Rubino says, “If the U.S. government is running crisis level deficits, which it is right now, borrowing money and paying interest on it means we are in a financial death spiral…”

“The debt goes up, the interest on the debt goes up and that raises the debt even further, and you just spiral out of control.

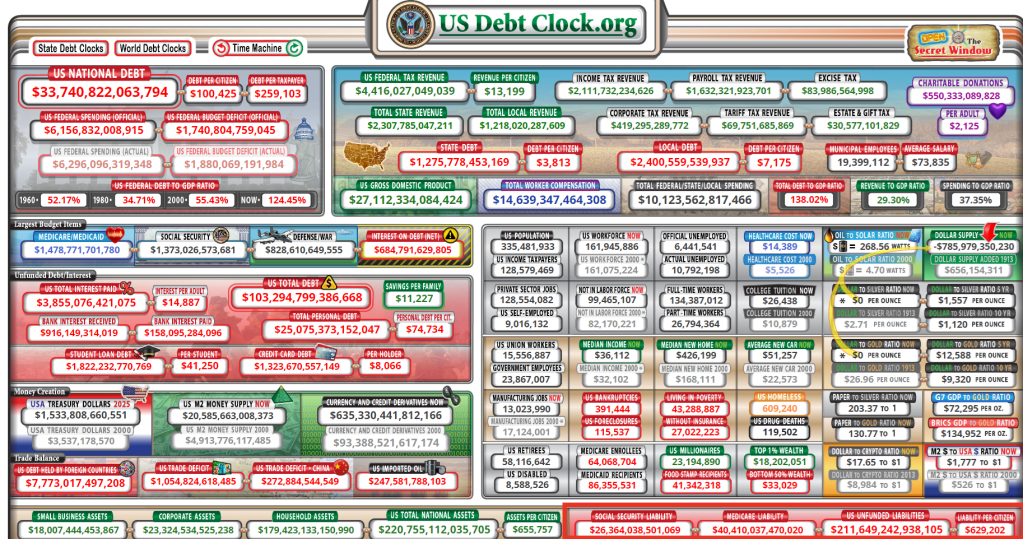

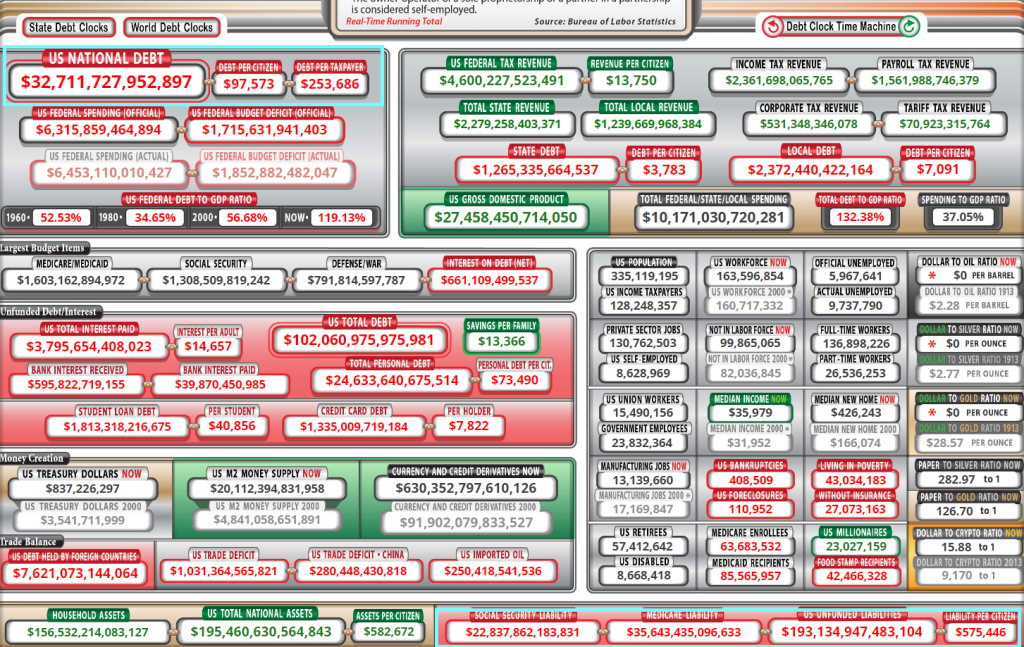

We are there right now. The official U.S. debt is $33.5 trillion. It’s growing by $1.7 trillion a year, and $1 trillion of that is interest costs.

Interest costs are rising as the overall debt goes up. Then throw in this incredibly reckless military spending in the guise of foreign aid, and you get a society that has completely lost control.

That’s where we are now.

We are in the blowoff stage of a 70-year credit super-cycle.

Those things do not end with a whimper, and they certainly do not end with a soft landing. They end with a bang, and the bang is going to be centered on the currency.

People are going to look at this and say, ‘Do I really want to hold the currency or bonds of a country that is destroying its finances at this trajectory and this scale?’ The answer will be ‘No.’

At that point, it is game over for a deeply indebted economy. We are headed that way fast, and these wars are taking us that way even faster.”

If the Fed keeps raising interest rates, the economy tanks, but you protect the dollar. If you cut interest rates, you spike inflation even more, and the U.S. dollar tanks.

Rubino says in the end, we get a “massive reset,” and the everything bubble explodes.

Rubino says the dollar is going to decline and, at some point, it starts to go into freefall in terms of buying power. Rubino explains,

“If a currency starts to decline in a disorderly way, then you have a massive financial crisis on your hands.

That is definitely where Japan is right now. The U.S. is headed that way fast.

So, once we reach that point, there is no fix.

Then it is only a matter of time that everybody realizes that there is no fix, and they just bail on the whole experiment, and that’s where we are headed.”

Rubino talks about plunging home prices, more trouble coming in the commercial real estate market and why you need gold and silver as core assets during a currency reset.

Riots, already happening in American cities (not to mention looting in New York City, Chicago, San Francisco and Los Angeles), will accelerate if Congress attempts to curtail entitlements (now at $211.65 TRILLION).

The World Economic Forum (WEF) is a leading pusher of the ESG drug, pushed by the elite class intending to control the world. Unfortunately, numerous American politicians and influencers have attended the Davos meetings and have openly praised the WEF and its leader Klaus Schwab.

ESG investing, or sustainable responsible investing (SRI), uses this information about a company to inform investment decisions that prioritize all stakeholders.

Here’s how the Forum’s partners are leading the switch to stakeholder capitalism.

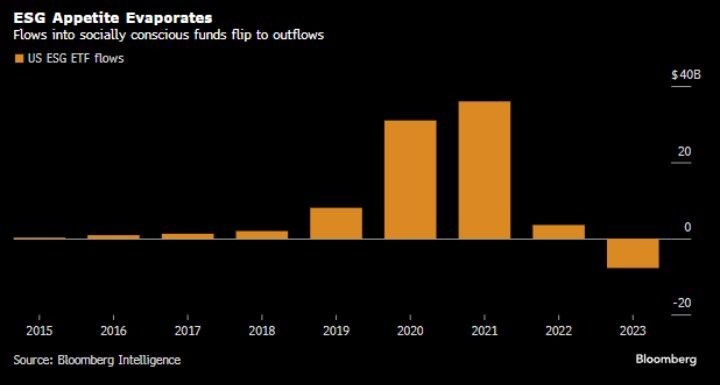

But all is not well with WEF’s ESG drug distribution. In fact, ESG flows into socially consious funds were a big thing during Covid (2020) and the first year of Biden’s Reign of Error. But ESG flows slowed sharply in 2022 and seeing net outflows in 2023.

US borrowers are retreating en masse from the world’s second-biggest ESG debt class.

The $1.5 trillion market for sustainability-linked loans, in which borrowing is tied to environmental, social or governance goals, has seen an overall slowdown in volumes this year as both interest rates and greenwashing fears rise. But nowhere has the decline been as precipitous as in the US, where the number of new sustainability-linked loans is down 80% from a year earlier.

