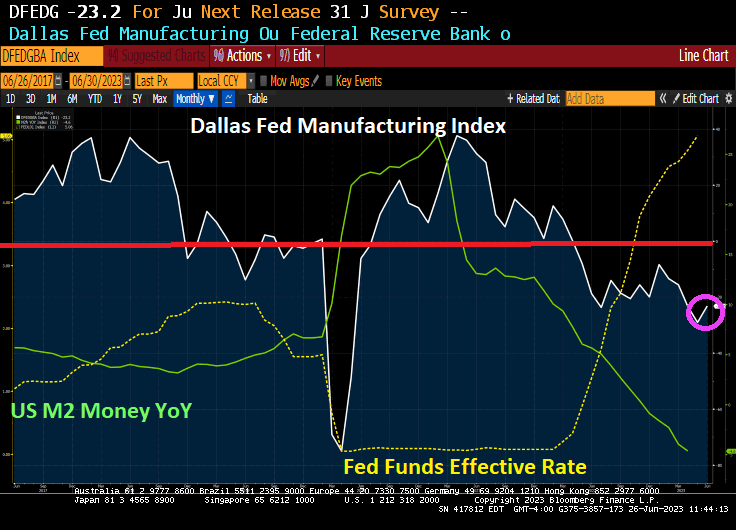

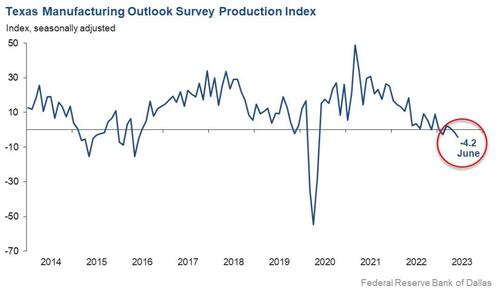

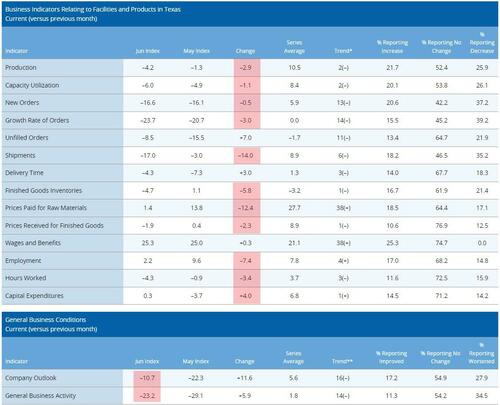

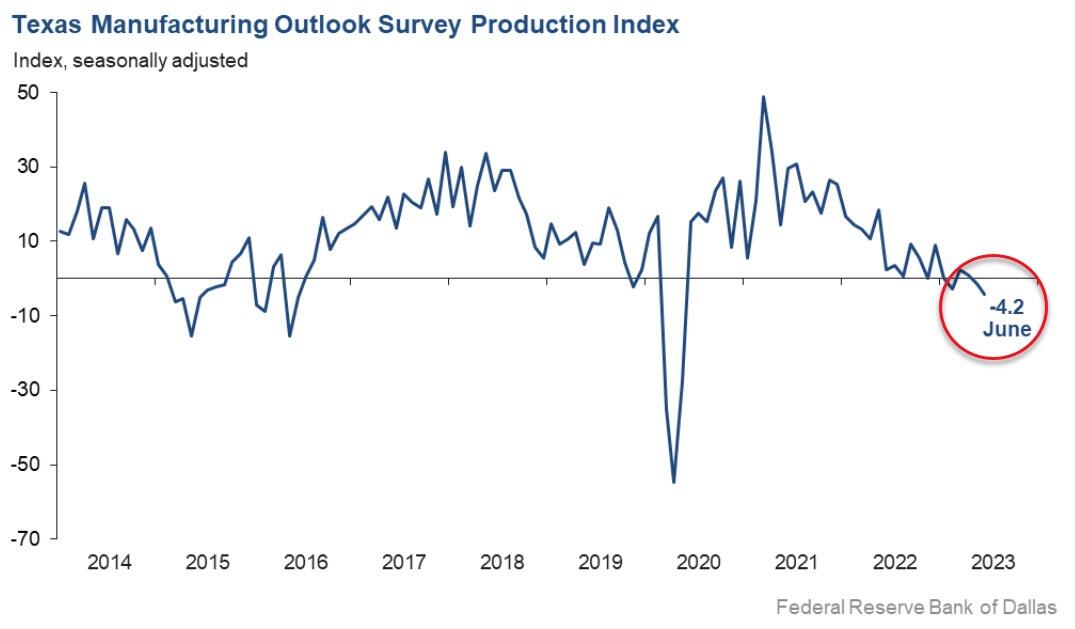

Texas factory activity declined in June, according to business executives responding to the Texas Manufacturing Outlook Survey. The production index, a key measure of state manufacturing conditions, fell three points to -4.2, a reading indicative of a slight contraction in output.

Labor market measures suggest weaker employment growth and declining work hours. Price pressures evaporated, while wage pressures remained elevated…

Yes, the Biden Administration may be the most incompetent administration in US history with Congress a close second. And did I mention CORRUPT??

