The US is Living La Vida Biden (living the Biden life!) Which means you are making millions if you are a political elite, but suffering if you live on Main Street.

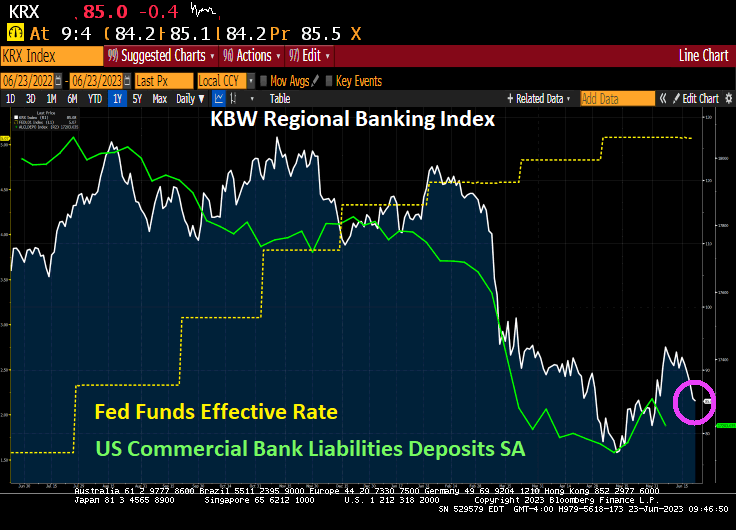

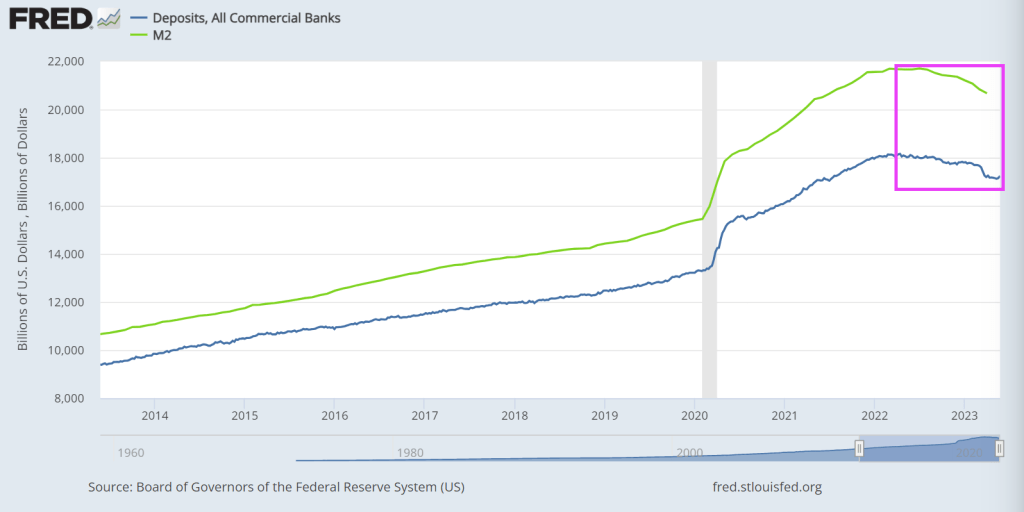

And regional banks (not the TBTF national banks) continue to suffer. The Bank Term Funding Program (1 of 2) is skyrocketing as The Fed cranks up rates to fight BidenFedflation (a combination of excessive monetary stimulus by The Fed and Biden’s lousy economic policies) and M2 Money growth crashes.

The regional banking index continues to fall as bank deposits shrink (like me when I used to jump in the Pacific Ocean in Santa Cruz).

Cryptos down this morning. But Bitcoin is above $30,000 … again.

Oil is down this morning but gold and silver are up slightly.

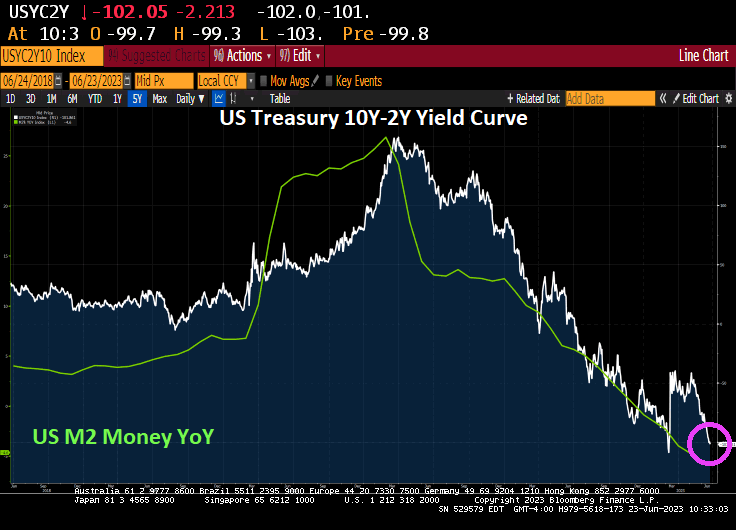

The 10Y-2Y US Treasury yield curve just dipped below -100 basis points (steep inversion) as M2 Money growth crashed and burned.

