Instead of The Boston Strangler, we now have the DC Strangler. Better known as The Federal Reserve and their war on inflation.

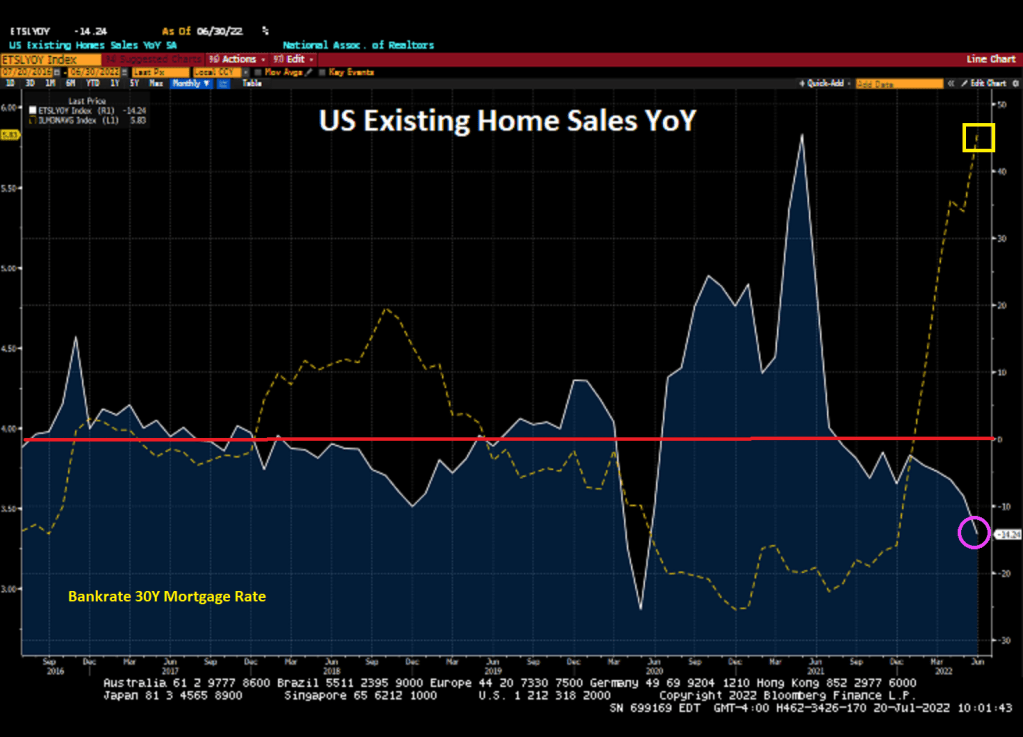

US existing home sales crashed -14.24% YoY and -5.40% MoM in June as The Fed tightens its icy grip on the housing market. Existing home sales were lower than expected at 5.12 million home sold SAAR.

Median price for existing home sales declined to 13.27% YoY as inventory available for sale remains MIA. And The Fed’s balance sheet is still out in force.

The US housing market in terms of sales has entered a bear market, but with The Fed’s balance sheet stimulus still hunting asset prices, it is a grizzly bear market in terms of affordability.

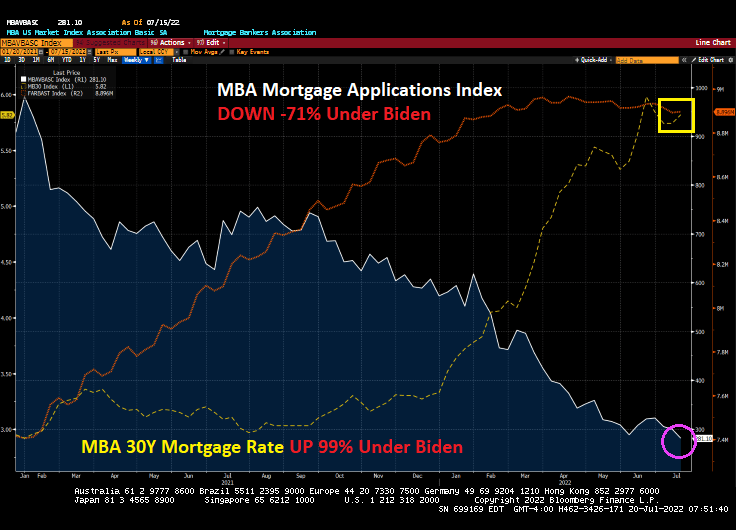

Mortgage applications declined for the third week in a row, reaching the lowest level since 2000.