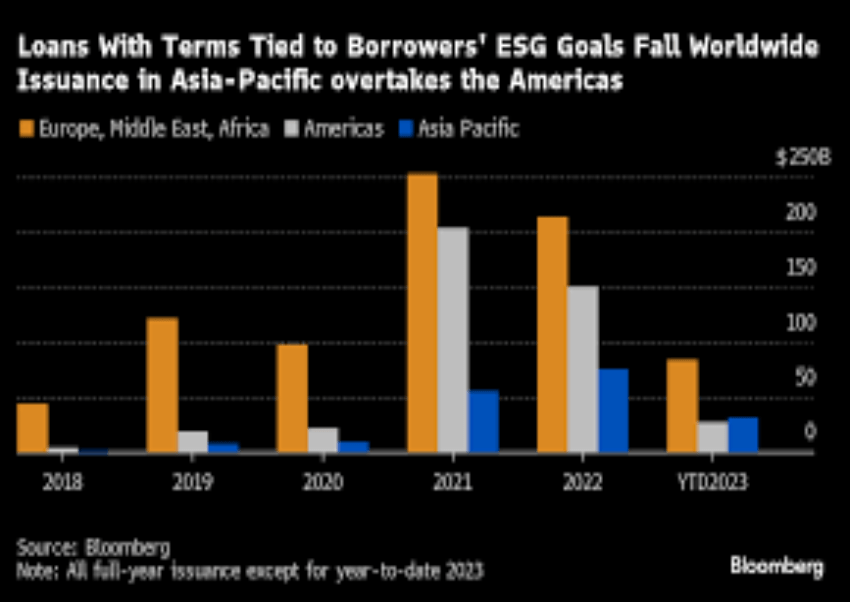

But ESG is still relatively popular in Europe, Middle East and Africa (orange). But taste for ESG is waning around the globe. But the selection of Biden as President in the US marked a surge in ESG -tied loans in 2021 and 2022 (not to mention the insane levels of spending out of Biden and Congress, much tied to the sustainability, green energy fantasy.

Loans with terms tied to borrower’s ESG goals have fallen worldwide.

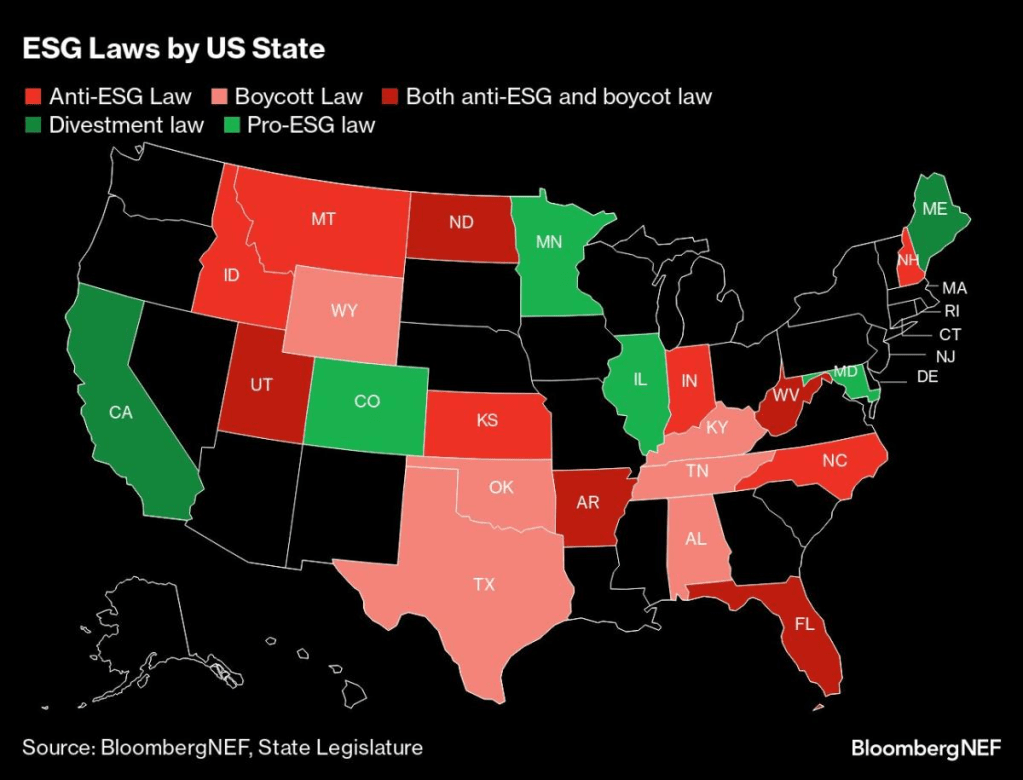

Several states (largely blue states like California, Minnesota, Illinois, and Colorado have pro-ESG laws) while several states have anti-ESG laws (largely red states like Montana, Idaho, North Dakota, Kansas, Utah, Indiana, Arkansas, Florida, and West Virginia).

And of course, global warning may not be as dire as John Kerry and Greta Thunberg say.

WEF’s Klaus Schwab about to get sniffed by his 80-year old puppet, Joe Biden. In fact, Biden is singing “I’m your puppet.”

Here is Hunter Biden welcoming the Green Energy fairy and all the trillions in misallocated spending it brings.

Biden says he wants 4 more years to finish the job. Like killing off the mortgage market completely, Joe?

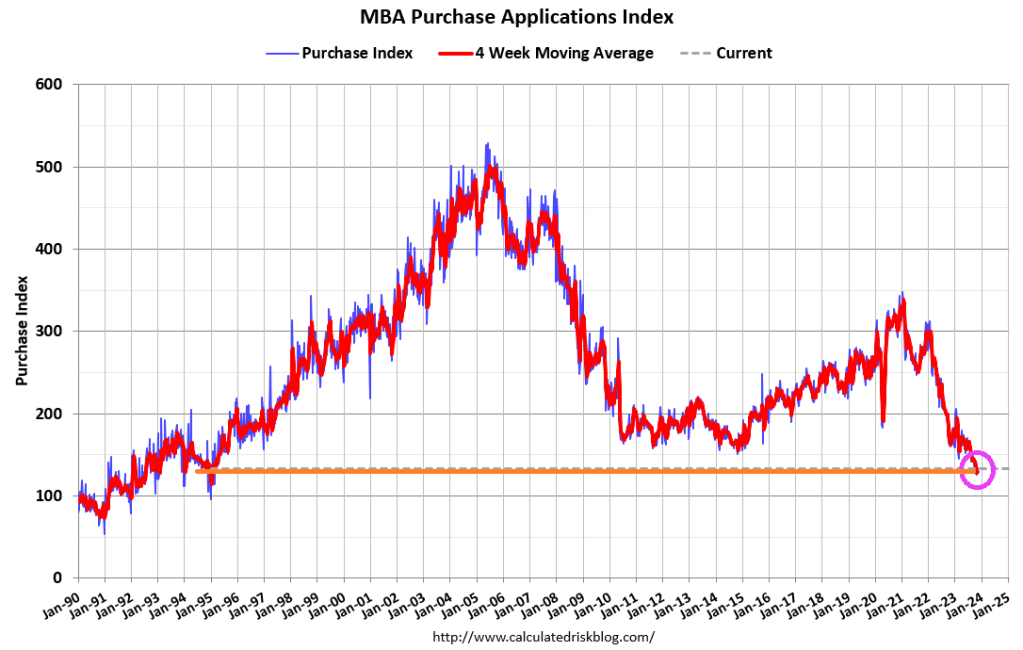

Mortgage applications increased 2.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 10, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 2.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 0.4 percent compared with the previous week. The seasonally adjusted Purchase Index increased 3 percent from one week earlier. The unadjusted Purchase Index decreased 0.3 percent compared with the previous week and was12 percent lower than the same week one year ago.

