Welcome to Boss Biden’s America! It reminds of woefully corrupt Boss Tweed and Tammany Hall in New York City. Today’s inflation report revealed that core CPI YoY was 4.7%. Ugh!

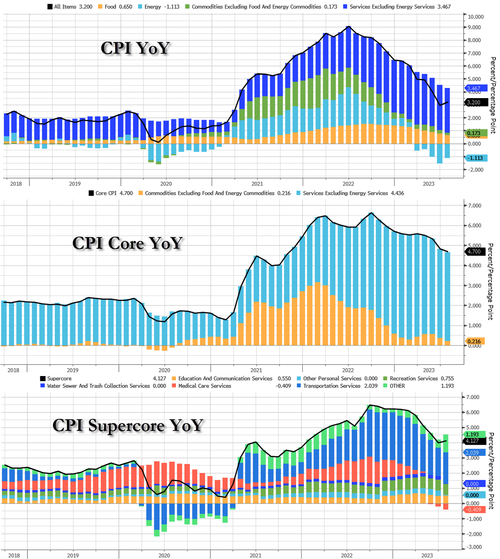

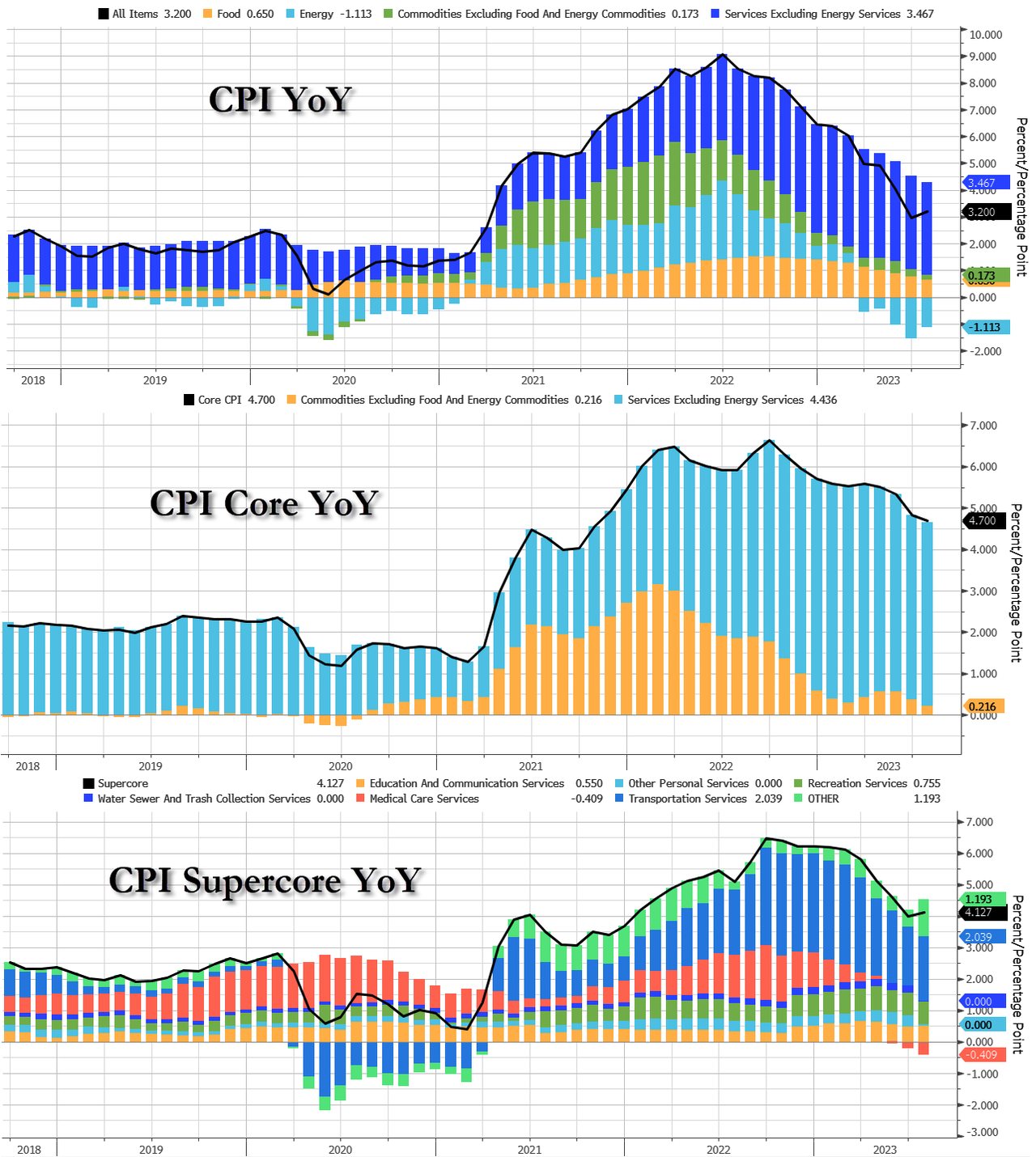

Expectations for this morning’s must-watch CPI print were for a MoM and YoY rise in the headline, and modest slowing of the core YoY. However, The Fed will be watching its new favorite signal – Core Services CPI Ex-Shelter – which reaccelerated in July (+0.2% MoM, and from +3.9% to +4.0% YoY).

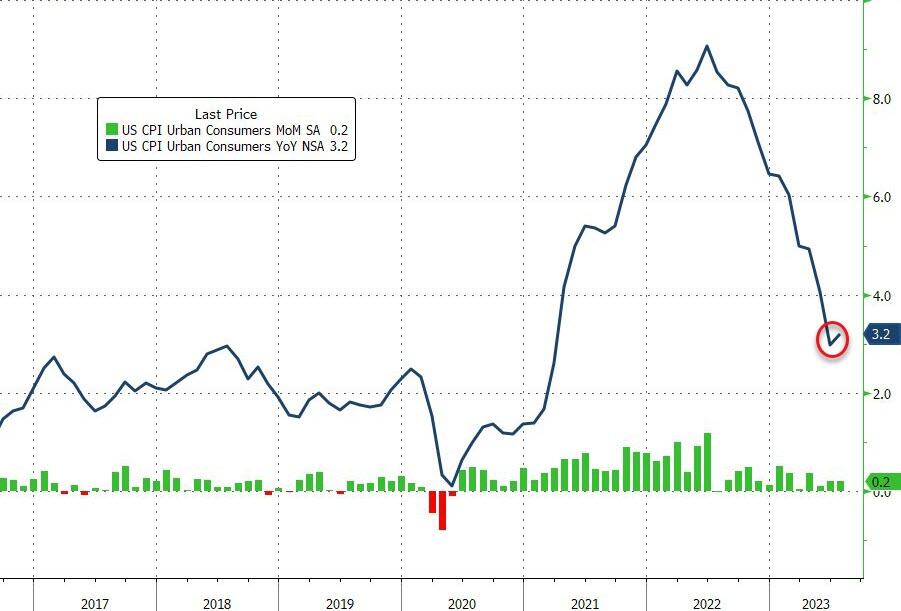

The headline CPI rose 0.2% MoM in July (as expected), the same as in June, pushing the YoY up to 3.2% (from 3.0% in June) but below the 3.3% expected…

