President Biden reminds me of Cousin Eddie, the dimwitted cousin of Clark Griswold’s wife in the Vacation movies. Except that Cousin Eddie is a nice dimwit while Biden is a nasty dimwit. And politcal stooge.

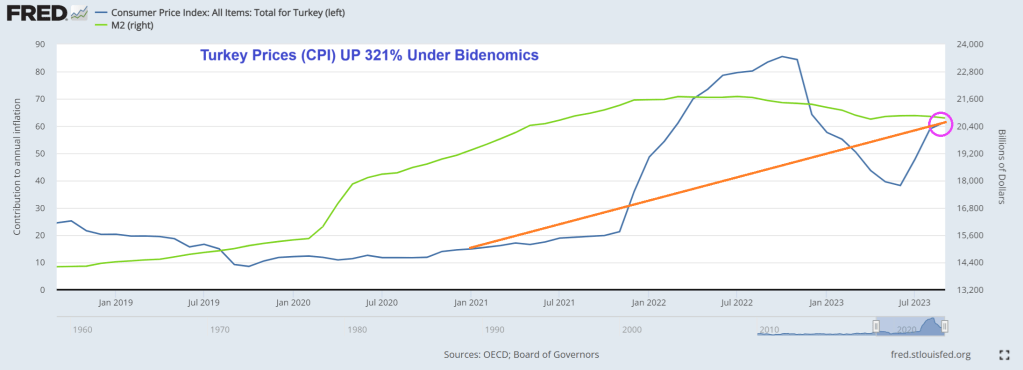

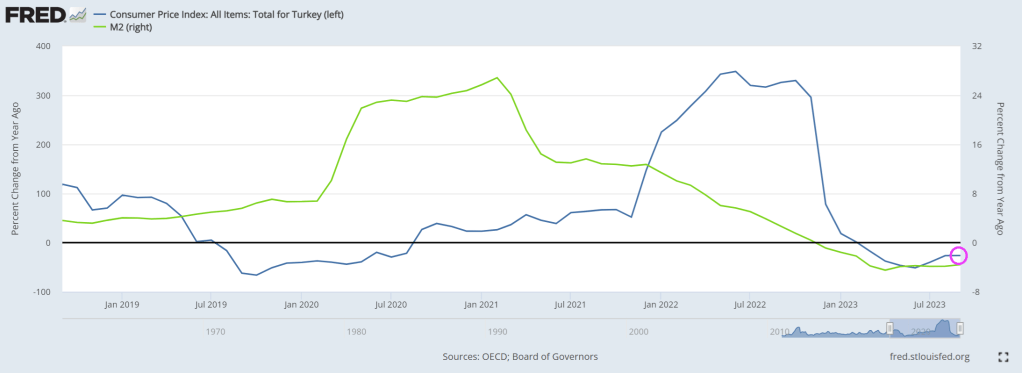

Given that turkey prices are up 321% under Biden, the famous Thanksgiving line “Save the neck for me, Clark” is most appropriate since we will be forced to eat every part of the turkey.

Of course, year-over-year growh in turkey prices (CPI) are now negative along with M2 Money growth. Note the surge in M2 Money growth (green line) followed by the surge in turkey prices (blue line). Now both are declining.

A Bidenomics turkey!

Here is Biden giving a Thanksgiving turkey a pardon, hoping he gets a pardon for his massive corruption. But which one is the turkey??

The World Economic Forum (WEF) is a leading pusher of the ESG drug, pushed by the elite class intending to control the world. Unfortunately, numerous American politicians and influencers have attended the Davos meetings and have openly praised the WEF and its leader Klaus Schwab.

ESG investing, or sustainable responsible investing (SRI), uses this information about a company to inform investment decisions that prioritize all stakeholders.

Here’s how the Forum’s partners are leading the switch to stakeholder capitalism.

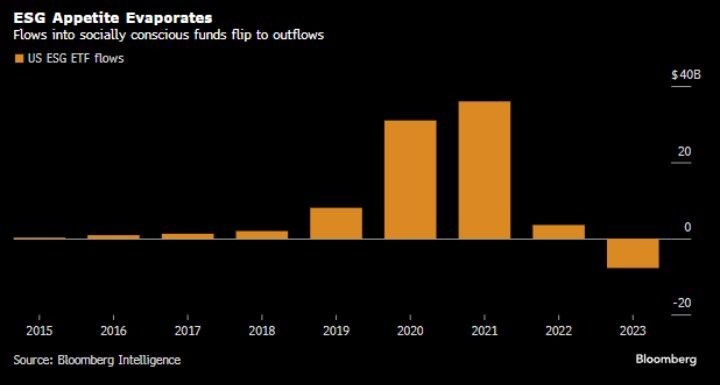

But all is not well with WEF’s ESG drug distribution. In fact, ESG flows into socially consious funds were a big thing during Covid (2020) and the first year of Biden’s Reign of Error. But ESG flows slowed sharply in 2022 and seeing net outflows in 2023.

