California just did what Slow Joe Biden and Senate Majority Leader Chuckles Schumer are threatening to do. Biden and Schumer still refuse to negotiate (allegedly) sending the US Federal government careening towards a staggering debt default. The source of both California and US Federal government fiscal problems? Out of control government spending, aka, government gone wild!

Now we have the State of California defaulting on $18.6 BILLION in debt. This is Governor Gavin Newsom (Nancy Pelosi’s nephew) bragging point to be President? Horrible fiscal management and a default?

In any case, California borrowed approximately $20 billion from the federal government to cover unemployment benefits during the pandemic, and with Gov. Gavin Newsom’s recent decision to not pay it back, employers are now saddled with the expense, according to experts.

“The state should have taken care of the loans with the COVID money it received from the government in 2021,” Marc Joffe, policy analyst at the Cato Institute—a public policy think tank headquartered in Washington, D.C.—told The Epoch Times.

In the proposed 2023–2024 budget, $750 million was allocated to start paying down the loans, but Newsom made changes to the plan in January and withdrew the funding.

The Epoch Times’ request for comment from Newsom’s office was not returned on deadline.

The decision leaves businesses in the state responsible for the loans—as mandated by federal regulations—so the federal unemployment tax rate of .6 percent is set to increase by .3 percent annually, starting in 2023, until the loan is extinguished.

“California is just not really an employer-friendly state,” Joffe said. “This one thing will not be a difference between a business remaining open or closing, but it’s just another burden on top of the many burdens the state puts on employers.”

Twenty-two states borrowed money for unemployment insurance from the federal government during the pandemic, with all but four—California, Colorado, Connecticut, and New York—paying back their debts.

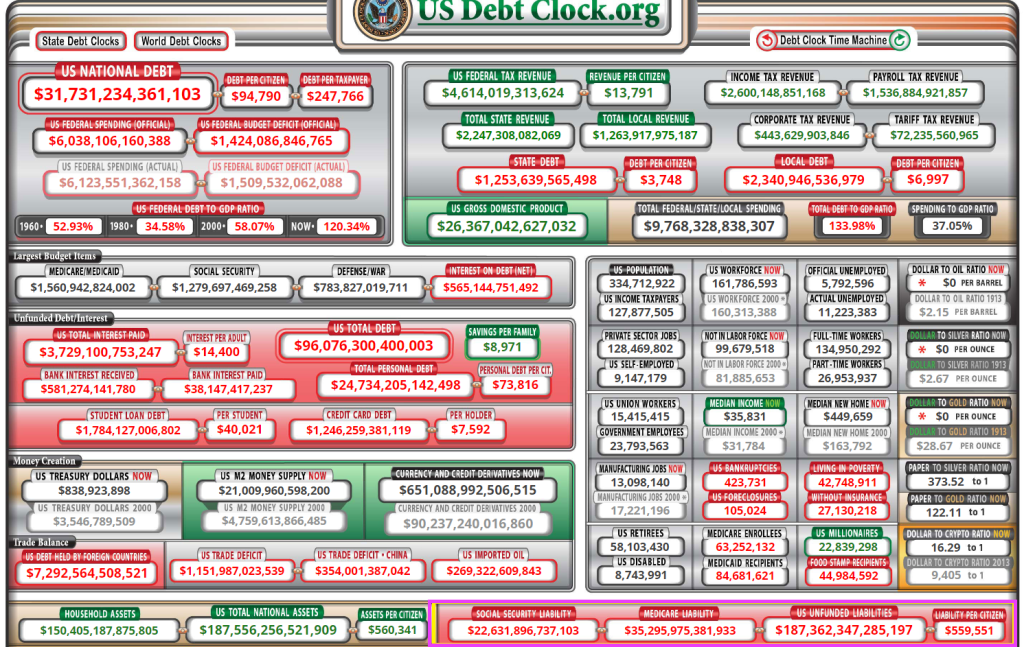

California owes the most, by far, with approximately $18.6 billion outstanding as of May 2, followed by New York’s $8 billion, Connecticut’s $187 million, and Colorado’s $77 million, according to U.S. Treasury Department data.

The discrepancy in amounts borrowed and owed by states lies in the different approaches to managing the pandemic, with California’s stricter lockdown causing unemployment to remain higher and longer, according to experts