Source: Bloomberg

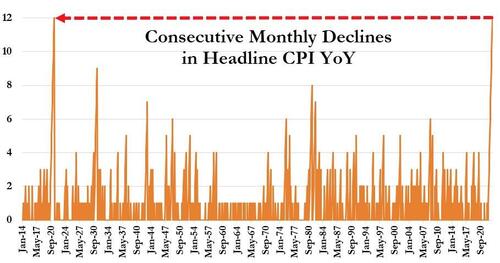

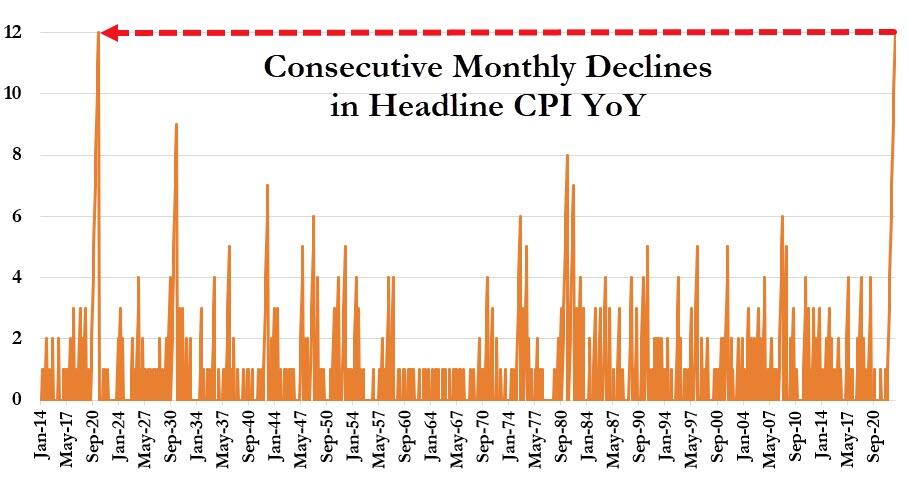

Today’s increase in CPI YoY broke the record-equaling streak of 12 straight months of declines.

Core CPI rose 0.16% MoM, with the YoY growth in prices slowing to 4.7%.

Source: Bloomberg

Both Goods and Services inflation (YoY) slowed in July – but Services remain extremely high at +6.1%…

Source: Bloomberg

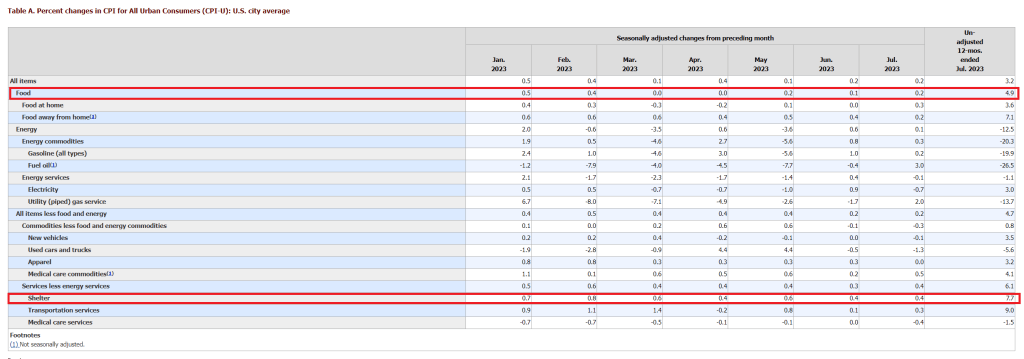

On an annual basis, the index for all items less food and energy rose 4.7% over the past 12 months with the shelter index rising 7.7% over the last year, accounting for over two-thirds of the total increase in all items less food and energy.

Other indexes with notable increases over the last year include motor vehicle insurance (+17.8 percent), recreation (+4.1 percent), new vehicles (+3.5 percent), and household furnishings and operations (+2.9 percent).

Source: Bloomberg

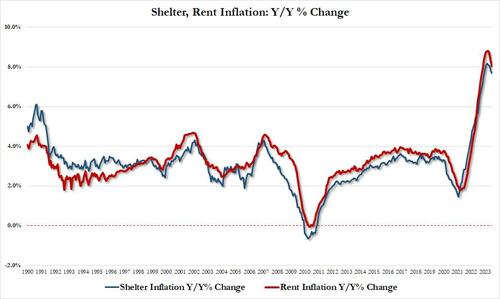

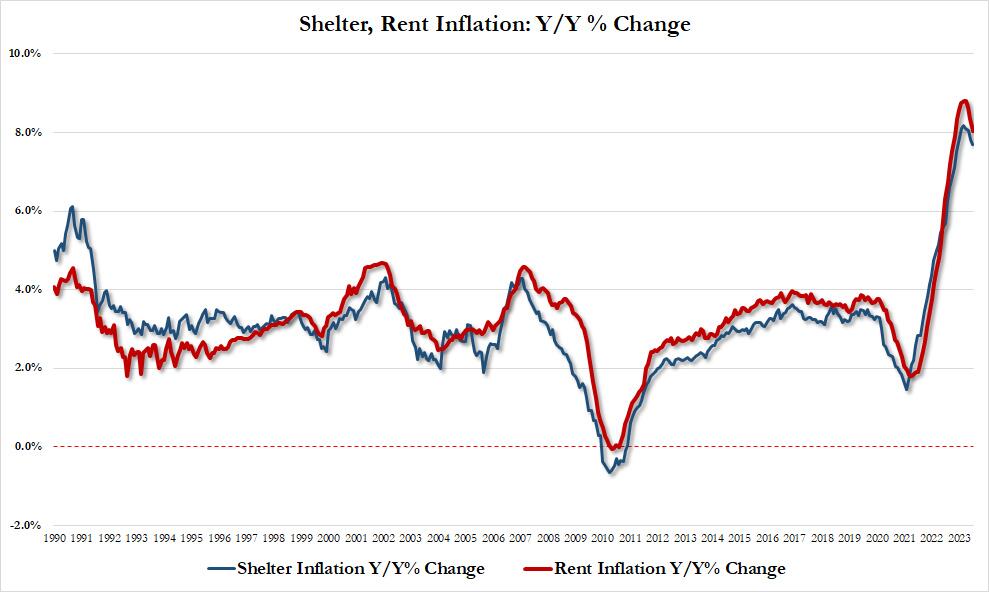

Taking a closer look at the all important shelter index, while it is still growing both sequentially and annually, the slowdown in growth is increasing more visible:

Shelter inflation up 7.69% YoY in July vs 7.83% in June, lowest since Dec 22; also up 0.43% MoM, lowest monthly increase since Jan 22

Rent inflation up 8.03% in July vs 8.33% in June, lowest since Nov 22; also up 0.41% MoM, lowest since March 22

The silver lining here, as noted by former Fed staffer Julia Coronado, is that “we are seeing core inflation slow before the expected big step down in rent/oer” which is great news as “lots of price sensitivity in travel and core goods that was slow to take hold but is now fully coming through.” In other words, if and when rent/shelter inflation actually post a decline (with the usual 12-18 month BLS lag), the Fed will be scrambling to fight inflation.

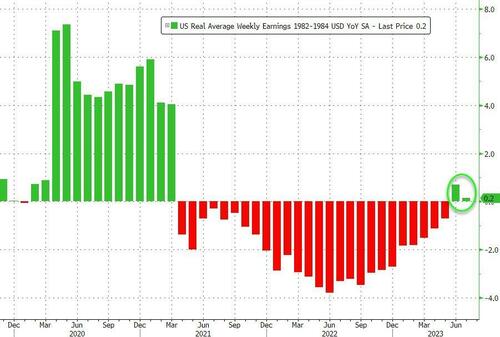

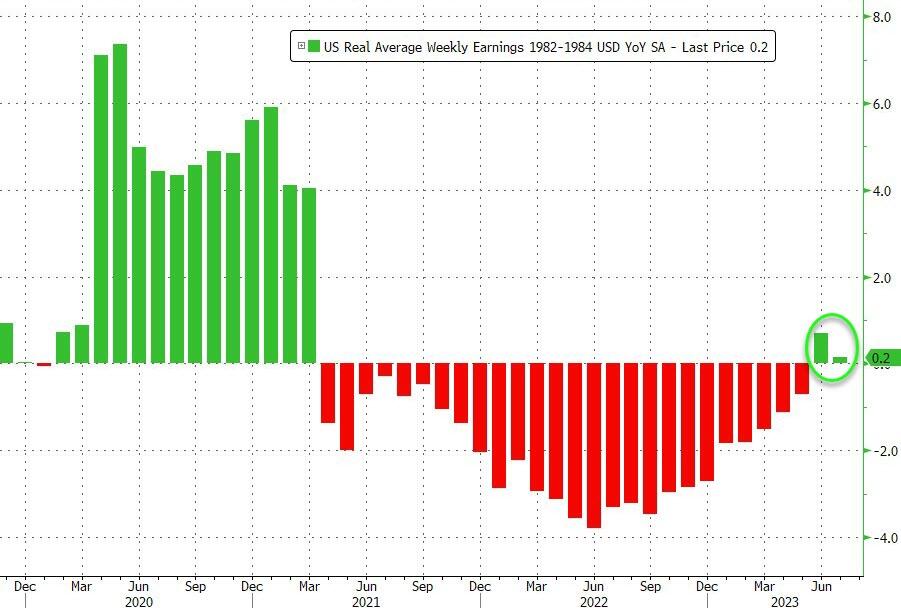

Turning to the wage aspect, for the second month in a row, ‘real’ wages rose YoY in July (but barely, +0.2%), and it appears that we are about to dip back into real contraction next month.