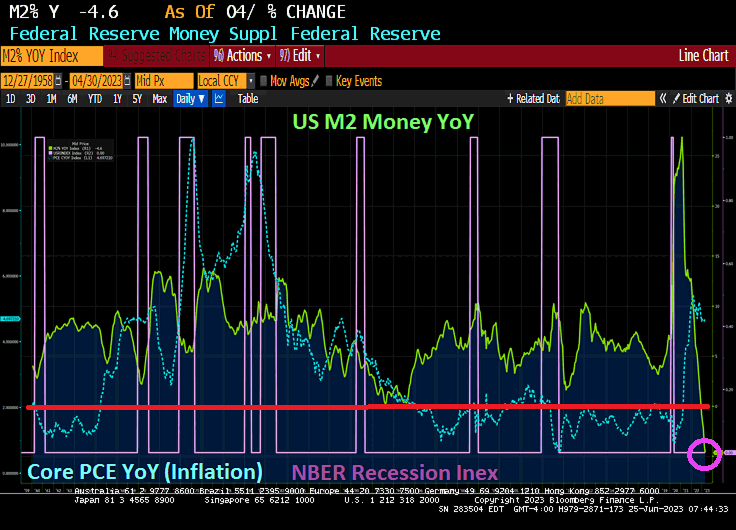

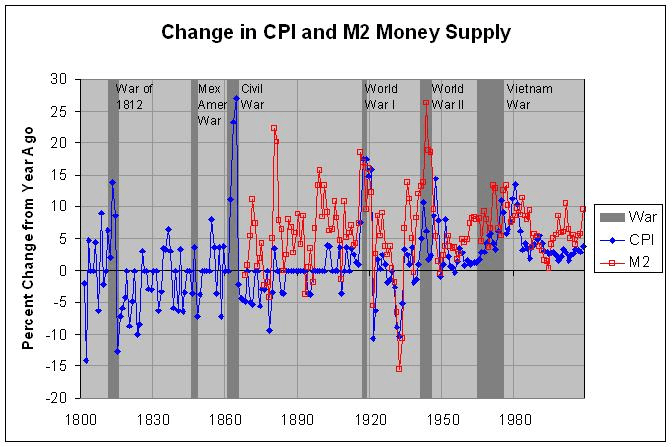

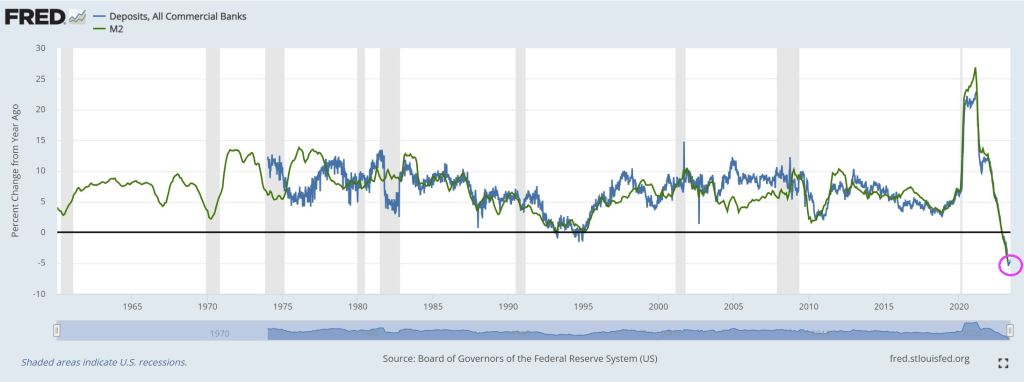

Money supply growth fell again in April from Jerome Powell And The Fed, plummeting further into negative territory after turning negative in November 2022 for the first time in twenty-eight years. April’s drop continues a steep downward trend from the unprecedented highs experienced during much of the past two years.

Yes, The Fed is printing money like it is going out of style! The war on Covid was similar to other wars fought where the US printed boatloads of money to pay for WWI. WWII, Korea and Vietnam wars. And the war against the middle class (known as The Best Depression). Apparently, The Fed is still waging war against the middle class.

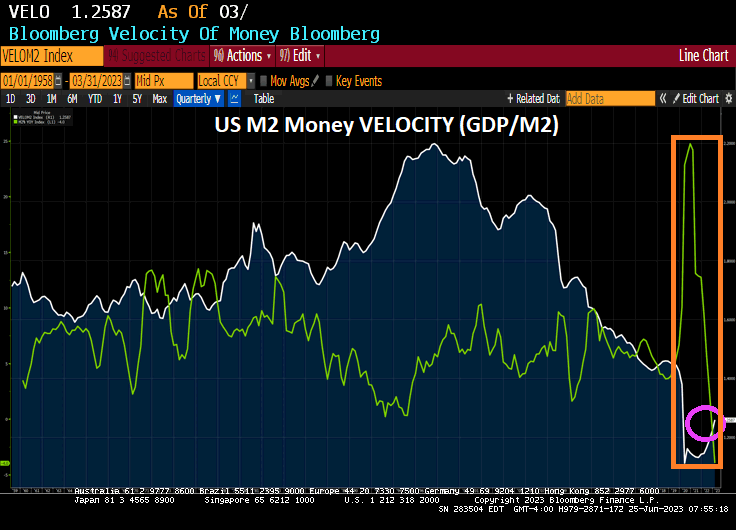

US M2 Money VELOCITY (GDP/M2) is near an all-time low after The Fed went berserk with money printing to combat the Covid economic and school shutdowns.

