Too much debt! US politicians are spending too much money and borrowing too much. Unfortunately, that is what Biden and Bidenomics is all about: Federal targeted spending and loads of debt.

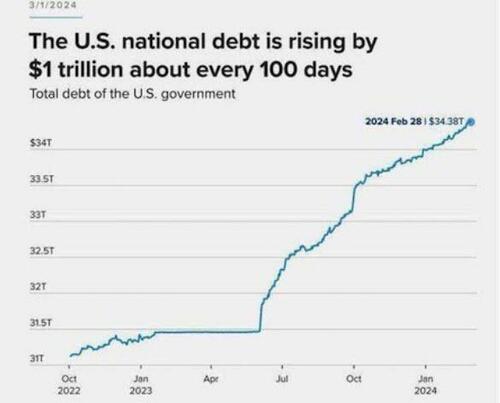

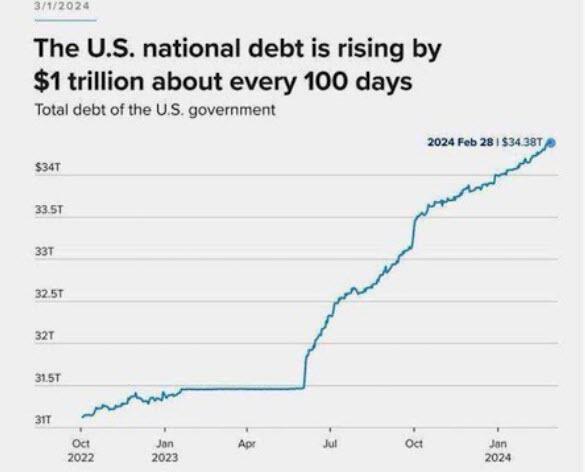

Now it requires $1 trillion of new debt every 100 days to achieve nothing but remaining static economically. The regime media pundits and the cabal on Wall Street tell us the economy is doing great. No recession in sight. All is well. The dumbed down and distracted ignorant masses don’t realize all the reported “economic growth” is “created” by the government, enabled by The Fed, spending billions on their wars in Ukraine and the Middle East, funneling the money into the Military Industrial Complex corporations; paying for the transportation, feeding, and housing of the illegal invading hordes; hiring more government drones to harass the citizenry, and desperately trying to prop up a corrupt tottering empire in its final death throes.

Anyone with even the slightest mathematical acumen knows increasing the national debt at a rate of $1 trillion every 100 days is a death wish. Why would those pulling the strings behind the scenes of this acceleration towards the cliff of national suicide be doing so at this point in time? It’s almost as if the November elections are a deadline for them to complete their exit strategy plan.

I believe we are entering the Great Taking phase of this clown show.

They are purposely creating a global financial disaster in order to take everything you and I have. It sounds crazy, but so is adding $1 trillion of debt every 100 days.

First, online shopping has crushed retail commercial space. Second, crime is rampant in The Big Apple. A slowing economy is contributing to the malaise in commercial real estate (CRE).

According to Bloomberg, Canadian pension funds – which until recently had been among the world’s most prolific buyers of real estate, starting a revolution that inspired retirement plans around the globe to emulate them because, in the immortal words of Ben Bernanke, Canadian real estate prices never go down…

Canada Pension Plan Investment Board has recently done three deals at deeply discounted prices, selling its interests in a pair of Vancouver towers, and a business park in Southern California, but it was its Manhattan office tower redevelopment project that shocked the industry: the Canadian asset manager sold its stake for just $1. The worry now is that such firesales will set an example for other major investors seeking a way out of the turmoil too, forcing a wholesale crash in the Manhattan real estate market which until now had managed to avoid real price discovery.

