Call this a double whammy! Red-hot rents combined with a slowing economy.

According to CoreLogic, single-family annual rent growth finished 2021 at a new record: 11.7% YoY for high tier rental properties and 10.4% YoY for low tier rental properties.

Of course, southern and southwest rental properties are seeing the fastest rent growth. Particularly Miami at 36% YoY. Phoenix is no slouch at 19% growth in rents.

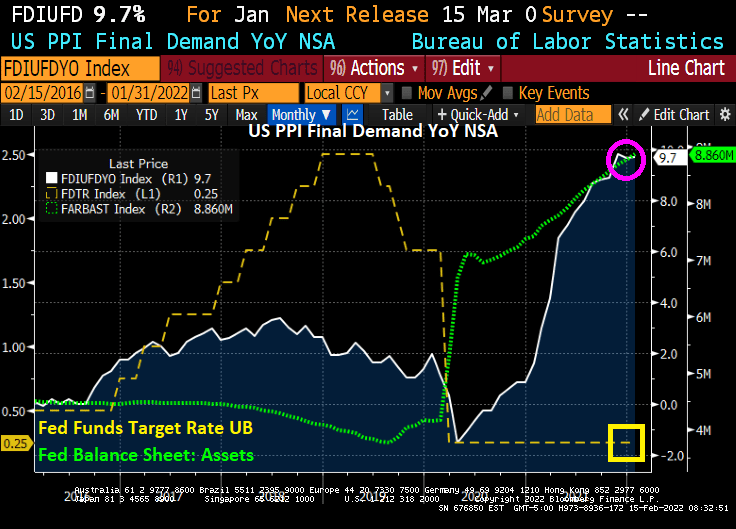

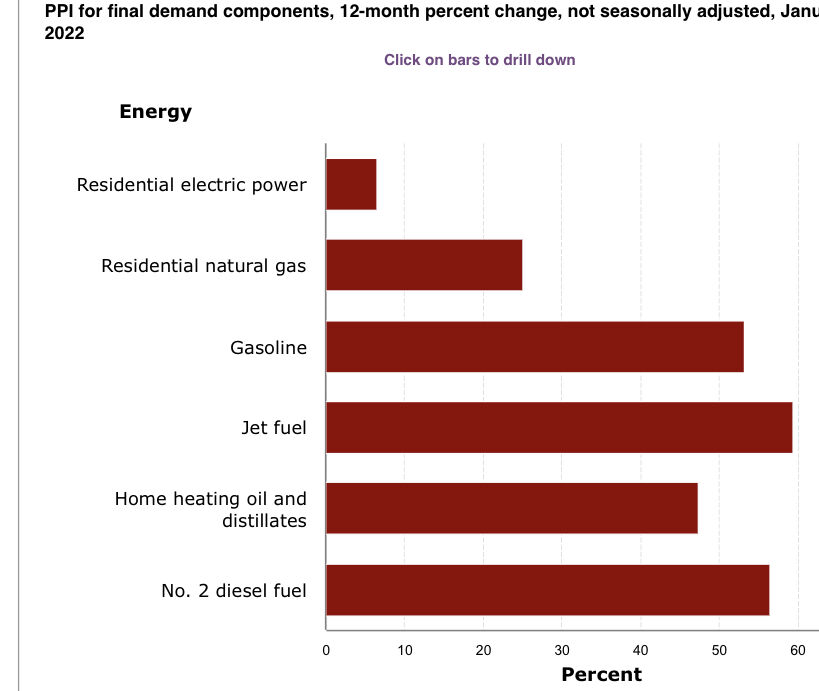

Today, the Final Demand Producer Price Index (PPI) printed at 9.7% YoY.

Biden claimed inflation was caused by COVID. How about 1) Biden’s anti-fossil fuel policies combined with 2) excessive fiscal (Biden and Congress) and excessive monetary stimulus (Fed)?

