Another dismal economic report under “Middle class” Joe Biden.

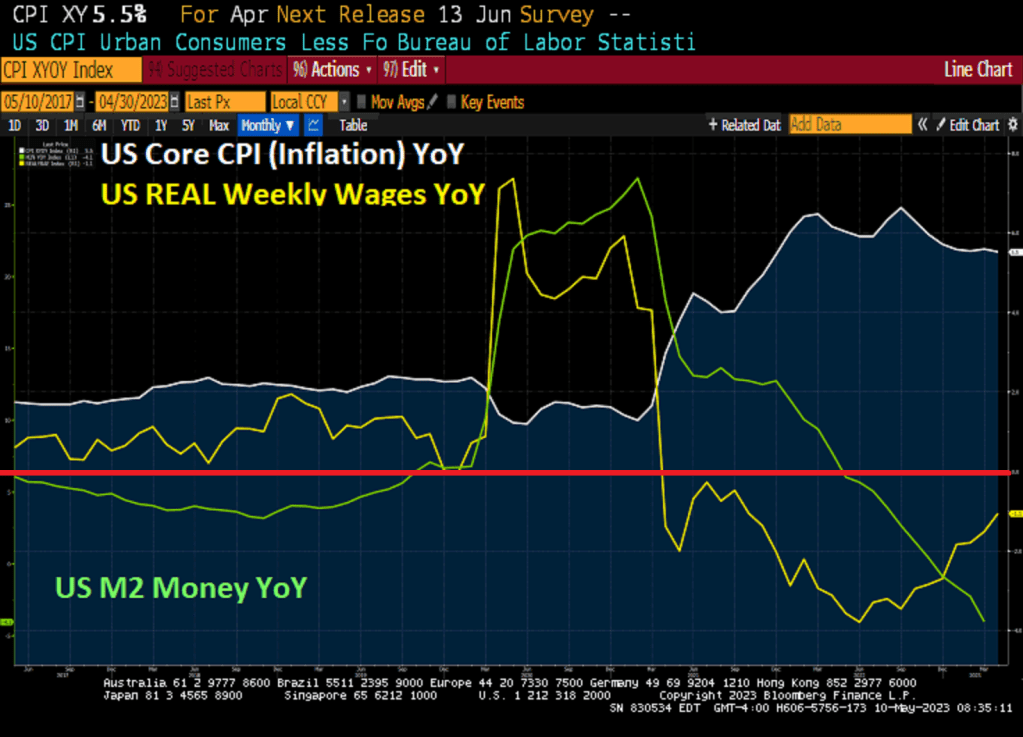

April’s inflation report is out and … it sucks. Core inflation (CPI less food and energy) remains elevated at 5.5% YoY, much higher than The Fed’s target rate of 2%. Even worse, US REAL average weekly wage growth is negative again at -1.1% YoY, negative growth for the 25th straight month.

Turns out that core inflation is higher than overall inflation. 4.9% YoY compared to core of 5.5% YoY.

Despite the hot core inflation report, Fed Funds Futures are pointing to declining rates over time.