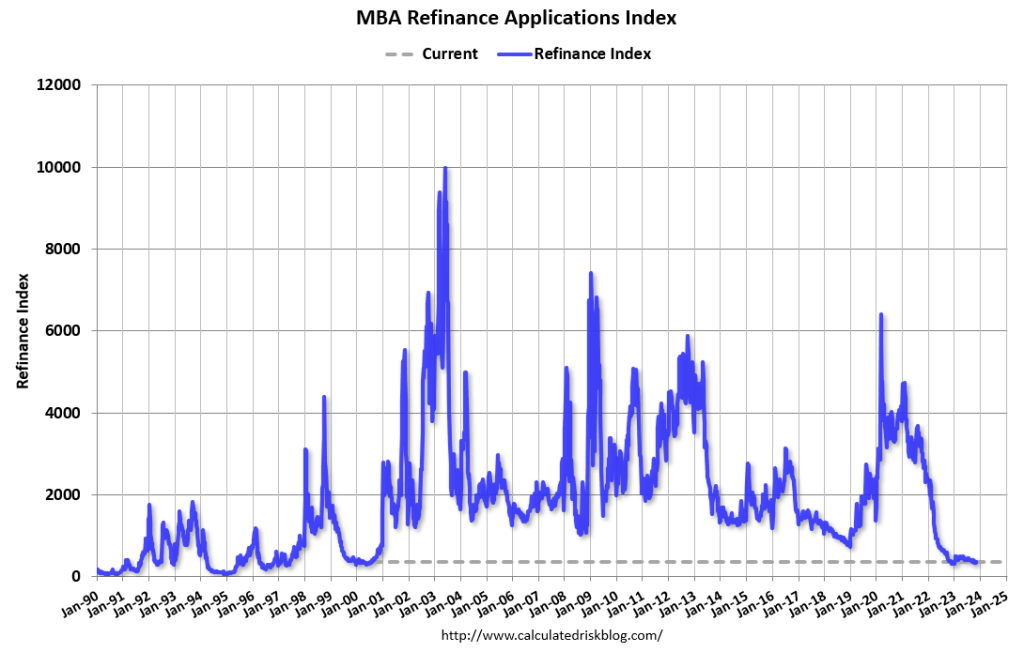

The Refinance Index increased 2 percent from the previous week and was 7 percent higher than the same week one year ago.

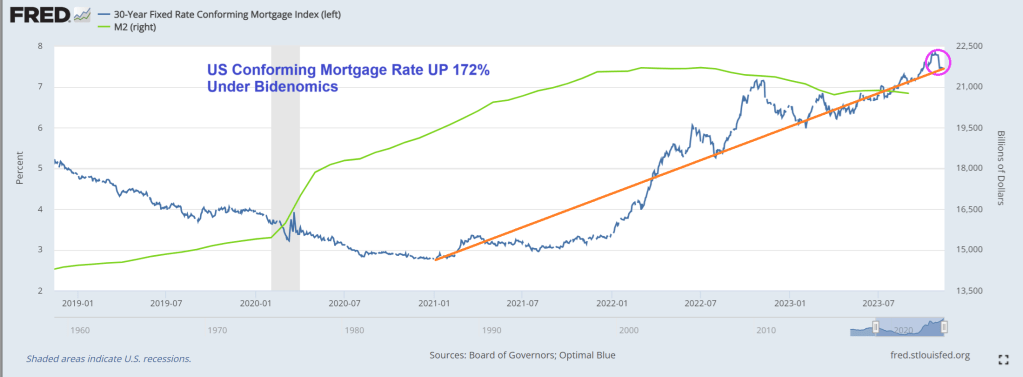

Of course, mortgage rates have been declining slightly over the past few weeks, but remain up 172% under Biden.

At least the stock market is booming after the inflation report signalled that The Fed is likely done with rate hikes.

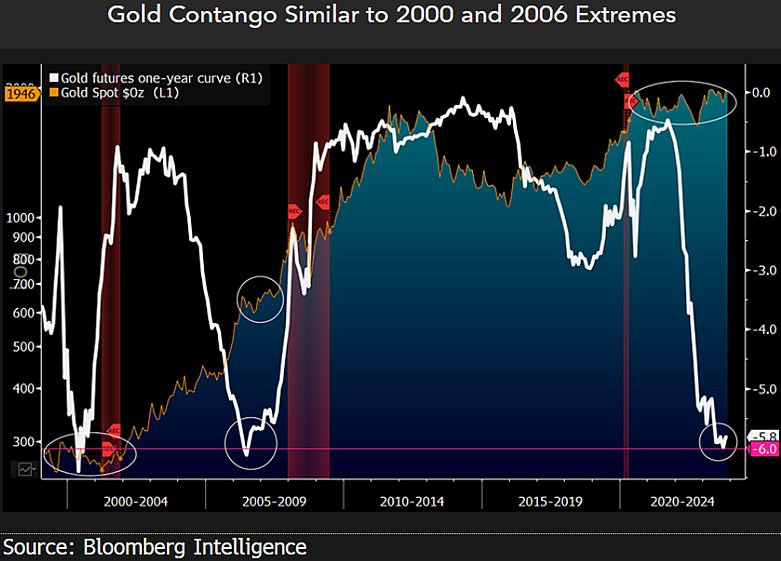

On the gold front, we are seeing evidence of contango.

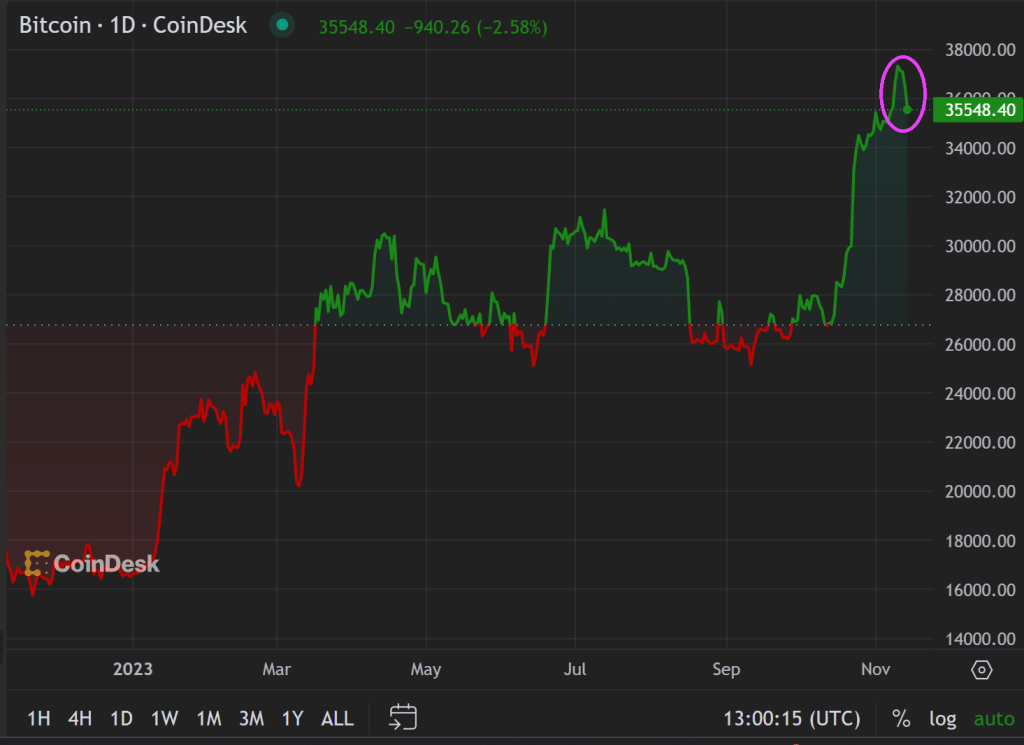

Bitcoin? Down a wee bit after a staggering rise in price over the past year.

Here is China’s Xi meeting with Biden’s likely replacement, “Greasy Gavin” Newsom and Newsom’s likely Treasury Secretary, Janet “Too Low For Too Long” Yellen. Newsom, Yellen and Xi all want havoc in America.

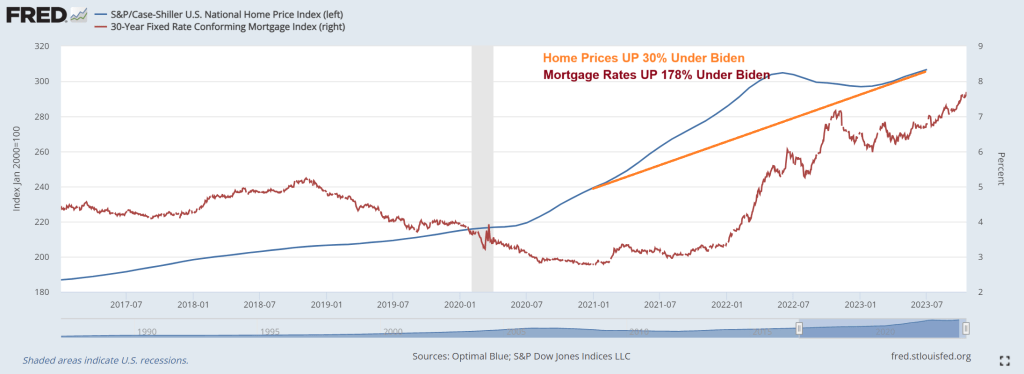

Under Bidenomics, home prices are up 30% while real weekly earnings growth has been negative for most of Biden’s Presidency. And mortgage rates are up 178% under Bidenomics.