Mortgage applications decreased 6.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 15, 2022.

The Refinance Index decreased 4 percent from the previous week and was 80 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 7 percent from one week earlier. The unadjusted Purchase Index increased 16 percent compared with the previous week and was 19 percent lower than the same week one year ago.

Heartache #1: Mortgage rates have risen 99% under Biden.

Heartache #2: Mortgage application have fallen -71% under Biden.

As The Federal Reserve continues to fight inflation caused by 1) excessive stimulus by The Federal Reserve and Federal government surrounding Covid and 2) Biden’s energy policies, we are seeing the mortgage market as collateral damage.

Mortgage rates are rising in part thanks to The Federal Reserve trying to control inflation (caused by Biden’s energy policies and spending). But mortgage rates are down slightly today.

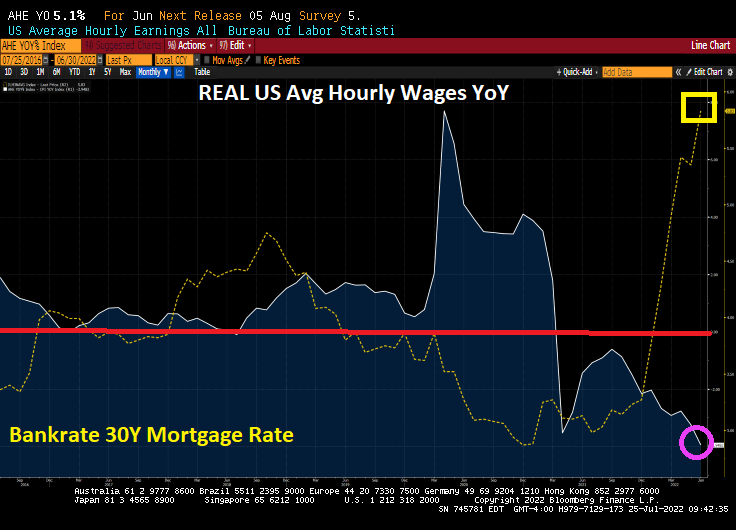

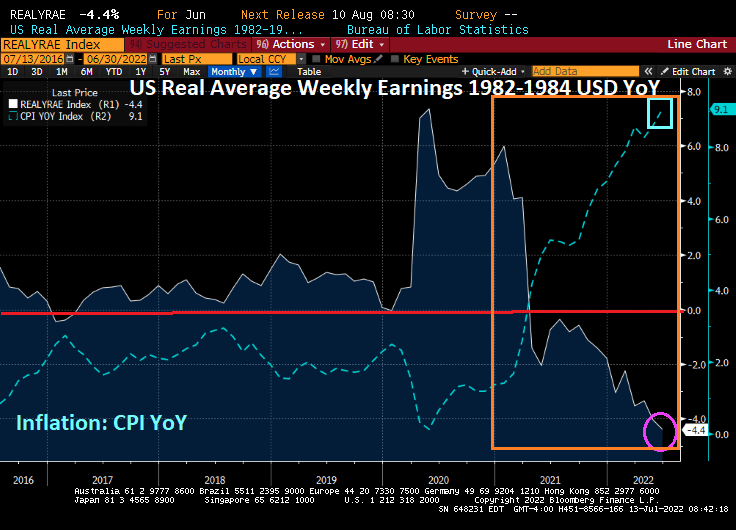

Bear in mind that REAL wage growth is negative, thanks to Bidenflation.