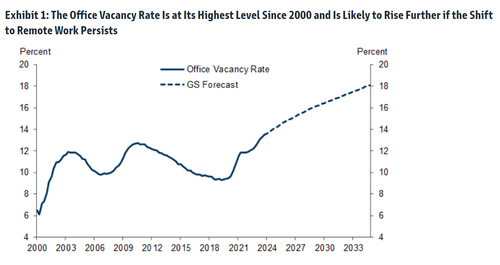

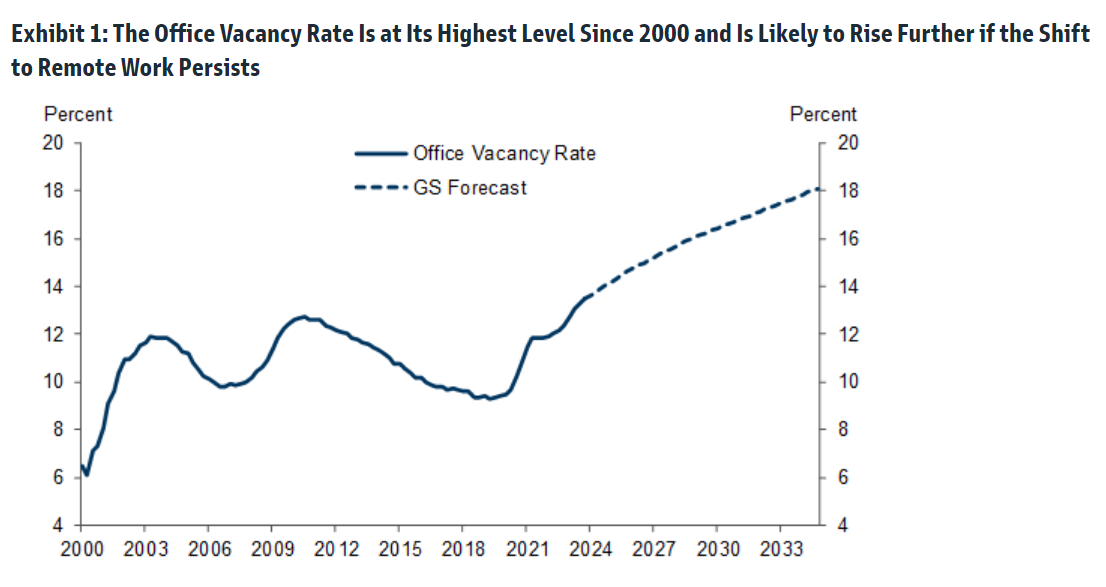

Indeed, as Goldman wrote earlier this week, while office vacancy rates are expected to keep rising well into the next decade..

… the average price of many nonviable offices has fallen only 11% to $307/sqft since 2019 (left side of Exhibit 6). The bank goes on to note that in the hardest-hit cities, as many as 14-16% of offices may no longer be viable, and their average transaction prices have already declined by 15-35%. However, because of lack of liquidity in this market, these recent transaction prices have not yet started to reflect the current values of many existing offices. Goldman ominously concludes that “alternative valuation methods, like those that are based on repeat-sales and appraisal values, suggest that actual office values may be far lower than the average transaction price.” Well, a $1 dollar price would certainly confirm that actual office values are far, far lower (more in the full Goldman note available to professional subscribers).

And going back to the historic firesale, at the end of last year the Canadian fund sold its 29% stake in Manhattan’s 360 Park Avenue South for $1 to one of its partners, Boston Properties, which also agreed to assume CPPIB’s share of the project’s debt. The investors, along with Singapore sovereign wealth fund GIC Pte., bought the 20-story building in 2021 with plans to redevelop it into a modern workspace.

360 Park Avenue South

“It’s the opposite of a vote of confidence for office,” said John Kim, an analyst tracking real estate companies for BMO Capital Markets. “My question is, who could be next?”

As office building anxiety has swept the financial world, as the persistence of both remote work and higher borrowing costs undercuts the economic fundamentals that made the properties good investments in the first place, a wave of banks from New York to Tokyo recently conceded that loans they made against offices may never be fully repaid, sending their share prices plunging and prompting fears of a broader credit crunch.

But the real test will be what price office buildings actually trade for – especially once the hundreds of billions of loan backing the properties mature….

…. and until now there have been precious few examples since interest rates started rising. That’s why industry-watchers see such shocking liquidations like CPPIB’s as a very ominous sign for the market.

The Manhattan firesale isn’t the pension fund’s first sale: last month, CPPIB sold its 45% stake in Santa Monica Business Park, which the fund also owned with Boston Properties, for $38 million. That’s a discount of almost 75% to what CPPIB paid for its share of the property in 2018. The deal came just after the landlords signed a lease with social media company Snap that required they spend additional capital to improve the campus, Boston Properties Chief Executive Officer Owen Thomas said on a conference call.

Peter Ballon, CPPIB’s global head of real estate, declined to comment on the recent deals, but said the fund has continued to invest in office buildings, including a recently completed, 37-story tower in Vancouver.

“Selling is an integral part of our investment process,” Ballon said in an emailed statement. “We exit when the asset has maximized its value and we are able to redeploy proceeds into higher and better returns in other assets, sectors and markets, including office buildings.”

As Bloomberg notes, the pension fund isn’t actively backing away from offices, but it’s not looking to increase its office holdings either. And where a property requires additional investment, CPPIB might simply look to sell so it can put that cash somewhere it can get higher returns instead, said the person, who asked not to be identified discussing a private matter.

CPPIB’s C$590.8 billion ($436.9 billion) fund is one of the world’s largest pools of capital, and its C$41.4 billion portfolio of real estate — stretching from Stockholm to Bengaluru — includes almost every property type, from warehouses, to life sciences complexes, to apartment blocks.

While that scale would mitigate any potential losses from individual transactions, it also means even a small shift in CPPIB’s office appetite has the power to cause ripple effects in the market.

While the 360 Park liquidation may be shocking, it’s just the first of many: with hybrid work schedules set to depress demand for office space in the long term, and higher interest rates increasing the cost of the constant upgrades needed to attract and keep tenants, even the best office buildings may not be able to compete with investment opportunities elsewhere.

“To get even better returns in your office investment you’re going to have to modernize, you’re going to have to put a lot more money into that office,” said Matt Hershey, a partner at real estate capital advisory firm Hodes Weill & Associates. “Sometimes it’s better to just take your losses and reinvest in something that’s going to perform much better.”

Mortgage applications decreased 5.6 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending February 23, 2024.

The Market Composite Index, a measure of mortgage loan application volume, decreased 5.6 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 3 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was12 percent lower than the same week one year ago.

The Refinance Index decreased 7 percent from the previous week and was 1 percent lower than the same week one year ago.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) decreased to 7.04 percent from 7.06 percent, with points increasing to 0.67 from 0.66 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

Confidence! It’s what consumers DON’T have under Bidenomics.

