The University of Michigan consumer survey results are out and there is good news! Sort of.

The UMich Buying Conditions for Houses rose to 47 in July! That is the good news. The bad news? It was at 142 in the last month before Covid and the economic/school shutdowns.

That is -67% lower than under pre-Covid Trump.

Nothing has been the same since Covid (aka, the Wuhan China Lab virus) where our corrupt politicians and lame street media (aka, government cheerleaders) show no interest in finding out what really happened.

Bitcoin cash is up 21.5% today.

Gold and silver are up today. Too bad I can’t buy nickel coins.

The Walking Dead’s Megan. The honorary symbol of Bidenomics.

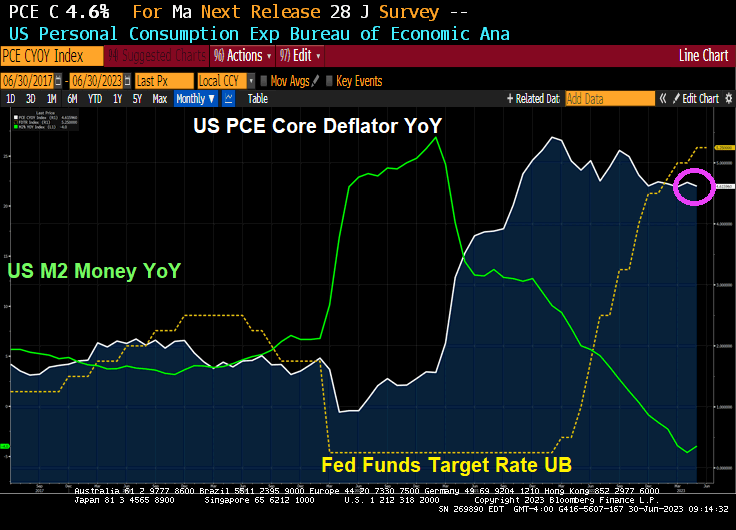

The film “The Core” was a silly film, but core inflation in the US is a serious problem for the middle class and low-wage workers. It remains elevated despite Treasury Secretary Janet “The Marxist Gnome” Yellen saying it was “transitory.” Looks pretty permanent to me!

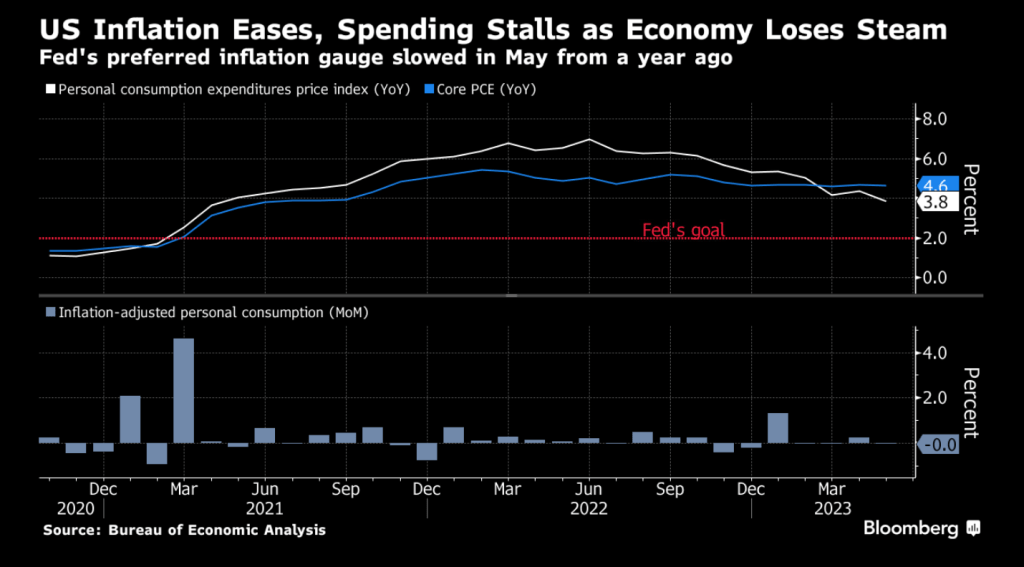

The Federal Reserve’s preferred measures of US inflation cooled (slightly) in May and consumer spending stagnated, suggesting the economy’s main engine is starting to lose some momentum.