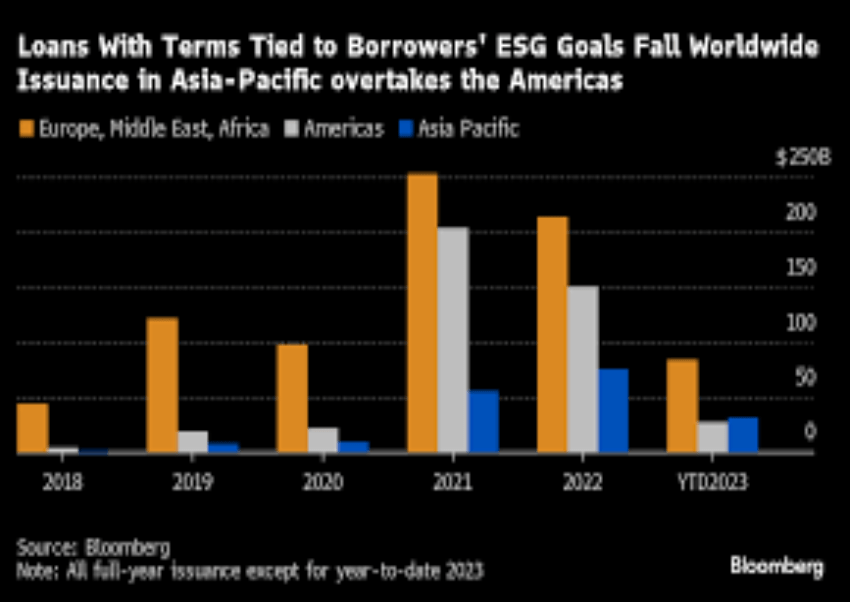

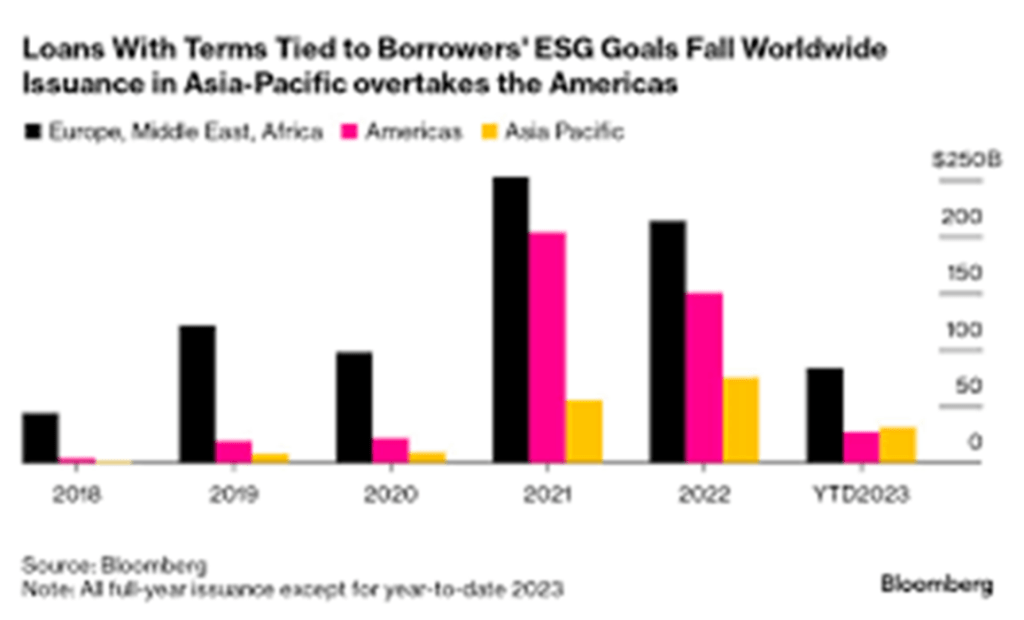

US borrowers are retreating en masse from the world’s second-biggest ESG debt class.

The $1.5 trillion market for sustainability-linked loans, in which borrowing is tied to environmental, social or governance goals, has seen an overall slowdown in volumes this year as both interest rates and greenwashing fears rise. But nowhere has the decline been as precipitous as in the US, where the number of new sustainability-linked loans is down 80% from a year earlier.

But ESG is still relatively popular in Europe, Middle East and Africa (orange). But taste for ESG is waning around the globe. But the selection of Biden as President in the US marked a surge in ESG -tied loans in 2021 and 2022 (not to mention the insane levels of spending out of Biden and Congress, much tied to the sustainability, green energy fantasy.

Loans with terms tied to borrower’s ESG goals have fallen worldwide.

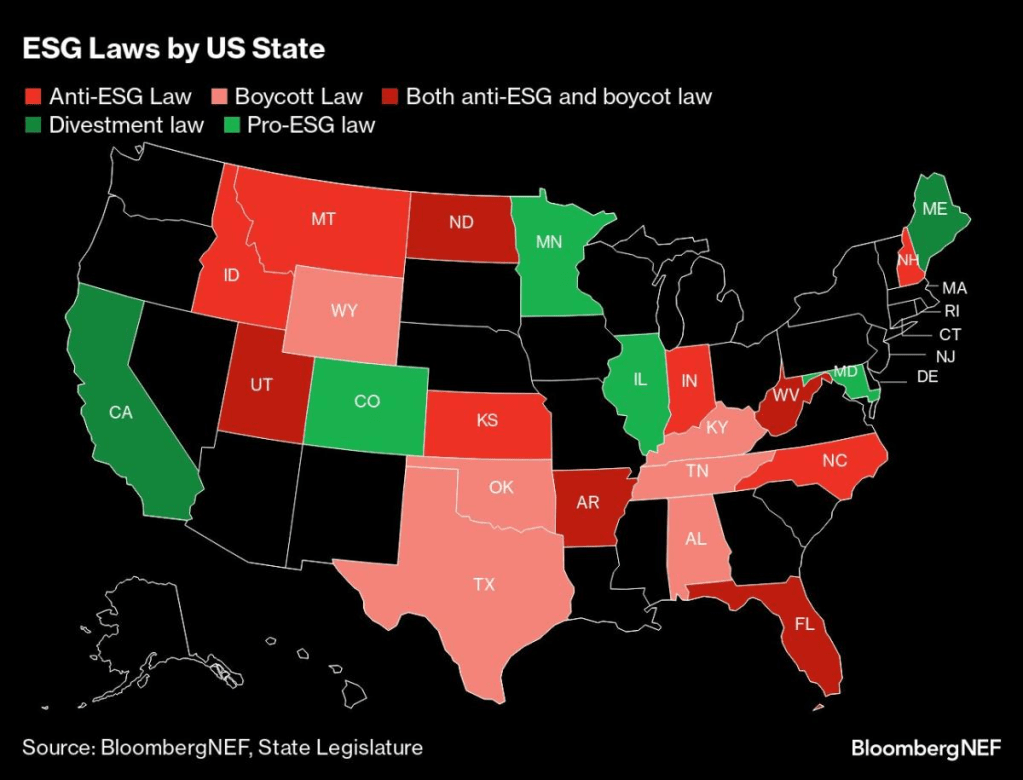

Several states (largely blue states like California, Minnesota, Illinois, and Colorado have pro-ESG laws) while several states have anti-ESG laws (largely red states like Montana, Idaho, North Dakota, Kansas, Utah, Indiana, Arkansas, Florida, and West Virginia).

And of course, global warning may not be as dire as John Kerry and Greta Thunberg say.

WEF’s Klaus Schwab about to get sniffed by his 80-year old puppet, Joe Biden. In fact, Biden is singing “I’m your puppet.”

Here is Hunter Biden welcoming the Green Energy fairy and all the trillions in misallocated spending it brings.

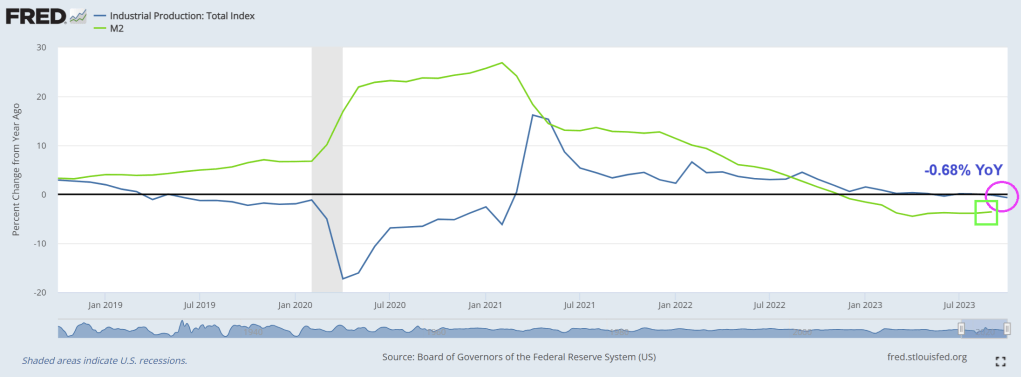

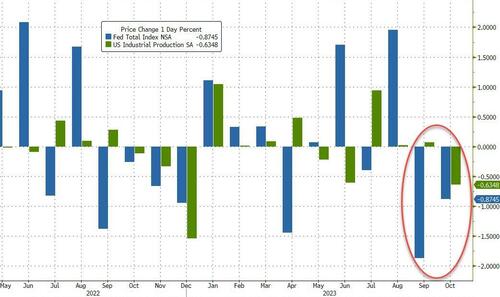

Notably, once again, the non-seasonally-adjusted industrial production tumbled more than then seasonally-adjusted data…

Source: Bloomberg

On the manufacturing specific sector, consensus was for a 0.4% drop MoM but it was considerably worse, dropping 0.7% MoM (and September’s print was revised down from +0.4% to +0.2% MoM). That is the biggest MoM drop since March and biggest YoY drop since the COVID lockdowns.

