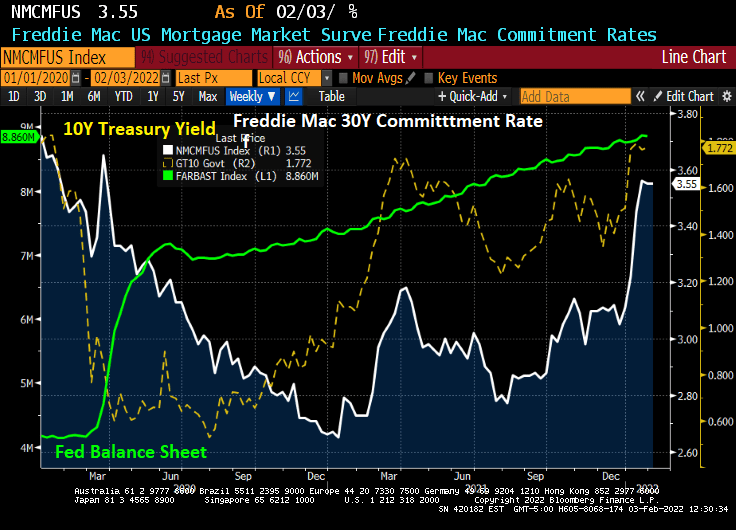

The result of Lagarde’s jaw boning?

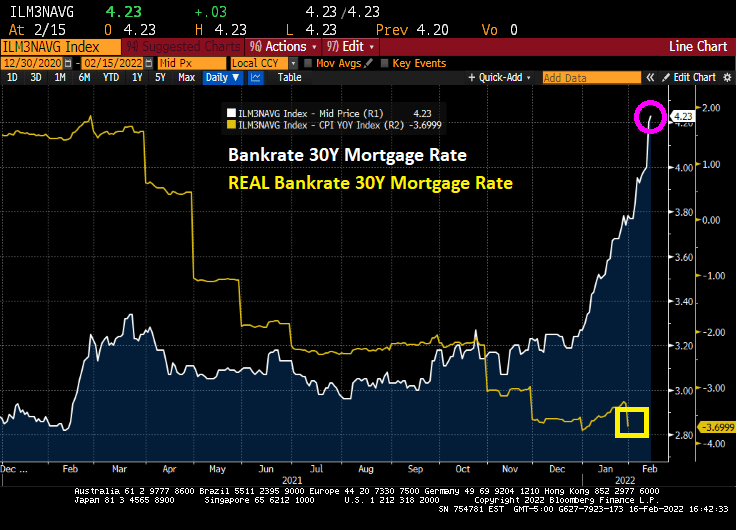

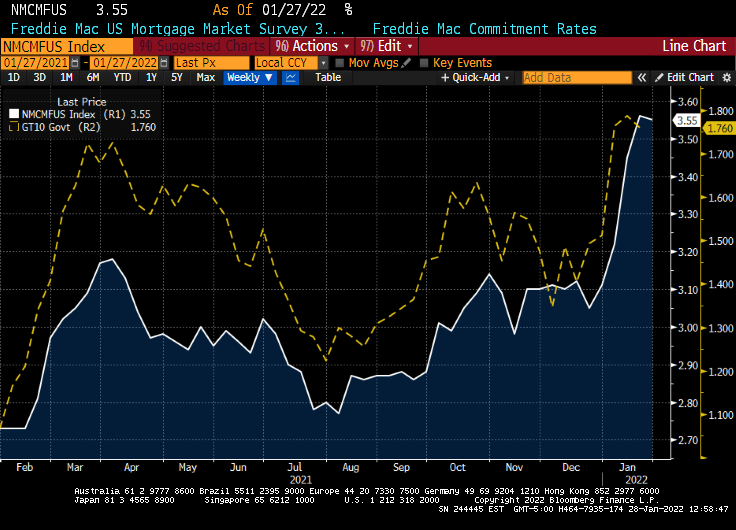

US mortgage rates are rising in anticipation of the US following Largarde’s lead. Powell and the Gang continue to lag.

Raphael Bostic and Goldman Sachs are both calling for dramatic rate increases to fight inflation … that they helped cause with their monetary stimulypto. I call this The Fed’s March of the Toreadors as The Fed now attempts to kill the bull market.

(Bloomberg) — The Treasury yield curve flattened to the lowest level in over a year on Monday as the prospect of a super-sized Federal Reserve rate increase in March gained traction, weighing disproportionately on shorter-dated tenors.

Two-year U.S. yields climbed as much as 4 basis points after Raphael Bostic, the president of the Fed’s Atlanta branch, said the U.S. central bank could raise its benchmark rate by 50 basis points if a more aggressive approach to taming inflation is needed.