The personal consumption expenditures price index rose 0.1% in May, Commerce Department figures showed Friday. From a year ago, the measure eased to the slowest pace in more than two years.

Consumer spending, adjusted for prices, was little changed after a downwardly revised 0.2% gain in April. From February through May, household spending has essentially stalled after an early-year surge. Spending on merchandise dropped, while outlays for services increased.

Excluding food and energy, the so-called core PCE price index increased 4.6% from May 2022. That’s in line with annual readings back to late 2022 and shows minimal relief from elevated price pressures. Economists consider this to be a better gauge of underlying inflation.

Indicator

Actual

Estimate

PCE price index (MoM)

+0.1%

+0.1%

Core PCE price index (MoM)

+0.3%

+0.3%

PCE price index (YoY)

+3.8%

+3.8%

Core PCE price index (YoY)

+4.6%

+4.7%

Real consumer spending (MoM)

0.0%

+0.1%

Under the hood of the government report, a key metric flagged by Fed Chair Jerome Powell showed a welcome slowdown. Services inflation excluding housing and energy services increased 0.2% in May from a month earlier, the smallest advance since July of last year, according to Bloomberg calculations. The figure was up 4.5% from a year ago.

The Taylor Rule now suggests a target rate of 10%. We are just halfway to target!

Meanwhile, Yellen Plans July China Trip, While US Preps Investment Curbs. Trying to convince China that the US won’t default on its $32 TRILLION and growing debt?

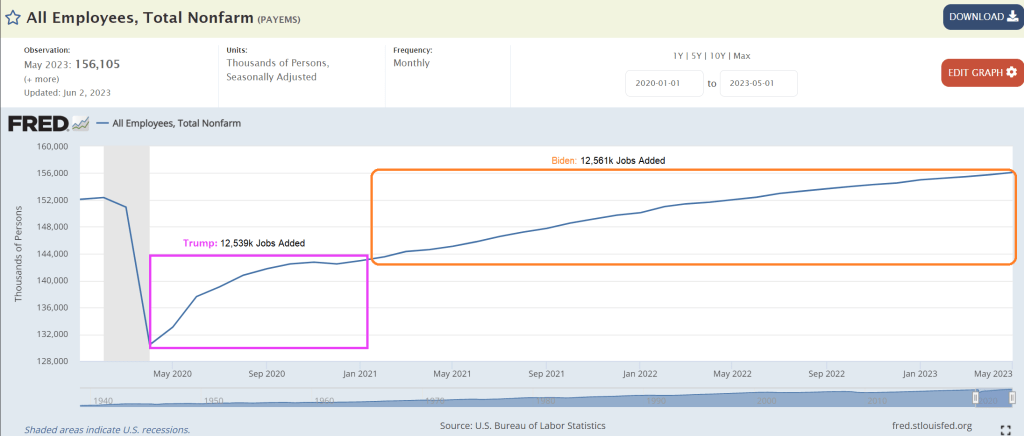

Bidenomics is a great marketing ploy where you have out of control Federal spending and magically decide to reopen the economy and school after Covid and focus only on jobs added after Biden was selected President and ignore the jobs added during Trump.

Real gross domestic income (GDI) is a measure of the incomes earned and the costs incurred in the production of gross domestic product. It’s another way of measuring U.S. economic activity. BEA also publishes the average of real GDP and real GDI.

REAL GDI dropped to -0.8% QoQ for Q1 2023. Kind of looks like Bidenomics is running out of gas.

On Biden’s claims that he created twice as many jobs as any other President, the US economy add 12.53 million jobs after April 2020 (Trump) while Bidenomics created took 2 1/2 years to add 12.56 million jobs.