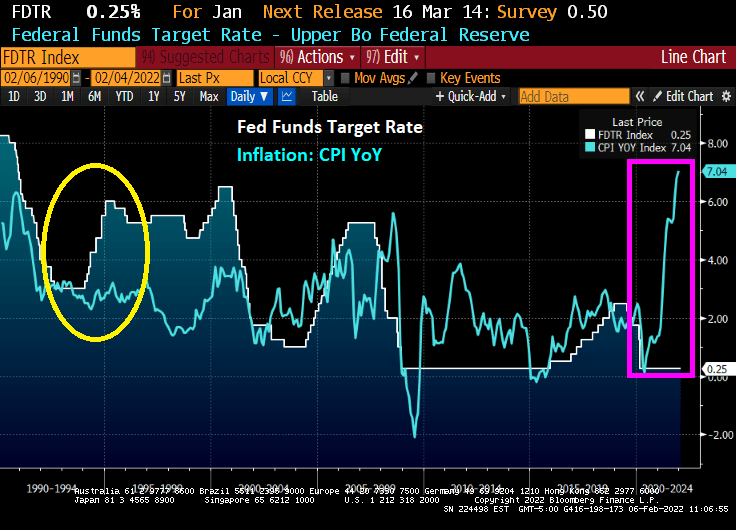

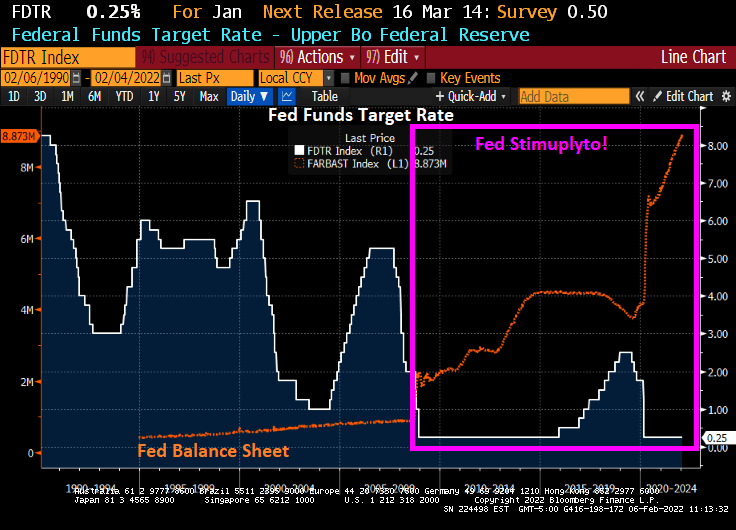

The Fed held its behind-closed-doors meeting on Monday, but nothing has been released about what they discussed. Suffice it to say, they have left the staggering monetary stimulus in play.

I wonder if The Fed is concerned about a soft landing with proposed rate increases.

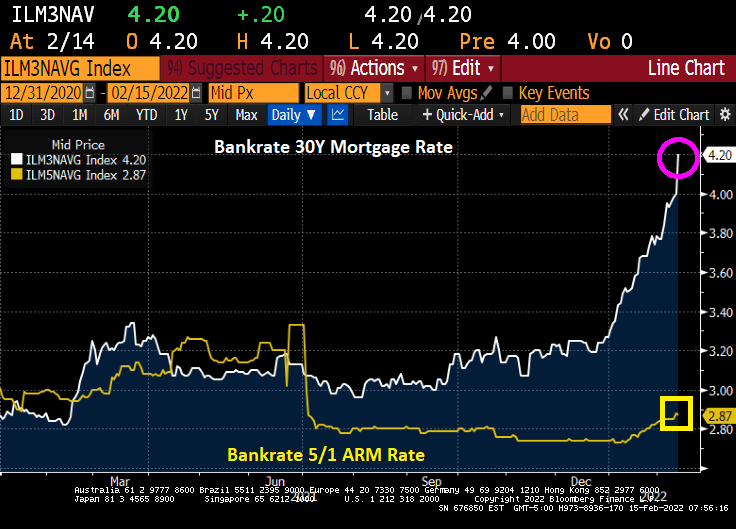

The US 30-year mortgage rate broke through the 4% barrier. According to Bankrate’s mortgage survey, the 30-year mortgage rate is now 4.2%.