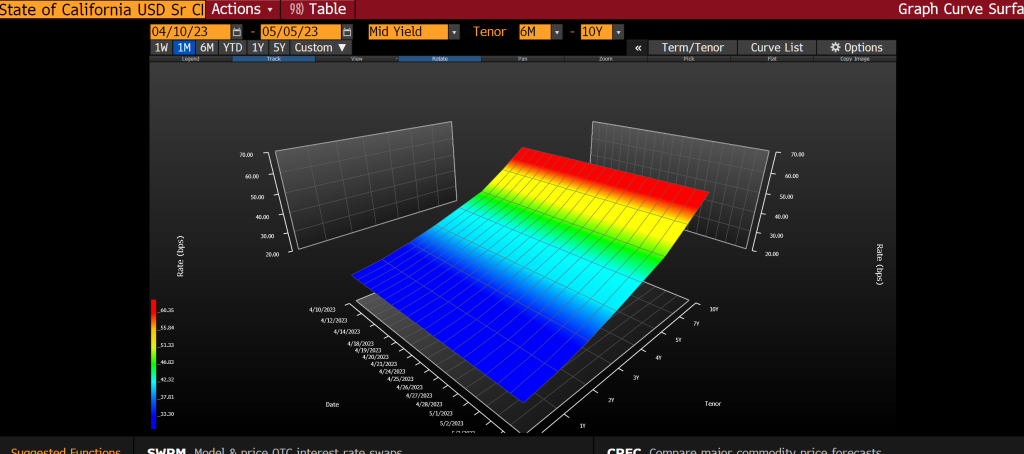

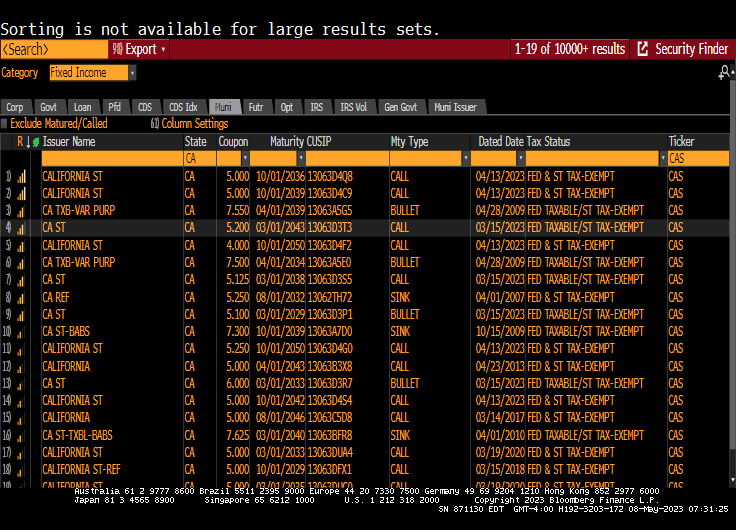

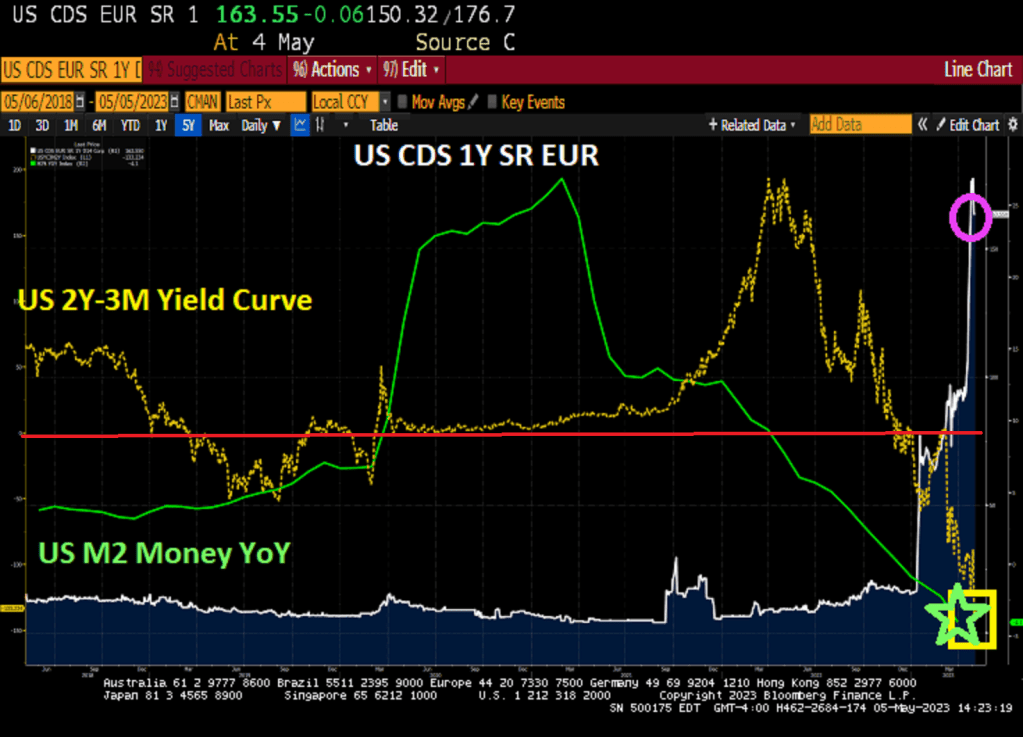

And CA CDS 1Y is tame (only 31), the CDS curve over a longer time frame looks miserable.

Now, Gruesome Newsom only default on Covid-related loans. The California municipal bond market is huge and CA has defaulted on those loans …. yet.

Speaking of insane fiscal “management,” a repartations plan in California could cost billions.

California’s reparations task force, which first convened nearly two years ago, has given the final approval to a list of recommendations on how the state may compensate and apologize to Black residents for historical discrimination.

“Reparations are not only morally justifiable, but they have the potential to address long standing racial disparities and inequalities,” Representative Barbara Lee (D-CA) said during a weekend meeting. The proposals now go to state lawmakers to consider reparations legislation and a final sum, which some economists could cost the state upwards of $800B, or almost 3x the state’s annual budget.

To be initially eligible, applicants must be a descendant of Black people who were in the country by the end of the 19th century, thouqh there are not yet details on how the payments would be funded. Age, state residence, and other factors will also play a role in determining compensation.

There is the rub – how does California finance the reparations? Raise taxes (unfair to people who never did anything wrong to blacks)? Borrow billions? Given that Newsom just defaulted on loans to California might mean that there will be relucatance to lend CA billions more.

CA Governor Gavin “Slick” Newsom. The Defaulter In Chief of California.

You must be logged in to post a comment.