Source: Bloomberg

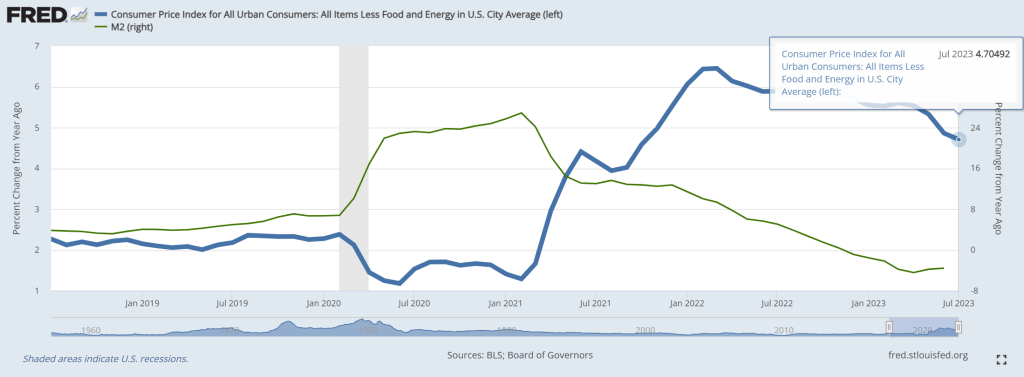

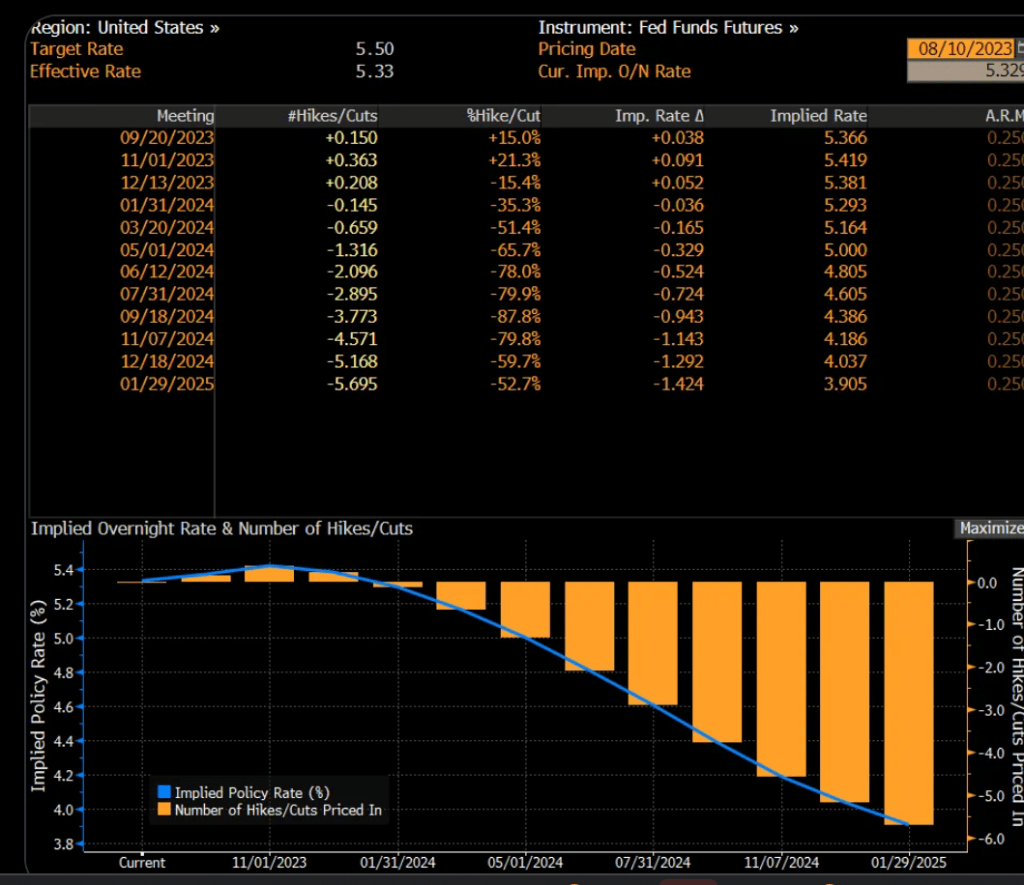

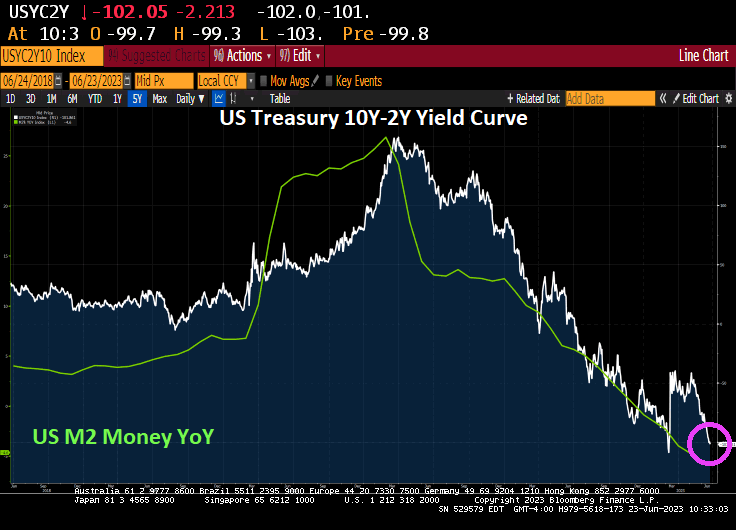

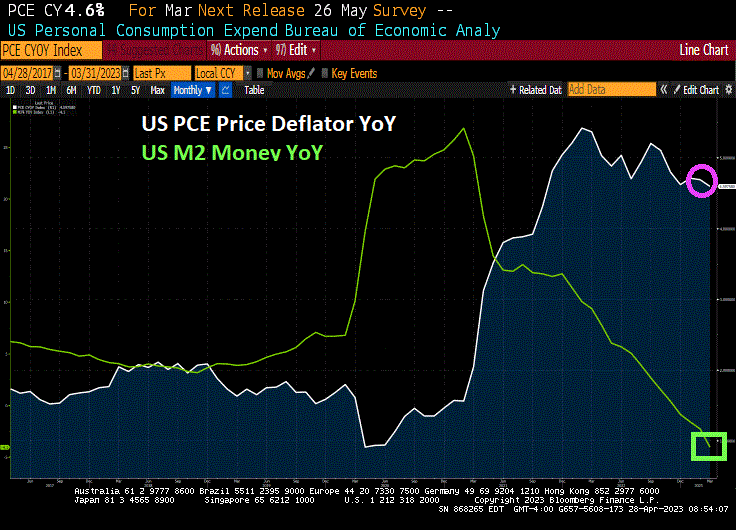

So the question becomes – is this an inflection point in inflation? (or is M2 still leading the way?)

Source: Bloomberg

Yet, Fed Funds Futures are pointing to no further Fed rate hikes.

With House Republicans releasing bank records showing over $20 million in payments to Biden family, associates, and Democrats denying any wrongdoing, I think we are seeing the Biden Administration as a rebirth of New York City’s Tammany Hall corrupt political machine led by Boss Tweed. Since Biden’s malfeasance/influence peddling occurred when he was Vice President under Barack Obama (aka, Barry Soetoro), Obama is the new Bathhouse John Coughlin the woefully corrupt Chicago Alderman and Hunter Biden is the new Hinky Dink (Michael Kenna, also a woefully corrupt Chicago Alderman).

Bathhouse Barry Soetoro, Boss Biden and Hinky Hunter at a basketball game.

When I see the faces of Alan Greenspan, Ben Bernanke, Janet Yellen and Jerome Powell, all I think of is …. the Minsky Moment brigade!

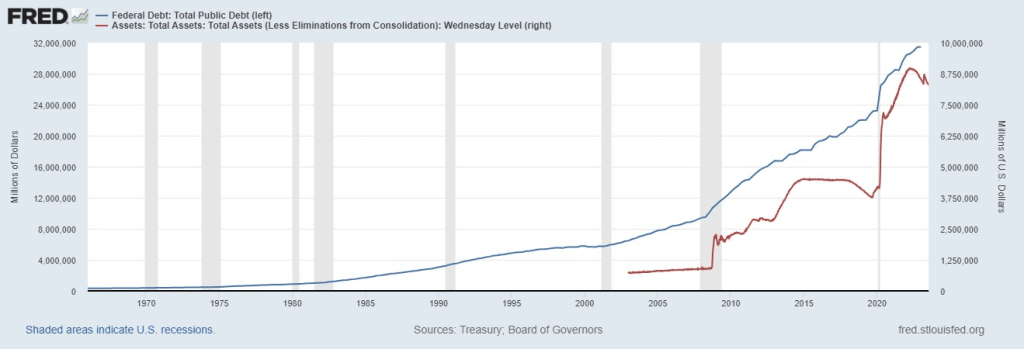

From Zero debt in 1776 to $21 trillion in 1997 and just in the last 4 years, debt has gone up by that same $21 trillion. This graph shows the debt explosion, a 63x increase.