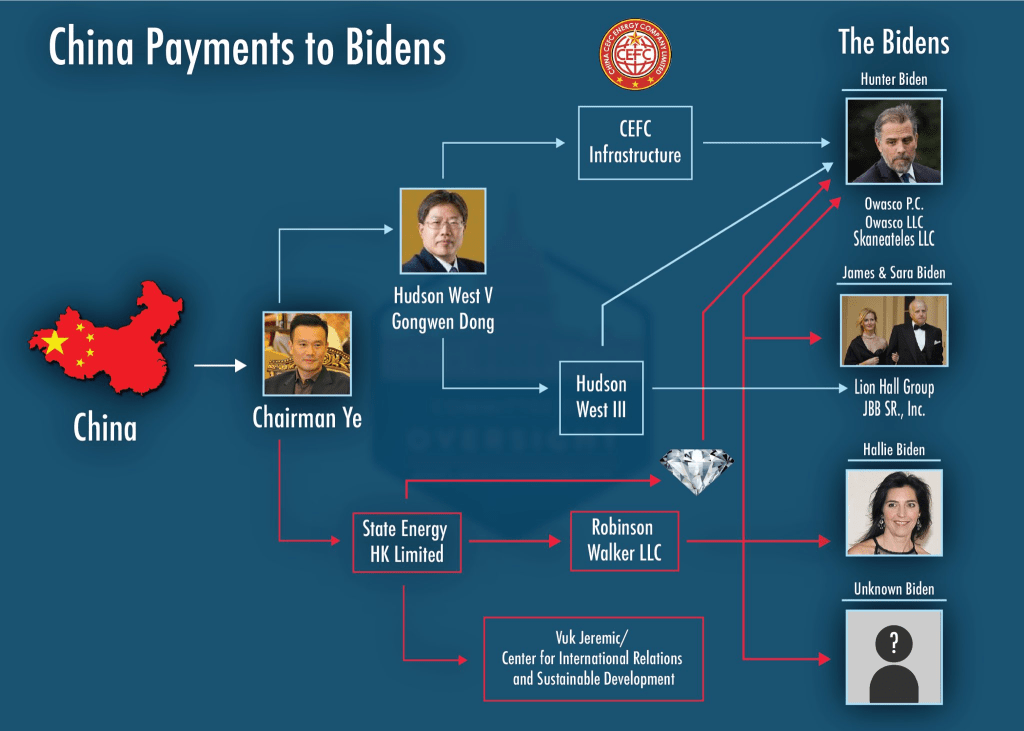

While the US middle class is getting screwed, The Biden family are raking in millions …. from China.

Resident Biden has been an unmitigated disaster for the US middle class, but fantastic for BIG corporate America and the donor class.

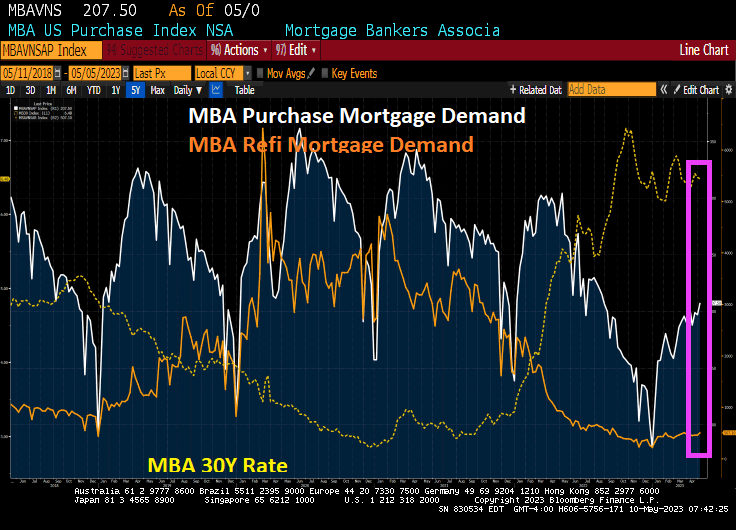

Mortgage applications increased 6.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 5, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 6.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 7 percent compared with the previous week. The Refinance Index increased 10 percent from the previous week and was 44 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 5 percent from one week earlier. The unadjusted Purchase Index increased 5.3 percent compared with the previous week and was 32 percent lower than the same week one year ago.

Here is the data.

Middle class Joe as he likes to call himself is actually BIG CORPORATE Joe. A friend of big donor and BIG pharmam, BIG banks, BIG tech, BIG defense contractors, BIG media. No wonder Hunter Biden refers to Joe as “The BIG guy!”

Biden’s approval ratings are terrible. Okay, Biden is the worst President in history, weak, can’t speak coherently and is letting chaos reign on the southern border. But from a consumer standpoint, he and crazy spending Congress have helped make America simply unaffordable for miillions.

Once again, Biden’s obsession with foolish green energy, Congress using Covid to spend trillions, then the green energy subsidy Act (aka, Inflation Reduction Act) where Biden and Congress agreed to make massive payoffs to big donors (the donor class). All this resulted in 40 year highs in inflation leading The Federal Reserve to raise interest rates to combat inflation.

For autos, the interest rate on an auto purchase has soared to it highest level since 2008. And car prices at up 19% under Biden’s Reign of Error.

And when we consider that US Real Average Weekly Earnings growth continues to be negative under Unaffordable Joe.

Housing? At least home price growth is slowing and even negative in some cities. But housing is still unaffordable for millions of Americans.