That is also the 8th straight month of YoY declines for Manufacturing production.

Source: Bloomberg

Output was weighed down by a 10% plunge in motor-vehicle production as the annualized rate of car assemblies dropped to 9.22 million units, the least since February 2022. Excluding parts production, autos and trucks production fell 16.5% MoM – the biggest drop since the COVID lockdowns…

Source: Bloomberg

Starting in September, the United Auto Workers union authorized targeted strikes against the Big Three Detroit automakers, disrupting production at the companies and at their suppliers. The UAW reached tentative agreements with management in late October, laying the groundwork for a rebound in factory output in November.

So theorteically, we should see bounce back next month. Unless demand – as WMT hinted at – has fallen off a cliff.

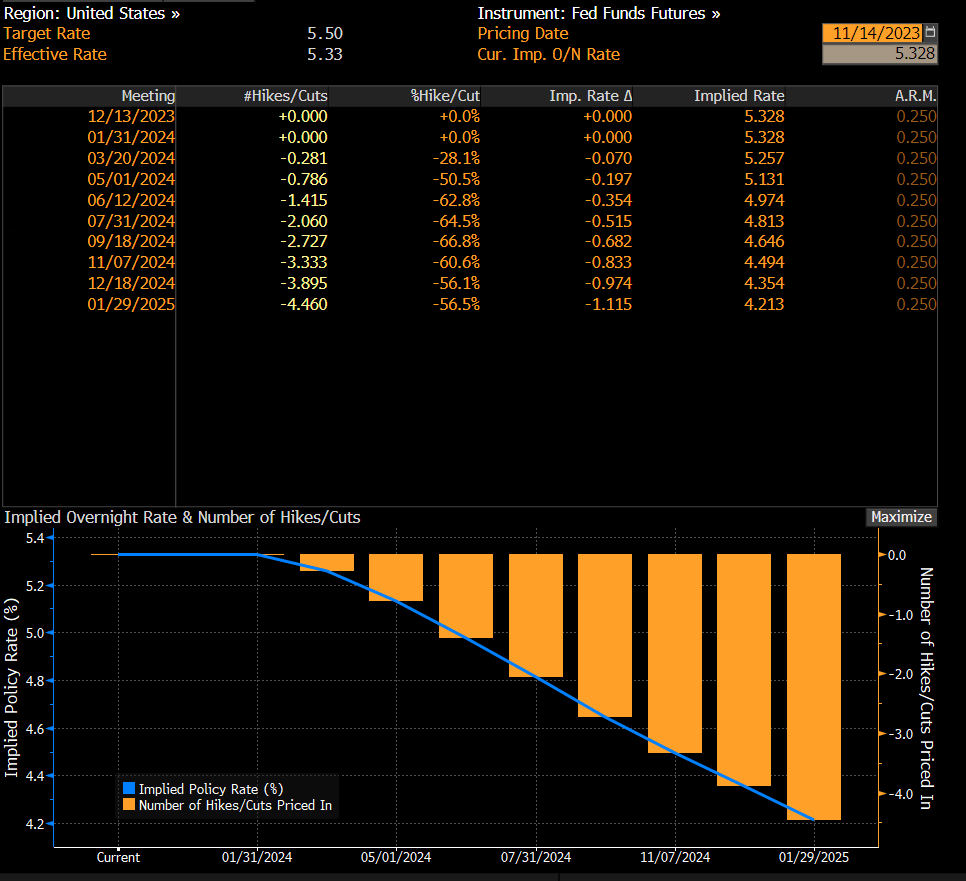

Its beginning to smell like Fed spirit! As the 2024 Presidential election rapidly approaches, The Fed will be pressured into lower interest rates to haul Biden’s befuddled and corrupt ass across the finish line. Or his replacement, Greasy Gavin Newsom. (Leaving an oil slick in his wake).

Lowering the mortgage rate will benefit the real estate market, which is currently been “Biden’d.” Due to inflation and The Fed’s mission to crush inflation.

High mortgage rates that approached 8% earlier this month continue to hammer builder confidence, but recent economic data suggest housing conditions may improve in the coming months.

Builder confidence in the market for newly built single-family homes in November fell six points to 34 in November, according to the National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI) released today. This is the fourth consecutive monthly drop in builder confidence, as sentiment levels have declined 22 points since July and are at their lowest level since December 2022. Also of note, nearly the entire HMI data for November was collected before the latest Consumer Price Index was released and showed that inflation is moderating.

Mortgage rates will likely decline in 2024 as The Fed reverses its inflation-crushing policy for Presidential election interference.

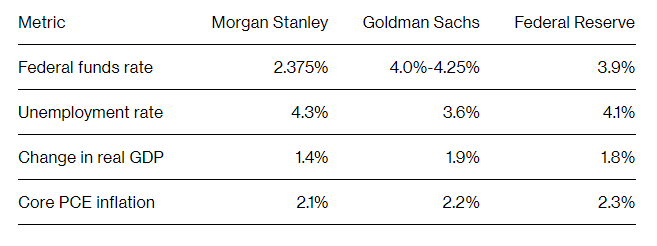

And Morgan Stanley forecasts the Fed Funds Rate to plunge to 2.375%.

Joe Biden is 80 and not exactly the most energetic President that can inspire confidence.

Maybe the economy needs Viagra.

I really wish Biden would stop babbling about “his” approach to economic growth, a Chinese Communist approach of top down economic management.

Under Biden, Americans have seen a 17.6% price hike and a 3% pay cut. Inflation has averaged 5.9% — more than double the level of inflation under any of the last four presidents.

Biden says he wants 4 more years to finish the job. Like killing off the mortgage market completely, Joe?