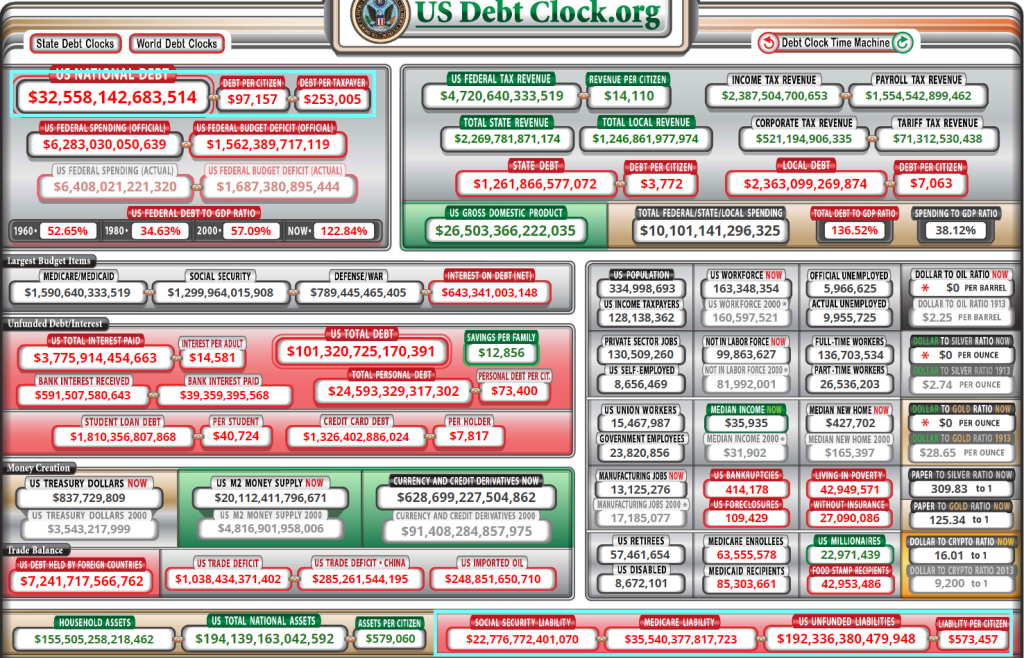

And then we have Congress promising >$192 trillion in entitlements (wealth transfers) that will likley be added to the already >$32 trillion in Federal debt.

Joe Biden, or “Blow Biden” after the cocaine was discovered in the White House the other day, owns the abysmal mortgage and housing market thanks to The Fed fighting inflation caused by Bidenomics (massive Federal spending and massive Fed stimulus).

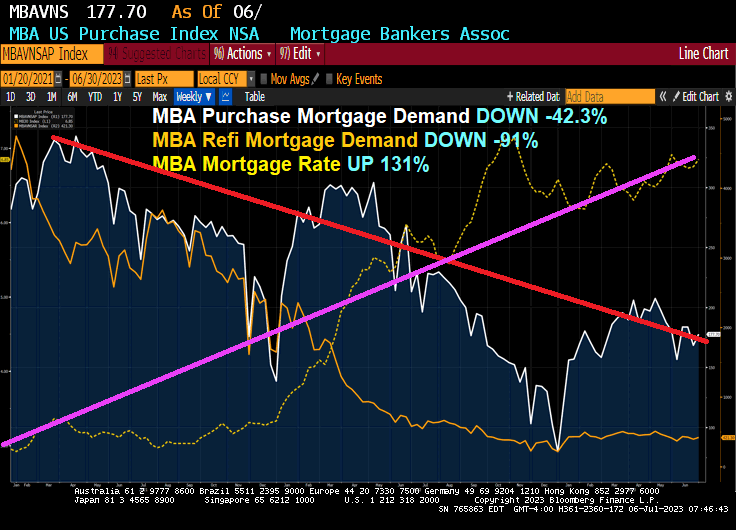

Mortgage applications decreased 4.4 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 30, 2023. Last week’s results included an adjustment for the Juneteenth holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 4.4 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 6 percent compared with the previous week. The Refinance Index decreased 4 percent from the previous week and was 30 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. The unadjusted Purchase Index increased 6 percent compared with the previous week and was 22 percent lower than the same week one year ago.

Here is the rest on the story:

As liquidity dries up under Bidenomics. Or Yellenomics. Take your pick!

Seriously, can The Biden Administration get any more embarrassing? Or dangerous to American civil liberties?

The US is Living La Vida Biden (living the Biden life!) Which means you are making millions if you are a political elite, but suffering if you live on Main Street.