Even more interesting is the 5/1 Adjustable Rate Mortgage (ARM) rate falling slightly to 2.87%. That is quite a spread between the 30-year fixed and 5/1 ARM rates! That is 133 basis points.

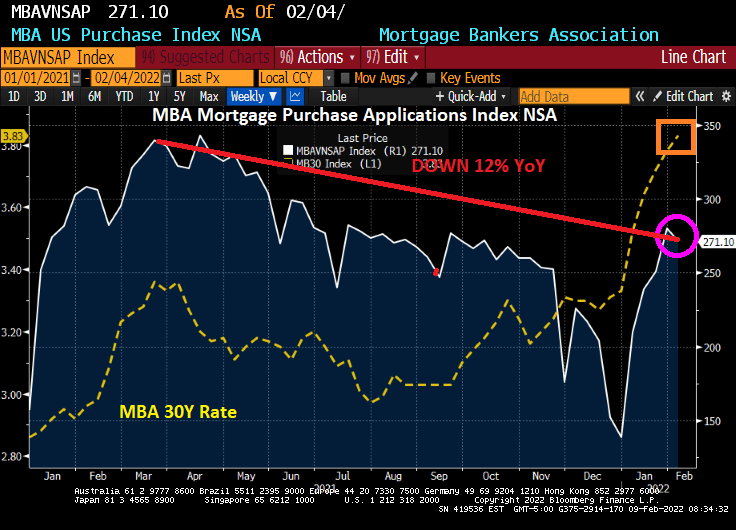

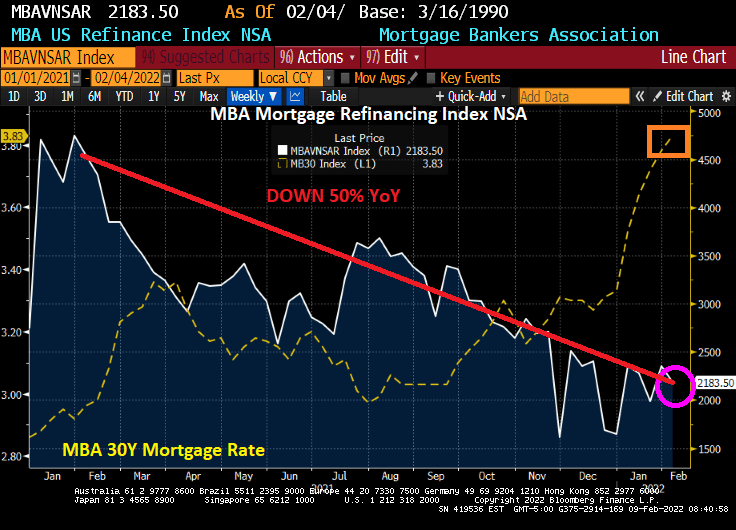

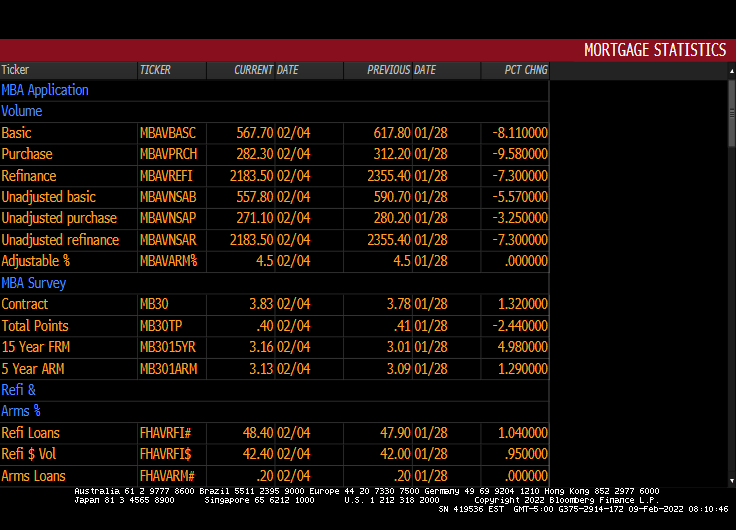

The Mortgage Bankers Association (MBA) released their weekly mortgage application survey this morning. Mortgage applications decreased 8.1 percent from one week earlier, for the week ending February 4, 2022.

The Refinance Index decreased 7 percent from the previous week and was 52 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 10 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 12 percent lower than the same week one year ago.

And mortgage refinancing applications are down 50% since the same week last week.

Here are the stats. Pretty much down across the board.

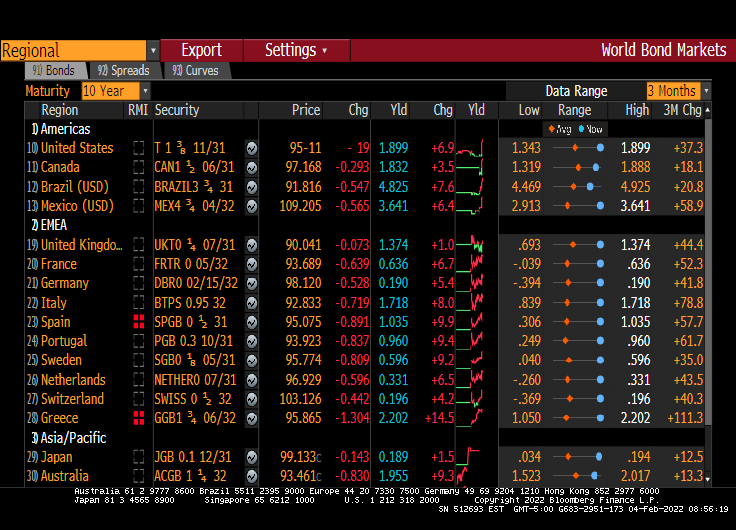

Once upon a time, European PIGS (Portugal, Italy, Greece and Spain) saw incredible spikes in their sovereign yields related to Greek credit default contagion. But the European Central Bank (ECB), World Bank (WB), International Money Fund (IMF) rose to the rescue.

But here we go again! Thanks to rising inflation, the ECB is threatening to remove the massive monetary stimulus. Sound familiar??