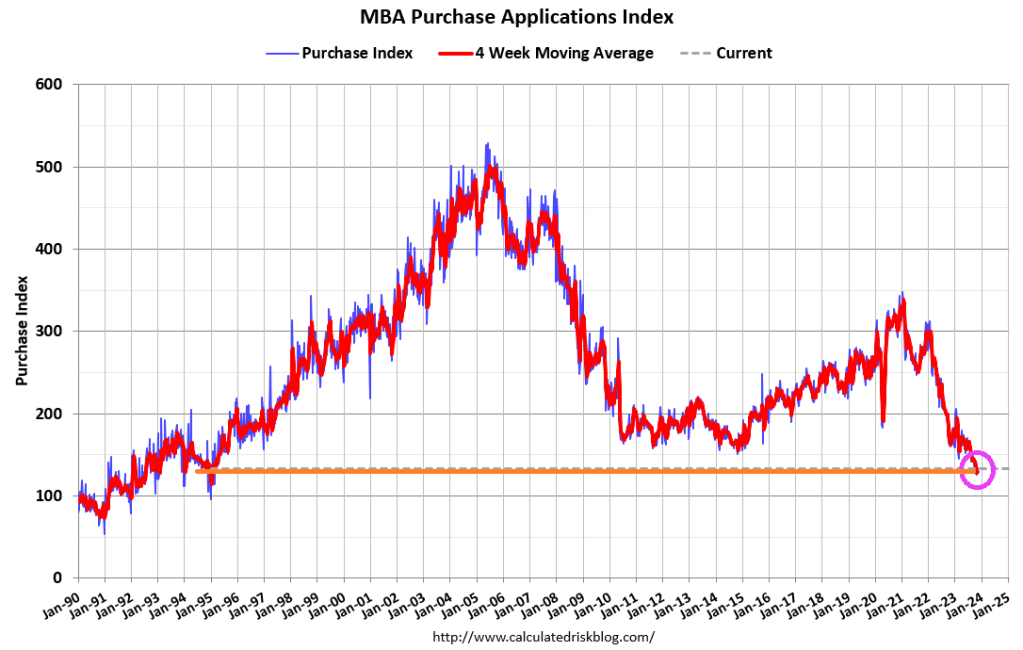

Mortgage applications increased 2.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 10, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 2.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 0.4 percent compared with the previous week. The seasonally adjusted Purchase Index increased 3 percent from one week earlier. The unadjusted Purchase Index decreased 0.3 percent compared with the previous week and was12 percent lower than the same week one year ago.

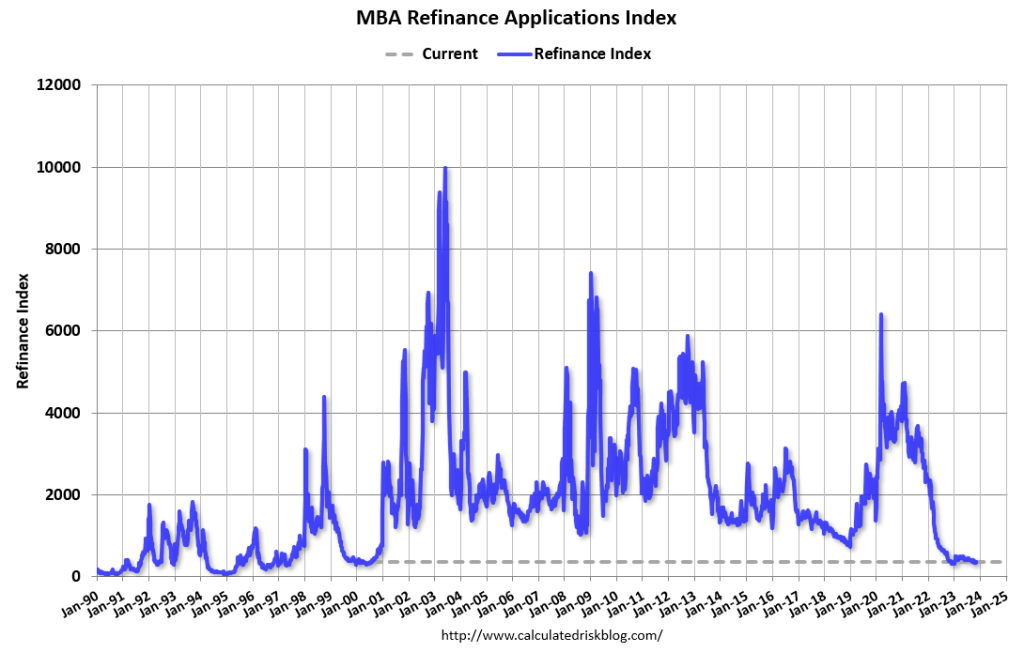

The Refinance Index increased 2 percent from the previous week and was 7 percent higher than the same week one year ago.

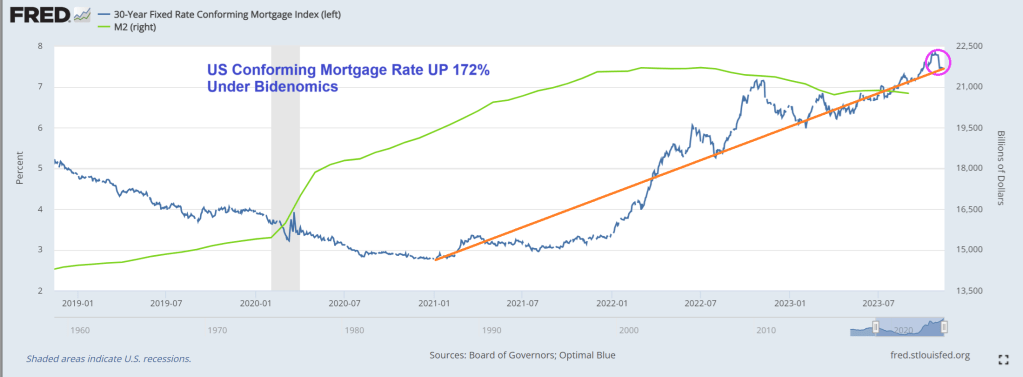

Of course, mortgage rates have been declining slightly over the past few weeks, but remain up 172% under Biden.

At least the stock market is booming after the inflation report signalled that The Fed is likely done with rate hikes.

On the gold front, we are seeing evidence of contango.

Bitcoin? Down a wee bit after a staggering rise in price over the past year.

Here is China’s Xi meeting with Biden’s likely replacement, “Greasy Gavin” Newsom and Newsom’s likely Treasury Secretary, Janet “Too Low For Too Long” Yellen. Newsom, Yellen and Xi all want havoc in America.

Republicans elected Mike Johnson from Louisiana as House Speaker, then were surprised when Johnson agreed with big spending Senators McConnell and Schumer on Biden’s mega spendathon. Also, several Republicans voted with Democrats NOT to impeach Cuba Pete (Mayorkas) for allowing 8 million illegals to cross the southern border. Bottom line: the Biden Administration and Congress are closely held subsidiaries of the elite 1% and US large corporations. The middle class be damned! But we will get fooled again in every election.

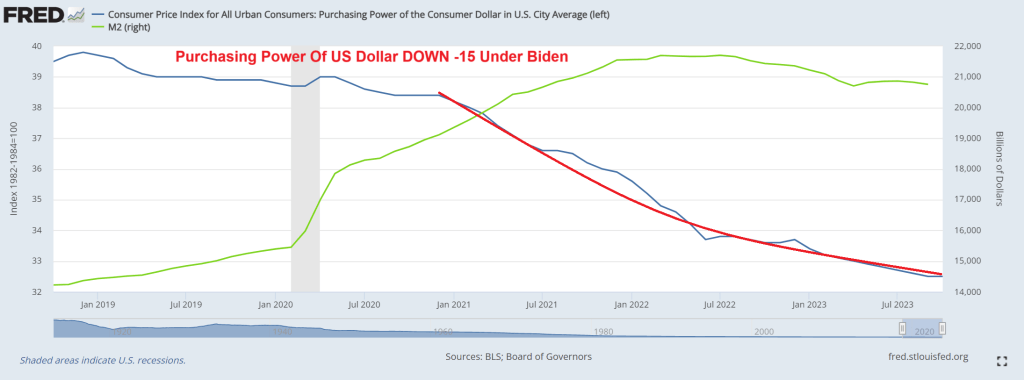

Since Biden’s inaugration in January 2021, the purchasing power of the US dollar is down a staggering -15%.