For the fourth straight month, The Conference Board revised its consumer confidence data significantly lower. In fact January’s was the biggest downward revision since Feb 2022. And Conference Board Consumer Confidence was DOWN to -3.90 in January, the worst since Feb 2022.

It really isn’t surprising the consumer confidence stinks. Food prices (CPI) are UP 21% under Vacation Joe Biden. Diesel fuel prices are UP 90% under Listless Joe.

Well, Biden’s appearance on (unfunny) Seth Myer’s Late Night Show certainly didn’t make me feel more confident about America’s future.

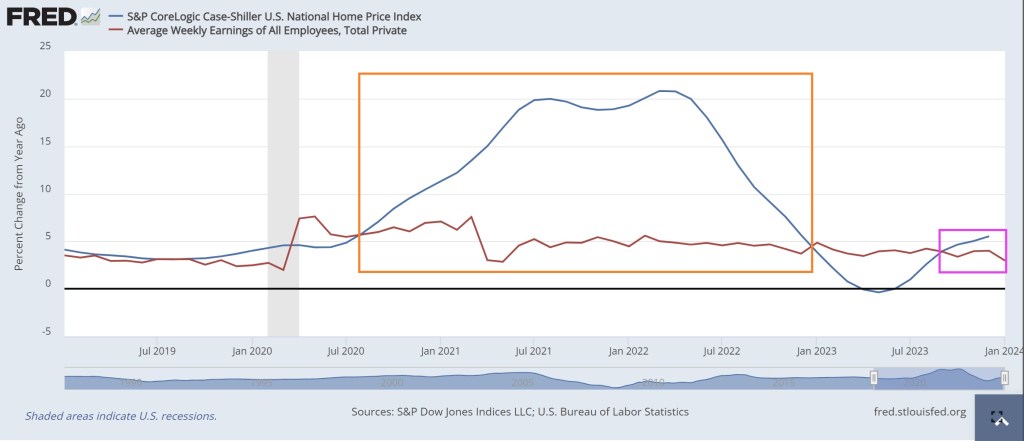

The Case-Shiller National home price index rose in December by 5.54% year-over-year (YoY) while average weekly earnings has remained lower that home price growth since September 2023 (pink box) and from August 2020 to December 2023.

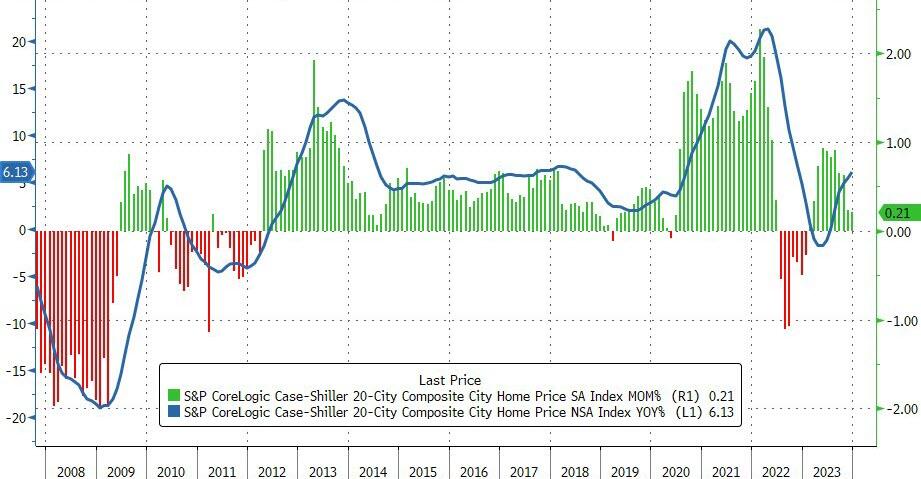

Home prices in America’s 20 largest cities rose for the 11th straight month in December (the latest data released by S&P Global Case-Shiller today), up 0.21% MoM (in line with the 0.20% MoM expected and 0.24% prior).

San Diego reported the highest year-over-year gain among the 20 cities with an 8.8% increase in December, followed by Los Angeles and Detroit, each with an 8.3% increase. Portland showed a 0.3% increase this month, holding the lowest rank after reporting the smallest year-over-year growth.