The housing situation will only get worse as Title 42 expires and millions of illegal immigrants invade the US. Texas Governor Abbot should ship all of them to Wilmington Delaware, home of Unaffordable Joe Biden. Let him suffer for once from his own folly.

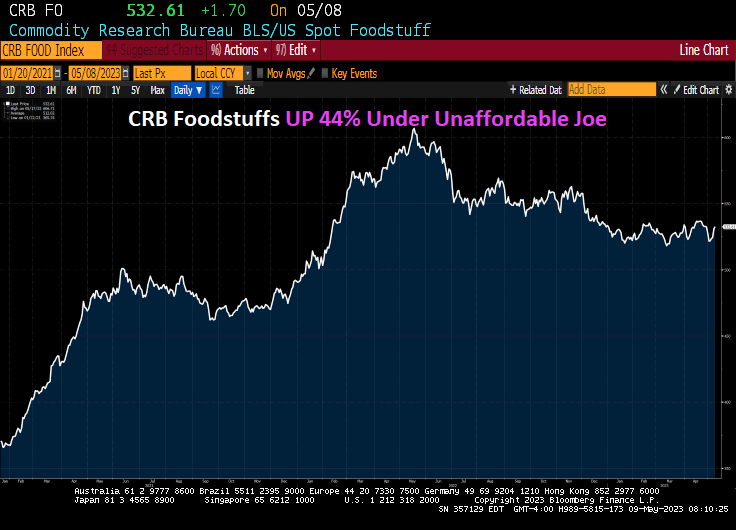

Food? Don’t get me started. The Commodity Research Bureau is up 44% under Unaffordable Joe.

Okay, Biden is a useful idiot for BIG banks, BIG Pharma, BIG tech, BIG defense, and BIG government. He is popular with the 1% and people who watch “The View.” But many of the 99% are suffering under Unafforable Joe.

The Federal government in Washington DC is broken beyond repair. Politicians get elected by promising free or cheap things, so they keep delivering the bacon. Or pork to political donors. The top 1% get massive payoffs (like green energy subsidies or bank bailouts), the bottom 99% get out of control entitlements like Social Security, Medicare and Medicaid. And other unsustainable entitlements. In fact, student loans are now an entitlement since some voters will vote for the corrupt politician (no, Joe Biden isn’t the only corrupt politician in Washington DC) who will forgive their student loans.

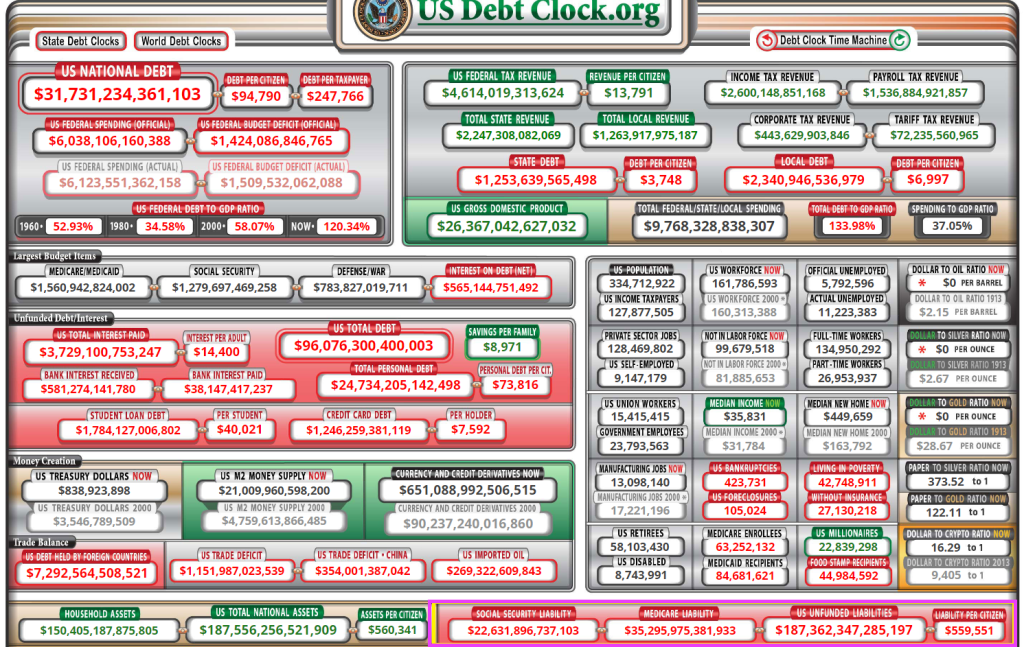

In fact, we now have $187 TRILLION in UNFUNDED liabilities that were promised to the 99%. The 1% will always get their political contributions paid. Biden and Schumer have promised their donor class trillions in spending, so that are threatening to let the US debt default to protect the 1%.