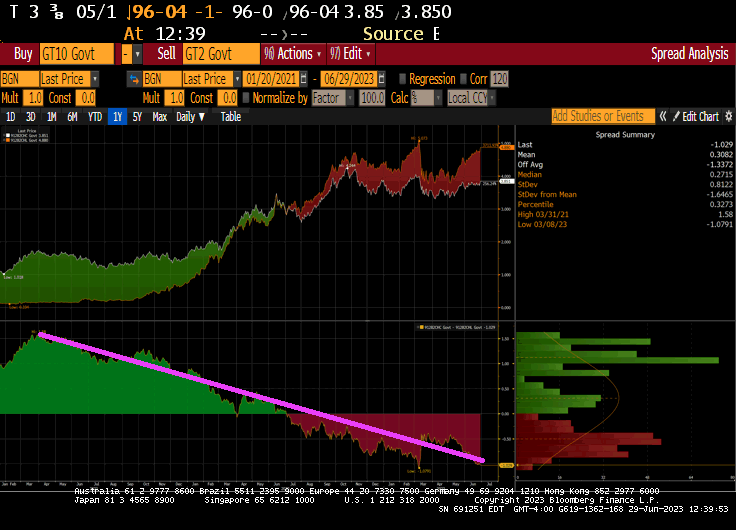

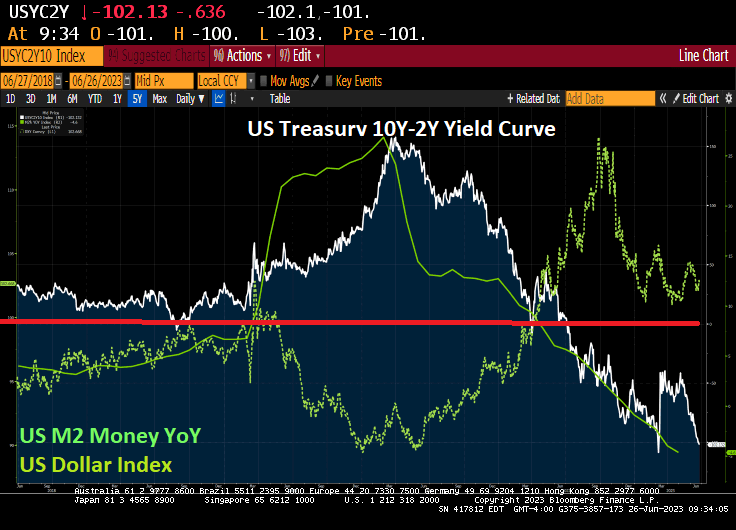

The US Treasury yield curve (10Y-2Y) is now inverted at -103 basis points.

As Fed stimulus wears out, so is the Treasury 10Y-2Y yield curve.

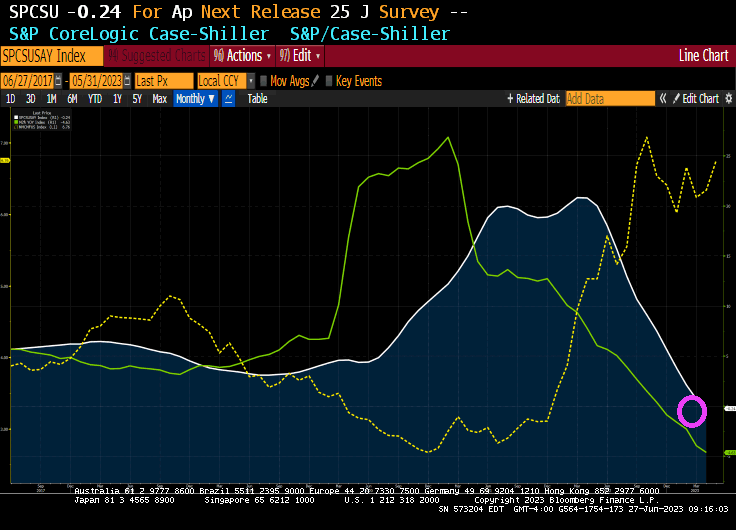

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a -0.2% annual decrease in April, down from a gain of 0.7% in the previous month. The 10-City Composite showed a decrease of -1.2%, down from the -0.7% decrease in the previous month. The 20-City Composite posted a -1.7% year-over-year loss, down from -1.1% in the previous month.