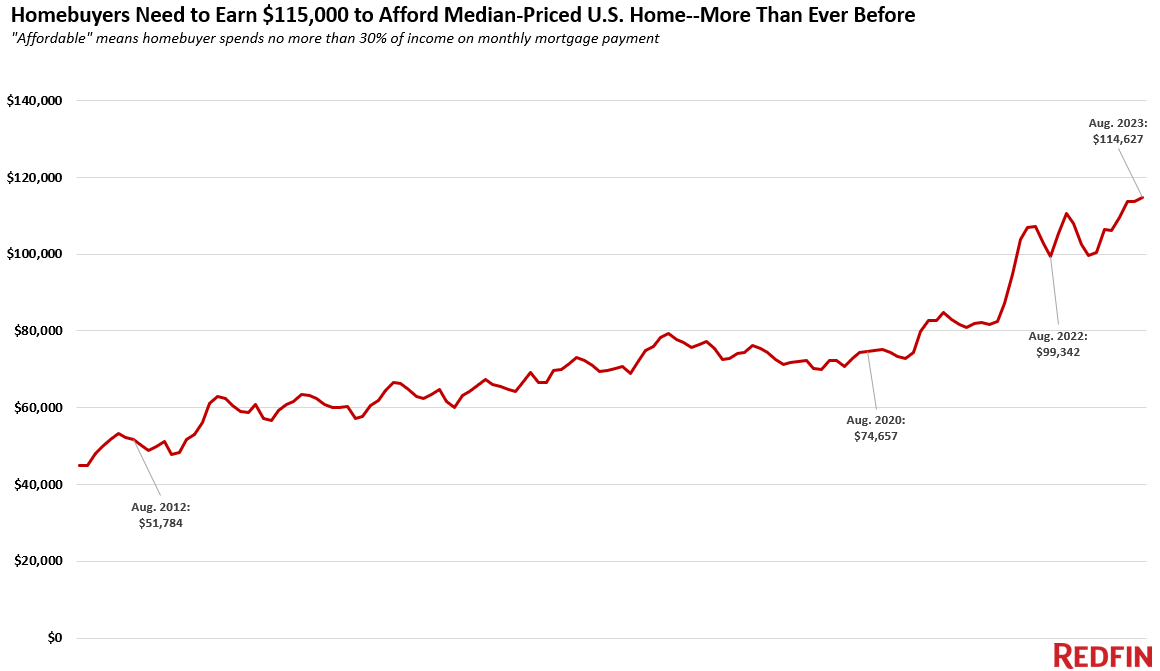

It’s harder than ever for Americans to afford a home.

A homebuyer must earn $114,627 to afford the median-priced U.S. home, up 15% ($15,285) from a year ago and up more than 50% since the start of the pandemic. That’s the highest annual income necessary to afford a home on record.

This is based on a Redfin analysis that compares median monthly mortgage payments for homebuyers in August 2023 and August 2022. The income data in this analysis is adjusted for inflation. See the bottom of this report for more on methodology.

Housing costs are higher than ever because of the one-two punch of sky-high mortgage rates and rising home prices. The average rate on a 30-year fixed mortgage was 7.07% in August. Mortgage rates have climbed even higher since then, hitting 7.57% during the week ending October 12–their highest level in over two decades. But even though soaring mortgage rates have dampened demand, low inventory is causing home prices to increase. The typical U.S. home sold for about $420,000 in August, up 3% year over year and just about $12,000 shy of the all-time high hit in mid-2022.

The typical U.S. homebuyer’s monthly mortgage payment is $2,866, an all-time high. That’s up 20% from $2,395 a year earlier, and by that time payments had already increased substantially from the beginning of the pandemic, a time of ultra-low mortgage rates and yet-to-skyrocket home prices. In August 2020, for instance, the typical monthly payment was $1,581, based on that month’s average mortgage rate of 2.94% and median home price of $329,000. At that time, a homebuyer would have needed to earn $75,000 per year to afford the typical home.

The typical American household earns about $40,000 less than the income needed to buy a median-priced home. The median household income was roughly $75,000 in 2022, the most recent year for which annual income data is available. Hourly wages have risen in 2023, but not nearly as fast as the income necessary to afford a home is rising: The average U.S. hourly wage has increased by about 5% over the last year.

“In a homebuyer’s ideal world, rising mortgage rates would push demand and home prices down enough to make up for high interest payments. But that’s not what’s happening now: Although new listings are ticking up slightly, inventory is still near record lows as homeowners hang onto their low mortgage rates–and that’s propping up prices,” said Redfin Economics Research Lead Chen Zhao. “Buyers–particularly first-timers–who are committed to getting into a home now should think outside the box. Consider a condo or townhouse, which are less expensive than a single-family home, and/or consider moving to a more affordable part of the country, or a more affordable suburb.”

Affordability is less of a problem for all-cash and move-up buyers. The major increase in income necessary to afford a home hits first-time homebuyers hardest. Buyers who can afford to pay cash aren’t impacted by high mortgage rates, and they likely earn more than the income necessary to purchase a home, anyway. Buyers who are selling a home to buy another one are in a better boat than first-timers because they have likely built up equity in their current home, which takes a bit of the sting out of soaring monthly payments. The caveat to the caveat is those who bought at the height of the pandemic-era market with an ultra-low mortgage rate and need to sell now: Not only are they giving up a low rate, they also may have lost money on their home.

Metro-level highlights: Income needed to buy a home has risen in all major metros, with biggest uptick in Miami and smallest in Austin

August 2023, analysis includes 100 most populous U.S. metros for which data is available

Metros where necessary income has increased most: In both Miami and Newark, NJ, homebuyers must earn 33% more than a year ago to afford the typical home–the biggest percent increase of the major U.S. metros. Homebuyers in Miami need to earn $143,000 annually to afford the area’s typical monthly mortgage payment of $3,580, and Newark buyers need to earn roughly $160,000 to afford that area’s $3,989 payment.

Other metros where necessary income has increased by over 30%: The income necessary to afford a median-priced home has increased by over 30% in four other metros, all in the eastern half of the country: Bridgeport, CT ($183,000); Dayton, OH ($60,000); Rochester, NY ($66,000); and Hartford, CT ($95,000).

Buyers need to earn more in every major metro: Skyrocketing mortgage rates have caused the income necessary to buy a home to increase in every major metro, even the places where prices have declined over the last year.

Necessary income has increased least in pandemic homebuying hotspots: Austin, TX homebuyers must earn $126,000 to afford the median-priced home, 8% more than a year ago–the smallest increase of all the major U.S. metros. That’s despite Austin home prices falling 7% year over year in August after they skyrocketed during the pandemic, with remote workers flocking in. Boise, ID, another pandemic homebuying hotspot where demand has since dropped, experienced the next-smallest increase: up 9% to $127,000. Salt Lake City, Fort Worth, TX and Lakeland, FL come next, with year-over-year increases of about 13% each. Home prices are down from a year ago in all those metros.

Homebuyers must earn six figures to buy a home in half the major metros in the country: In 50 of the 100 metros in this analysis, buyers must earn at least $100,000 to afford the median-priced home in their area. Buyers must earn at least $50,000 everywhere in the country.

Bay Area buyers must earn $400,000: Buyers in the most expensive markets in the country–San Francisco and San Jose, CA–must earn more than $400,000 to afford the median-priced home in their area, both up nearly 25% year over year. The next five metros are all in California: Anaheim ($300,000), Oakland ($250,000), San Diego ($241,000), Los Angeles ($237,000) and Oxnard ($233,000).