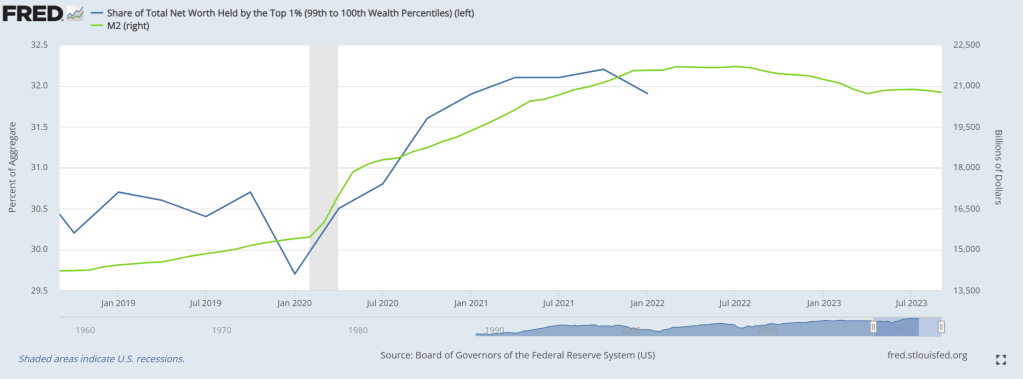

Yes, under control of large corporations and the 1%, the economy is an economic wasteland. But the 1% are doing great under Bidenomics! With The Fed’s help of course.

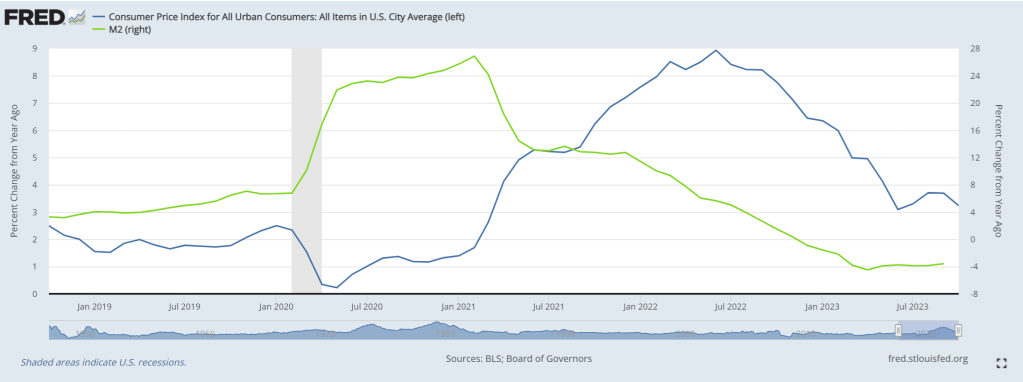

Here is a chart of core inflation relative to M2 Money printing. Easy way to cool inflation … stop printing money!

Here is China’s Xi and America’s “China Joe” Biden.

Seriously, Biden has always been known as being stupid and corrupt. Now he has dementia. A PERFECT President for the 1% in their war against the middle class. Biden is the penultimate “useful idiot” with an emphasis on idiot.

On a amusing or sad note, Biden campaign communications director Michael Tyler’s message to Americans who are worse off economically under Biden: “That’s precisely why we need another four years to finish the job.” OMG! What does “finish the job” mean?? I am afraid to ask.

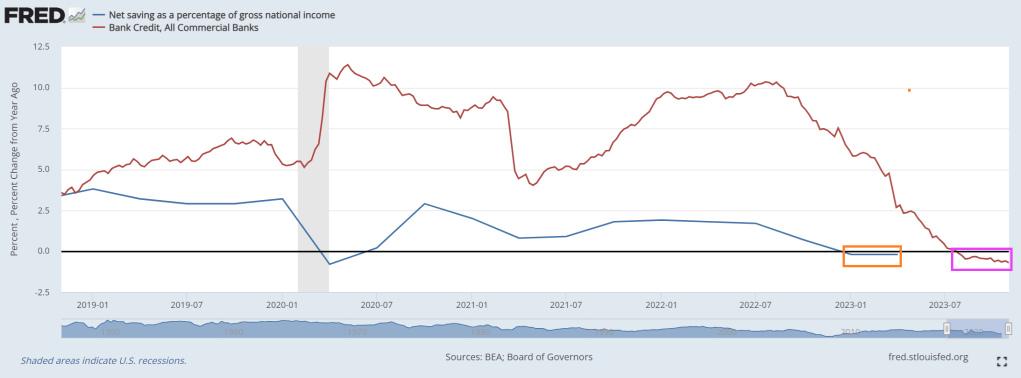

Where we currently sit is … bank credit growth is in the red (15th straight week of negative growth) and net savings as a percentage of gross national income has seen negative growth YoY for 2 consequtive quarters.

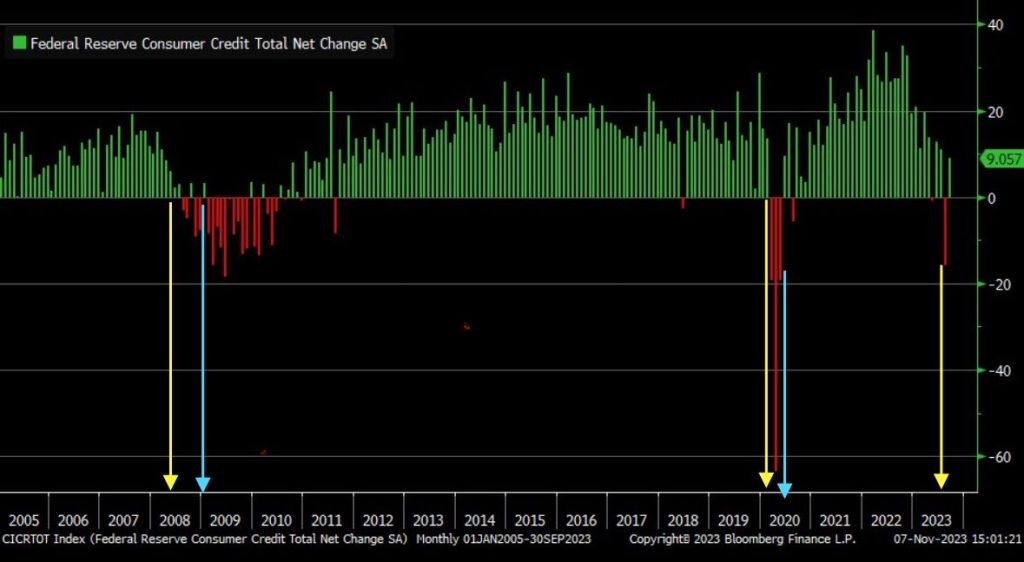

September marked the largest consumer credit drop since May 2020, signaling a significant recession warning.

And with Bidenflation (or Yellenflation) and The Fed’s counterattack, we are seeing bank stocks losing relative to the tech sector.

Proshares Bitcoin (BITO)’s assets have nearly doubled in the past 30 days.

Yes, the Three Stooges (Biden, Yellen, Powell) have put the US on a highway to hell!