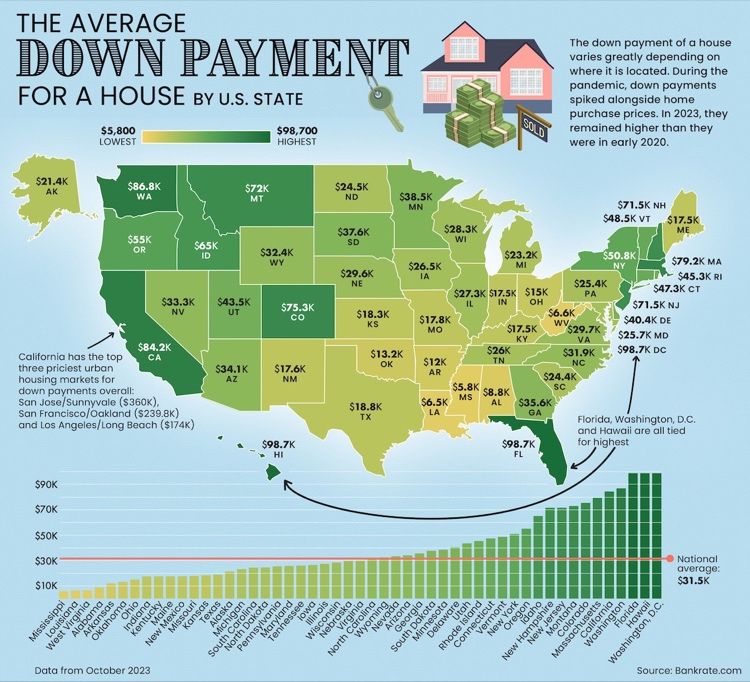

Given the current level of home prices, here is a picture of the average down payment for a house by state. Florida and Washington DC lead the nation followed by Washington state and California.

Director John Carpenter had two films, “Escape From New York” and the less popular “Escape From LA.” Carpenter’s vision of a dystopian future with Manhattan as a prison island, filled with criminals and Los Angeles as a just a weird, dystopian area filled with gangs and sleazebags. Apparently, Carpenter read George Orwell with a splash of Franz Kafka in writing these films which are sadly becoming a reality. With Biden’s immigration “policy” (let everyone in without checking who they are) is a blueprint for a new film “Escape From The USA!” I wonder if Kurt Russell is available to reprise his role as Snake Plisken?

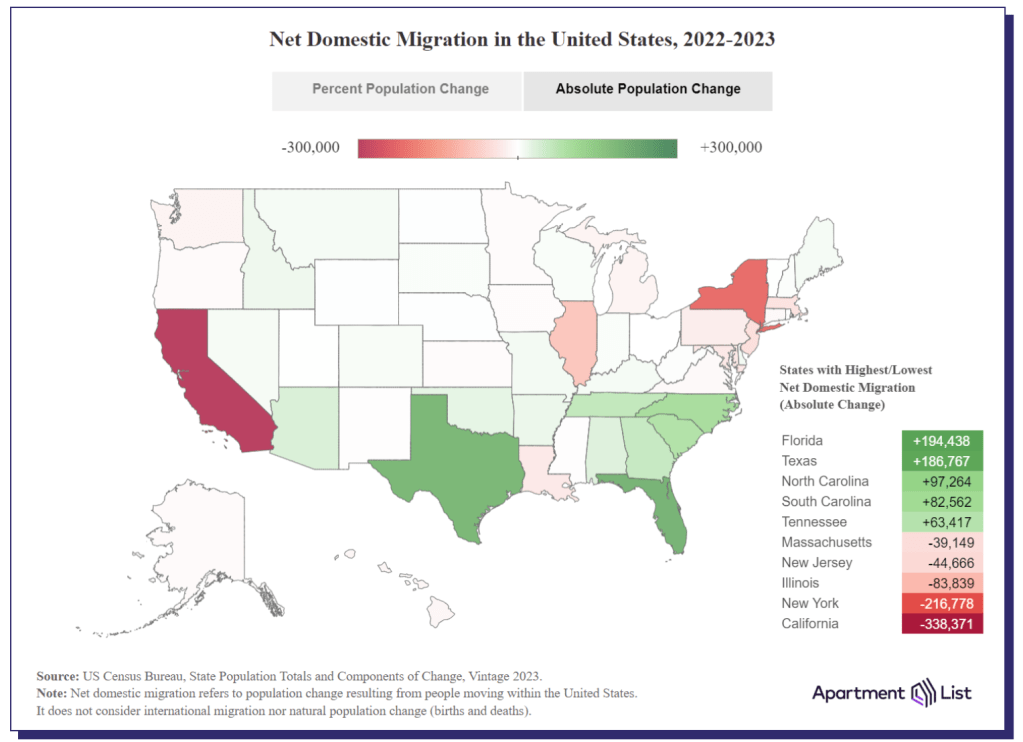

Like John Carpenter foretold, both California and New York are leading the nation in outmigration. BAD crime, high taxes, insane politicians and droves of illegal immigrants are making living in those state very difficult. Throw in the NY AG Letisha James and Judge Engmoron’s Marxist show trials of Donald Trump for doing absolutely nothing wrong and many people are are plain fed up. Illinois under the “leadership” of Chicago Fats (Governor J.B. Pritzker) and horrendous Chicago mayor Brandon Johnson (who makes former Chicago Mayor Lori Lightfoot almost look reasonable) is third in the nation for outmigration. Once again, high taxes, high crime, lots of illegal immigrants, and inane policies are causing people and businesses to flee. John Carpenter should do a film “Escape From Chicago.”

Where are people fleeing to? Florida leads followed by Texas, then the Carolinas, and Tennessee. Generally, these states have lower taxes, lower crime, and less intrusive politicians. E.g., no Gavin Newsom (CA), no Kathy Hochul (NY) and no J.B. Pritzker (IL).