And unfunded entitlements are expected to soar, particularly Medicare.

Mandatory spending is expected to soar while discretionary spending is almost flat in terms of growth.

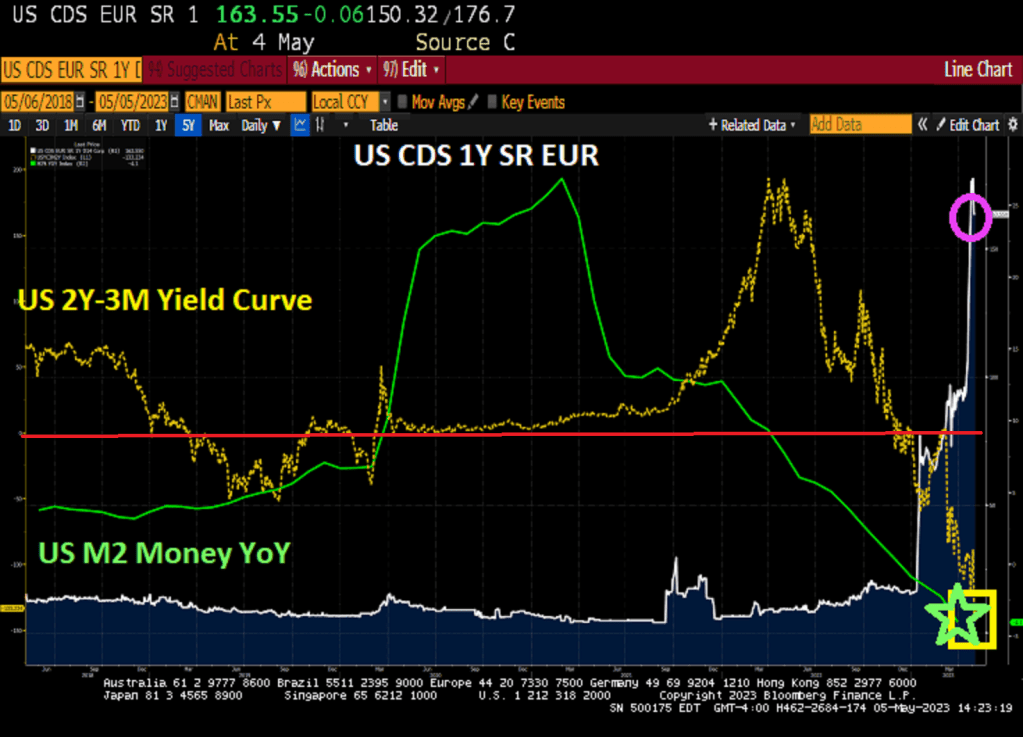

Meanwile, the US credit default swap remains elevated as the US Treasury short curve (2Y-3M) is near the most inverted in history.

And this headline, “Biden Not Ready Yet to Invoke 14th Amendment to Avoid US Default”. That means Biden would adopt extraordinary powers to prevent a debt default. Hence, the idiocy like the trillion dollar coin.

Nobel Laureate and Statist useful idiot Paul Krugman wants to keep spending trillions. As a result, he argues “Don’t worry about the declining US dollar hegemony … as long as the US doesn’t default.” Translation: Krugman agrees with Dementia Joe that Republicans should just pass Biden’s budget with no strings attached. C’mon Krugman. The growth of BRICs (Brazil, Russia, India, South Africa and growing) is partly due to 1) perceived weakness of Senile Grandpa Joe and 2) the fiscal spending and debt growth in Washington DC. Of course it matters, but Krugman wants to keep spending on green lunacy and entitlements until we break the back of the country. Sounds like Krugman is on board with Cloward-Piven.

They can’t cut promised entitlements. Look at France where Macron raised the retirement age by 2 years and there are endless riots. So debt default is the only option, though painful.