Rust Belt buyers need the least income–but it’s still up from a year ago: Detroit homebuyers must earn about $52,000 to afford the area’s median-priced home, up 19% from a year ago. That’s the lowest income required to afford a home in the U.S. Next come three Ohio metros (Akron, Dayton and Cleveland) and Little Rock, AR, all of which require roughly $60,000 in annual income to buy a home.

Face it, the US economy and housing/mortgage markets are addicted to gov!

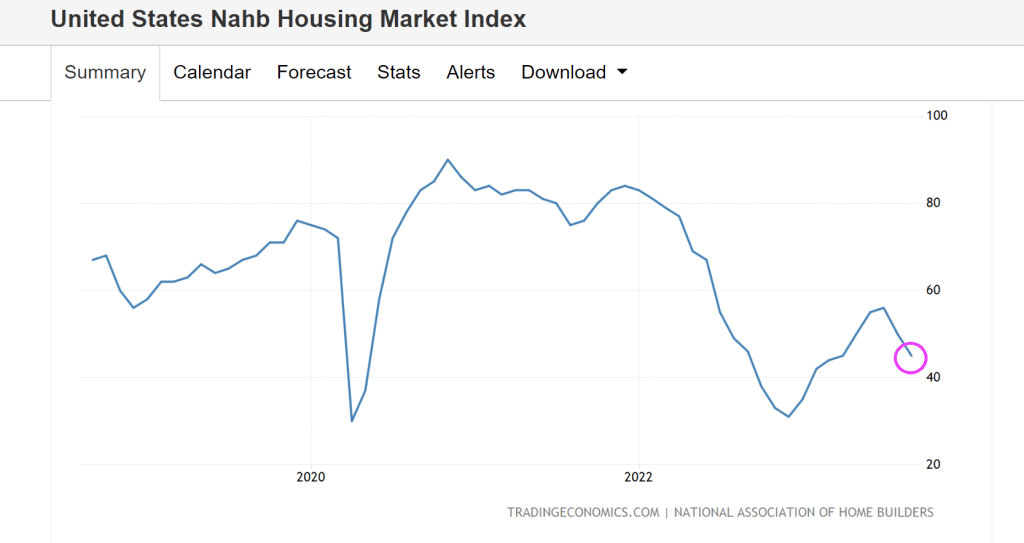

U.S. homebuilders are feeling pessimistic about their business for the first time in seven months, thanks to stubbornly high mortgage rates.

Builder confidence in the single-family housing market fell 5 points in September to 45 on the National Association of Home Builders/Wells Fargo Housing Market Index. The decrease follows a 6-point drop in August. Anything below 50 is considered negative.

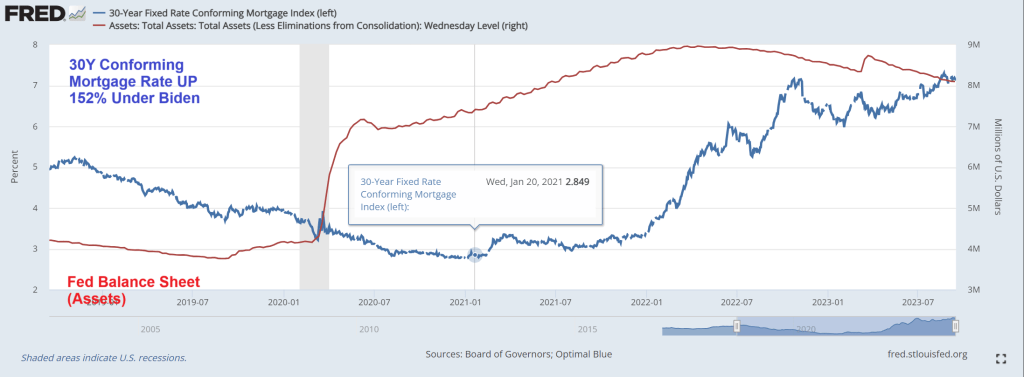

Mortgage rates are up 152% under Biden’s Reign of Economic Error. Note the big assist the economy got from Covid-related Fed stimulus (red line). The Fed’s balance sheet is still over $8 trillion.

Joe Biden is an incredibly weak President. I am not talking about his age or his deteriorating mental faculties. I am talking about ordering his attorney general to indict his chief political opponent, Donald Trump. How does the world interpret this weakness? BADLY.

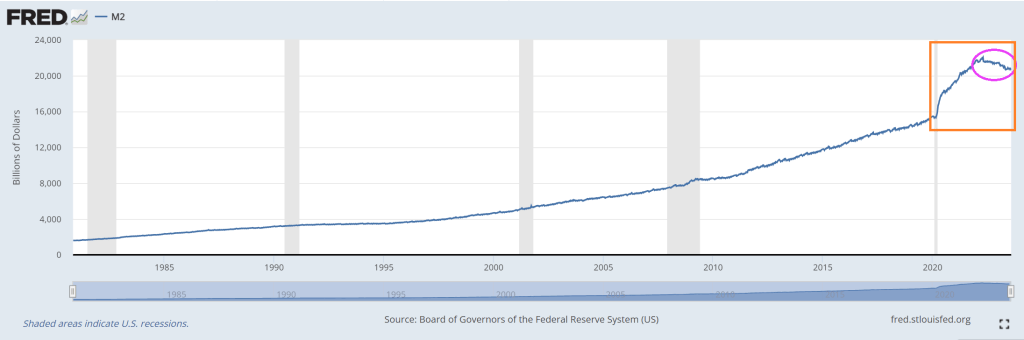

The US has gone off the rails in terms of printing money, particularly since COVID struck and money printing went wild.

Under Biden’s Reign of Error and the US reckless money printing, more countries are abandoning King Dollar (based of fiat currency) and joining BRICS. Brazil, Russia, India, China, South Africa and a host of countries joining like Argentina, Saudi Arabia, Iran, Egypt, UAE, etc.

Now, the rest of the world is still stuck on the US Dollar as reserve currency … for now. But as Biden gets weaker and weaker, watch more countries join BRICs.

According to Reuters, there are over 40 countries that have expressed interest in joining BRICS. A smaller group of 16 countries have actually applied for membership, though, and this list includes Algeria, Cuba, Indonesia, Palestine, and Vietnam. Pretty soon, under Biden’s crazy leadership, we may be the last man standing in using the US Dollar as reserve currency.

Then we have the other shoe dropping with Bidenomics.

As soon as Biden took office, he set out to destroy industries that produce reasonably priced energy. He focused tremendous effort on deficit spending and borrowing to hand out “government goodies” to buy votes; recipients of this government largesse, in large part, included debt-saddled students, the green mafia, and leftist activists.

When Biden took office, inflation was under 2%, despite COVID and supply chain disruptions; shortly after, it skyrocketed to over 9%. Now inflation increases are “down” but prices remain exceptionally high compared to pre-Biden.

For example, crude oil prices, which affect almost everything and are used in over 6,000 products, are roughly double what they were when Biden took over.

President Trump focused on reduced regulations and energy independence, and implemented lower tax rates, all moves that greatly helped the American people. In contrast, Biden focuses on ensuring bureaucrats rapidly increase regulations which raises costs for everyday Americans; he’s waging economic war against us. Very few of Biden’s regulations go through Congress. From the White House archives:

Between FY 2017 and FY 2019, the Trump Administration has cut nearly eight regulations for every new, significant regulation….

The Council of Economic Advisers (CEA) estimates that this pro-growth approach to Federal regulation will raise real incomes by upwards of $3,100 per household per year.

Here are some recent reports of how well Biden policies are working:

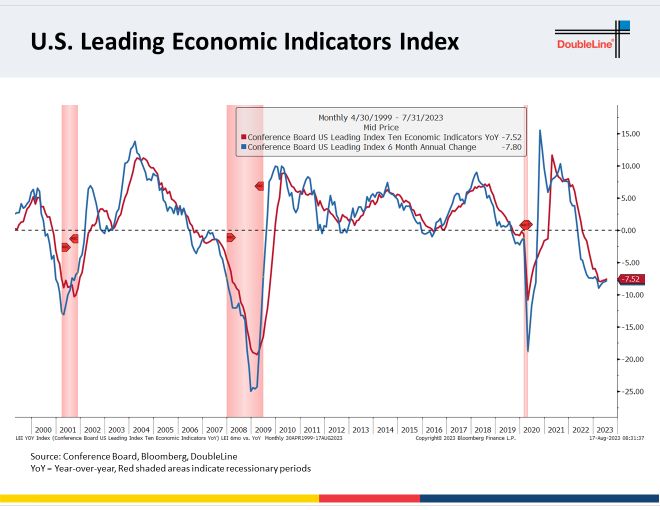

Leading economic indicators have fallen for sixteen straight months. Maybe that is why people think the economy is moving in the wrong direction?