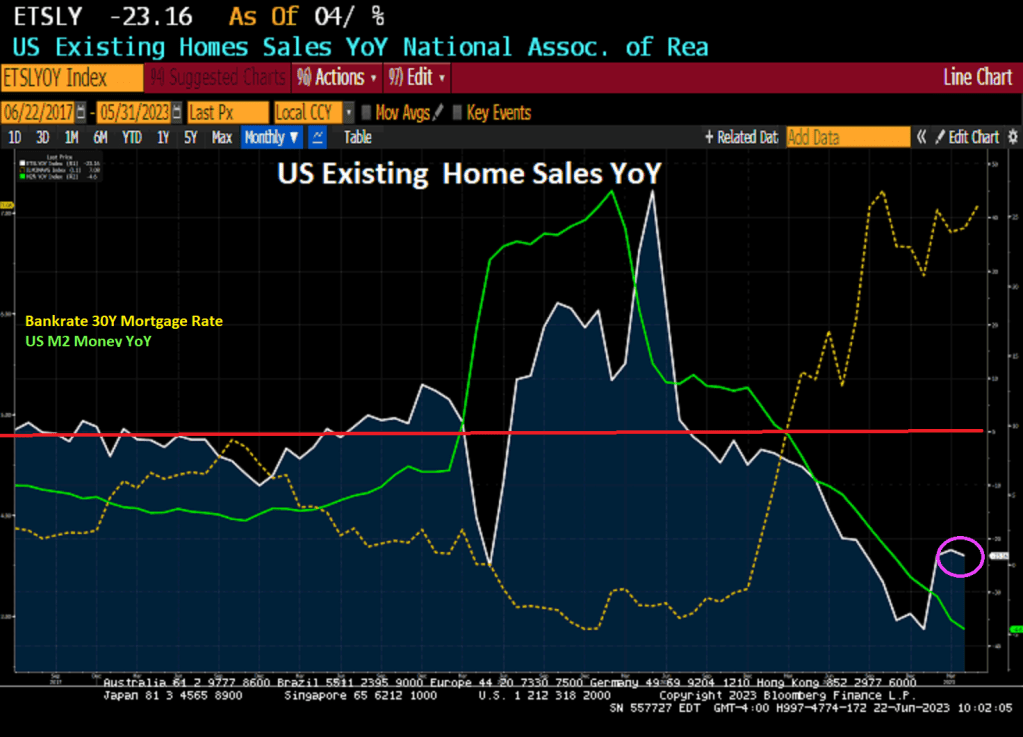

Like a bad good news, bad news joke, the good news is that US existing home sales ROSE 0.2% in May. The bad news? Existing home sales are DOWN -23.16% on a year-over-year basis.

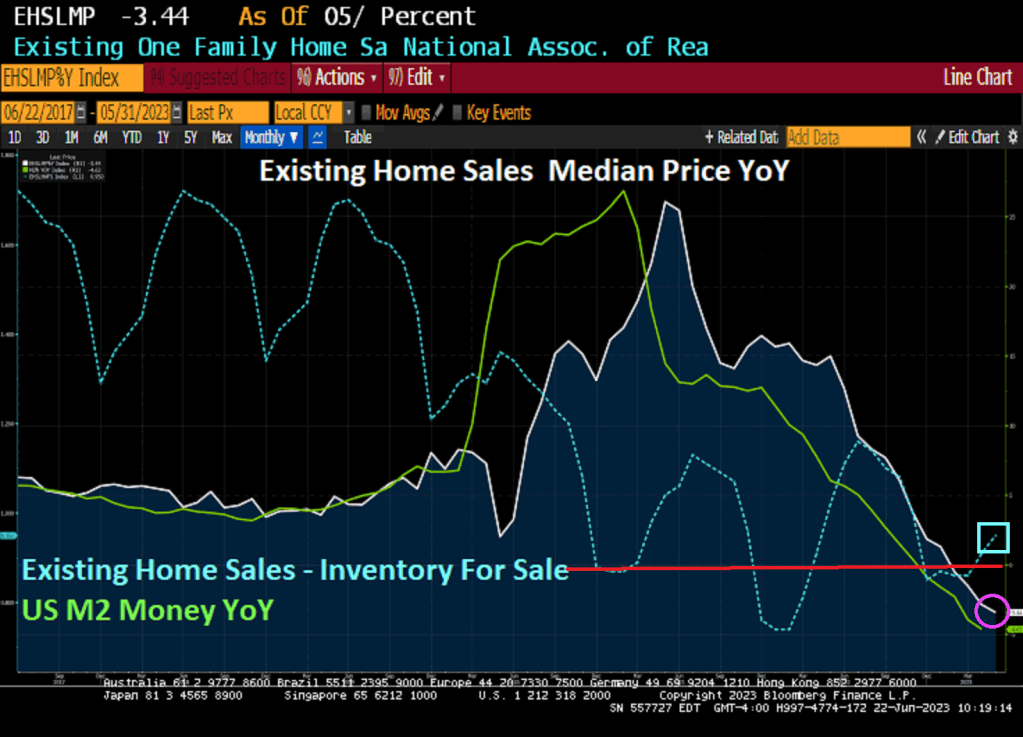

And the median price of existing home sales fell -3.44% YoY as inventory for sales remains missing in action (like Biden debating Democrat challengers).

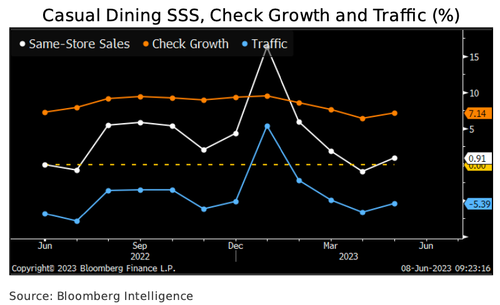

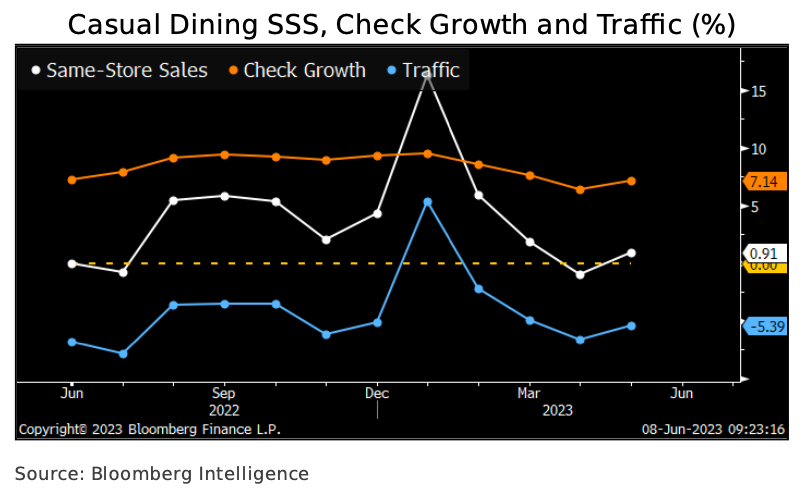

Bloomberg Intelligence’s Michael Halen penned a new note titled “2H Restaurant Sales: Inflation Killing Appetites.” It outlines, “Consumer spending finally buckles under more than two years of inflation and price hikes,” and the likely result is a trade-down of casual-dining chains like Brinker and Cheesecake Factory for quick-service chains like McDonald’s and Wendy’s.

The trade-down, which could start as early as this summer, is expected to dent consumer spending in restaurants such as Cheesecake Factory, Texas Roadhouse, and at brands operated by Brinker and Darden, Halen said.

Casual-dining industry same-store sales rose just 0.9% in May, according to Black Box Intelligence, as traffic dropped 5.4%. We expect cash-strapped low- and middle-income diners to cut restaurant visits and checks through year-end due to more than two years of real income declines and ballooning credit-card balances.