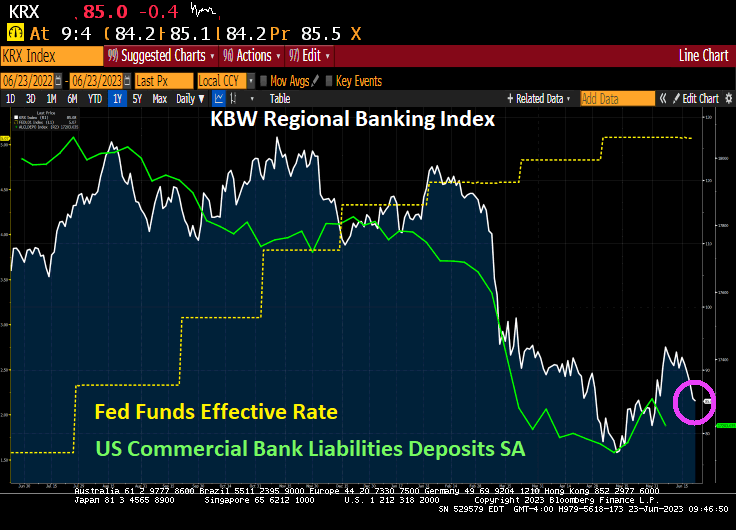

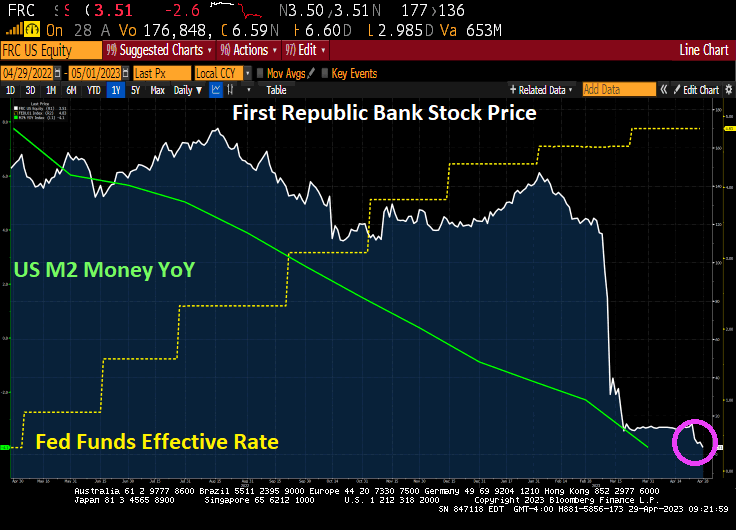

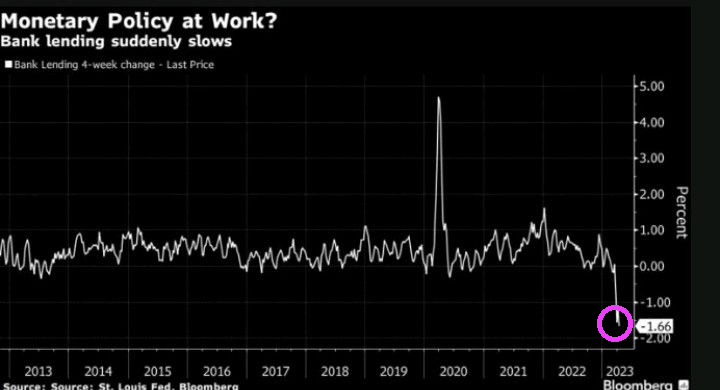

And regional banks (not the TBTF national banks) continue to suffer. The Bank Term Funding Program (1 of 2) is skyrocketing as The Fed cranks up rates to fight BidenFedflation (a combination of excessive monetary stimulus by The Fed and Biden’s lousy economic policies) and M2 Money growth crashes.

The regional banking index continues to fall as bank deposits shrink (like me when I used to jump in the Pacific Ocean in Santa Cruz).

Cryptos down this morning. But Bitcoin is above $30,000 … again.

Oil is down this morning but gold and silver are up slightly.

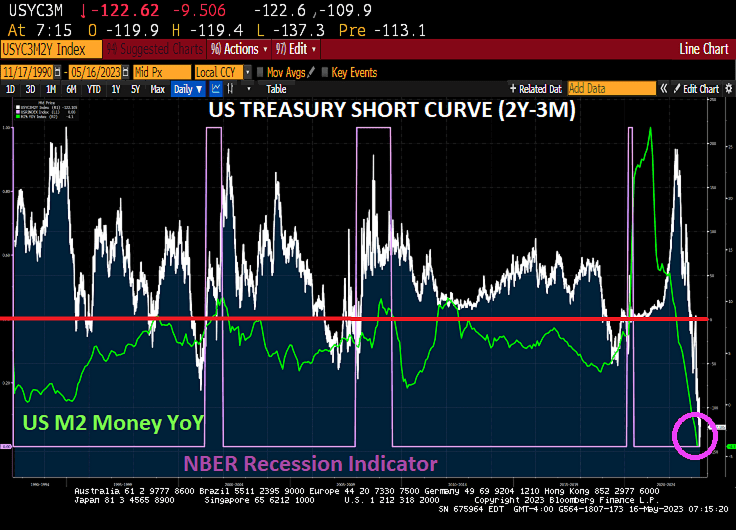

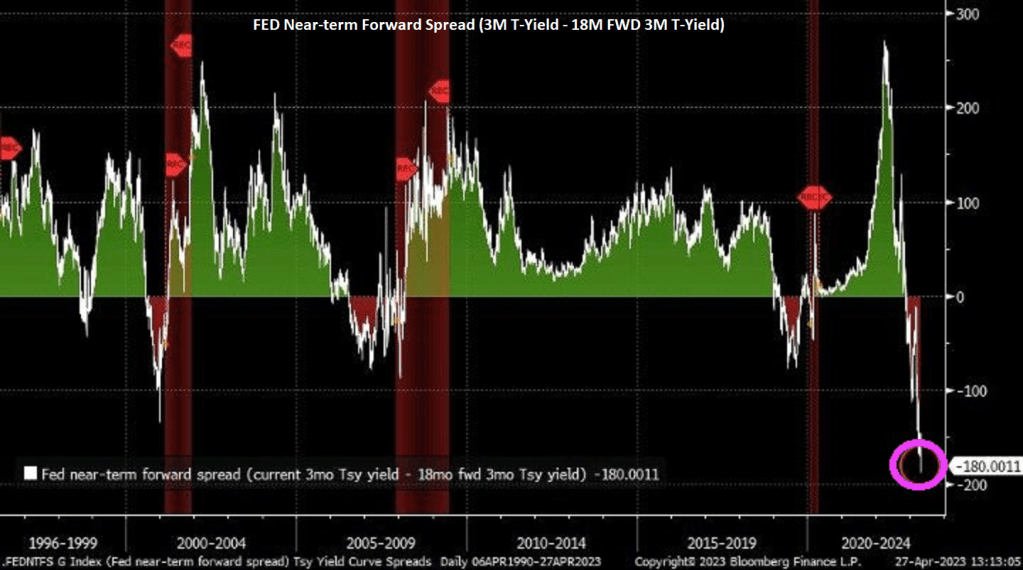

The 10Y-2Y US Treasury yield curve just dipped below -100 basis points (steep inversion) as M2 Money growth crashed and burned.

Between work at home, Bidenflation and The Feral Reserve, commercial real estate and regional banks are suffering … and it could get a lot worse. And Joe Biden (aka, Negan) in general. Living in Negan Country!

The work-from-home trend has been taking its toll on office landlords and is now making its way through to banks’ commercial loan portfolios, leading some analysts to predict that more trauma could be on the way for regional banks this year.

And in the current climate of bank failures, short sellers, and nervous depositors, banks with large exposures to commercial real estate (CRE) loans are racing to clean up and sell down their loan portfolios in hopes that they will not fall victim to another round of bank runs.

“There is an estimated $1.5 trillion of commercial property debt that will be due for repayment in about 18 months,” Peter Earle, an economist at the American Institute for Economic Research, told The Epoch Times. “It’s not improbable that even if interest rates have fallen by that time, some of that real estate debt will nevertheless be impaired and have an adverse impact on regional banks.”

In step with a recent trend in the CRE market, tech giant Google announced in May that it was attempting to sublease 1.4 million square feet of vacant office space in its Silicon Valley home base in order to “match the needs of our hybrid workforce.” Despite more employees returning to their offices this year, average office occupancy rates across the United States are still below 50 percent.

According to a report by Bank of America, 68 percent of CRE loans are held by regional banks. Approximately $450 billion in CRE loans will mature in 2023. JPMorgan Chase estimated that CRE loans comprise, on average 28.7 percent of the assets of small and regional banks, and projected that 21 percent of CRE loans will ultimately default, costing banks about $38 billion in losses.

Double Hit (of Biden’s Policies) Commercial mortgages are getting hit on two fronts: first, by the lack of demand for office space, leading to credit concerns regarding landlords, and second, by interest rate hikes that make it significantly more expensive for borrowers to refinance.

According to a June 12 report by Trepp, a CRE analytics firm, CRE loans that were originated a decade ago, when average mortgage rates were 4.58 percent, are now coming due, and in today’s market, fixed-rate CRE loan rates are averaging around 6.5 percent.