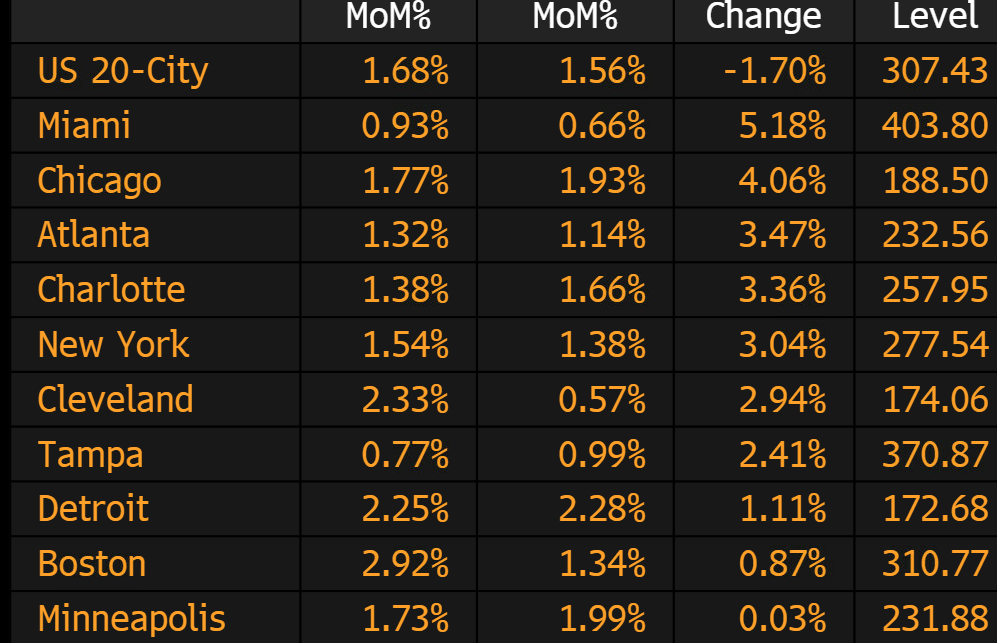

The winners in April? Miami and … Chicago?

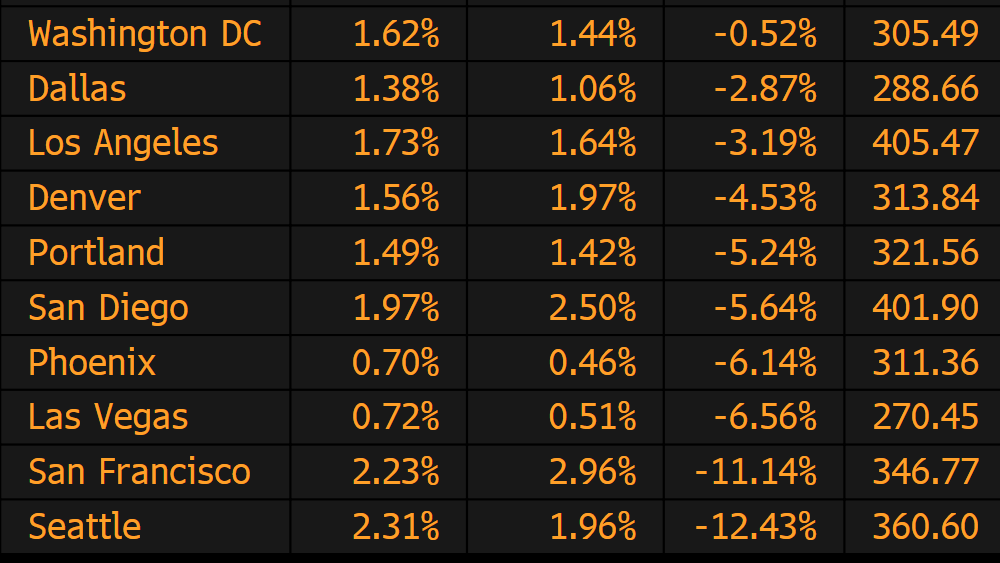

The biggest losers in April? Seattle and San Francisco both suffered YoY losses over -11%.