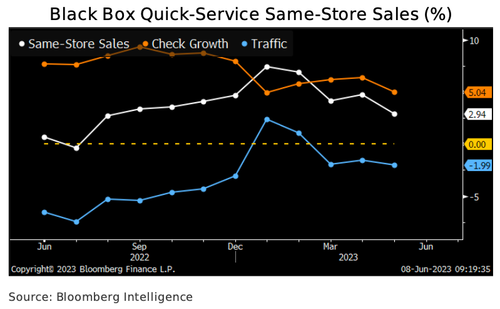

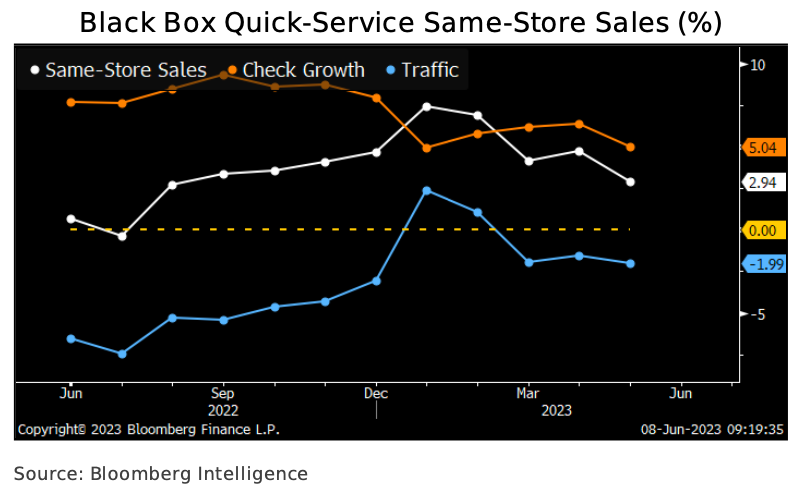

Halen provides more details about quick-service restaurants to fare better than causal-dining ones as “consumer spending finally buckles.”

Quick-service restaurants’ same-store sales could moderate with consumer spending in 2H but should fare better than their full-service competitors. Results rose 2.9% in May, according to Black Box data, as a 5% average-check increase was partly offset by a 2% guest-count decline. Check- driven comp-store sales gains are unsustainable, and we think inflation and menu price hikes will motivate low- and middle-income diners to reduce restaurant visits and manage their spending in 2H. On Domino’s 1Q earnings call, management said lower-income consumers shifted delivery occasions to cooking at home. Still, a trade-down from full-service dining due to cheaper price points may cushion the blow.

McDonald’s, Burger King, Wendy’s, and Jack in the Box are among the quick-service chains in Black Box’s index.