Here are the Eurozone 10-year sovereign yields as of this morning. Greece is up a whopping 27.4 basis points, Italy is up 11.7 BPS, Portugal is up 9.3 BPS and Spain is up 9.2 BPS. The core of the Eurozone, France and Germany, are up 4.3 and 3.0 BPS, respectively.

Germany has REAL 10Y Bunds yields of -4.7%.

Like the USA, the Eurozone Taylor Rule is much higher than the ECB’s Main Refinancing rate of 0%..

Here is ECB’s Christine Lagarde saying “What, me worry??”

(Bloomberg) What a difference 25 years makes. Worried that inflation was about to turn higher, the Federal Reserve in February 1994 began raising interest rates, taking the federal funds rate from 3% to 6% a year later. As it turned out, those worries were unfounded: The U.S. consumer price index barely budged, finishing the year at 2.7%, right where it had started.

Although inflation in many developed-world countries is now well above those levels — 7% in the U.S. alone — of the major central banks only the Bank of England has started to raise short-term rates. They are now, um, 0.25%. Across the developed world, short rates are still either barely above zero or negative. What’s more astonishing is that even though they have cut their purchases, the Federal Reserve and European Central Bank continue to buy about $140 billion of longer-maturity bonds every month, suppressing long-term yields even as inflation rages.