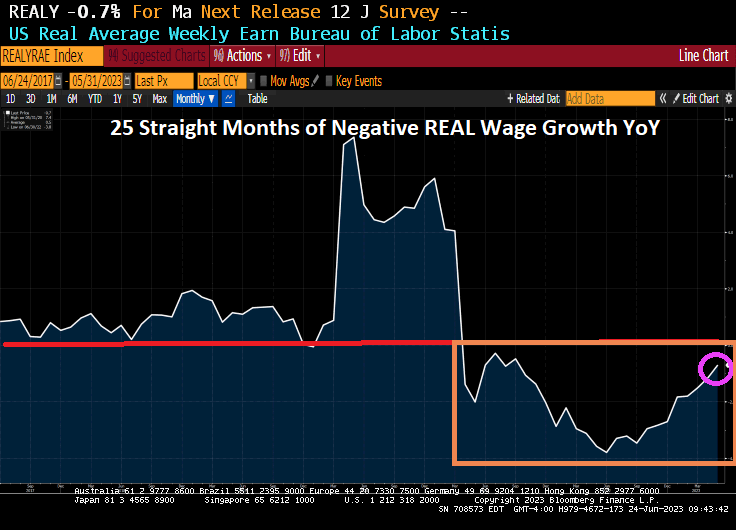

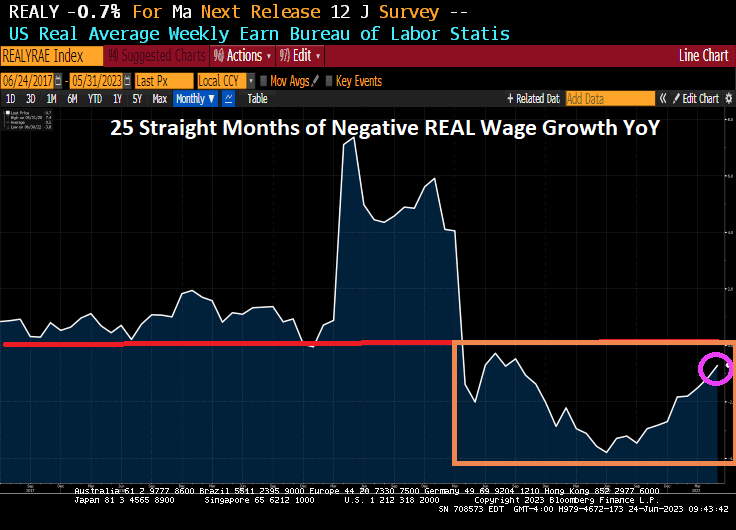

Then with The Fed’s massive monetary expansion and sudden contraction, we have REAL average weekly earnings growth YoY in negative territory for 25 straight months.

The Walking Dead’s Negan, the poster child for The Federal Reserve.

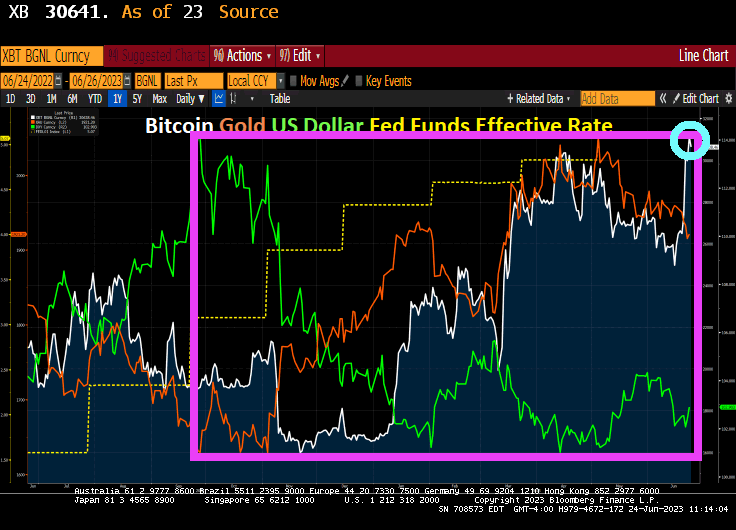

Well, with Jerome Powell And The Fed tightening monetary policy (about half way there!), we have seen competitors to the US Dollar Bitcoin and Gold have soared since September 26, 2022. Bitcoin is up 61%, Gold is up 18% and the US Dollar is down -10%.

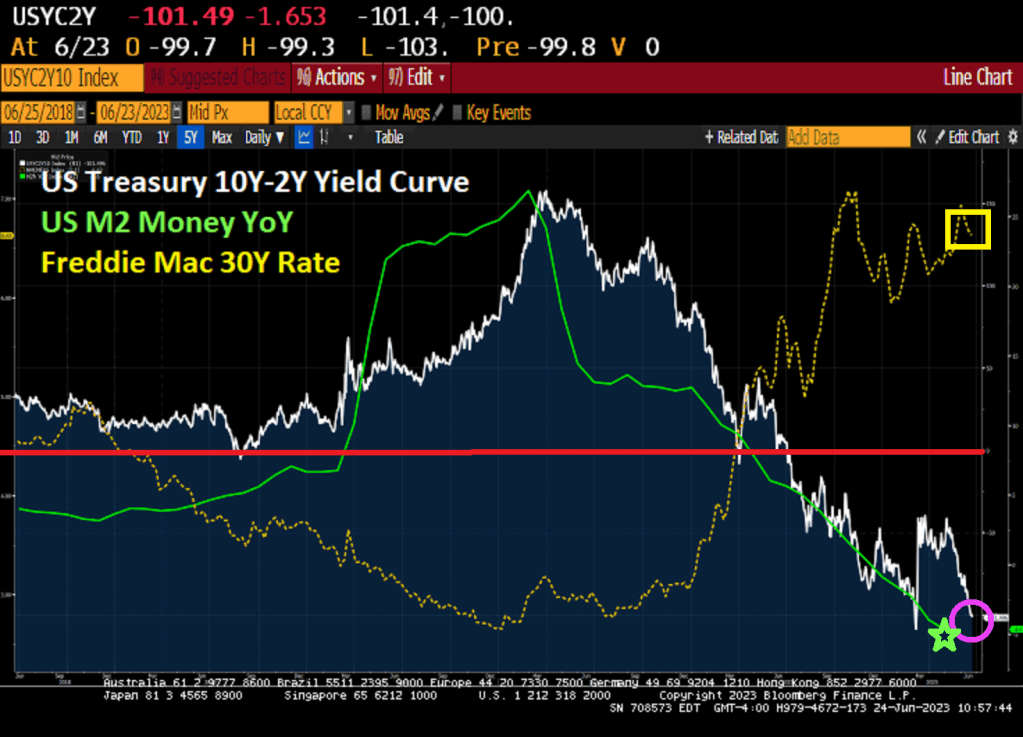

Mortgage rates hover around 7% as the US Treasury 10-2Y curve inverts to over -100 basis points with M2 Money growth crashed and burned.