Will Congress and future administrations stop prominsing endless spending that benefits the 1%? Not likely. Our political system is hopelessly broken.

I am sure that China’s Communist Party has sent Dementia Joe a message “We own you! You better not default on what you owe us!!” Or default so we can own you financially.

Three of the four horsemen of the financial apocalypse. Yellen is the fourth horseman, but is too short to appear in the picture.

Yes, the banking system under green zealots and spendiholics Biden, Pelosi and Schumer have helped drive inflation to 40 years highs leading The Fed to counterattack and raise interest rates and slow M2 Money supply.

Ok, it is well-known that Biden was the stupidest man in the US Senate. And with Washington’s Patty Murray in the Senate, that is quite an accomplishment.

But Biden is President and is still stupid and spiraling down the dementia rabbit hole. He is blaming Republicans for their budget proposal to end the debt ceiling crisis despite saying previously that he would negotitate. Apparently, Biden’s puppet masters are telling him to risk default by playing the blame game.

So, US credit default swap (CDS 1Y, SR, EURO) price remains elevated which indicates that Biden, Yellen and Schumer may actually default on US debt.

As M2 Money growth crashes and burns, the US Treasury 2Y-3M yield curve inverts to lowest in history.

Biden loves to brag about the greatest economy in history! Sure Joe. Life during Biden.

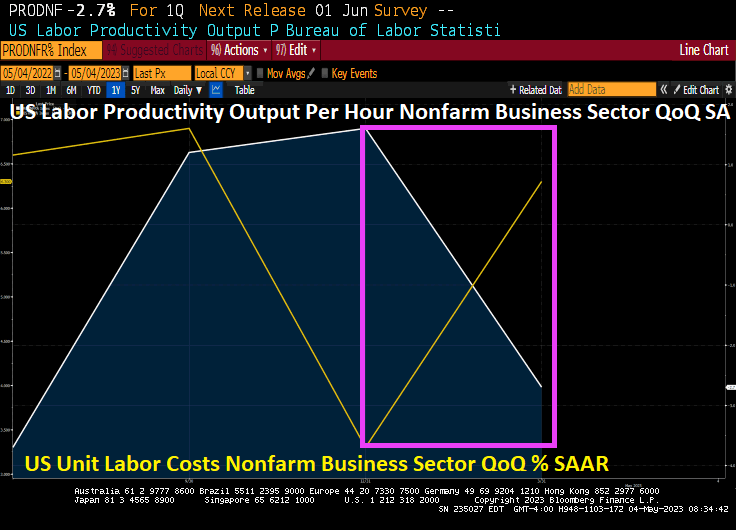

Challenger jobs cuts in April were 176% year-over-year. Non farm productivity in Q1 fell -2.7% QoQ. And unit labor costs in Q1 almost doubled to 6.3% QoQ, almost doubled from the Q4 2022 figure of 3.2%.

At least The Fed is going to pause it manic rate hikes. Then begin dropping them again.

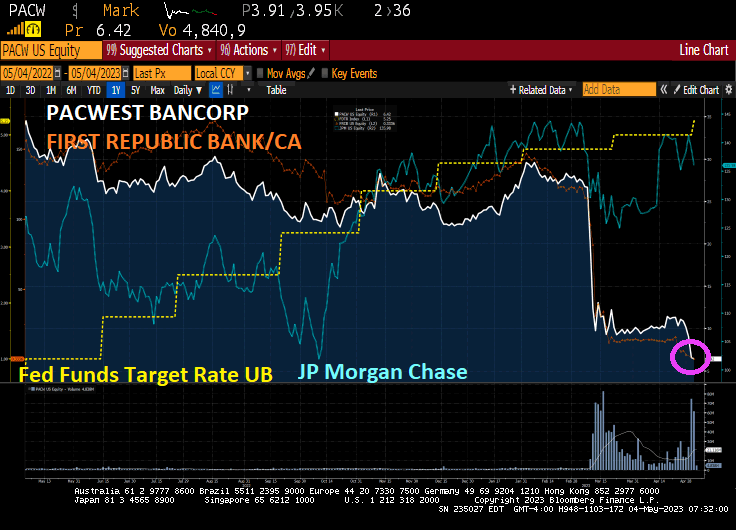

As Connor MacLeod said in the film Highlander, “There can only be one!” The US banking system under Joe Biden’s Reign of Error is like the film Highlander: apparently, there can only be one bank. And it is likely JP Morgan Chase.