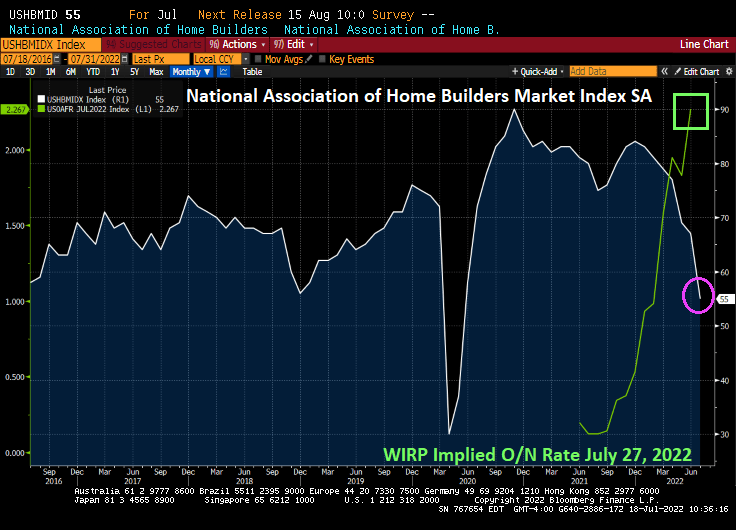

As The Fed Reserve prepares to raise their target rate in a week by 75 basis points to 2.50%, the NAHB Home Builder’s confidence index plunged.

The 30-year mortgage rate is up 89% under Biden as his green energy fiasco is helping drive inflation to its highest level in 40 years leading The Fed to tighten its monetary policies.

We are all aware that inflation is soaring, since the Covid outbreak in 2020 and the massive overaction by The Federal Reserve and Federal government in terms of stimulus spending and economic lockdowns.

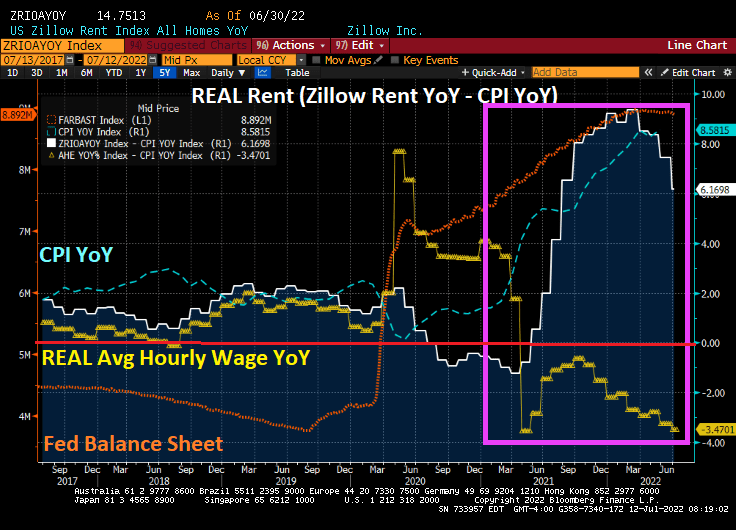

Things were “normal” before Covid in that REAL housing rent (white line) and REAL average hourly earnings YoY (yellow line) moved together. But after Covid shutdowns and Federal stimulus “relief” (orange line), we see that inflation (blue line) took off along with the growth in housing rent. The problem, of course, is that REAL average hourly earnings YoY has been declining. I call this “The Great Divide in housing affordability”.