Some central banks say that rate hikes are coming, but their extraordinary reluctance to deal with actual inflation means it will become entrenched. Not only will policy makers have to raise rates more than they envision, but they will have to cut the size of their massive balance-sheet assets, too. Don’t expect that the process will be anything other than awful for risky assets of all stripes.

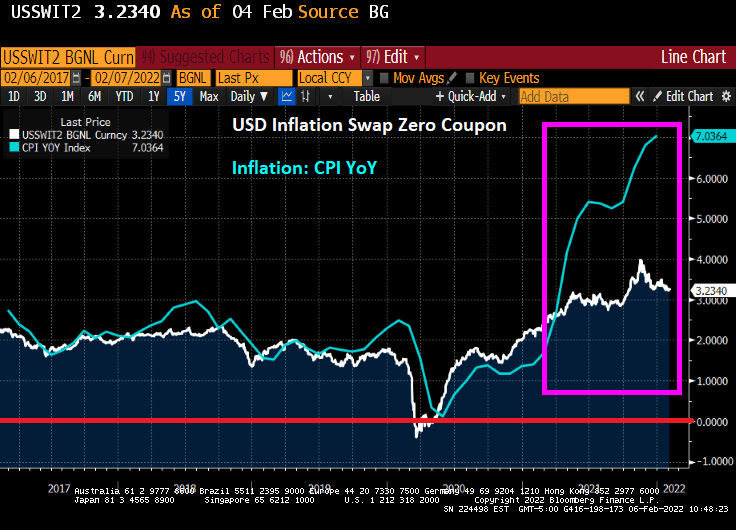

Over the last year and a half, inflation has not only accelerated but also broadened. It started with goods prices and has now expanded to services, even in the moribund euro zone. Central bankers and markets still believe inflation rates will come down a lot. The part of the swaps market that in essence predicts inflation in the future is pricing in a drop in the U.S. CPI to 3.6% by the spring of 2023 and to 3.25% the year after. Alas, like central bankers, the inflation swap market’s record is dreadful. In late spring of 2020, markets predicted a CPI of minus 1.35% a year later and staying below zero by the spring of 2022.

The US DollarInflation Swap is a poor predictor of inflation, at least under President Biden.

I’m not suggesting inflation will remain at current nosebleed levels. More likely is that having had a couple of decades of headline inflation that was on the low side — for central bankers, but not for anyone else — we are in for a few years when it remains above their targets.

Short rates will of course need to rise. That is problem enough for markets, but the bigger problem comes from the trillions of dollars of assets that central banks have accumulated on their balance sheets. Taken together, the Fed, ECB, Bank of Japan, Bank of England and Swiss National Bank have some $27 trillion of assets. In 2007, before the global financial crisis, the combined total was a little more than $4 trillion. Central bank assets will stop growing this year, undermining a major source of support for all types of bonds. But if inflation remains persistently high, central banks won’t simply be able to let their assets roll off as they mature, as most assume. They will have to start selling them. That is the big problem.

Central banks resorted to buying bonds and other financial assets (so-called quantitative easing) for a few reasons. The main one was to drive up inflation and inflation expectations from uncomfortably low levels by injecting more liquidity into the financial system and driving down longer-dated yields. Now that central banks have got much more inflation than they wanted, they will, by the equal and opposite token, need to sell the assets they bought. The longer inflation remains at current levels, the greater the pressure to sell. And they will probably need to do so sooner and faster than most expect and at prices a lot lower than they fetch today. The Fed alone owns about 30% of all the notes and bonds issued by the U.S. Treasury Department.

To say that central bank purchases have had a large effect on yields would be an understatement. One way of seeing this is to split the yield of a longer-dated bond into the part that reflects the expected path of interest rates over the life of the security from everything else. That “everything else” is the term premium. This should compensate investors for, say, sudden surges in inflation. Clearly, this is no longer true. Depending on what model you use, the term premium on 10-year Treasury reached a high of 450 basis points to 500 basis points in the early 1980s. At the nadir of the pandemic, it was minus 100 points and is now about minus 10 points. To be clear, this means that you get less buying a 10-year Treasury than would be suggested by the expected path of rates over the life of the bond — expectations that are almost certainly too low.