Take the JP Morgan Chase (JPMC) acquisition of First Republic Bank:

In Acquiring First Republic Bank, JP Morgan Has:

Bypassed laws against acquiring bank while controlling 10%+ of US deposits

Shared $13 billion in losses with the FDIC

Received a $50 billion loan from the FDIC

Effectively bought back its own deposits

Expects to profit $5 billion+ over the next 5 years

This crisis has taught us that rules don’t matter in times of panic, particularly to regulators.

And now we have PacWest Bancorp. Lender says it’s been approached by potential investors. Bill Ackman warns US regional banking system at risk.

The turmoil at PacWest shows how investor angst still remains elevated after a string of failures and deposit outflows in the sector despite Federal Reserve Chair Jerome Powell’s assurance Wednesday that authorities were closer to containing the crisis. It’s reignited the debate over whether more US regional lenders will fall after this year’s collapse of SVB Financial Group’s Silicon Valley Bank, Silvergate Capital Corp., Signature Bank and most recently First Republic Bank.

Smaller banks are under pressure after a year of interest-rate hikes hammered the value of their bond holdings and drove unrealized losses to an estimated $1.84 trillion. Trouble in commercial real estate is adding to the pain, while depositors take their money out to seek better returns elsewhere. These stresses have put the spotlight on these lenders, which typically have fewer resources to defend themselves.

We are seeing a consolidation of the banking system .. again as smaller and regional banks fail and get gobbled up by the Too-Big-To-Fail (TBTF) banks like … JP Morgan Chase.

Biden’s Reign of Error is not over yet. His campaign slogan (which was also Bill Clinton’s campaign reelection slogan) is “Finish the job!” With Biden’s idiotic mortgage idea of punishing borrowers with good credit and giving subsidies to those with bad credit, Biden is trying to finish off the US economy and banking system.

Some are marvelling that M2 Money VELOCITY (GDP/M2) is rising as if this is a miracle. It isn’t. Under Biden, public debt has increased by $3.7 trillion. But as The Fed pulls back and M2 Money growth slows, M2 Money Velocity is rising. But still below historic levels.

Doctor, doctor (Yellen). We have a bad case of excessive and wasteful Federal spending and debt.

China doesn’t have to invade the US. Biden, Schumer and Jeffries are destroying the country on their own.

While Biden is bailing out banks and Ukraine (and taking bribes from China), I am struggling to buy a bottle of wine.

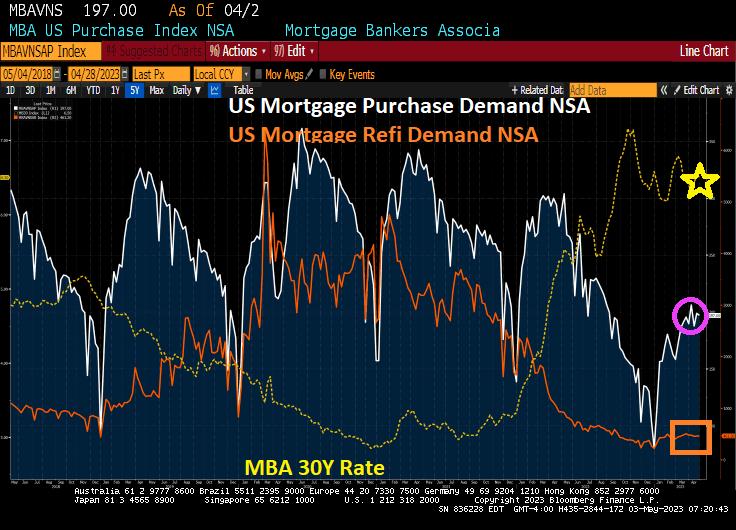

This is last data dump for mortgage demand (applications) before Biden’s idiotic woke mortgage policies go into effect (taxing those with good credit to subsidize those with lousy credit) take effect. I call this Bolshevik Biden’s Mortgage Market.

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 28, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 0.4 percent compared with the previous week. The Refinance Index increased 1 percent from the previous week and was 51 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 32 percent lower than the same week one year ago.

You must be logged in to post a comment.