I could have used 3 shades of Joe, but 50 shades of Joe sounds better!

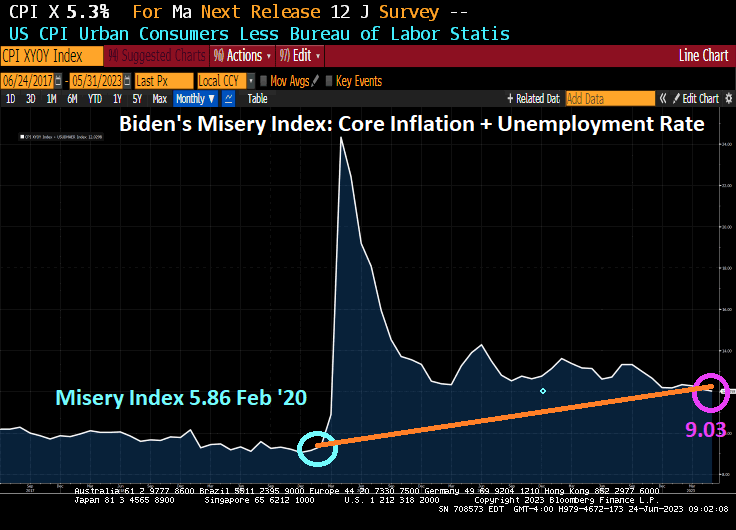

But the fact remains that Americans are far more miserable under Biden than they were under Trump before the Chinese Wuhan Covid virus was unleashed. 9.03 today (Core CPI YoY + U-3 Unemployment) than it was in February 2020 under Trump (5.86). While not twice as bad, inflation is continues to cause serious problems for America’s middle class and low-wage workers.

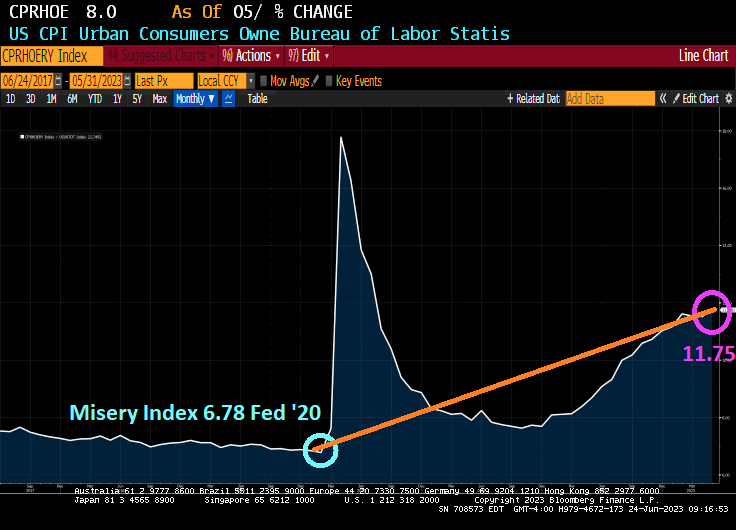

Speaking of the middle class and low wage workers, let’s look at the Renter’s Misery index (CPI Owner’s equivalent rent YoY + Unemployment rate). It was 6.78% in February 2020 under Trump and before Covid struck and is now 11.75% under Inflation Joe.

Speaking of misery, how 25 straight months of negative REAL wage growth? Real weekly wage growth went negative in April 2021, just a few months after Biden was installed as President.

Now, there was winners under Biden. Green energy donors, the big banks, big pharma, big tech, but media … essentially any big donors from big entities got massive payoffs. The middle class and low-wage workers? As Jerry Reid once sang, “They got the coal mine and we got the shaft.”

While I am miserable under Biden and Yellen’s “Reign of Error,” apparently much of the USA is miserable under Biden/Yellen as well compared to the pre-Covid days of Donald Trump. 9.03% misery index (unemployment rate+ core inflation) today compared to 5.86% at the end of 2019 under Trump (before we got Fauci’d and Weingarten’d (the National Teachers’ Union President who pushed public school shutdowns)).

(Bloomberg) If a recession is going to come in the next 12 months — and most economists surveyed by Bloomberg say it probably is — then President Joe Biden should hope it begins sooner rather than later.

The last three one-term presidents — Jimmy Carter, George H.W. Bush, and Donald Trump — have all had their reelection hopes felled by an economic downturn.

But the list of presidents who survived recessions on their watch is just as long. Richard Nixon, Ronald Reagan and George W. Bush all won reelection — in the first two cases by landslides.

The difference, for the most part, is timing.

Two-term presidents get recessions out of the way early. One-term presidents have bad economic news as voters are deciding.

That means a short recession that begins soon — offering the chance for a rebound by Election Day 2024 — might be the best-case scenario for Democrats.

“The historical record suggests that a recession in the second half of 2023 would probably be less damaging to the president’s reelection prospects than a recession in the first half of 2024,” said Larry Bartels, who studies the intersection of politics and economics at Vanderbilt University. But he also said there’s not much that Biden can do at this point to change the direction of the economy in the short term.