The current cost-of-living crisis is a manufactured one. As inflation rose, the Federal Reserve was forced to raise interest rates, which saw fewer people move. The cycle is very understandable, as simply explained in this one headline, “Housing Crunch: Home Sales Fall To Six Month Low…But Prices Rise Anyway”.

Parcel volumes are dropping by so much, freight pilots are “worried” about job security.

People are running up credit card debt and defaulting on car loans because of high inflation, and because their real wages haven’t been able to sustain them. Now, even more are falling behind on their payments. From CNN:

More Americans are failing to make payments on their credit cards and auto loans, another sign of rising financial pressure on consumers.

New credit card and auto loan delinquencies have now surpassed pre-Covid levels, according to a Wednesday report issued by Moody’s Investors Service.

After years of promoting and subsidizing electric cars, they represent around 6% of total sales, and demand is clearly slowing. It wasn’t that long ago that well-to-do people were buying these electric toys so quickly that they were placed on waiting lists; now, inventories are building because they are too impractical and expensive:

Auto News understands that there is currently a 103-day supply of unsold EVs in the United States. While it did not specify how many units are sitting on dealership lots, it says there is a higher supply of unsold EVs than any other automotive segment, except those in the ultra-luxury and high-end luxury segments with supplies also reaching over 100 days.

So what is Biden’s solution? Force people to buy them.

Here are some simple economics questions for the media and other Democrats:

Does flooding the U.S with illegals help or hurt housing availability and affordability?

Will the intentional destruction of oil and coal companies help or hurt the middle class and the poor?

Yet, the media and other Democrats brag that Biden’s economic policies are great, and when the public gives Biden poor marks, they say that we just don’t understand, and we’re not willing to get behind a candidate if they fail to make us feel “warm and fuzzy.”

Are journalists really that unaware?

Of course, they always sought to destroy Trump as his policies, even as poverty sank to record lows amongst minorities, because they don’t really care about anything but big government. According to Census data:

In 2019, the poverty rate for the United States was 10.5%, the lowest since estimates were first released for 1959.

Poverty rates declined between 2018 and 2019 for all major race and Hispanic origin groups.

Two of these groups, Blacks and Hispanics, reached historic lows in their poverty rates in 2019.

Results and facts haven’t mattered to the complicit leftist media for a long time.

And perhaps the worst mistake Biden made (amongst his laundry list of horrible mistakes, [Afghanistan retreat, not showing up to E Palestine Ohio, Bidenomics that is a payoff to green donors and BIG corporate interests, an embarrasing visit to Maui two weeks after the fire, indicting his leading political opponent, ….) is the appointment of the WORST Federal Reserve Chair (Janet Yellen) as Treasury Secretary.

Preliminary benchmark revision smaller than some had projected

Biggest payrolls adjustment in transportation and warehousing

Are you surprised that the Biden Administration has been lying about job creation?? Not really since Biden compulsively lies about everything. Including his corruption.

US job growth was probably less robust in the year through March than previously reported, according to government data released Wednesday.

The number of workers on payrolls will likely be revised down by 306,000 for March of this year, according to the Bureau of Labor Statistics’ preliminary benchmark revision.

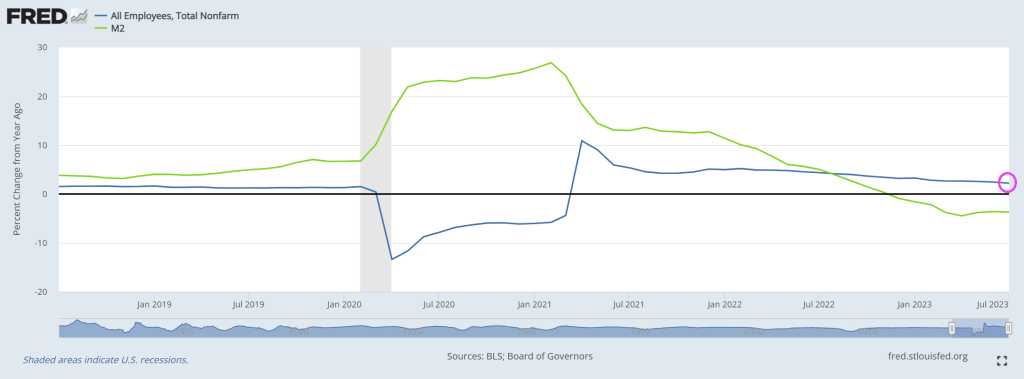

Even without the revision, job growth has slowed to 2.2% YoY in July as M2 Money growth slowed to -3.7% YoY.

Let see what our Overlords say at the Jackson Hole Fed symposium.