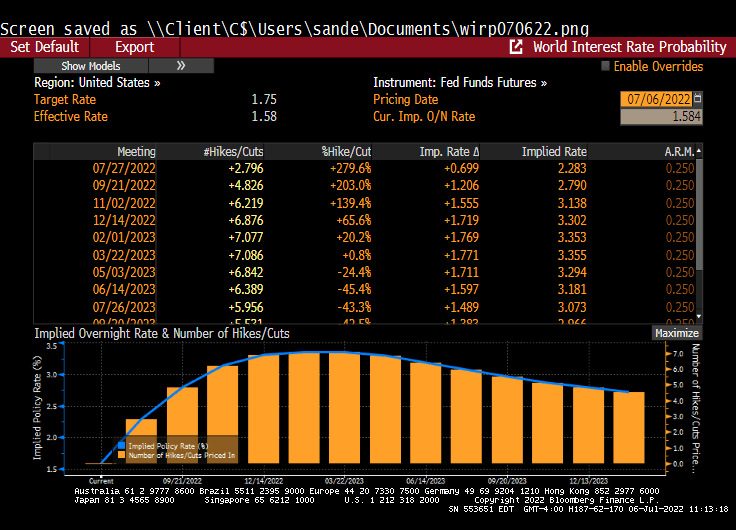

The question, of course, is whether The Federal Reserve will continue their “war on inflation” with a 75 basis point rate increase.

Inflation is at its fastest pace in 40 years, and is expected to increase even higher in tomorrow’s inflation report.

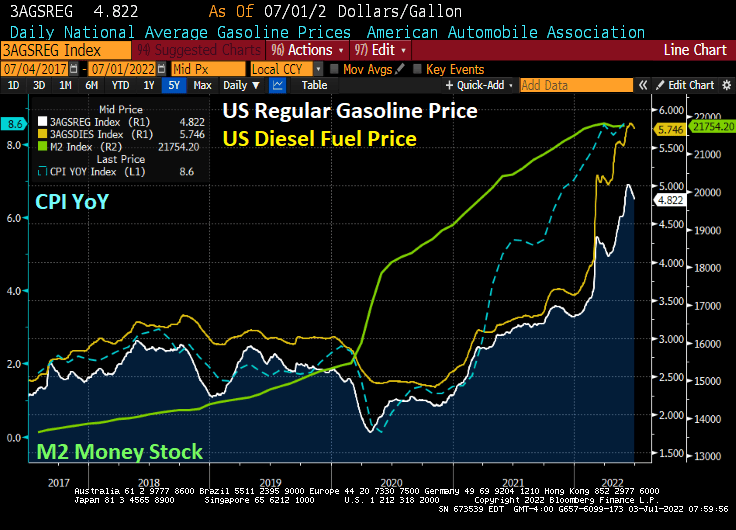

Gasoline prices have been dropping recently, but remain above $4.50 per gallon (regular gas price was $2.40 per gallon on Biden’s inauguration day. And no, it wasn’t the Biden Administration selling nearly 1 million barrels of crude oil from the strategic petroleum reserve to the Chinese government-owned Sinopec that Biden’s son Hunter is an investor (so, The Big Guy aka Joe Biden gets a 10% piece of the action). It is a slowing global economy that is helping to lower gasoline prices.