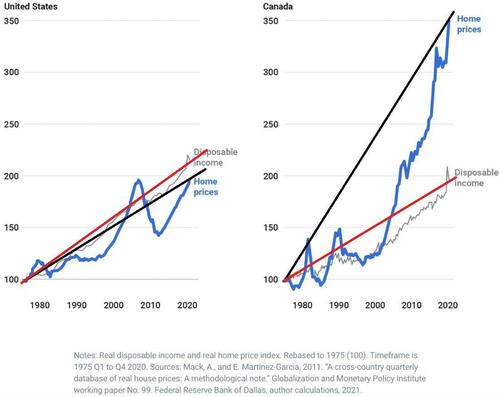

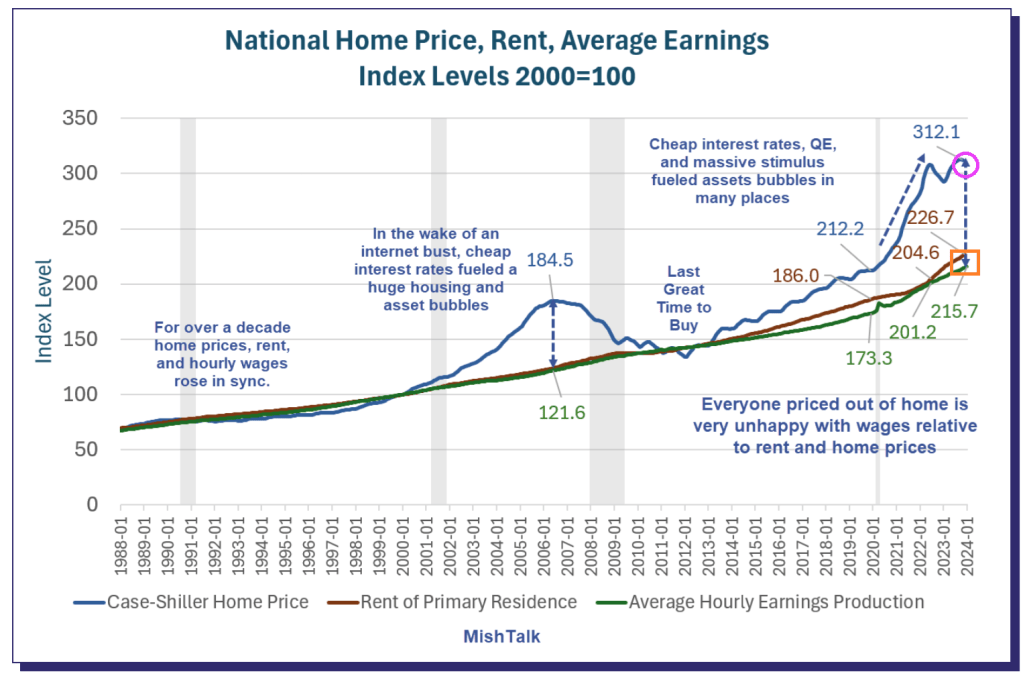

Another reason that people are fleeing New York and California is cost of living. To be sure, Bidenomics (an insidious malinvestment plan, aka, donor-nomics) has made matters worse. Home prices (blue line) and rents (red line) has soared and are far higher than the grow in average earnings (green line). Los Angeles is wonderful if you are a celebrity like Steve Spielberg, Tom Hanks and The Office’s Jenna Fischer where you live in a mansion and are protected by the police force. But other parts of Los Angeles are filled with the homeless, illegal immigrants, rampant crime, and is simply unlivable.

Escape From New York is appropriate for today’s situation. An idiot Mayor and Governor, illegals crowding the streets and hotels, crime through the roof, illegals attacking police. And Joe Biden acting like The Duke of New York, A number One! I guess the closest person we have to Snake Plisken is Donald Trump.

On a related note, Georgia is still seeing positive net in-migration. But as the Fani Willis corruption scandals unfolds and their weak-kneed Governor Kemp does nothing, we have yet another film John Carpenter could make “Escape From Atlanta.” Or a computer game like “Call of Booty.”

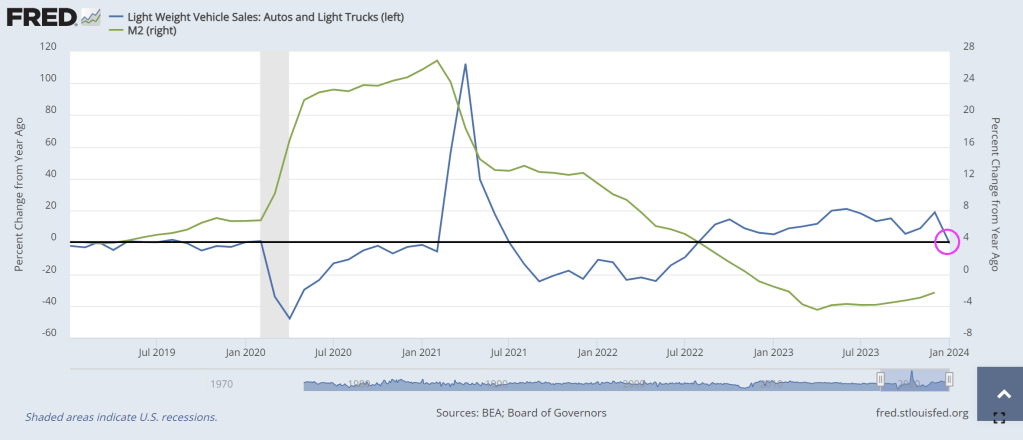

Cars and light trucks are seeing declining YoY sales in January (-0.7%) as M2 Money growth remains negative.