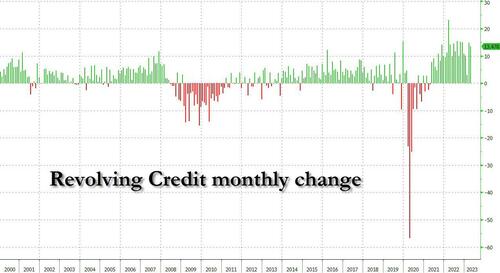

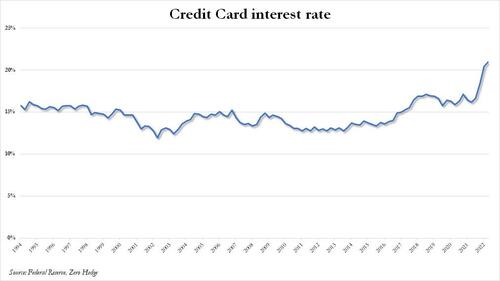

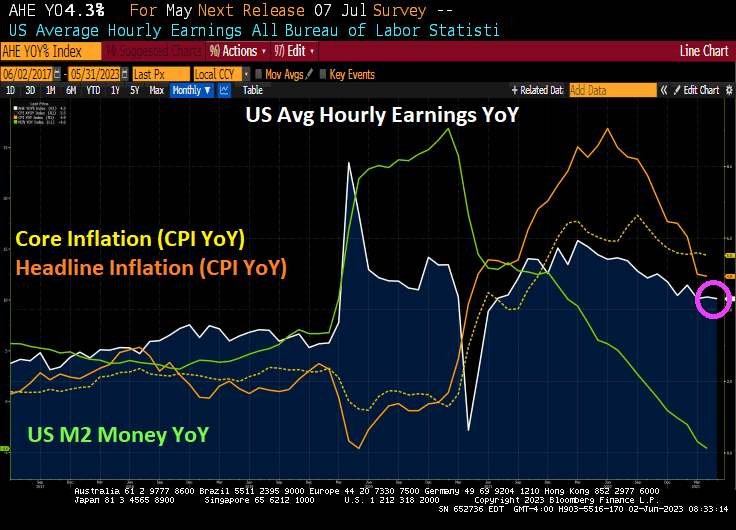

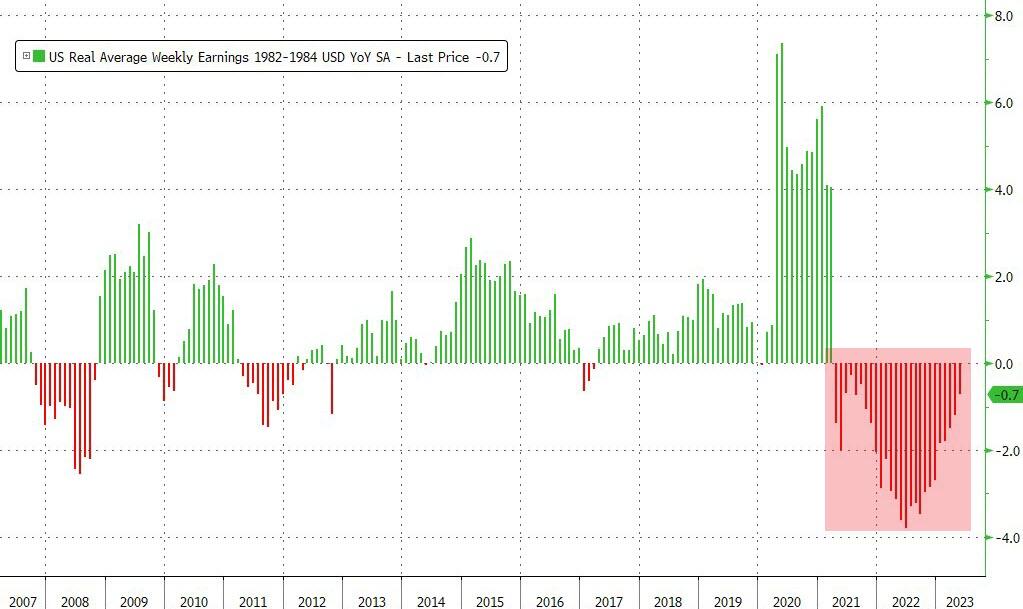

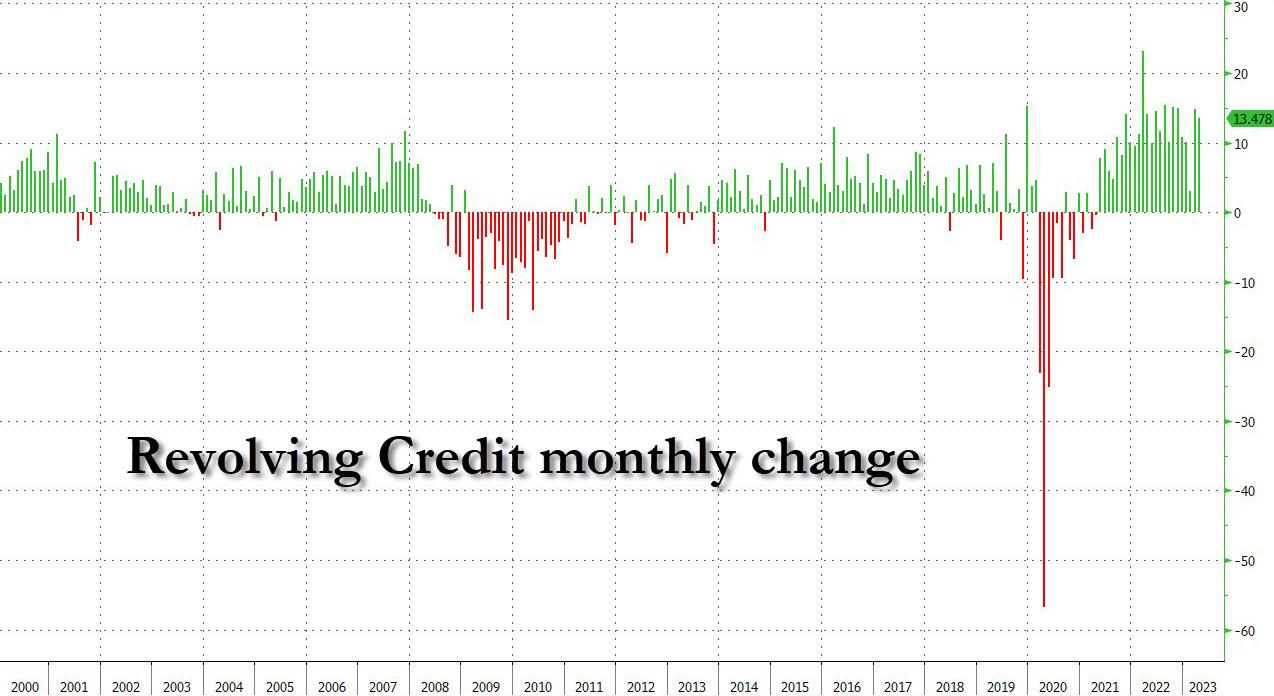

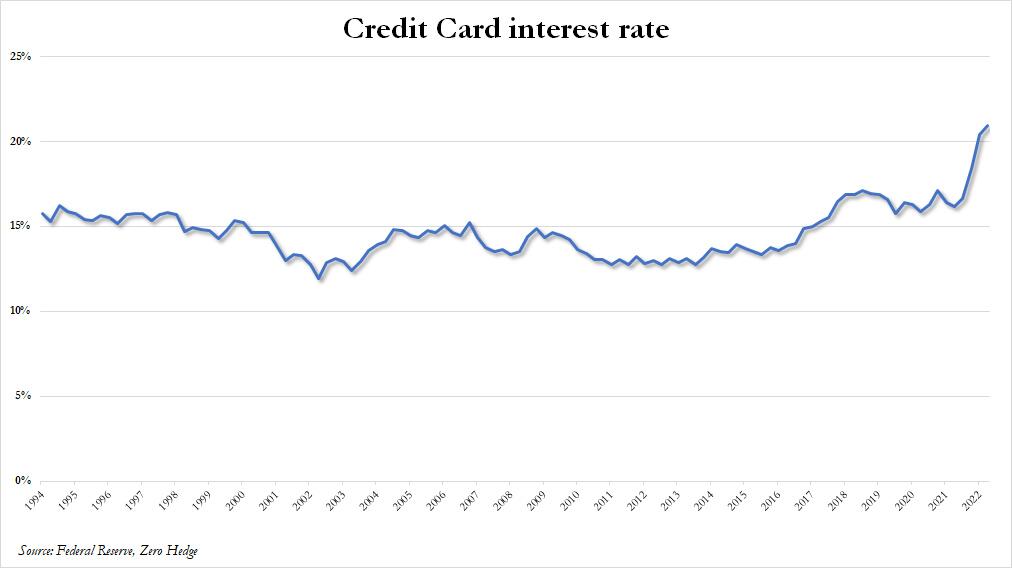

The latest inflation data shows consumers have endured the 26th straight month of negative real wage growth. What this means is that inflation is outpacing wage gains. And bad news for household finances, hence why many have resorted to record credit card usage.