Term premiums below zero suggest bond investors are no longer compensated for things like inflation.

The driving down of government bond yields also compressed yields and spreads on investment-grade and junk bonds. That was the intent. Junk spreads reached their narrowest level ever in June of last year. With so little yield available in fixed income and central banks seemingly always on hand to bail them out, investors flooded into equities. As a result, many developed-world equity indexes are either very expensive or, in the case of the U.S., not far off their most expensive levels ever based on valuation measures that are a decent guide to future returns. That is what a decade and a half of market manipulation by central banks has done.

The policies of zero or negative rates and seemingly infinite QE looked idiotic (and were) when they were adopted, and time has not been kind. Paradoxically, they could only be sustained if central banks were wrong, and their policies failed to spark inflation. Now that inflation has taken hold, rates will go up substantially and balances sheets will need to shrink.

What would you pay for fixed-income assets now if you knew that central banks will become, in effect, forced sellers later? I can’t see how any financial asset will escape the damage from the likely lurch higher yields. The way out of these policies will be as nasty as the way in was nice.

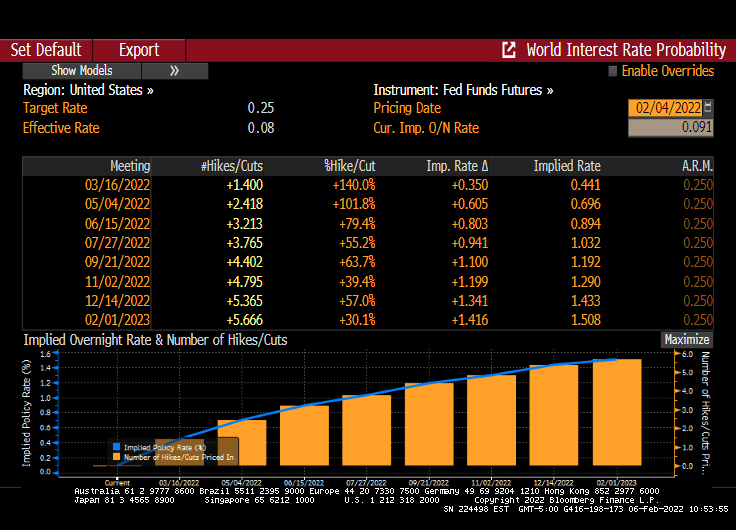

Particularly since Fed Funds Futures are pointing toward 6 rate increases over the next year.

At least Treasury Secretary Janet Yellen is wearing her Mao jacket.

Inflation is literally burning a hole though the pockets of Americans. The Flexible Price CPI is raging at 18% YoY. The Dallas Fed has their preferred measure of inflation, the trimmed mean CPI, is growing at only 3.05% YoY. The classic measure of inflation, CPI YoY, is growing at 7.12%.

That is of course if you can find things to buy at the grocery store.

I remember when Fleetwood Mac played at Bill Clinton’s first inauguration party. Perhaps Fleetwood Mac can play at the midterm election party commemorating the rampant inflation under Biden’s “leadership”: Bare Shelves.

How bad is inflation in the USA? Try 18%, based on the Flexible Consumer Price Index.

The Flexible Price Consumer Price Index (CPI) is calculated from a subset of goods and services included in the CPI that change price relatively frequently. Because flexible prices are quick to change, it assumes that when these prices are set, they incorporate less of an expectation about future inflation.