Automotive News was the first to report Ford Motor Co. halted shipments of all 2024 F-150 Lightning electric pickup trucks for an undisclosed quality control issue just weeks after slashing production volumes for the EV model due to sliding demand.

“We expect to ramp up shipments in the coming weeks as we complete thorough launch quality checks to ensure these new F-150s meet our high standards and delight customers,” company spokeswoman Emma Bergg wrote in a statement.

Last month, Ford announced plans to slash the Lightning production in April “to achieve the optimal balance of production, sales growth and profitability.”

The automaker (and many others, like Mercedes Benz) is recalibrating its electric vehicle strategy as the Biden administration plans to downshift the EV transition as demand plummets.

Thousands of auto dealers nationwide recently warned the ‘climate change warriors’ in the White House: the 2030 EV push is backfiring.

“Currently, there are many excellent battery electric vehicles available for consumers to purchase. These vehicles are ideal for many people, and we believe their appeal will grow over time. The reality, however, is that electric vehicle demand today is not keeping up with the large influx of BEVs arriving at our dealerships prompted by the current regulations. BEVs are stacking up on our lots,” the dealers said.

They warned: “Already, electric vehicles are stacking up on our lots which is our best indicator of customer demand in the marketplace.”

“Key takeaways thus far from earnings season are that the EV slowdown is not showing any evidence of an inflection, Level 4 autonomy headwinds continue to persist, and fears over supplier inventory overbuild are likely overblown.

The Hollies said it best: Stop, stop, stop. FIAT Money Printing that is.

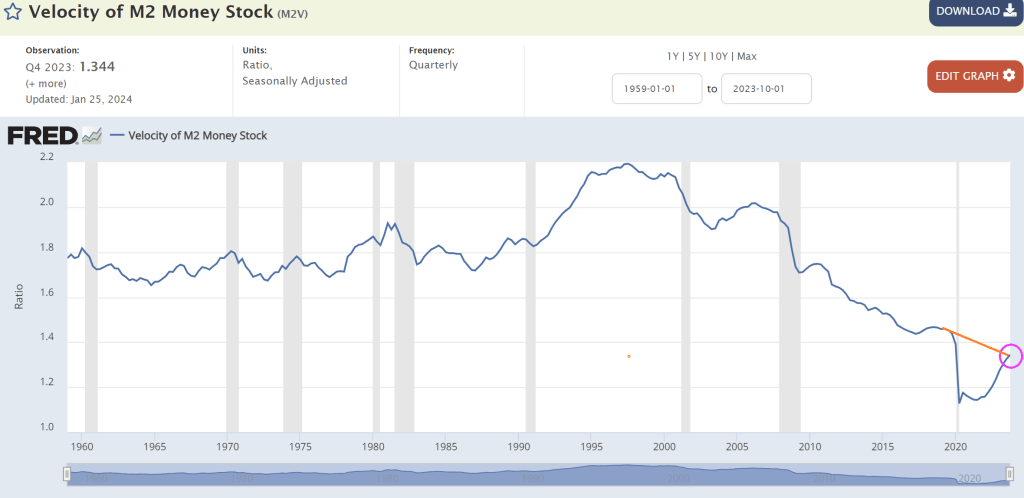

Typically, we look at M2 Money Velocity (GDP/M2) as a measure of how much the economy grows by expanding the money supply.

M2 Money Velocity is currently at 1.344, and still below where we were under Trump prior to Covid. After Powell printing palooza after Covid, M2 Money Velocity collapsed and is slowly rising, but remains low by historic standards.