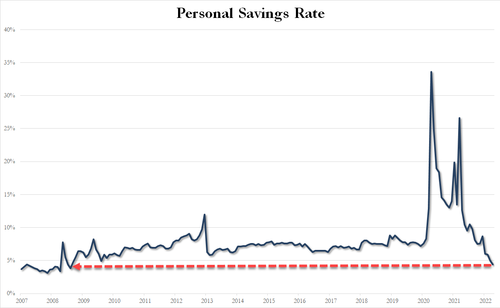

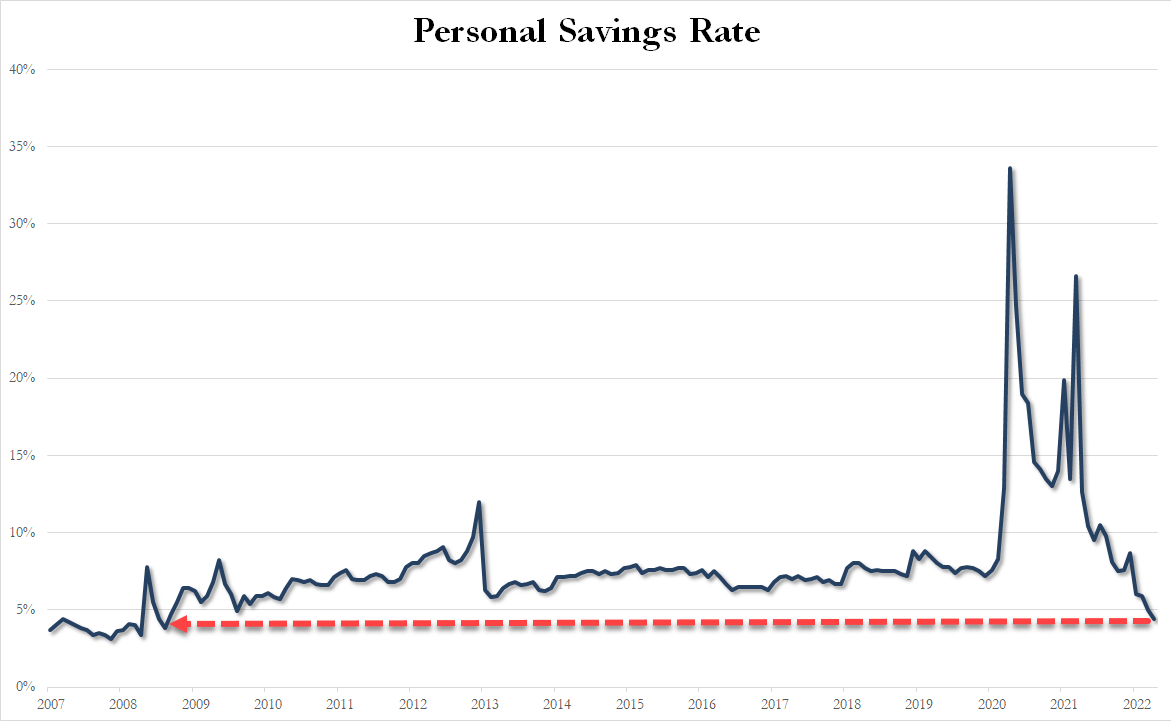

And the personal savings rate has collapsed to just 4.4%, its lowest level since Sept. 2008 (the dark days of Lehman). And why is this? To afford shelter, gas, and food, consumers are drawing from emergency funds due to the worst inflation storm in a generation.

As revolving consumer credit has exploded higher and the last two months have seen a near-record increase…

… even as the interest rate on credit cards has jumped to the highest on record.

With record credit card debt load and highest interest payments in years, plus depleted savings, oh yeah, and we forgot, the restart of student loan payments later this year, this all may signal a consumer spending slowdown at causal diners while many trade down for McDonald’s value menu. Even then, we’ve reported consumers have shown that menu items at the fast-food chain have become too expensive.

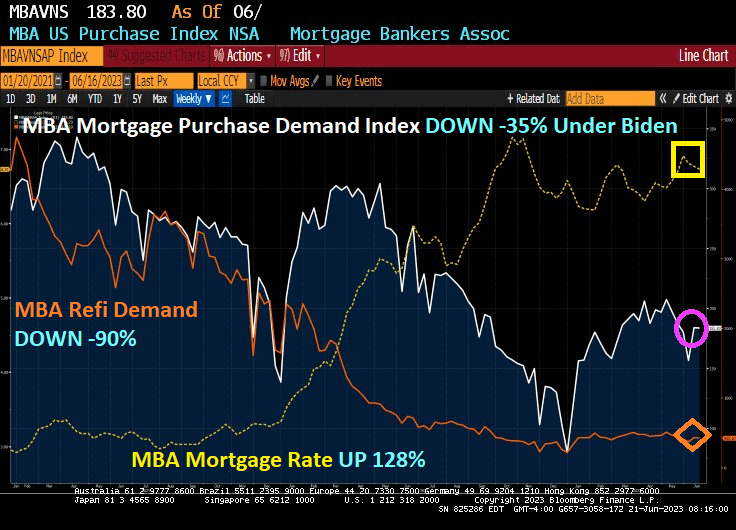

The good news? Mortgage purchase demand fell only -0.05% from last week. The bad news? Mortgage purchase demand is down -35% since Resident Biden was sworn in. And mortgage refinancing demand is down a whopping -90%. Reason? Mortgage rates are up 128% under Clueless Joe.

Mortgage applications increased 0.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 16, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 0.5 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 1 percent compared with the previous week. The Refinance Index decreased 2 percent from the previous week and was 40 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index decreased 0.1 percent compared with the previous week and was 32 percent lower than the same week one year ago.

And as Paul Harvey used to say, here is the rest of the story.

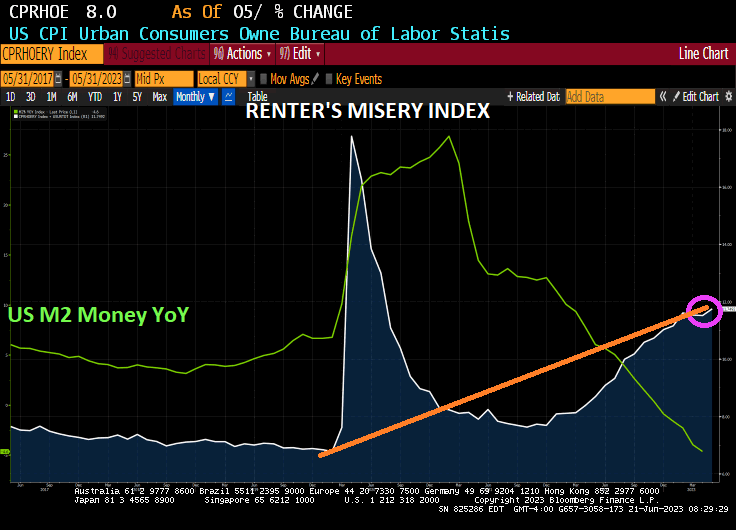

And the renter’s misery index, CPI for owner’s equivalent rent YoY + U-3 unemployment rate, is now a staggering 11.75% verus 6.78% in February 2020, the last month before the Chinese Wuhan virus led to economic and school shutdowns. And we have Donald Trump as President instead of this corrupt clown.

What is the difference between baseball legend Shoeless Joe Jackson and Clueless Joe Biden? While both sold out their teams for personal wealth, at least Shoeless Joe was good at baseball. Clueless Joe is a corrupt bully. Shoeless Joe was allegedly stupid, but so is Clueless Joe.