Banks that make CRE loans consider factors like debt service coverage ratios (DSCRs), which measure a property’s income relative to cash payments due on loans. Simulating mortgage interest rates from 5.5 percent to 7.5 percent, Trepp projected that between 28 percent and 44 percent, respectively, of currently outstanding CRE loans would fail to meet the 1.25 DSCR ratio today, and thus be ineligible for refinancing.

These calculations were done assuming current cash flows from properties stay the same and that loans are interest-only, but with vacancies rising, many landlords may have substantially less cash flow available. In addition, whereas interest-only CRE loans were 88 percent of the market in 2021, lenders are now switching to amortizing mortgages to reduce risk, which significantly increases debt service payments.

Refinancing Issues Fitch, a rating agency, projected that approximately one-third of commercial mortgages coming due between April and December of this year will be unable to refinance, given current interest rates and rental income.

“It’s a very different world now from the one in which the majority of these loans were made,” Earle said. “In a zero-interest-rate environment, before the COVID lockdowns saw many businesses shift to a remote work basis, many of these loan portfolios full of office properties looked great. Now, a substantial portion of them look quite vulnerable.”

The Trepp report highlighted several regional markets, such as San Francisco, where office sublease offers jumped 140 percent since 2020, and Los Angeles, where office vacancies hit a historic high of 22 percent. Available office space in Washington D.C. increased to 21.7 percent in the first quarter of 2023.

New York has been hit hard, as well. Office occupancy rates in New York City plummeted from 90 percent to 10 percent in 2020 during the COVID pandemic, but only recovered to 48 percent this year. Revenue from office leases fell by 18.5 percent between December 2019 and December 2022.

Vacancy Rates at 30-Year High Overall, according to a report by analysts at New York University and Columbia Business School, office vacancy rates are at a 30-year high in many American cities.

The report found that “remote work led to large drops in lease revenues, occupancy, lease renewal rates, and market rents in the commercial office sector.”

The authors predict that, even if office occupancy returns to pre-pandemic levels, “we revalue New York City office buildings, taking into account both the cash flow and discount rate implications of these shocks, and find a 44% decline in long run value. For the U.S., we find a $506.3 billion value destruction.”

As predicted, delinquencies in commercial mortgage loans are now creeping up. Missed payments in commercial mortgage-backed securities (CMBS) increased half a percent in May over the prior month to 3.62 percent, Trepp reports. The worst component of the CMBS market, which includes multi-unit rental buildings, medical facilities, malls, warehouses, and hotels, was offices, where delinquencies increased 125 basis points to more than 4 percent.

To put this in perspective, however, CMBS delinquencies exceeded 10 percent in 2012 and 2020. And analysts say that lending criteria for CRE have been more conservative than they were before the mortgage crisis of 2008, leaving more cushion on ratios relative to a decade ago.

All the same, the credit crunch at regional banks has created a vicious circle, where banks race to pare down their CRE portfolios, and the dearth of financing leaves more landlords facing default as outstanding loans mature. To make matters worse, commercial property values, which provide collateral for the loans, appear to be taking a hit as well.

In an effort to rapidly clean up their CRE loan portfolios and avoid the fate of failed banks like Silicon Valley Bank, Signature Bank, and First Republic Bank, banks are now attempting to sell off the loans, often taking a loss in the process.

In May, PacWest, a regional bank, sold $2.6 billion of construction loans at a loss. Citizens Bank reportedly has put $1.8 billion of its CRE loans up for sale during the first quarter of this year. Customers Bancorp reduced its CRE lending by $25 million and put $16 million of its existing portfolio up for sale.

Wells Fargo, one of the top four largest U.S. banks, is also downsizing its CRE portfolio, and in announcing the move CEO Charlie Scharf stated, “we will see losses, no question about it.”

“Between the Fed’s 500+ basis point hikes over the past 16 months and the failure of Silicon Valley Bank, and others, earlier this year, a credit tightening is already underway,” Earle said. “That has put a lot of pressure on regional lenders.”

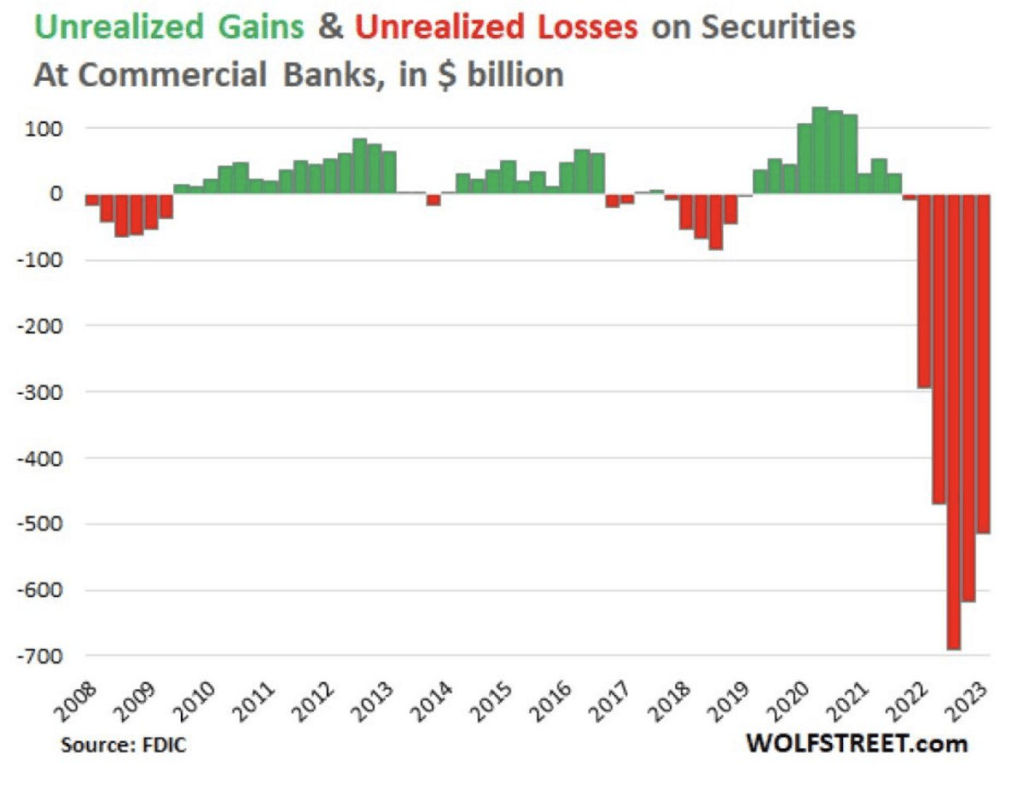

A March academic study titled “Monetary Tightening and U.S. Bank Fragility in 2023” stated that the market value of assets held by U.S. banks is $2.2 trillion lower than what is reported in terms of their book value. This represents an average 10 percent decline in the market value of assets across the U.S. banking industry, and much of this decline came from commercial real estate loans.