That narrowed the gap with ten-year counterparts — which rose about half as much — to the least since October 2020. The last time the Fed delivered a half-point increase to borrowing costs was at the height of the dot-com bubble in 2000.

The repricing extended a move spurred last week, after Fed Chair Jerome Powell underscored the policy maker’s determination to put a lid on inflation. The market positioning may have been exacerbated by hedge funds that had been leaning the wrong way before Powell’s address.

Traders are currently betting the Fed will deliver 32 basis points of tightening in March, more than fully pricing an increase of a quarter-point. That puts the implied probability of a 50-basis-point increase at almost 30%. The odds of such a move in December were zero.

Consumer prices rose an annual 7% in December, the fastest pace in almost four decades. Powell left the door open to increasing rates at every meeting, and didn’t rule out the possibility of a 50-basis-point hike.

In an interview with the Financial Times, Bostic stuck to his call for three quarter-point interest rate increases in 2022, while saying that a more aggressive approach was possible if warranted by the economic data. Bostic is a non-voting member of the FOMC this year.

Since the rapid growth in inflation was caused by a combination of too much Fed stimulus, too much fiscal stimulus and “green” energy policies, it is unclear whether an increase of 50 basis points will do much, particularly if Bostic’s own Atlanta Fed GDPNow forecast of 0.051% is accurate. Raising ratesif the economy is slowing??

To be clear, Bostic and others are trying to signal The Fed’s intent well in advance to avoid a surprise knock-down of the stock market. Or a killing of the bull market.

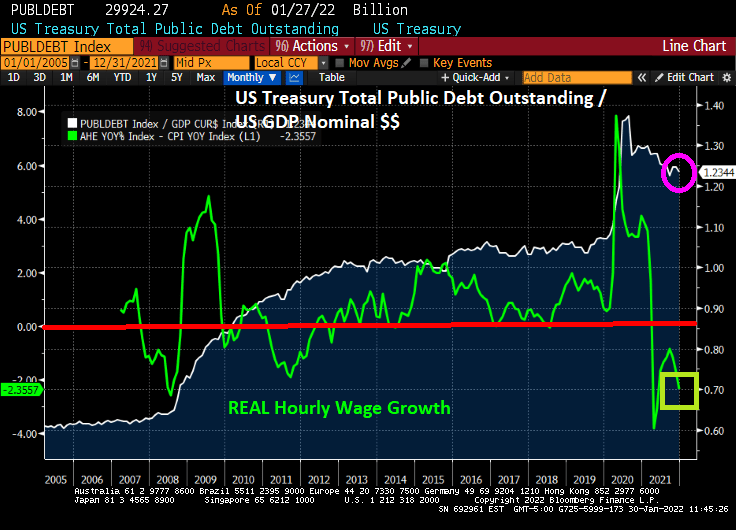

Nothing has been the same since the financial crisis of 2008 (except we still have insider-trading superstar Nancy Pelosi as US House Speaker). What has changed is that US Public Debt to GDP (nominal dollars) has doubled.

Has doubling Federal debt helped the hourly worker? Initially we saw a surge in REAL hourly wage growth in 2009 as the US began to recover from the housing bubble burst and ensuing financial crisis. Another surge in REAL wage growth occurred when Federal debt exploded as the COVID crisis took hold. BUT more recently we see that REAL wage growth is negative.

The other aspect of pain for hourly workers is inflation which has reached 7%, the highest rate in 40 years.

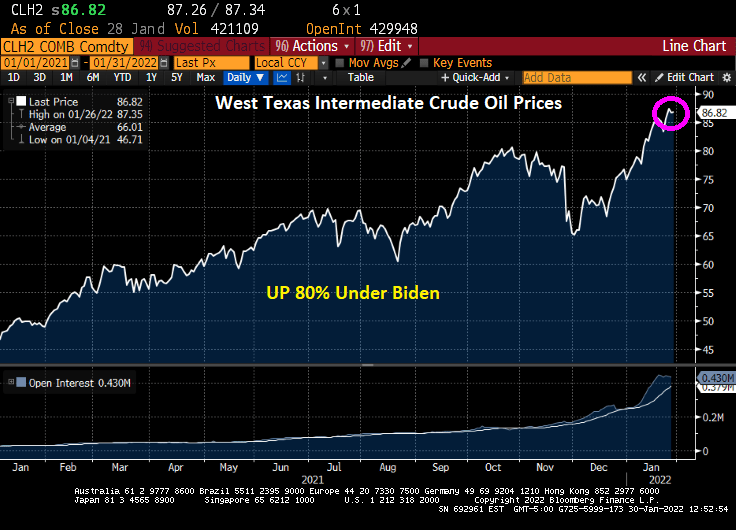

Adding to the frustration of hourly workers is energy prices rising 80% under President Biden’s reign of error.