The economic projections accompanying the Federal Reserve’s decision to hold interest rates Wednesday suggest that policymakers see less likelihood of a downturn than before. Officials’ median forecast for gross domestic product growth rose from 0.4% to 1% in 2023, with the expansion expected to pick up slightly in 2024 and 2025.

Bond traders responded to the rate decision with a signal that they’re expecting an increased likelihood of a recession in the next year.

A 65% Chance

The typical modern recession lasts 10 months, so an early, short and shallow recession would give Biden time to regain his economic footing. A late, long and deep recession could put Biden among the list of one-term presidents whose time in the White House was cut short by an untimely slump.

The consensus of economists in a Bloomberg survey shows a 65% chance of a recession in the next 12 months, up from 31% a year ago.

The same survey shows an expectation for a return to modest growth in real gross domestic product next year, with growth approaching 2%. That’s tepid in historical terms, but could be a welcome trajectory for Democrats.

“It’s not the absolute level of the economy. It’s the direction of the economy six months out from the elections that really influences the vote,” said Celinda Lake, who served as Biden’s pollster in 2020.

While they’ve largely directed their fire on each other over social and cultural issues, 2024 Republican presidential candidates have criticized Biden’s stewardship of the economy, blaming him for an inflation rate that in mid-2022 reached 9.1%, its highest point in four decades. But that spike has now ebbed to 4% in data out Tuesday.

Former Vice President Mike Pence mentioned “a looming recession” in his campaign announcement video last week, and former President Donald Trump has asserted for nearly a year that the US is already in a recession.

Biden, for his part, isn’t conceding that a recession is inevitable. “They’ve been telling me since I got elected we’re going to be in a recession,” he said earlier this year.

In a campaign speech to union members in Philadelphia Saturday, Biden touted the progress the economy has made since the pandemic recession, and said legislation on infrastructure, clean energy and semiconductors will help build for the long term.

“The investments we’ve made these past three years have the power to transform this country for the next five decades,” he said. “And guess who’s going to be at the center of that transformation? You.”

White House spokesman Andrew Bates said recession predictions “keep turning out like pollsters’ calls before the midterms: wrong.”

But in a Wall Street Journal op-ed this month, Biden also acknowledged that the US “must look out for risks and guard against them.”

Lake said that’s the right tone. “There was a time in the economic conversation when his optimism seemed out of touch with what’s going on,” she said. “Now he says, ‘I get it. It’s good but it’s not good enough.’”

‘Misery index’

Yes, the Misery Index remains elevated under Biden’s “Reign of Error” compared to pre-Covid levels under Trump.

Fed Governor Christopher Waller said Friday headline inflation has been “cut in half” since peaking last year, but prices excluding food and energy (aka, CORE inflation) has barely budged over the last eight or nine months.

“That’s the disturbing thing to me,” Waller said during a question-and-answer session following a speech in Oslo, Norway. “We’re seeing policy rates having some effects on parts of the economy. The labor market is still strong, but core inflation is just not moving, and that’s going to require probably some more tightening to try to get that going down.”

At a separate event Friday, Richmond Fed President Thomas Barkin said inflation remained “too high” and was “stubbornly persistent.”

“I want to reiterate that 2% inflation is our target, and that I am still looking to be convinced of the plausible story that slowing demand returns inflation relatively quickly to that target,” Barkin said in a speech in Ocean City, Maryland. “If coming data doesn’t support that story, I’m comfortable doing more.”

The Federal Open Market Committee paused its series of interest-rate hikes Wednesday, but policymakers projected rates would move higher than previously expected in response to surprisingly persistent price pressures and labor-market strength.

The consumer price index this week showed headline inflation slowed, but core prices excluding food and energy continued to rise at a pace that’s concerning for Fed officials. Employers continued adding jobs at a rapid clip in May, and job openings climbed in April, recent data showed.

Barkin warned that prematurely loosening policy would be a costly mistake.

“I recognize that creates the risk of a more significant slowdown, but the experience of the ’70s provides a clear lesson: If you back off inflation too soon, inflation comes back stronger, requiring the Fed to do even more, with even more damage,” he said. “That’s not a risk I want to take.”

Policy Report

Separately, the Fed released a new report Friday that said tighter US credit conditions following bank failures in March may weigh on growth, and that the extent of additional policy tightening will depend on incoming data.

“The FOMC will determine meeting by meeting the extent of additional policy firming that may be appropriate to return inflation to 2% over time, based on the totality of incoming data and their implications for the outlook for economic activity and inflation,” the Fed said in in its semi-annual report to Congress.

Read More: Fed Says Tighter Credit Conditions to Weigh on US Growth

The Fed report, which provides lawmakers with an update on economic and financial developments and monetary policy, was published on the central bank’s website ahead of Chair Jerome Powell’s testimony before the House Financial Services Committee on June 21. He will appear before the Senate banking panel the following day.

“Evidence suggests that the recent banking-sector stress and related concerns about deposit outflows and funding costs contributed to tightening and expected tightening in lending standards and terms at some banks beyond what these banks would have reported absent the banking-sector stress,” the report said.

Between work at home, Bidenflation and The Feral Reserve, commercial real estate and regional banks are suffering … and it could get a lot worse. And Joe Biden (aka, Negan) in general. Living in Negan Country!

The work-from-home trend has been taking its toll on office landlords and is now making its way through to banks’ commercial loan portfolios, leading some analysts to predict that more trauma could be on the way for regional banks this year.

And in the current climate of bank failures, short sellers, and nervous depositors, banks with large exposures to commercial real estate (CRE) loans are racing to clean up and sell down their loan portfolios in hopes that they will not fall victim to another round of bank runs.