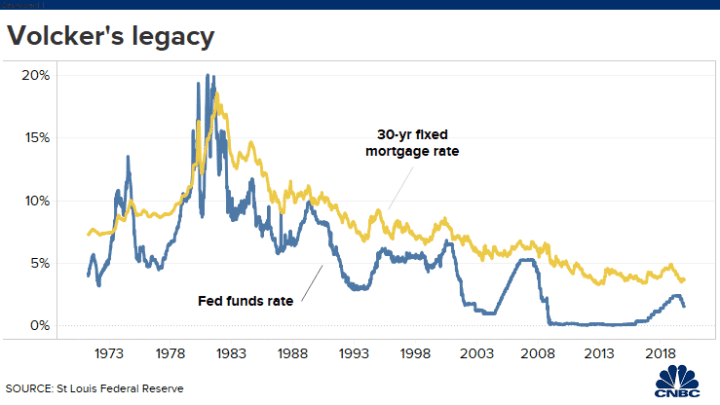

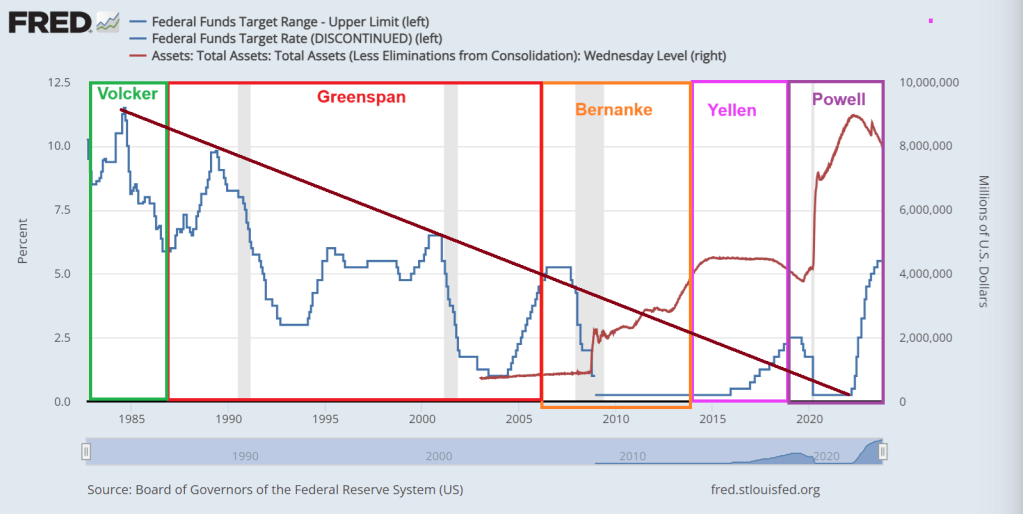

I had a wonderful time speaking at the Passive Investors Conference last night. One question I was asked was “Why doesn’t Powell (the current Fed Chair) pull “a Volcker” to cool inflation. She was referring to former Fed Chair Paul Volcker’s sudden raising of The Fed’s target rate which resulted in a cooling of inflation, but also an increase in the 30-year fixed mortgage rate to 16.63% in 1981.

Notice the trend in the Fed’s target rate and 30-year mortgage rate after Volcker’s rate shock. The trend in both has been downward as inflation was cooled.

But, each Fed Chair ranged from hyperactive to hypoactive (meaning doing little). Volcker and Greenspan saw wild swings in The Fed’s target rate. Bernanke pretty much only lowered rates AND expanded the Quantitative Easing (QE) or asset purchases by The Fed. And nothing has been the same since.

Yellen, now Treasury Secretary, continued Bernanke’s practice of zero interest rate policies (ZIRP) and QE (asset purchases) … until Donald Trump was elected President. In fact, Yellen raise rates only once prior to Trump’s election as President. Then raises rates 8 consecutive times. This is why I call Yellen “TLTL Janet”. Too low for too long Janet.

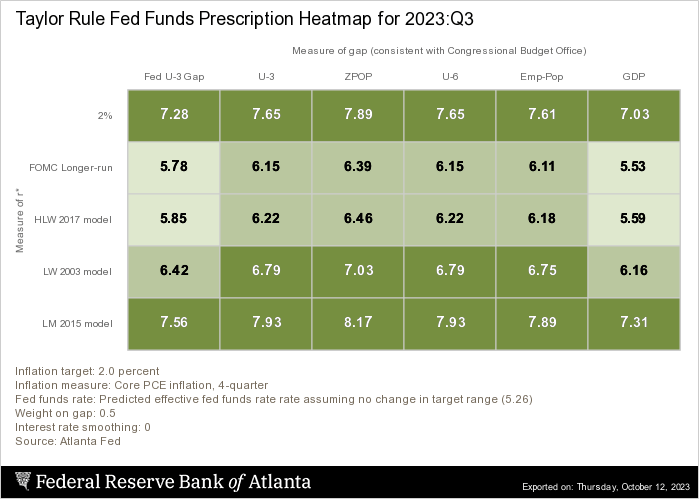

The she was replaced with DC insider Jerome Powell. Trump’s economy was strong (one explanation for Yellen trying to cool the economy with 8 consecutive rate hikes). But the Covid struck and Powell/Fed Open Market Committee overreacted, lowered the target rate back to 25 basis points and massively expanded the balance sheet. Powell also oversaw a rapid increase in the target rate, very Volckerish! But Powell stopped short of the rate suggested by The Taylor Rule of around 6.5% to 8.17%. The current target rate is 5.50%. So, Powell stopped far short of rates need to cool inflation.

But with Bidenomis came Bidenflation and a reversal of misfortunes for The Fed. They started rapidly raising rates … again.