Fed Governor Christopher Waller said Friday headline inflation has been “cut in half” since peaking last year, but prices excluding food and energy (aka, CORE inflation) has barely budged over the last eight or nine months.

“That’s the disturbing thing to me,” Waller said during a question-and-answer session following a speech in Oslo, Norway. “We’re seeing policy rates having some effects on parts of the economy. The labor market is still strong, but core inflation is just not moving, and that’s going to require probably some more tightening to try to get that going down.”

At a separate event Friday, Richmond Fed President Thomas Barkin said inflation remained “too high” and was “stubbornly persistent.”

“I want to reiterate that 2% inflation is our target, and that I am still looking to be convinced of the plausible story that slowing demand returns inflation relatively quickly to that target,” Barkin said in a speech in Ocean City, Maryland. “If coming data doesn’t support that story, I’m comfortable doing more.”

The Federal Open Market Committee paused its series of interest-rate hikes Wednesday, but policymakers projected rates would move higher than previously expected in response to surprisingly persistent price pressures and labor-market strength.

The consumer price index this week showed headline inflation slowed, but core prices excluding food and energy continued to rise at a pace that’s concerning for Fed officials. Employers continued adding jobs at a rapid clip in May, and job openings climbed in April, recent data showed.

Barkin warned that prematurely loosening policy would be a costly mistake.

“I recognize that creates the risk of a more significant slowdown, but the experience of the ’70s provides a clear lesson: If you back off inflation too soon, inflation comes back stronger, requiring the Fed to do even more, with even more damage,” he said. “That’s not a risk I want to take.”

Policy Report

Separately, the Fed released a new report Friday that said tighter US credit conditions following bank failures in March may weigh on growth, and that the extent of additional policy tightening will depend on incoming data.

“The FOMC will determine meeting by meeting the extent of additional policy firming that may be appropriate to return inflation to 2% over time, based on the totality of incoming data and their implications for the outlook for economic activity and inflation,” the Fed said in in its semi-annual report to Congress.

Read More: Fed Says Tighter Credit Conditions to Weigh on US Growth

The Fed report, which provides lawmakers with an update on economic and financial developments and monetary policy, was published on the central bank’s website ahead of Chair Jerome Powell’s testimony before the House Financial Services Committee on June 21. He will appear before the Senate banking panel the following day.

“Evidence suggests that the recent banking-sector stress and related concerns about deposit outflows and funding costs contributed to tightening and expected tightening in lending standards and terms at some banks beyond what these banks would have reported absent the banking-sector stress,” the report said.

But it isn’t just San Francisco. Phil Hall reports that Fitch Ratings reduced its 2023 outlook for the U.S. real estate investment trust (REIT) sector outlook from “Neutral” to “Deteriorating,” citing the tumult in the commercial real estate space.

While Fitch noted that most of its rated REITs “have the capacity to withstand such a slowdown within rating sensitivities [and] those with ample dry powder could capitalize on distressed property sales by weaker capitalized players.” But at the same time, the ratings agency warned that banks – which account for nearly half of the $5.5 trillion commercial mortgage market – saw their lending levels drop by 20% between February and April, with more tightening expected.

“At minimum, this will lead to further contractions in CRE credit, further limiting conditions for property transactions,” Fitch added in its announcement of the outlook reduction, adding that “CRE transaction volume has steadily declined since early 2022 due to the confluence of operating fundamentals pressure, higher interest and capitalization rates, limited buyer financing, and looming recession risk. The rapid jump in rates has resulted in unusually wide value discrepancies between buyers and sellers across most property types and markets, particularly in the struggling office sector. Our forward-looking U.S. equity REIT ratings incorporate assumptions about future property disposition volumes and valuations.”

Fitch predicted the U.S. economy will go into a recession, most likely late in the year – a previous forecast put the downturn at mid-year – and forecasted property performances will vary by sector over the next two years.

“Sectors experiencing strong fundamentals, such as industrial and shopping centers, will likely see some cooling in demand, with tenants showing greater reluctance to lease space, including delaying decisions, resulting in less pricing power for landlords,” Fitch continued. “Tighter lending conditions and weaker economic growth will add to the secular pressures facing some property formats (e.g. office, enclosed malls). The office REIT sector has met, or modestly underperformed, our low expectations during 2023. Leasing volumes have generally underperformed as occupiers add the business cycle to the list concerns and reasons for conservatism, along with secular pressure from remote work. Conversely, the industrial sector, although no longer white hot, continues to deliver above average occupancies and outsized rent growth that have modestly exceeded our projections.”

While Fitch stressed that REITs were “unlikely to directly encounter meaningful stress” based on the recent problems in the banking industry, although it also acknowledged that it did not expect “REITs’ access to unsecured revolvers will be impeded, although facilities up for renewal will likely see higher pricing and some banks have reduced appetites for traditional bank syndicate activities, such as making funded term loans – particularly in hard hit sectors, such as office. We also do not expect meaningful portfolio vacancies caused by bank tenant failures, which are unlikely to be widespread.”

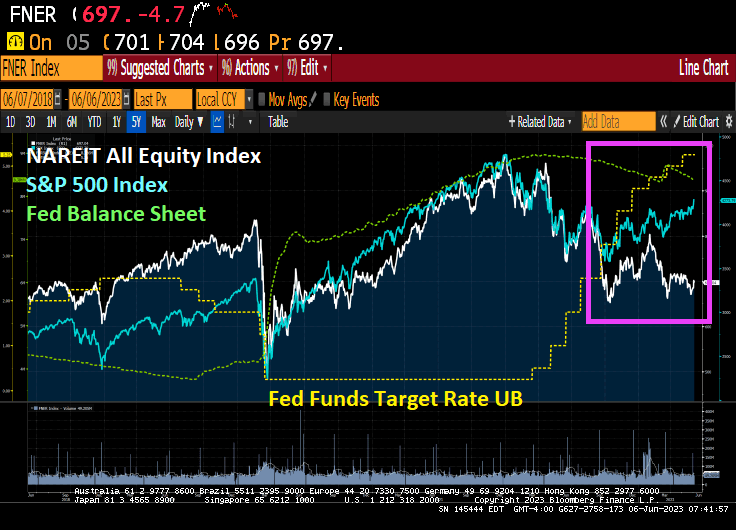

The NAREIT All-equity index has gotten pummelled by the S&P 500 index since The Fed started tightening monetary policy to fight inflation …. that The Fed helped cause in the first place.