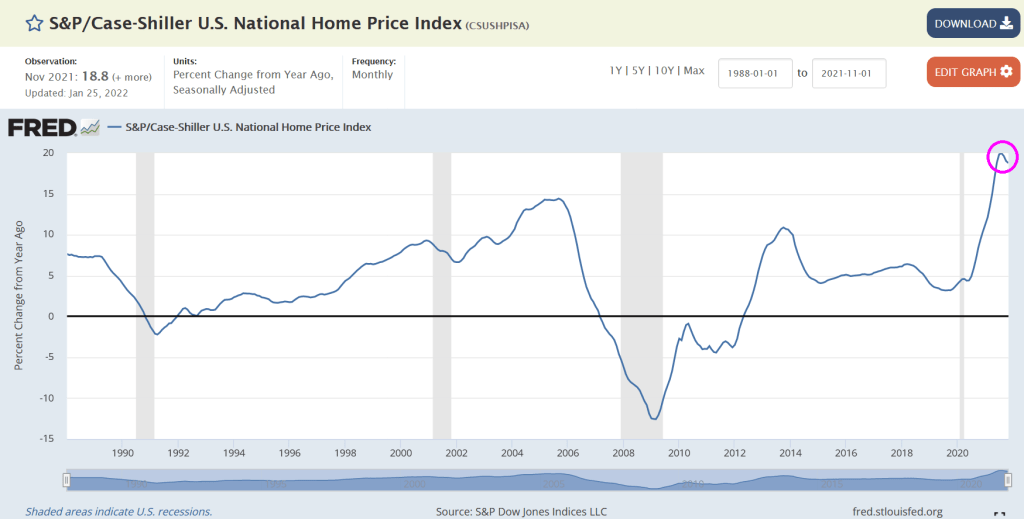

Again, remember that Federal inflation numbers woefully undercount housing and rent inflation. For example, the Case-Shiller National Home Price index (as of November 2021) was growing at 18.8%.