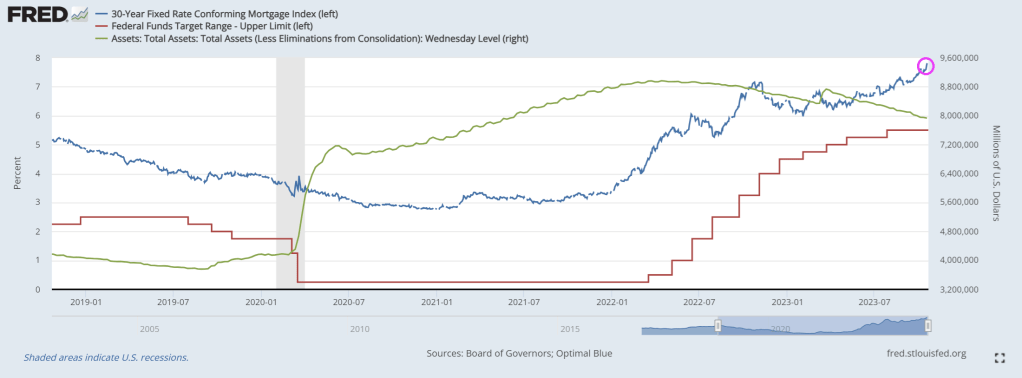

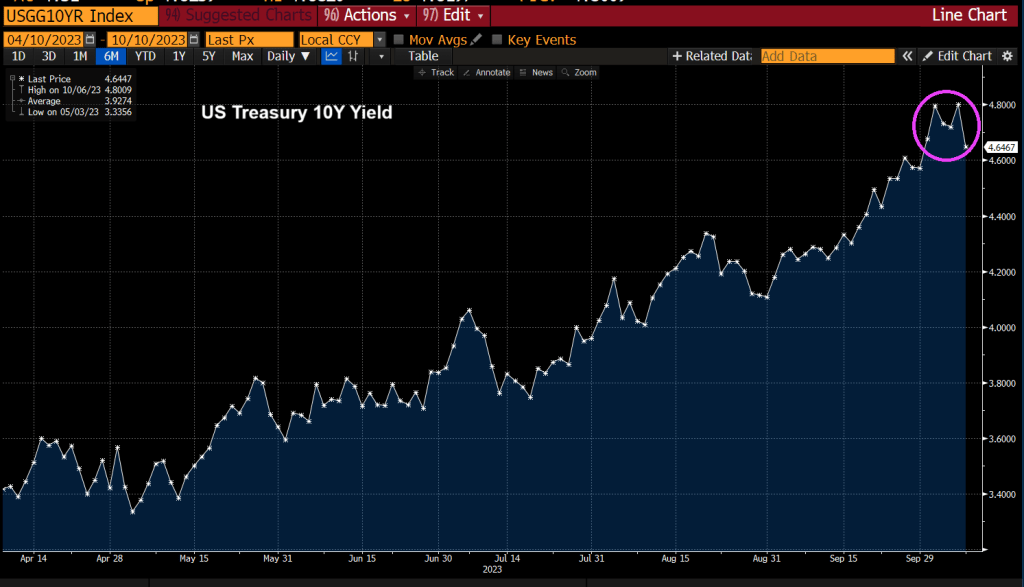

Mortgage rates continue to climb as The Fed stubbornly won’t reduce its balance sheet.

Biden/Congress have a broken fiscal model where spending is out of control. And The Fed can’t buy all the debt Biden/Yellen want to issue.

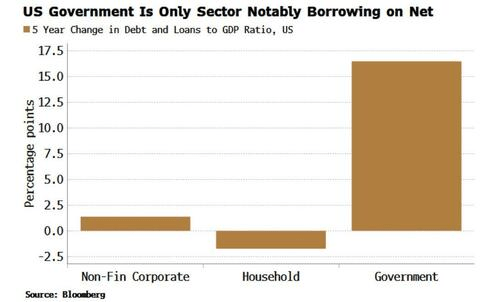

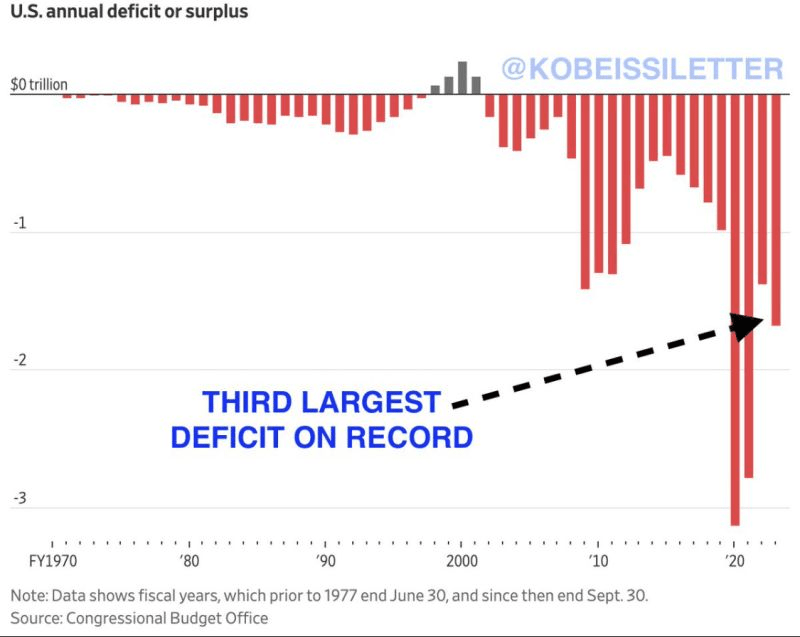

US deficits are the third highest on record.

We might as well have Taylor Swift as Fed Chair. And Travis Kelce as Treasury Secretary replacing TLTL Janet.

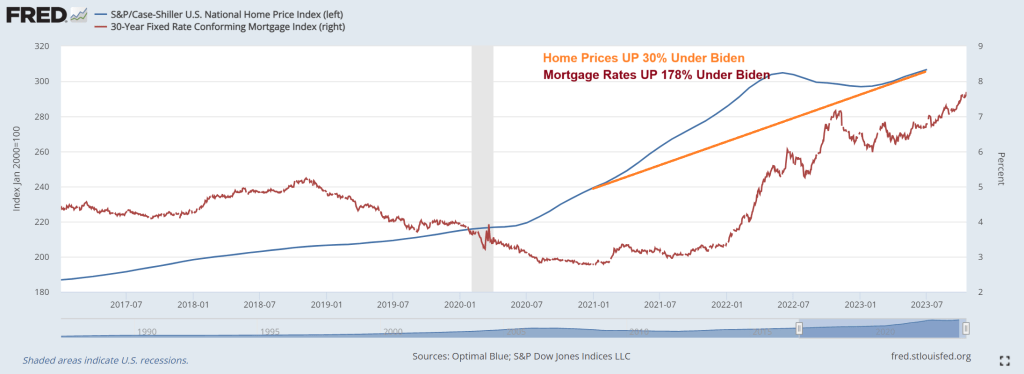

Under Bidenomics, home prices are up 30% while real weekly earnings growth has been negative for most of Biden’s Presidency. And mortgage rates are up 178% under Bidenomics.

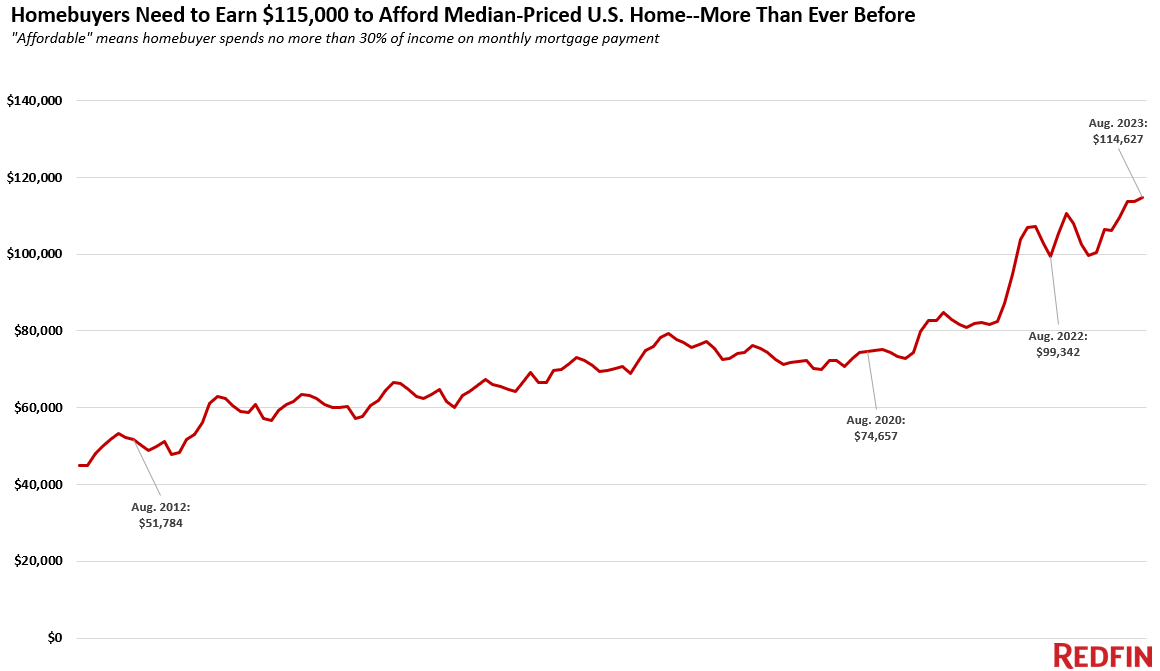

It’s harder than ever for Americans to afford a home.