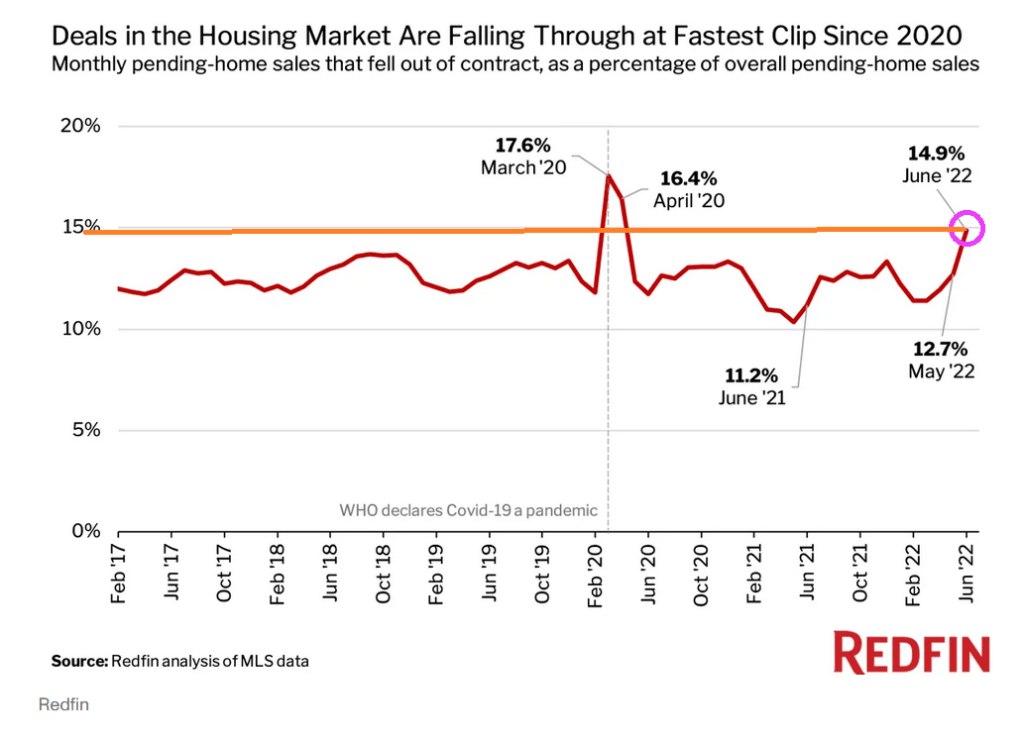

With rising mortgage rates, we are seeing a surge in pending home sales cancellations.

Atlanta Fed’s Raphael Bostic thinks that the US economy is so strong that it can easily handle a 75 basis point increase at the next FOMC meeting. Fortunately, he is not a voting member.

Generally speaking, The Federal Reserve cuts rates as a recession approaches. But not this time!

The Federal Reserve is expected to raise their target rate by 75 basis points at the next FOMC meeting.

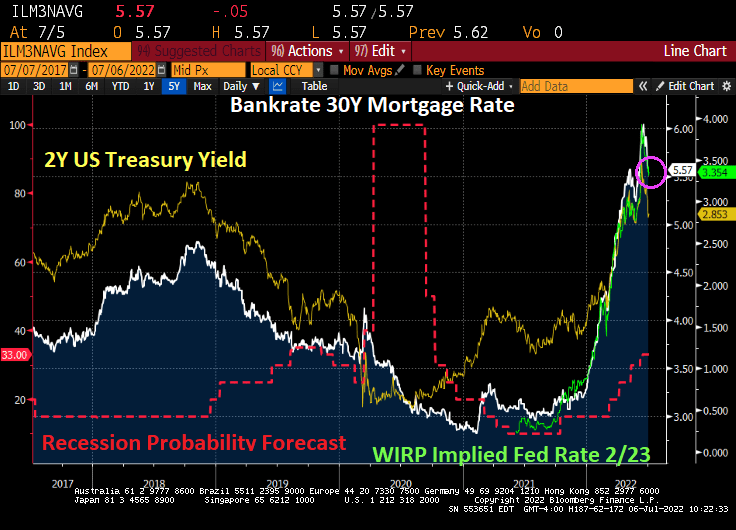

We are already seeing Fed rate hikes being priced into the mortgage markets, as Bankrate’s 30-year mortgage rate fell to 5.57% after rising above 6% in June. The reason? Recession fears have caused Treasury yields to fall.

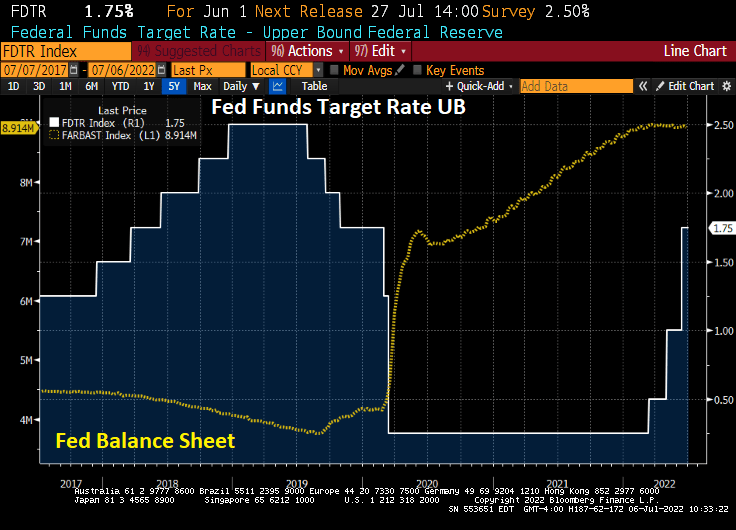

The Fed is hiking their target rate, but has been sloth-slow in unwinding their balance sheet.