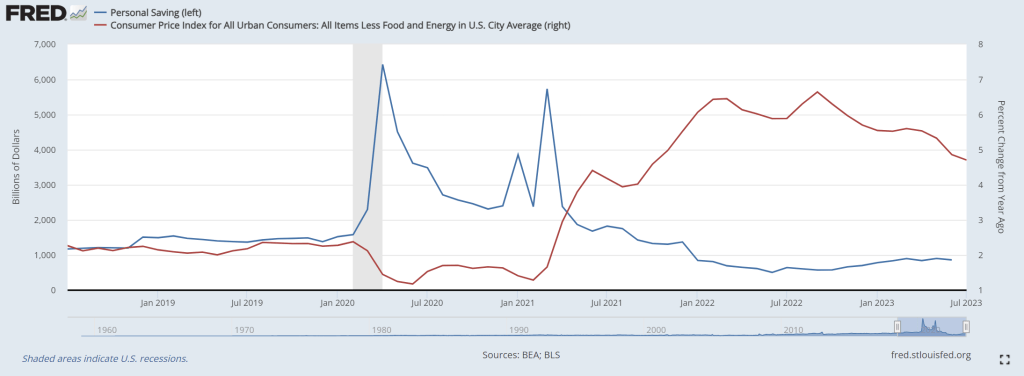

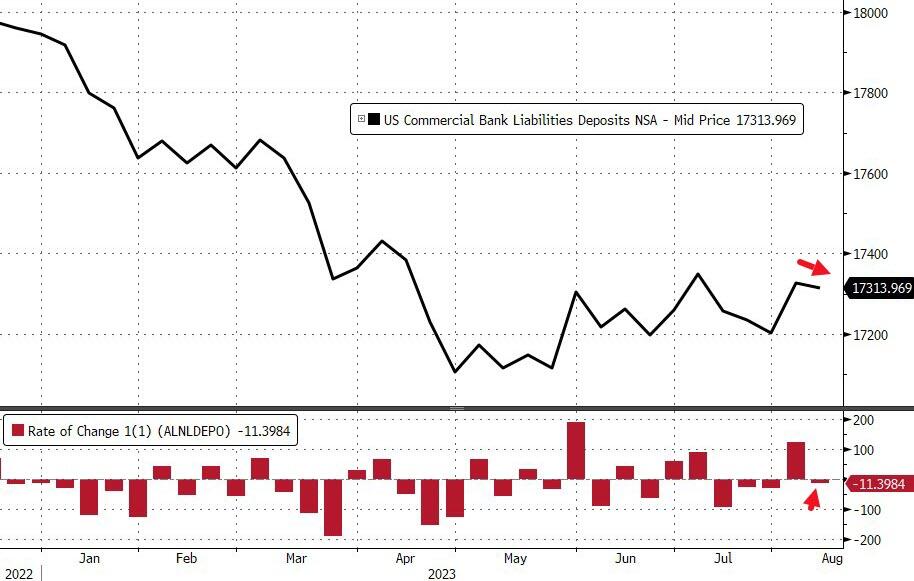

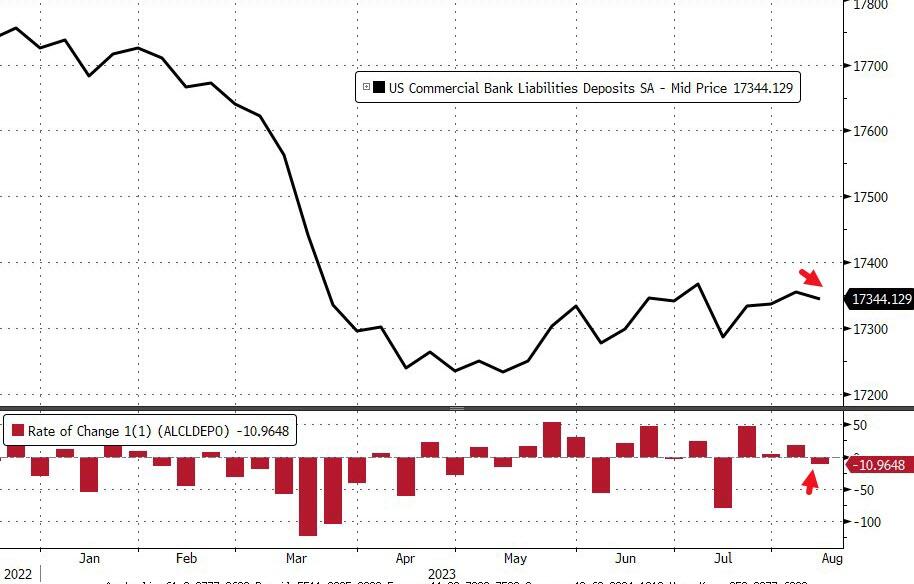

US personal savings are being exhausted as The Fed raises rates to fight inflation. I call this phenomenon “low riding” where consumers are being punished by The Federal Reserve and Biden Administration.

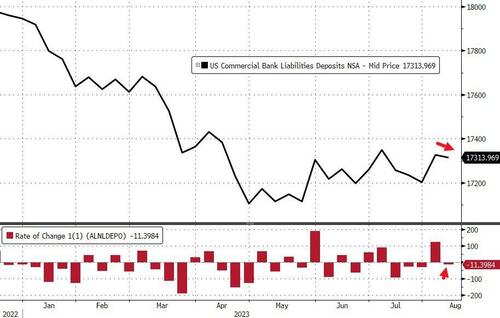

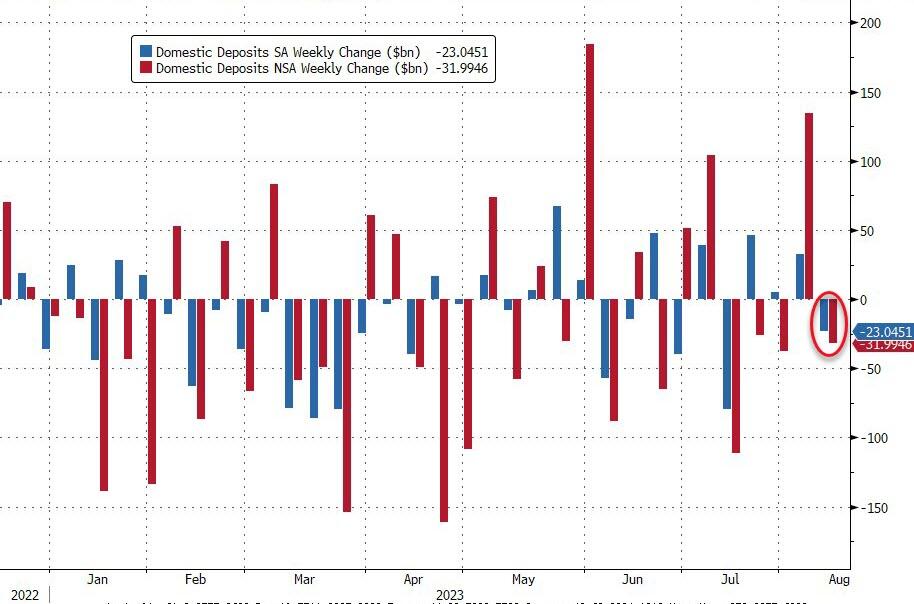

On a seasonally-adjusted basis, The Fed says that total deposits dropped $11BN last week (the first decline in 4 weeks). We also note that the prior week’s inflow was revised higher…

Source: Bloomberg

After last week’s enormous $121BN NSA deposits inflow, last week saw an $11BN outflow (on a non-seasonally-adjusted basis)…

Source: Bloomberg

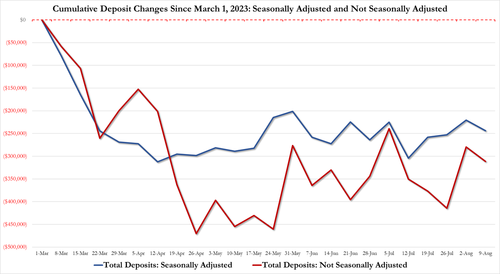

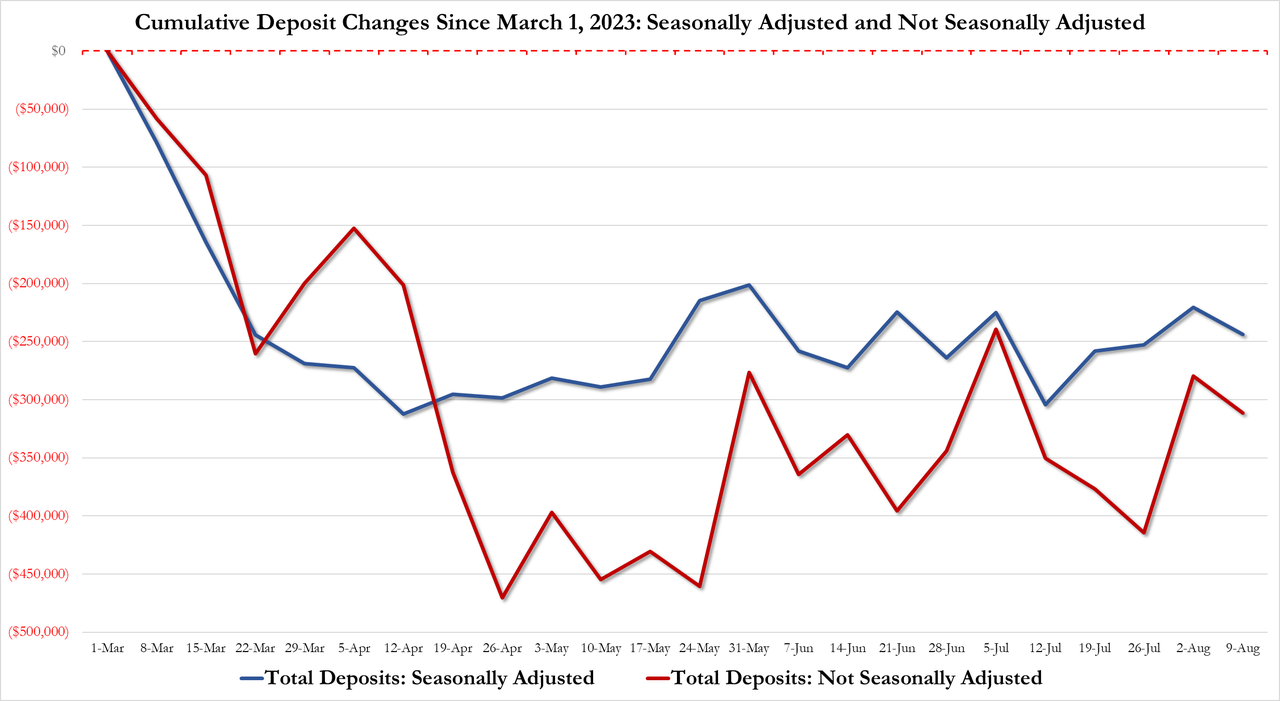

The gap between SA deposits and NSA deposits remains more manageable (until the next time The Fed decides to fiddle)…

The divergence between money-market fund assets and bank deposits remains extreme…