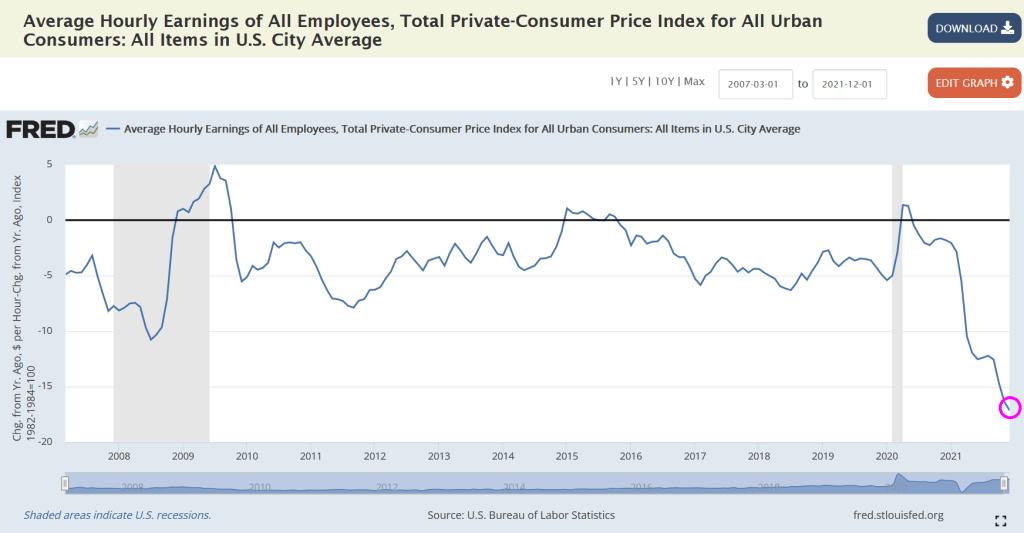

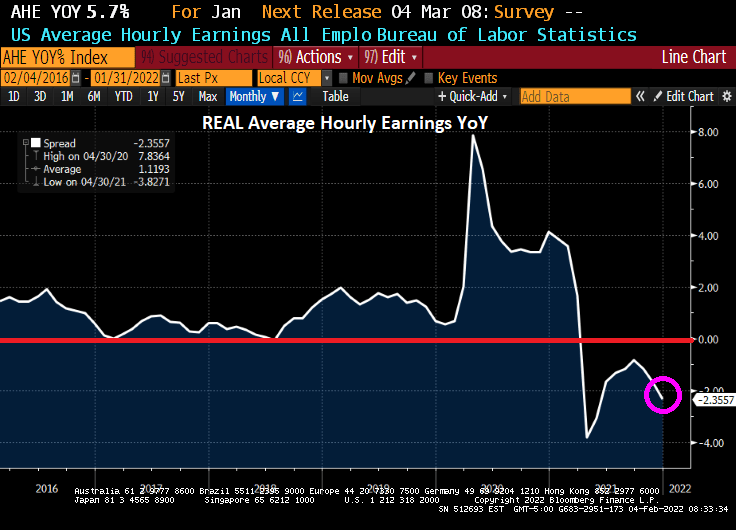

The sad part is that inflation-adjusted average hourly earnings growth of all employees is crashing thanks to inflation.

Well, the COVID hysteria from the Biden Administration and the media preparing us for a horrible jobs report was … incorrect. In fact, the January jobs report was “exceptional”. 467,000 jobs were added and average hourly earnings growth ROSE to 5.7% YoY.

The bad news? Thanks to surging inflation, REAL average hourly earnings growth YoY FELL to -2.36%.

Unemployment ROSE to 4.0% from 3.9% as more people dropped out of the labor force in January. On the bright side, labor force participation rate rose to 62.2% from 61.9%.

Leisure and hospitality employment (one of the most vulnerable to inflation) expanded by 151,000 in January, reflecting job gains in food services and drinking places (+108,000) and in the accommodation industry (+23,000).

The reaction in the bond market? US 10-year yields are up 6.9 basis points as Eurozone is up across the board.

Energy prices are up (except natural gas futures).

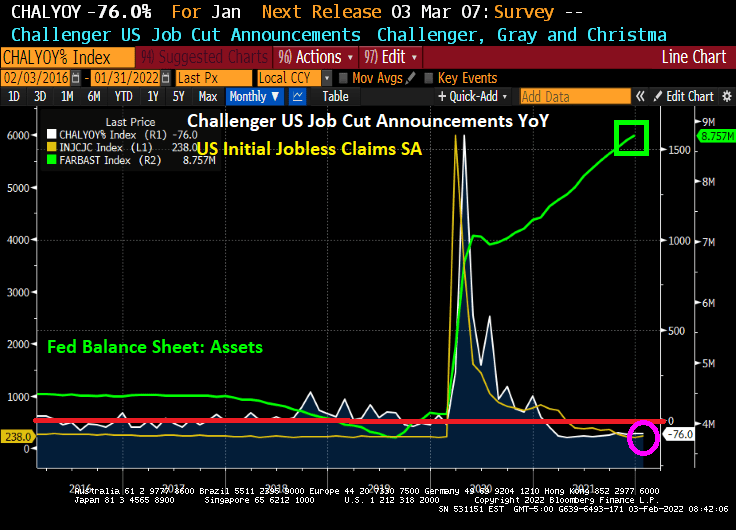

Between the Biden Administration, Anthony Fauci and the media constantly screaming about the devastating effects of Omicron, I would have expected massive job cuts and a large spike in jobless claims. But alas, the numbers and charts tell a different story.

Today, we saw that the Challenger job cuts for January fell further to 76%. Initial jobless claims fell to 236k. And The Federal Reserve is still hyper-stimulating the economy.

After listening to Biden spokesperson Jen Psaki preparing us for an end-of-times job report, I was expecting today’s news dump to be terrible. But alas, it just looks like another day in Stimulyoptoville.

Hey Jen, where’s the beef? Now that I think of it, Jen Psaki looks like Wendy from the burger franchise. Except that the burger Wendy doesn’t terrify people.

You must be logged in to post a comment.