Under Biden, the US is beginning to morph into a lawless Socialist sewer like Venezuela. Joe Maduro??

The US economy was sitting high on the global mountain top before Covid. Then Covid struck, The Federal Reserve and Congress went wild with stimulus spending and inflation went wild. This is Biden Country, a feeble shell of this once great nation.

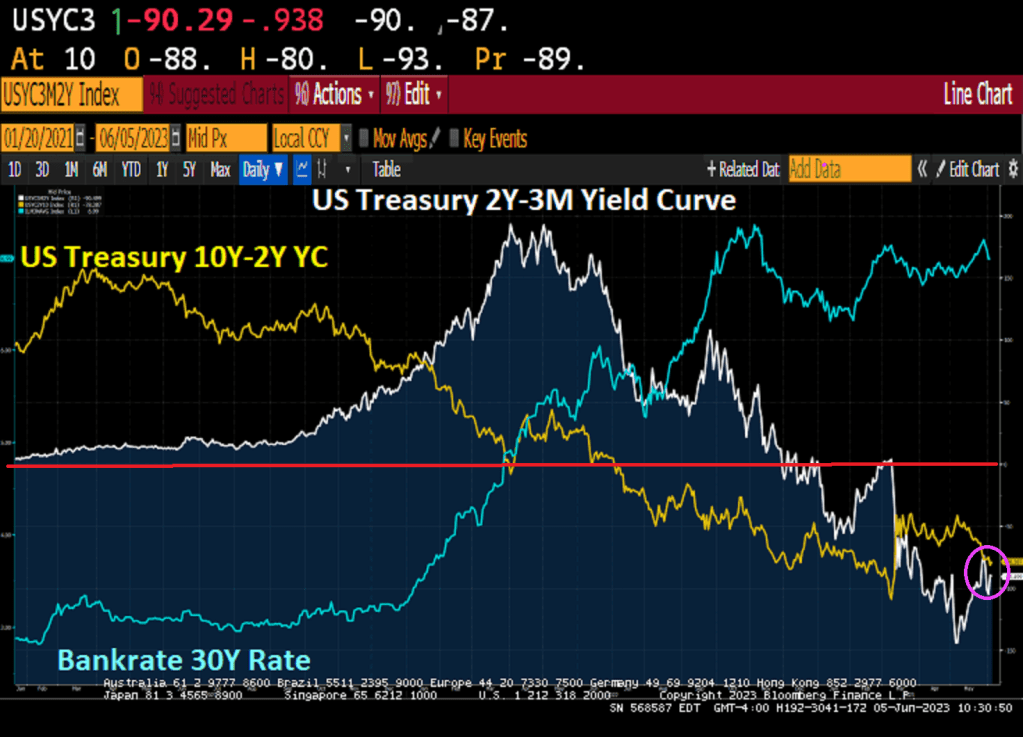

As The Fed tries to counter the years of excess monetary stimulus pre and post Covid by raising rates, we have seen mortgage rates rise 143% under Biden’s leadership. At the same time, the US Treasury yield curves (short 2Y-3m and long 10Y-2Y) remain deeply inverted.

As of this AM, The Fed Funds Futures market is pricing in a chance of continued rate hikes by The Fed, but mostly we are at 5.25% at least until November when rates are forecast to begin declining.

And the Taylor Rule is still signaling rate hikes to 10.12%. We are at only 5.25%. And with Biden feebily running for reelection, the only path forward is rate CUTS.

Well, Kevin McCarthy (RINO-CA) and Patrick McHenry (RINO-NC) along with Jim Jordan (RINO-OH) and Marjorie Taylor Greene (RINO-GA) sold out America to Green Joe Biden (the Jolly Green Giant?) and pretty much guaranteed a Biden reelection as President and Democrats winning the House majority at the next election. Way to go McCarthy, McHenry, Jordan an Greene! You sold out America to the Progressive, destructive Left.

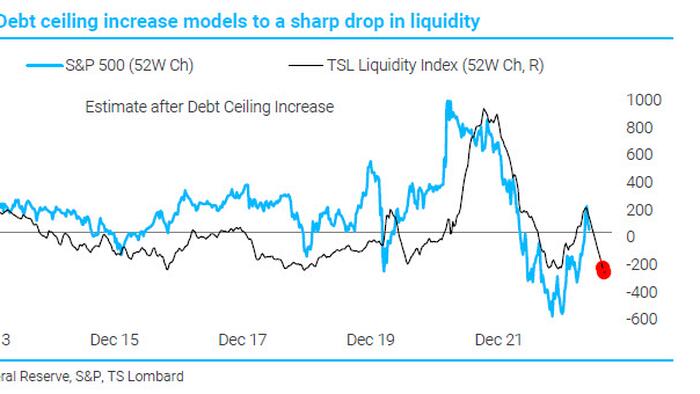

With a debt ceiling deal freshly inked, the US Treasury is about to unleash a tsunami of new bonds to quickly refill its coffers.This will be yet another drain on dwindling liquidity as bank deposits are raided to pay for it — and Wall Street is warning that markets aren’t ready.

The negative impact could easily dwarf the after-effects of previous standoffs over the debt limit. The Federal Reserve’s program of quantitative tightening has already eroded bank reserves, while money managers have been hoarding cash in anticipation of a recession.

JPMorgan Chase & Co. strategist Nikolaos Panigirtzoglou estimates a flood of Treasuries will compound the effect of QT on stocks and bonds, knocking almost 5% off their combined performance this year. Citigroup Inc. macro strategists offer a similar calculus, showing a median drop of 5.4% in the S&P 500 over two months could follow a liquidity drawdown of such magnitude, and a 37 basis-point jolt for high-yield credit spreads.

The sales, set to begin Monday, will rumble through every asset class as they claim an already shrinking supply of money: JPMorgan estimates a broad measure of liquidity will fall $1.1 trillion from about $25 trillion at the start of 2023.

“This is a very big liquidity drain,” says Panigirtzoglou. “We have rarely seen something like that. It’s only in severe crashes like the Lehman crisis where you see something like that contraction.”

It’s a trend that, together with Fed tightening, will push the measure of liquidity down at an annual rate of 6%, in contrast to annualized growth for most of the last decade, JPMorgan estimates.

The US has been relying on extraordinary measures to help fund itself in recent months as leaders bickered in Washington. With default narrowly averted, the Treasury will kick off a borrowing spree that by some Wall Street estimates could top $1 trillion by the end of the third quarter, starting with several Treasury-bill auctions on Monday that total over $170 billion.