“There is an estimated $1.5 trillion of commercial property debt that will be due for repayment in about 18 months,” Peter Earle, an economist at the American Institute for Economic Research, told The Epoch Times. “It’s not improbable that even if interest rates have fallen by that time, some of that real estate debt will nevertheless be impaired and have an adverse impact on regional banks.”

In step with a recent trend in the CRE market, tech giant Google announced in May that it was attempting to sublease 1.4 million square feet of vacant office space in its Silicon Valley home base in order to “match the needs of our hybrid workforce.” Despite more employees returning to their offices this year, average office occupancy rates across the United States are still below 50 percent.

According to a report by Bank of America, 68 percent of CRE loans are held by regional banks. Approximately $450 billion in CRE loans will mature in 2023. JPMorgan Chase estimated that CRE loans comprise, on average 28.7 percent of the assets of small and regional banks, and projected that 21 percent of CRE loans will ultimately default, costing banks about $38 billion in losses.

Double Hit (of Biden’s Policies) Commercial mortgages are getting hit on two fronts: first, by the lack of demand for office space, leading to credit concerns regarding landlords, and second, by interest rate hikes that make it significantly more expensive for borrowers to refinance.

According to a June 12 report by Trepp, a CRE analytics firm, CRE loans that were originated a decade ago, when average mortgage rates were 4.58 percent, are now coming due, and in today’s market, fixed-rate CRE loan rates are averaging around 6.5 percent.

Banks that make CRE loans consider factors like debt service coverage ratios (DSCRs), which measure a property’s income relative to cash payments due on loans. Simulating mortgage interest rates from 5.5 percent to 7.5 percent, Trepp projected that between 28 percent and 44 percent, respectively, of currently outstanding CRE loans would fail to meet the 1.25 DSCR ratio today, and thus be ineligible for refinancing.

These calculations were done assuming current cash flows from properties stay the same and that loans are interest-only, but with vacancies rising, many landlords may have substantially less cash flow available. In addition, whereas interest-only CRE loans were 88 percent of the market in 2021, lenders are now switching to amortizing mortgages to reduce risk, which significantly increases debt service payments.

Refinancing Issues Fitch, a rating agency, projected that approximately one-third of commercial mortgages coming due between April and December of this year will be unable to refinance, given current interest rates and rental income.

“It’s a very different world now from the one in which the majority of these loans were made,” Earle said. “In a zero-interest-rate environment, before the COVID lockdowns saw many businesses shift to a remote work basis, many of these loan portfolios full of office properties looked great. Now, a substantial portion of them look quite vulnerable.”

The Trepp report highlighted several regional markets, such as San Francisco, where office sublease offers jumped 140 percent since 2020, and Los Angeles, where office vacancies hit a historic high of 22 percent. Available office space in Washington D.C. increased to 21.7 percent in the first quarter of 2023.

New York has been hit hard, as well. Office occupancy rates in New York City plummeted from 90 percent to 10 percent in 2020 during the COVID pandemic, but only recovered to 48 percent this year. Revenue from office leases fell by 18.5 percent between December 2019 and December 2022.

Vacancy Rates at 30-Year High Overall, according to a report by analysts at New York University and Columbia Business School, office vacancy rates are at a 30-year high in many American cities.

The report found that “remote work led to large drops in lease revenues, occupancy, lease renewal rates, and market rents in the commercial office sector.”

The authors predict that, even if office occupancy returns to pre-pandemic levels, “we revalue New York City office buildings, taking into account both the cash flow and discount rate implications of these shocks, and find a 44% decline in long run value. For the U.S., we find a $506.3 billion value destruction.”

As predicted, delinquencies in commercial mortgage loans are now creeping up. Missed payments in commercial mortgage-backed securities (CMBS) increased half a percent in May over the prior month to 3.62 percent, Trepp reports. The worst component of the CMBS market, which includes multi-unit rental buildings, medical facilities, malls, warehouses, and hotels, was offices, where delinquencies increased 125 basis points to more than 4 percent.

To put this in perspective, however, CMBS delinquencies exceeded 10 percent in 2012 and 2020. And analysts say that lending criteria for CRE have been more conservative than they were before the mortgage crisis of 2008, leaving more cushion on ratios relative to a decade ago.

All the same, the credit crunch at regional banks has created a vicious circle, where banks race to pare down their CRE portfolios, and the dearth of financing leaves more landlords facing default as outstanding loans mature. To make matters worse, commercial property values, which provide collateral for the loans, appear to be taking a hit as well.

In an effort to rapidly clean up their CRE loan portfolios and avoid the fate of failed banks like Silicon Valley Bank, Signature Bank, and First Republic Bank, banks are now attempting to sell off the loans, often taking a loss in the process.

In May, PacWest, a regional bank, sold $2.6 billion of construction loans at a loss. Citizens Bank reportedly has put $1.8 billion of its CRE loans up for sale during the first quarter of this year. Customers Bancorp reduced its CRE lending by $25 million and put $16 million of its existing portfolio up for sale.

Wells Fargo, one of the top four largest U.S. banks, is also downsizing its CRE portfolio, and in announcing the move CEO Charlie Scharf stated, “we will see losses, no question about it.”

“Between the Fed’s 500+ basis point hikes over the past 16 months and the failure of Silicon Valley Bank, and others, earlier this year, a credit tightening is already underway,” Earle said. “That has put a lot of pressure on regional lenders.”