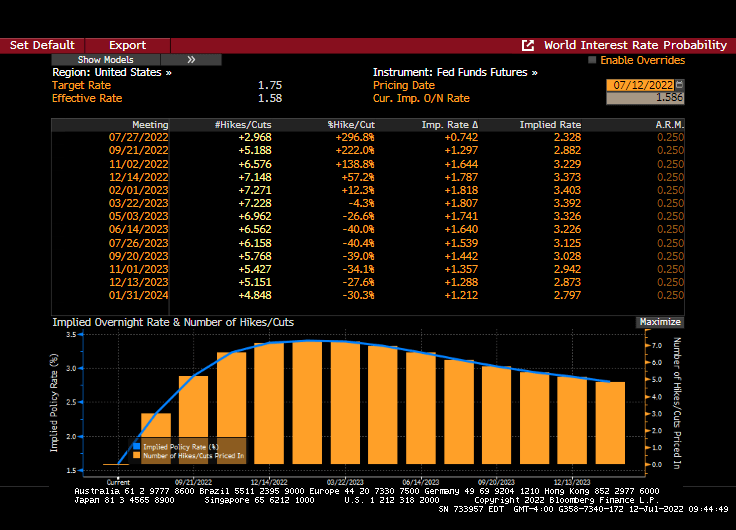

Yes, The Fed has been sloth-slow in removing the Covid-related stimulus. But is The Fed trying to pull a “Volcker” by raising rate to choke off inflation EVEN IF THE ECONOMY ENTERS RECESSION? Fed Funds Futures data is pointing to a reversal of Fed rate hikes by Feb 2023.

Here is Fed Chair Jerome Powell showing the amount of Covid-related stimulus removed recently.

TED refers to the difference between the three-month Treasury bill and the three-month LIBOR based in U.S. dollars, a measure of fear in the market.

The 3-month TED spread is rising awfully fast. A sign of impending recession.

US bank credit default swaps (CDS) are rising fast as inflation gets ugly.

The US Treasury 10Y-3M curve is bumping against the zero barrier.

I am still shaking my head at President Biden chastising gasoline stations for not lowering prices at the pump when refiners are near full capacity and the Biden Administration is doing nothing to increase the supply of US-source non-green energy.

Hey, I thought Mayor Pete Buttigieg, the US Transportation Secretary, was supposed to unclog the supply-chain crisis! Instead, we get heartaches on heartaches as diesel prices rise 118% under Biden AND now the bottle-necks may get a lot worse.

A US Supreme Court decision that could force California’s 70,000 truck owner-operators to stop driving is set to create another choke point in already-stressed West Coast logistics networks, a truckers’ organization said.

“Gasoline has been poured on the fire that is our ongoing supply-chain crisis,” the California Trucking Association said in a statement following the Supreme Court’s decision to deny a judicial review of a decision of a lower court, a process known as certiorari.

“In addition to the direct impact on California’s 70,000 owner-operators who have seven days to cease long-standing independent businesses, the impact of taking tens of thousands of truck drivers off the road will have devastating repercussions on an already fragile supply chain, increasing costs and worsening runaway inflation,” the CTA said.

The association asked the Supreme Court for a review of a case challenging California’s Assembly Bill 5, a law that sets out three tests to determine whether a worker is an employee entitled to job benefits or an independent contractor who isn’t. The trucking industry relies on contractors, and has fought to be exempt from state regulations for years because of federal law.

With few exceptions, the relationship between independent truckers and their carriers, brokers and shippers will be governed by the tests.

As if US consumers aren’t getting crushed by rising prices already. In response to the Covid outbreak, The Fed slammed its foot on the money accelerator along with Federal government stimulus. Throw in Biden’s anti-drilling executive orders, and we have a nightmare.

Consumer confidence is already crumbling under inflation and rising energy prices.

You must be logged in to post a comment.