What happens as the billions wind their way through the financial system isn’t easy to predict. There are various buyers for short-term Treasury bills: banks, money-market funds and a wide swathe of buyers loosely classified as “non-banks.” These include households, pension funds and corporate treasuries.

Banks have limited appetite for Treasury bills right now; that’s because the yields on offer are unlikely to be able to compete with what they can get on their own reserves.

But even if banks sit out the Treasury auctions, a shift out of deposits and into Treasuries by their clients could wreak havoc. Citigroup modeled historical episodes where bank reserves fell by $500 billion in the span of 12 weeks to approximate what will happen over the following months.

“Any decline in bank reserves is typically a headwind,” says Dirk Willer, Citigroup Global Markets Inc.’s head of global macro strategy.

Bitcoin Faces Downside Risks After Debt Deal Moves Forward

Just when markets appear to be moving past the months-long drama around the US debt ceiling, holders of risky assets such as cryptocurrencies are likely facing a fresh challenge while the Treasury looks to rebuild its depleted cash balance with an estimated $1 trillion Treasury-bill deluge.

“The impending reserve drawdown, due to the [Treasury General Account] rebuild, may prove to be a headwind,” Citi Research strategists including Alex Saunders wrote in a note.

Citi analyzed the performance of risky assets during drawdowns and found that they were vulnerable to higher volatility and weaker returns. As such, the near-term outlook doesn’t seem too rosy for Bitcoin and Ether. “Both coins average negative returns in these scenarios, and BTC has significantly underperformed in the median case,” the strategists wrote Thursday.

The TGA, which keeps money for the Treasury, ballooned during the pandemic. It expanded again last year and is now about as low as it has ever been. Treasury, as a result, will need to replenish its dwindling cash buffer to maintain its ability to pay its obligations through bill sales, estimated at well over $1 trillion by the end of the third quarter. This supply burst may drain liquidity from the banking sector and raise short-term funding rates against an economy many say is likely to fall into recession.

This doesn’t bode well for digital-asset investors, who were just recovering from fears of a no-deal scenario for the US debt ceiling. While Bitcoin edged higher on Friday, it’s still hovering around the $27,000-mark that it has failed to break away from for several weeks.

“Crypto markets were not immune to fears of the US defaulting on its debt, selling off on negative developments and rallying on headlines suggesting progress,” the strategists said. They added that crypto has typically “fared well” amid issues concerning traditional financial institutions, citing the banking turmoil in March, a period in which Bitcoin outperformed. But perhaps risks of an institution such as the US government defaulting “doesn’t paint a favorable outlook for decentralized digital assets.”

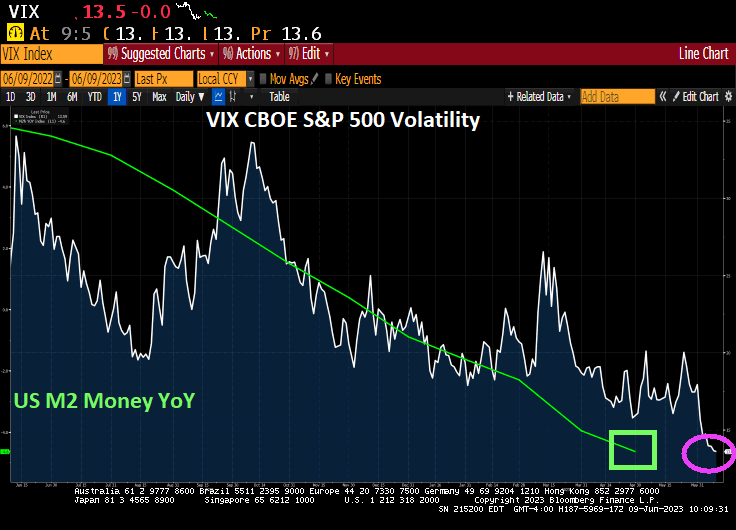

To illustrate, the strategists used the Cboe Volatility Index, or VIX, as an indicator of the market’s fear to gauge whether a resolution would be passed before hitting the ceiling. And whenever equity market concerns were eased, that’s when Bitcoin outperformed.

“While in theory the potential default of an institution as impactful as the US government would bode well for decentralized technologies and systems, this may not currently be the case given that the crypto industry is still in its infancy and regulation has yet to be well-defined,” they wrote. “Another theory is that not raising the debt ceiling would lead to reduced US government debt and a lower fiscal deficit, and provide more credibility to fiat, particularly the dollar.”

On Friday, the Senate passed legislation to suspend the US debt ceiling and impose restraints on government spending through the 2024 election. The measure now goes to President Joe Biden, who forged the deal with House Speaker Kevin McCarthy and plans to sign it just days ahead of a looming US default.

Year-to-date, Bitcoin has rebounded some 60% after starting the year at around $16,500. Such optimism comes after 2022’s 64% drop, its second-worst year in its history. It rose about 1% to $27,178 as of 3:32 p.m. in New York, and is marginally higher from last Friday.

Bitcoin’s support hovers around $26,500, said Fiona Cincotta, senior market analyst at City Index, adding that a break below $25,000 could mean a deeper sell-off.

“The problem is the macro backdrop, which is relatively uncertain going forward with recessionary fears,” she said. “I think what will be looking for to make Bitcoin shine is a nice dovish pivot from the Federal Reserve. That might be the tide where we will see another decent leg higher.”

Range-bound trading has been Bitcoin’s defining characteristic of late, with its 30-day volatility reigning low at 1.8%, firmly staying firm within its two-month-long trading range. Despite growing short-term volatility, options implied volatility trended lower over the past week, according to K33’s Bendik Schei and Vetle Lunde. Even so, Bitcoin exchange-traded products continued to see steady outflows while Bitcoin volumes — spot and futures — are trending lower.

McCarthy, McHenry, Jordan and Greene, honorary Frenchmen!

The not-so-good news? A large diverengence between the Establishment survey and Household survey. +339k versus -310k. What’s it going to be?

The bad news? While US average hourly earnings YoY cooled to 4.3%, inflation is still roaring at 4.9% (headline) and 5.5% (core). So Americans are still losing ground to inflation.

The unemployment rate rose to 3.7% in May while the underemployment rate rose to 6.7%.

With unemployment rising to 3.7%, the Taylor Rule implies a Fed Funds Target rate of 10.12%. We are currently at 5.25%. Or just a little over halfway there. But The Fed is talking a pause in rate hikes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.