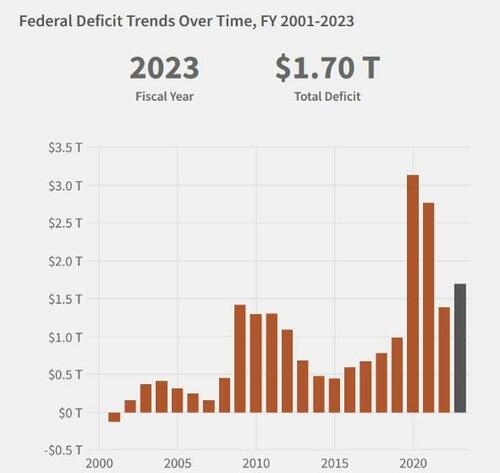

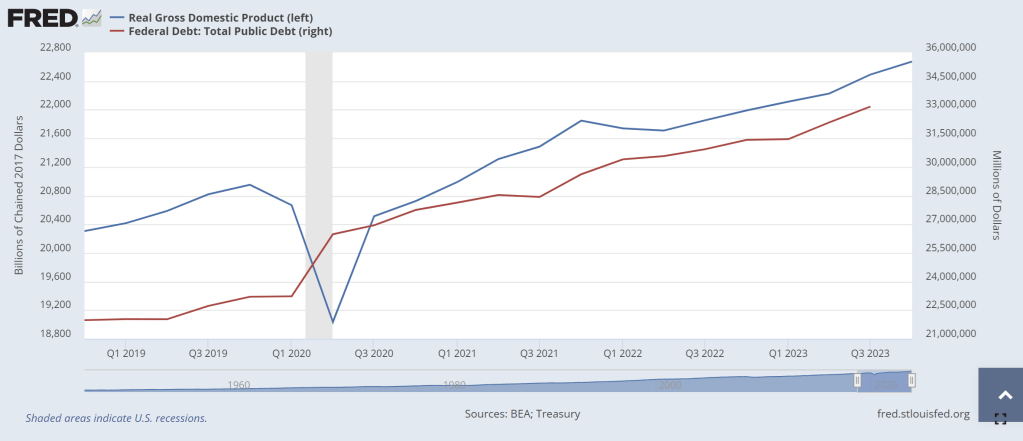

Perhaps a more interest velocity is DEBT velocity (GDP/DEBT). Under Biden’s Reign of Error, Federal debt has increased by $6,539,359 million while real GDP has increased by only $1,948.731 billion (or roughly $2 trillion in GDP growth after $6.54 trillion in debt). Or a DEBT velocity of 0.3. Yikes! No wonder China is bailing on US debt!

This chart makes debt issuance look better than it really is. Again, the DEBT VELOCITY of 0.3 is terrible meaning that for every $1 of Federal debt, we get 30 cents in Real GDP under Biden. One of my macroeconomics textbooks stated that debt growth is fine as long as real GDP growth rises faster than debt growth. Apparently, Treasury Secretary Janet Yellen didn’t read that textbook! Real GDP has grown by 9.43% under Biden while Federal debt has grown by … gulp .. 24%.

Yes, the US is borrowing like the proverbial drunken sailor while they “invest” in green energy, wars in Ukraine and the Middle East, and massive social welfare programs (like the old breads and circuses from the dying Roman Empire). When watching the media’s obsession with Taylor Swift and Chief’s Tight End Travis Kelce at The Super Bowl, it reminded me of “Breads and Circuses” as our nation is collapsing like a dying star. (That is why I Iike Gold, Silver and Bitcoin!)

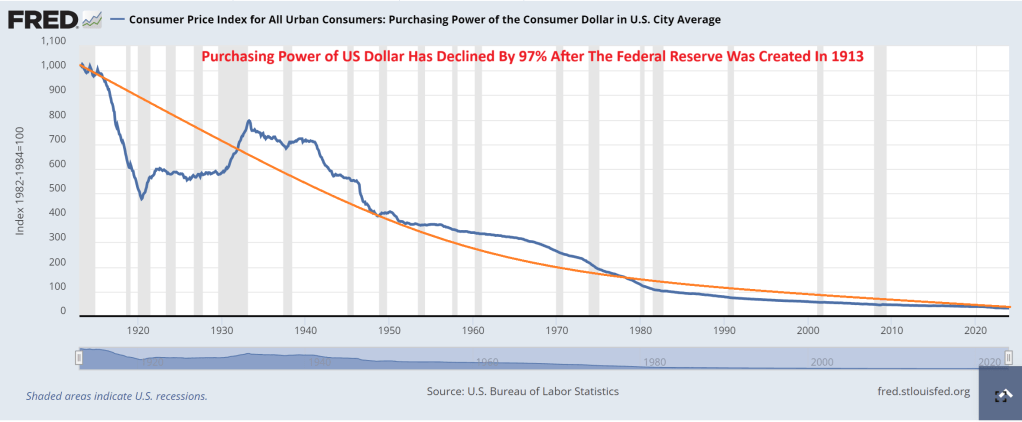

What about The Federal Reserve? It was created in 1913 after signed into existence by President Woodrow Wilson. Since The Fed’s inception, consumer purchasing power has declined by 97%.

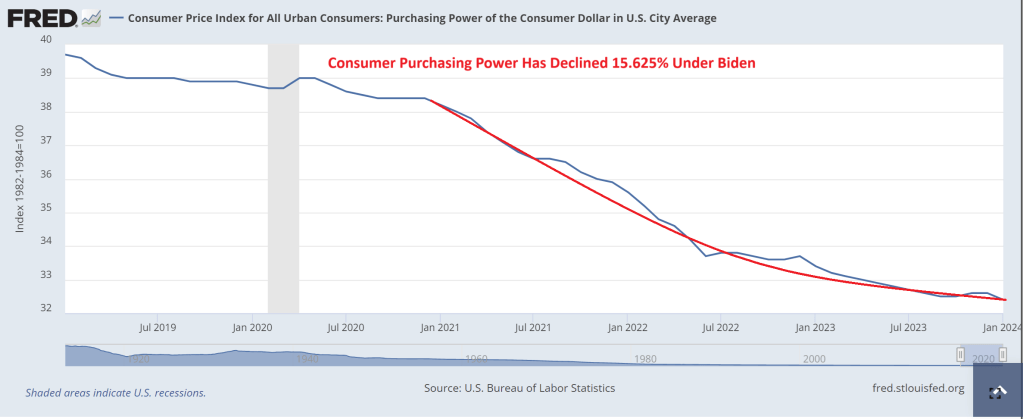

And under Biden, inflation has been so bad that consumer purchasing power is down 16%.