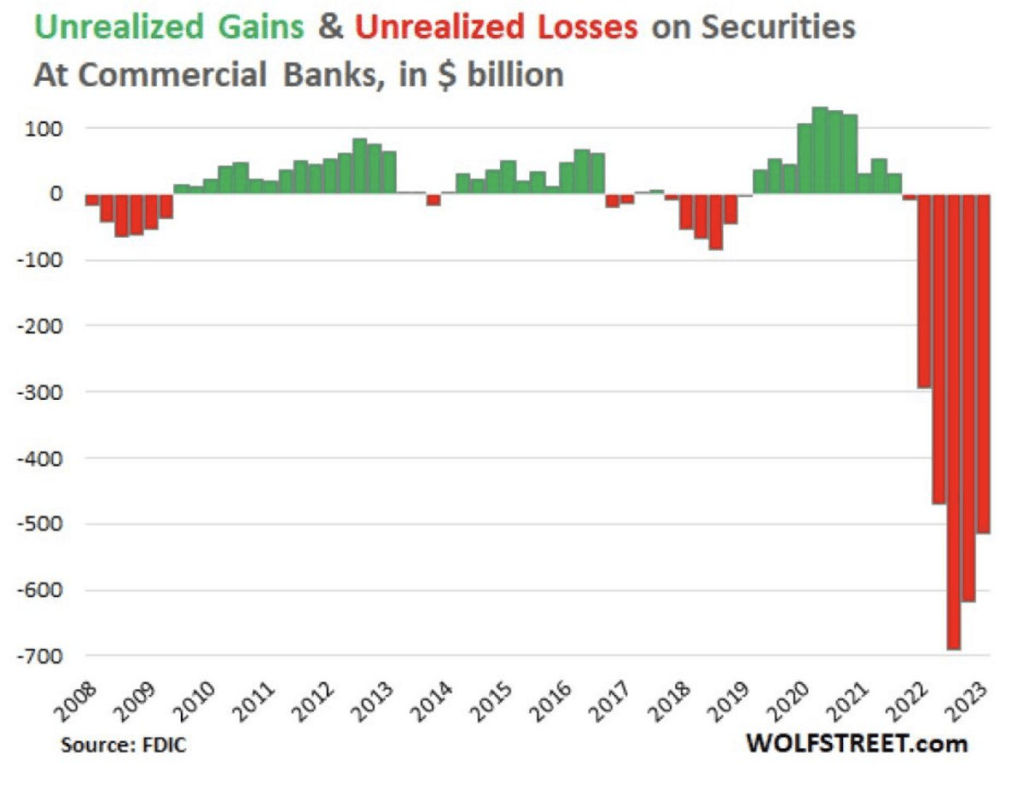

A March academic study titled “Monetary Tightening and U.S. Bank Fragility in 2023” stated that the market value of assets held by U.S. banks is $2.2 trillion lower than what is reported in terms of their book value. This represents an average 10 percent decline in the market value of assets across the U.S. banking industry, and much of this decline came from commercial real estate loans.

Consequently, the authors wrote, “even if only half of uninsured depositors decide to withdraw, almost 190 banks with assets of $300 billion are at a potential risk of impairment, meaning that the mark-to-market value of their remaining assets after these withdrawals will be insufficient to repay all insured deposits.”

Nicolas Maduro of Venezuela must be envious of Joe Biden. I don’t think even Maduro has the stones to have his politiical opponent charged with espionage in the run-up to a Presidential election. Particularly when the US President has been bribed by China and Ukraine and has similiar sensitive document hoarding issues (at least Trump didn’t leave boxes of sensitive documents in a garage like Biden did when he keeps his Chevy Corvette).

So where do we sit today after Biden has signed the debt ceiling increase and massive spending splurge?

First, look at the crashing bank deposit problem. Well, the solution is for The Fed to fire up the money printing press! Keep on printing!

This not surprising if you have read Nobel Laureate George Stigler’s treastise on regulatory capture. Essentially, big corporations (big media, big tech, big banking, big pharma, big defense, big agriculture, etc.) essentially own Congress, the Biden Administration and Federal regulators. After all, Biden has been bribed with millions of dollars by China and Ukraine and, like a Banana Republic, has is avoiding prosecution and instead prosecuting his political opponent, Trump. Don’t worry, if they get Trump that will indict DeSantis for something.

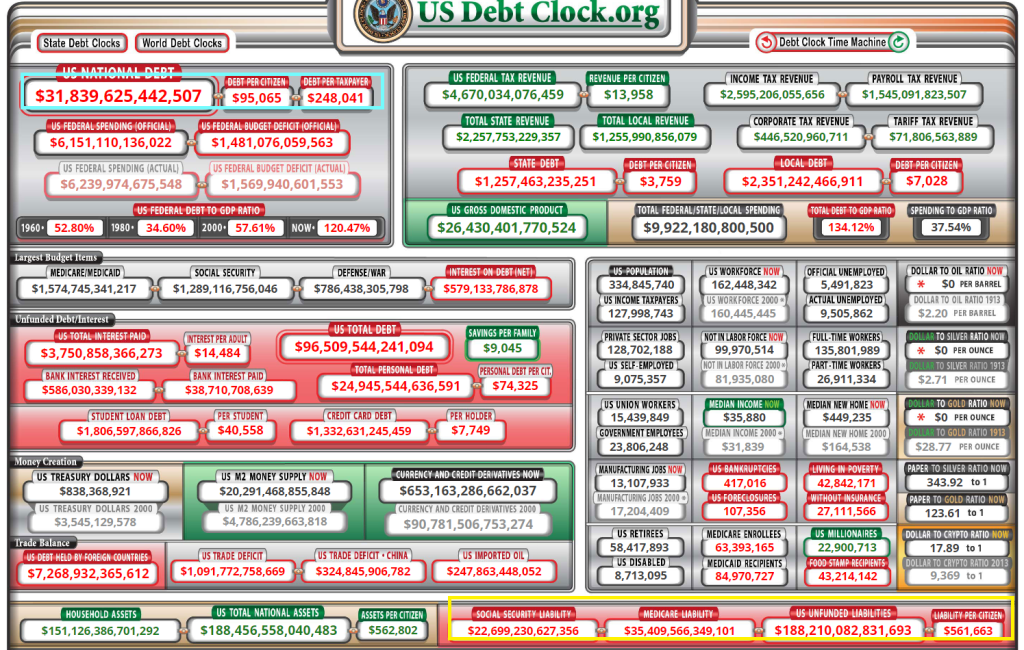

US debt stands at $31.8 TRILLION with $188 TRILLION in unfunded liabilities (which means higher personal taxes and much more debt).