Source: Bloomberg

On a seasonally-adjusted basis, Small Banks saw $5.6BN deposit inflows last week while Large Banks suffered $28.7BN outflows (with foreign bank inflows of $12BN making up the difference)…

Source: Bloomberg

And so, for a nice change, everything is tidy with domestic US banks seeing deposit outflows on an SA and NSA basis…

Source: Bloomberg

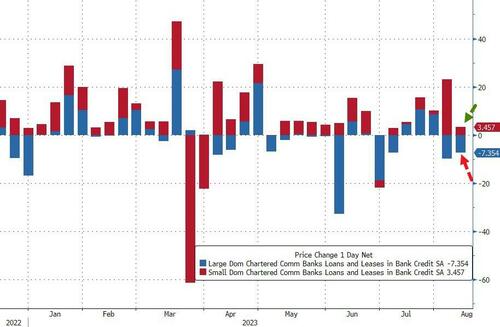

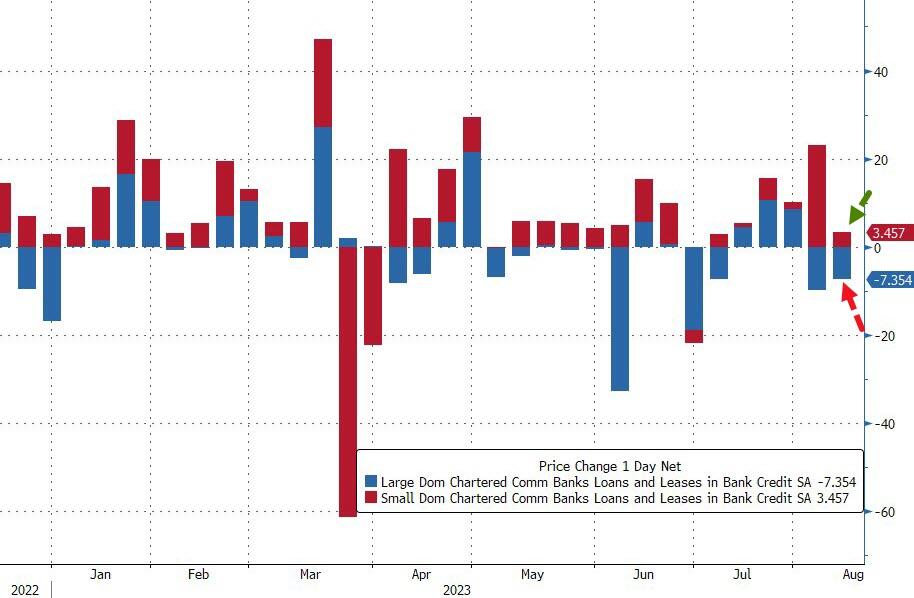

On the other side of the ledger, small banks continued to pump out loans (+$3.56BN, sixth straight week of increases), while large banks saw a $7.4BN contraction in loan volumes…

Source: Bloomberg

So, if The Fed’s data is to be believed, Small banks are ‘winning’ – deposit inflows and making loans; while large banks are leaking – deposit outflows and shrinking loans. All while Treasury prices tumble, stressing small bank balance sheets.

Just remember, the sitting US President Joe Biden goes under several psuedonyms like Robert Peters, Robin Ware, and JRB Ware in his email conversations about Ukraine with his son Hunter. But don’t forget another pseudonym: The Reverend Kane from Poltergeist 2!

Between The Federal Reserve’s outrageous overreaction to Covid (printing like there was no tomorrow), and Biden’s massive spending spree (lots of moldy (green) spending, we have see horrid inflation.

And The Fed trying (sort of) to combat inflation, we see that 30-year CONFORMING mortgage rate for 80% LTV or lower credit borrowers is up 163.5% under Bidenomics.

Under Bidenomics, public debt (owed by the US Treasury) is up 19% or greater than $5 triillion. Now wonder Biden throws are billions like it is water.

I seriously want the Biden Administration (and almost every member of Congress) why we are sending billions of dollars to Ukraine while barely giving Maui fire victims barely anything. The US is already $33 trillion in debt with >$193 trillion in unfunded liabilites. I want to ask Biden and Congress HOW the US is going to afford $193 trillion in unfunded liabilites?

Of course, NO ONE wants to face the reality of the disastrous fiscal poliicies of Washington DC politicians. Not McConnell, not McCarthy, not Schumer and especially not Billions Biden. Remember 10% for The Big Guy where Democrats argue that is meaningless. Or mini-me, Robert Reich (Clinton’s labor secretary) who claimed that the US economy is the best he has ever seen! Yes, Reich, for the top 1%. Of couse, no one will ask fools like Reich how we will pay for $33 trillion in debt and the $193 trillion in unfunded liabilies … and fund a war in Ukreiane in seeming perpetuity.

The themesong of Bidenomics is Randy Newman’s “Mr. President,” Have pity on the working man instead of paying off green energy BIG donors.

The massive green enegy spending spree by Biden and Congress (disguised as Inflation Reduction Act) is the keystone of Bidenomics. Or loadstone.

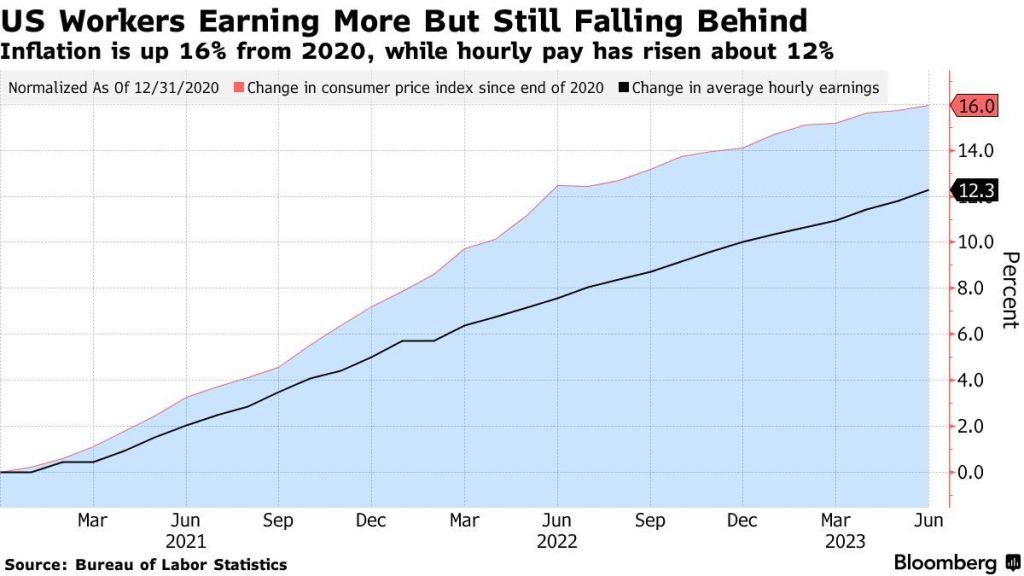

Since Biden became President, hourly pay has risen 12%! Unfortunately, Bidenomics spending spree (along with endless Fed monetary stimulus) has caused inflation to rise 16%. That is a net -4% decline in REAL earnings.

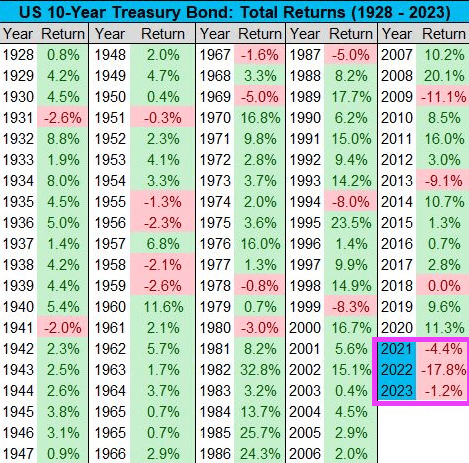

10-Year Treasury Yield is now 4.28%, the highest level since October 2007. From a total return perspective, the 10-Year Treasury Bond is now down 1% in 2023, on pace for its third consecutive negative year. With data going back to 1928, that’s never happened before. BUT we’ve never had Joe Biden as President before 2021.

And then we have the Conference Board’s Leading Economic Idicators, sucking wind.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.