In summary, The Federal Reserve has been printing like crazy (I would say Batshit Crazy, but I actually think bats are adorable). And Treasury (under former Fed Chair Janet Yellen) has been borrowing like crazy too. While politicians claim the economy is in great shape, it is really because The Fed is printing wildly, Yellen is borrowing wildly, and much of US GDP is not due to the private sector, but Federal government spending … to the donor class. This is NOT a sustainable and will eventually crash into a ravine.

So, despite recent declines in energy prices, gasoline prices are still up 46.25% under “Green Joe” and the all important for shipping, diesel prices, are still up 55.6% under Brainless Joe.

One would think that massive rises in gasoline and diesel prices would make everyone buy an electric vehicle (EV). But alas, the high cost and unreliability of EVs is turning off consumers. (I own a hybrid and wish I didn’t).

This time it deals with supply chain logistics, with Bloomberg reporting this week that in the year and a half since passing the Inflation Reduction Act, automakers are finding out the hard way that the rigorous criteria for manufacturing batteries using materials from the United States and its free-trade allies could render them cost-inefficient compared to global competitors.

Companies like Tesla are instead taking advantage of a temporary shift in the rules to stock up with cheaper batteries from countries like China.

The Biden administration’s new rules will all but cut out China from the supply chain, however, which will make it tougher to find affordable metal suppliers.

This, in turn, will threaten President Biden’s goal to boost the domestic electric vehicle market. Bloomberg writes that mining companies and labor unions insist that without curtailing the influx of cheaper, Chinese-subsidized materials, the U.S. can’t develop a competitive EV market.

Meanwhile, the higher costs are driving automakers away from EVs. And as battery material requirements are set to double by 2027, fulfilling these mandates will be increasingly difficult, putting Biden’s ambitious EV strategy at risk.

The demand side of the equation also looks less than favorable. We wrote just hours ago about how Ford was slashing prices on its Mach E and Lightning 150. Tesla has been slashing prices to stoke demand for nearly a year now.

Both Ford and GM have said they’re going to curtail their investment in EVs. General Motors, who posted better than expected earnings earlier this month, said that it plans on changing its product lineup to include more hybrid vehicles, drifting away from pure electric vehicles.

CEO Mary Barra said on the earnings call: “Let me be clear, GM remains committed to eliminating tailpipe emissions from our light-duty vehicles by 2035, but, in the interim, deploying plug-in technology in strategic segments will deliver some of the environment or environmental benefits of EVs as the nation continues to build this charging infrastructure.”

Recall, a report from Consumer Reports last year found that electric vehicles have almost 80% more problems and are “generally less reliable” than conventional internal combustion engine cars.

But hey, what good is a “free” market if the government doesn’t have complete and total control of consumer choice, right Joe? After all, Biden drives a gas guzzling Chevy Corvette. When Biden sells his Corvette and buys a Chevy Bolt, I might believe him. Nah!

So, the free market is standing up to Biden’s hard left tyranny.

My new nickname for Biden is Dopey. And Kamala Harris is Happy (because she laughs constantly). Mayorkas is Bashful (he doesn’t do anything). NY Senator Chuck Schumer is Grumpy. Jill Biden is Doc (for her pathetic PhD in Education). The intellectual seven dwarves are running our country into the ground.

I remember the joke made by Jay Leno about Obama. Go to a McDonalds and order whatever you want and give the bill to the person behind you. Unfortunately, that is the Democrat playbook under Obama/Biden (hereafter termed “O’Biden”). For example, Biden is bragging about forgiving student loan debt relief in the amount of $1.2 Billion in student debt for roughly 153,000 borrowers. And bragging that he is ignoring the US Supreme Court like a banana republic dictator. Like the Jay Leno “joke,” SOMEONE has to pay for this election year vote pandering. But that is the beauty/tragedy of BIG government. It is so big and the numbers so monstrous that many kind of shrug and go “eh.” But someone pays and its the middle class in the form of taxes and inflation.

Who is going to pay for the 10 million illegal immigrants that have crossed the southern border under Biden? While Paul Krugman points to a higher GDP from immigration (illegals still buy goods and services), but mostly are a deadweight drag on social services such as welfare, Medicare, schools, healthcare system, etc.). And of course migrant crime is going off the charts. Who pays for Biden’s border fiasco? The middle class and low wage workers, of course. Elites benefit from uncontrolled immigration, generally live in compounds with private security that the rest of us can’t afford. Remember President Carter and the Cuban Mariel boat lift where Fidel Castro emptied his prisons and sent them to Florida creating absolute mayhem and a huge spike in crime? Biden and Cuba Pete Mayorkas turning up the heat on immigration and its accompanied crime wave.

O’Biden loves to spend other people’s money. Aka, OUR money. Case in point. According to the CBO, net interest on the exploding Federal debt under O’Biden now exceeds our defense spending and that gap is expected to explode. To be sure, the US is funding billions in the middle east, handing over billions to Zelensky and Ukrainian oligarchs, and we have China. What a mess!

So, when will “Billions Biden” stop spending other people’s money? Well, only a barely-held Republican House can stop Biden. Meanwhile I will focus on soaring food prices and eat cheap cabbage rolls and drink coffee. Until Biden kills off those pleasures.

But don’t worry! We might get Gavin Newsom, the ultimate used car salesman, to replace Biden against Trump. But Biden’s ego is so massive (why I have no idea) that he won’t go down without a fight. And what about Cacklin’ Kamala?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.