A homebuyer must earn $114,627 to afford the median-priced U.S. home, up 15% ($15,285) from a year ago and up more than 50% since the start of the pandemic. That’s the highest annual income necessary to afford a home on record.

This is based on a Redfin analysis that compares median monthly mortgage payments for homebuyers in August 2023 and August 2022. The income data in this analysis is adjusted for inflation. See the bottom of this report for more on methodology.

Housing costs are higher than ever because of the one-two punch of sky-high mortgage rates and rising home prices. The average rate on a 30-year fixed mortgage was 7.07% in August. Mortgage rates have climbed even higher since then, hitting 7.57% during the week ending October 12–their highest level in over two decades. But even though soaring mortgage rates have dampened demand, low inventory is causing home prices to increase. The typical U.S. home sold for about $420,000 in August, up 3% year over year and just about $12,000 shy of the all-time high hit in mid-2022.

The typical U.S. homebuyer’s monthly mortgage payment is $2,866, an all-time high. That’s up 20% from $2,395 a year earlier, and by that time payments had already increased substantially from the beginning of the pandemic, a time of ultra-low mortgage rates and yet-to-skyrocket home prices. In August 2020, for instance, the typical monthly payment was $1,581, based on that month’s average mortgage rate of 2.94% and median home price of $329,000. At that time, a homebuyer would have needed to earn $75,000 per year to afford the typical home.

The typical American household earns about $40,000 less than the income needed to buy a median-priced home. The median household income was roughly $75,000 in 2022, the most recent year for which annual income data is available. Hourly wages have risen in 2023, but not nearly as fast as the income necessary to afford a home is rising: The average U.S. hourly wage has increased by about 5% over the last year.

“In a homebuyer’s ideal world, rising mortgage rates would push demand and home prices down enough to make up for high interest payments. But that’s not what’s happening now: Although new listings are ticking up slightly, inventory is still near record lows as homeowners hang onto their low mortgage rates–and that’s propping up prices,” said Redfin Economics Research Lead Chen Zhao. “Buyers–particularly first-timers–who are committed to getting into a home now should think outside the box. Consider a condo or townhouse, which are less expensive than a single-family home, and/or consider moving to a more affordable part of the country, or a more affordable suburb.”

Affordability is less of a problem for all-cash and move-up buyers. The major increase in income necessary to afford a home hits first-time homebuyers hardest. Buyers who can afford to pay cash aren’t impacted by high mortgage rates, and they likely earn more than the income necessary to purchase a home, anyway. Buyers who are selling a home to buy another one are in a better boat than first-timers because they have likely built up equity in their current home, which takes a bit of the sting out of soaring monthly payments. The caveat to the caveat is those who bought at the height of the pandemic-era market with an ultra-low mortgage rate and need to sell now: Not only are they giving up a low rate, they also may have lost money on their home.

Metro-level highlights: Income needed to buy a home has risen in all major metros, with biggest uptick in Miami and smallest in Austin

August 2023, analysis includes 100 most populous U.S. metros for which data is available

Metros where necessary income has increased most: In both Miami and Newark, NJ, homebuyers must earn 33% more than a year ago to afford the typical home–the biggest percent increase of the major U.S. metros. Homebuyers in Miami need to earn $143,000 annually to afford the area’s typical monthly mortgage payment of $3,580, and Newark buyers need to earn roughly $160,000 to afford that area’s $3,989 payment.

Other metros where necessary income has increased by over 30%: The income necessary to afford a median-priced home has increased by over 30% in four other metros, all in the eastern half of the country: Bridgeport, CT ($183,000); Dayton, OH ($60,000); Rochester, NY ($66,000); and Hartford, CT ($95,000).

Buyers need to earn more in every major metro: Skyrocketing mortgage rates have caused the income necessary to buy a home to increase in every major metro, even the places where prices have declined over the last year.

Necessary income has increased least in pandemic homebuying hotspots: Austin, TX homebuyers must earn $126,000 to afford the median-priced home, 8% more than a year ago–the smallest increase of all the major U.S. metros. That’s despite Austin home prices falling 7% year over year in August after they skyrocketed during the pandemic, with remote workers flocking in. Boise, ID, another pandemic homebuying hotspot where demand has since dropped, experienced the next-smallest increase: up 9% to $127,000. Salt Lake City, Fort Worth, TX and Lakeland, FL come next, with year-over-year increases of about 13% each. Home prices are down from a year ago in all those metros.

Homebuyers must earn six figures to buy a home in half the major metros in the country: In 50 of the 100 metros in this analysis, buyers must earn at least $100,000 to afford the median-priced home in their area. Buyers must earn at least $50,000 everywhere in the country.

Bay Area buyers must earn $400,000: Buyers in the most expensive markets in the country–San Francisco and San Jose, CA–must earn more than $400,000 to afford the median-priced home in their area, both up nearly 25% year over year. The next five metros are all in California: Anaheim ($300,000), Oakland ($250,000), San Diego ($241,000), Los Angeles ($237,000) and Oxnard ($233,000).

Rust Belt buyers need the least income–but it’s still up from a year ago: Detroit homebuyers must earn about $52,000 to afford the area’s median-priced home, up 19% from a year ago. That’s the lowest income required to afford a home in the U.S. Next come three Ohio metros (Akron, Dayton and Cleveland) and Little Rock, AR, all of which require roughly $60,000 in annual income to buy a home.

Face it, the US economy and housing/mortgage markets are addicted to gov!

Like President Biden enjoying a barbeque at The White House with a live band (probably NOT Justin Moore singing “Small Town USA”) while Hamas declared war on Israel and Americans are being held hostage with the promise of public executions of hostages livestreamed. Nothing that “Empathy Joe” does ever surprises me anymore, but I am surprise that various Federal Reserve Presidents will speak today while Hamas terrorizes Israeli and US citizens.

It could be that investors think that Talking Heads at The Fed will claim that Fed rate increases are over. Then again, the Iran/Hamas terror campaign against Israel is spookking markets, driving up oil and gold prices and driving up “flight to safety” in US Treasuries.

President Biden called on Americans in Israel to book a commercial flight home, even though Israel has cancelled all flights. Does Old Joe even read the news??

{kind=link}

{kind=link}

You must be logged in to post a comment.