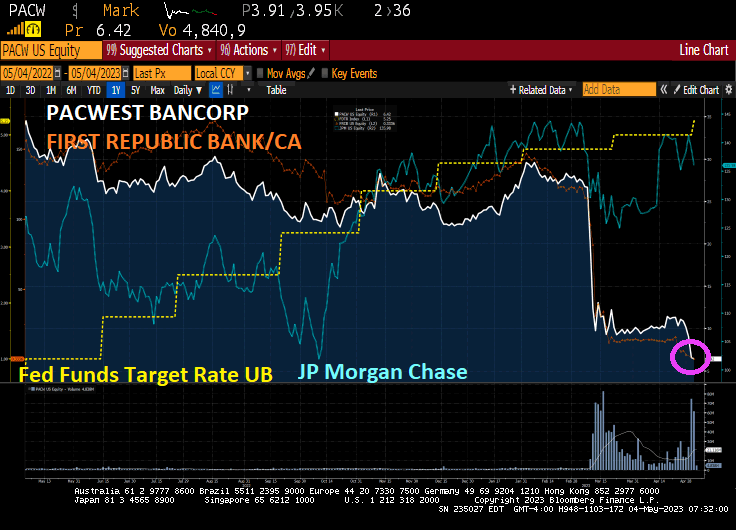

As Connor MacLeod said in the film Highlander, “There can only be one!” The US banking system under Joe Biden’s Reign of Error is like the film Highlander: apparently, there can only be one bank. And it is likely JP Morgan Chase.

Take the JP Morgan Chase (JPMC) acquisition of First Republic Bank:

In Acquiring First Republic Bank, JP Morgan Has:

Bypassed laws against acquiring bank while controlling 10%+ of US deposits

Shared $13 billion in losses with the FDIC

Received a $50 billion loan from the FDIC

Effectively bought back its own deposits

Expects to profit $5 billion+ over the next 5 years

This crisis has taught us that rules don’t matter in times of panic, particularly to regulators.

And now we have PacWest Bancorp. Lender says it’s been approached by potential investors. Bill Ackman warns US regional banking system at risk.

The turmoil at PacWest shows how investor angst still remains elevated after a string of failures and deposit outflows in the sector despite Federal Reserve Chair Jerome Powell’s assurance Wednesday that authorities were closer to containing the crisis. It’s reignited the debate over whether more US regional lenders will fall after this year’s collapse of SVB Financial Group’s Silicon Valley Bank, Silvergate Capital Corp., Signature Bank and most recently First Republic Bank.

Smaller banks are under pressure after a year of interest-rate hikes hammered the value of their bond holdings and drove unrealized losses to an estimated $1.84 trillion. Trouble in commercial real estate is adding to the pain, while depositors take their money out to seek better returns elsewhere. These stresses have put the spotlight on these lenders, which typically have fewer resources to defend themselves.

We are seeing a consolidation of the banking system .. again as smaller and regional banks fail and get gobbled up by the Too-Big-To-Fail (TBTF) banks like … JP Morgan Chase.

Biden’s Reign of Error is not over yet. His campaign slogan (which was also Bill Clinton’s campaign reelection slogan) is “Finish the job!” With Biden’s idiotic mortgage idea of punishing borrowers with good credit and giving subsidies to those with bad credit, Biden is trying to finish off the US economy and banking system.

Here is a chart of US office vacancies nationally (yellow), New York (white), San Franciso (green) and Los Angeles (orange). Note the rapid decline in office vacancies just prior to the financial crisis (often mislabeled as the subprime mortgage crisis). Then look at office vacancies after The Fed’s massive monetary experiment of setting rates to near zero and buying a ton of Treasuries, Agency MBS. etc. While San Francisco returned to pre-financial crisis levels of office vacancy, in general the office market never fully recovered.

And then “the slammer” struck: the COVID economic shutdowns. After 2020 shutdowns, office vacancy rates rose dramatically. Two complicating factors: 1) the US moved to working at home rather than commuting to an office and largely remains that way. 2) crime is going bonkers in American cities, particularly New York, Los Angeles and San Francisco (don’t worry, I haven’t forgotten about other gang nests like Chicago and Detroit). I saw that California’s woke governor Gavin “Nancy Pelosi’s nephew” Newsom said the word “gang” then apologized and replaced it with “organized groups.” No wonder Newsom can’t fix anything, but he is running for President of the US! (insert Edvard Munch’s “The Scream” painting here,)

The Fed responded to the financial crisis by lower rates to 25 basis points and printing a boat load of money. Unfortunately, office vacancies rose to a peak in October 2010 then began falling again. Only to start rising again after Trump took office in 2017. Alas, Covid struck in 2020, The Fed and Federal government panicked. States and local governments (not to mention teacher’s unions) shut down economies and schools. Office vacancies are now higher than at peak of the Covid shutdowns!!!

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.