Consequently, the authors wrote, “even if only half of uninsured depositors decide to withdraw, almost 190 banks with assets of $300 billion are at a potential risk of impairment, meaning that the mark-to-market value of their remaining assets after these withdrawals will be insufficient to repay all insured deposits.”

The US economy was sitting high on the global mountain top before Covid. Then Covid struck, The Federal Reserve and Congress went wild with stimulus spending and inflation went wild. This is Biden Country, a feeble shell of this once great nation.

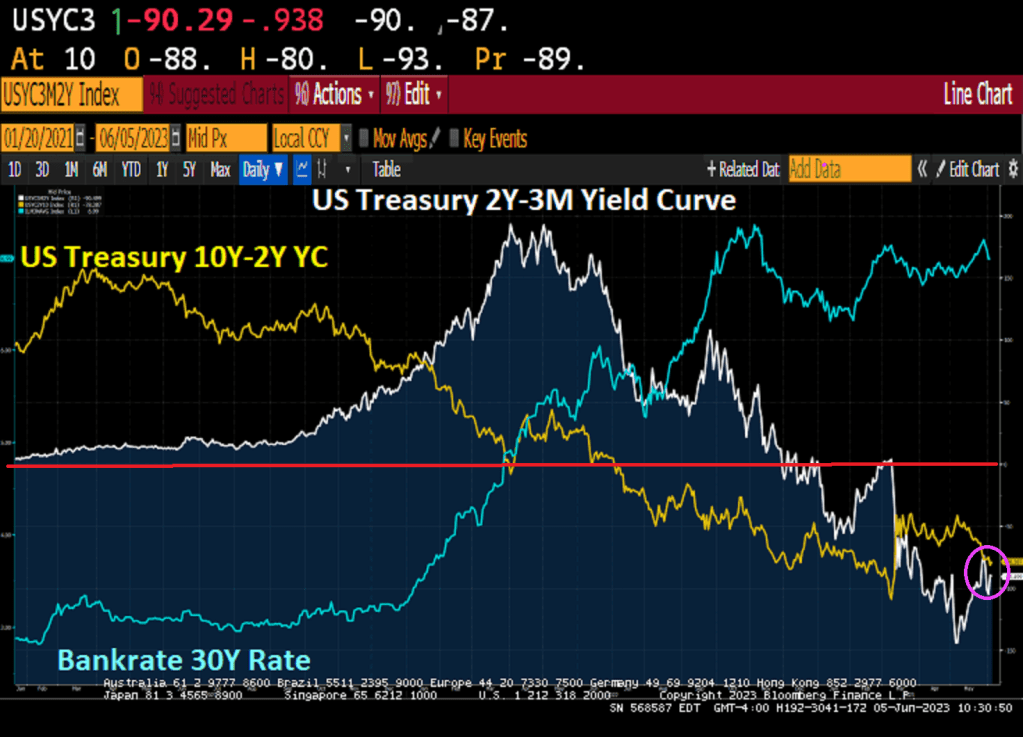

As The Fed tries to counter the years of excess monetary stimulus pre and post Covid by raising rates, we have seen mortgage rates rise 143% under Biden’s leadership. At the same time, the US Treasury yield curves (short 2Y-3m and long 10Y-2Y) remain deeply inverted.

As of this AM, The Fed Funds Futures market is pricing in a chance of continued rate hikes by The Fed, but mostly we are at 5.25% at least until November when rates are forecast to begin declining.

And the Taylor Rule is still signaling rate hikes to 10.12%. We are at only 5.25%. And with Biden feebily running for reelection, the only path forward is rate CUTS.

I used to think that The Kabuki Theater surrounding the raising of the US debt limit and passing a Federal budget would be over by now. But since Biden is being controlled by the hard left “Progressives” in Washington DC, he may be reckless enough to let the US default just so he can blame Republicans. And with our useless and deeply-biased main street media (MSM) just repeating Democrat talking points blaming Republicans, we may actually see a US debt default.

So while Yellen is warning that time is running out, notice she never encourage Blaming Biden to negotiate his insane budget downwards, we see a deeply inverted US Treasury short curve (2Y-3M).

(Bloomberg) Treasury Secretary Janet Yellen warned that “time is running out” to avert an economic catastrophe from failing to raise the debt ceiling, in remarks released as President Joe Biden and congressional leaders prepared to meet on the standoff.

Speaker Kevin McCarthy issued his own notice Monday evening ahead of Tuesday’s 3 p.m. gathering, saying, “We only have so many days left to deal with this.”

The two sides showed little signs of agreeing on much else other than the countdown in the runup to the second White House encounter on the debt ceiling in two weeks. While senior staff have been negotiating for days, Republicans are still pressing for sweeping spending cuts, while Democrats are determined to protect the president’s legislative achievements.

“We are already seeing the impacts of brinksmanship: investors have become more reluctant to hold government debt that matures in early June,” Yellen said in remarks prepared for delivery to a banking conference on Tuesday. “The impasse has already increased the debt burden to American taxpayers.”

The Treasury chief issued a fresh letter to congressional leaders Monday restating that the Treasury risks running out of sufficient cash for all federal obligations as soon as June 1. The livelihoods of millions of Americans “hang in the balance,” she said in excerpts of her speech to the Independent Community Bankers of America Capital Summit released by the Treasury.

There is the evil Hobbit! Sending a letter to Congress essentially blaming McCarthy for the fiasco when Biden could downsize his budget request to reasonable levels. But Yellen is an authoritarian Statist, not a free market type.

March’s Personal Consumption Expenditures Core Prices remain HOT despite The Fed crashing M2 Money growth. PCE Core price growth remained elevated at 4.6%.

Personal spending in March slowed to 0% growth.

The Taylor Rule infers a Fed Funds target rate of 10.27% Alas, we will never get there.

To show you how Yellen/Powell’s Too Low For Too Long (TLFTL) monetary polices coupled with Biden/Pelosi/Schumer’s (add McConnell to this foul-smelling witches’ brew), Powell and The Gang (aka, The Fed) slammed on the monetary brakes. On a year-over-year basis, M2 Money growth has crashed tl -3.13%. The shocking number is The Fed Fund Effective Rate which rose over 5,000% YoY.

Actually, the US has been on a money printing spree since 1995, but it was Covid spending and monetary expansion in 2020 that crushed M2 Money Velocity (GDP/M2).

Here is Supernatural’s Leviathan monster Dick Roman handing an award to sparkless President Joe Biden. But Biden did spark massive inflation that crushed the US middle class and low wage workers.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.