Most hourly wage earners can’t buy a Tesla or a $100,000 electric Chevy Silverado to take advantage of Biden’s green energy policies.

No, not the Klaus von Bulow type of “reversal of fortune” (when he killed his wife). I am talking about a reversal in fortune for America.

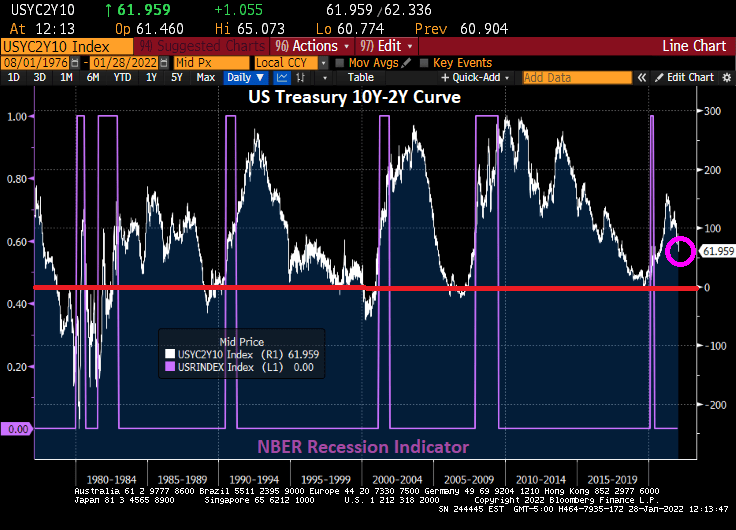

Let’s look at the 10Y-2Y Treasury curve. It typically falls below 0 basis points before every recession. Except the mini-COVID recession of 2020. But notice that the Treasury curve did not recover from the COVID recession as it typically did. More along the lines of 1984-1985.

Speaking of Reversal of Fortune, everything changed once Fed Chair Powell started to speak after Tuesday’s FOMC meeting.

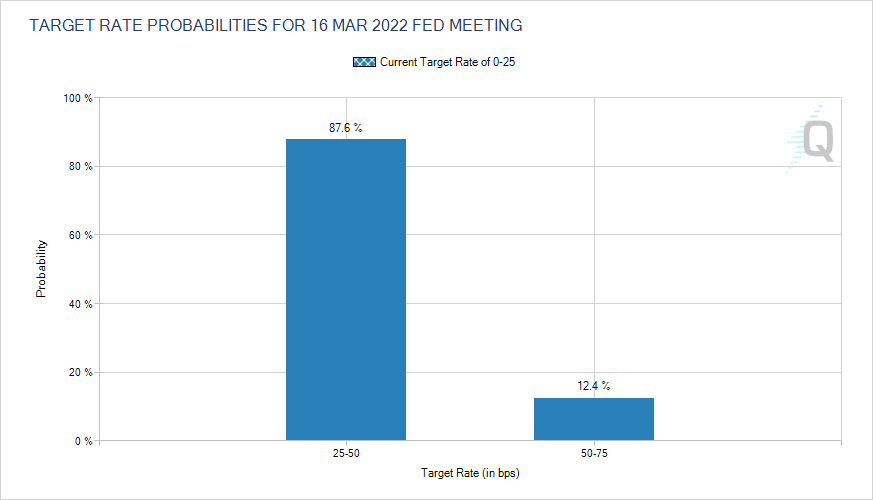

Hmm. Midterm elections, possible Russian invasion of The Ukraine, further problems in China, etc. While The Fed Funds Future data implies that The Fed may raise their target rate 5 times over the coming year, we’ll see.

If 2021 was a great year for the US housing market, 2022 faces “a new normal” marked by a slowing down of home price rises, job layoffs in the mortgage industry, and concerns over rising inflation and interest rate hikes, according to Douglas Duncan (pictured), Fannie Mae’s senior vice president and chief economist.

Duncan said “a shift” was underway in the market and the wider economy, which would result in far more moderate home price appreciation, expected to be between 7% and 7.5% this year due to the ending of fiscal and monetary stimulus.

“One of the elements of the shift is that you’re going to see house prices up, but not nearly as far as they were in the last two years because that was driven hugely by the fiscal and monetary stimulus (now) being removed,” he told MPA.

Ominously, he added that low interest rates “may never be seen again”. Or at least until Biden appoints more doves to The Federal Reserve Board of Governors.

You must be logged in to post a comment.