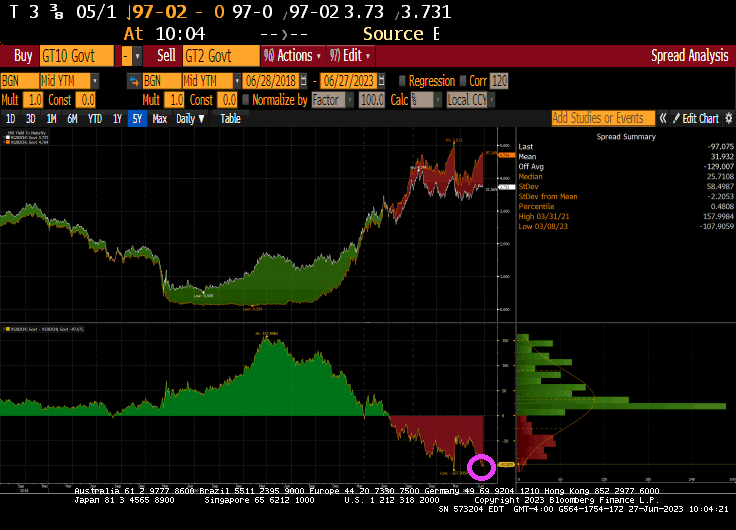

The US Treasury 10Y-2Y yield curve remains steeply inverted at -97 basis points.

Silverado! No, not the Chevy full-size pickup truck, but the precious metal Silver is up over 1% this morning!

The US Treasury 10Y-2Y yield curve remains inverted at -102.7 basis points for the 244th straight day as M2 Money YoY (aka, liquidity) evaporates.

Silver is up over 1% this morning.

Bitcoin Cash is up12.39% this morning.

Speaking of Silverado, a fully loaded new 2023 Chevy Silverado 1500 ZR2 costs around $100,000. Thanks Biden and Powell (BiPow?). Try financing that purchase with auto loan rates soaring!

I could have used 3 shades of Joe, but 50 shades of Joe sounds better!

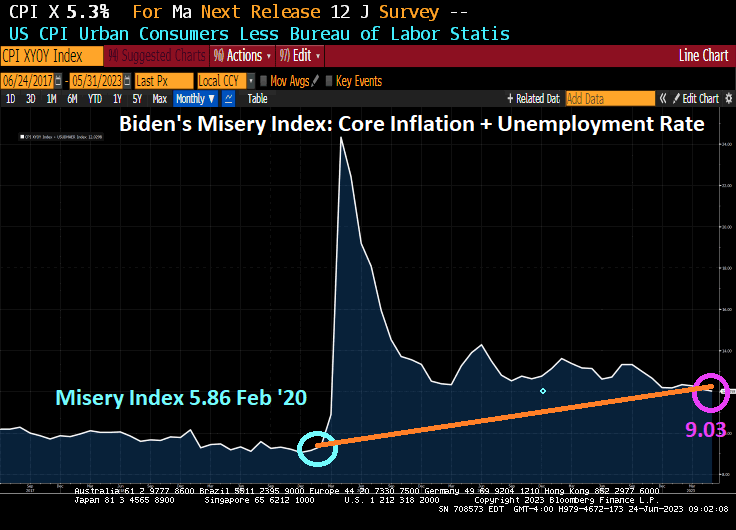

But the fact remains that Americans are far more miserable under Biden than they were under Trump before the Chinese Wuhan Covid virus was unleashed. 9.03 today (Core CPI YoY + U-3 Unemployment) than it was in February 2020 under Trump (5.86). While not twice as bad, inflation is continues to cause serious problems for America’s middle class and low-wage workers.

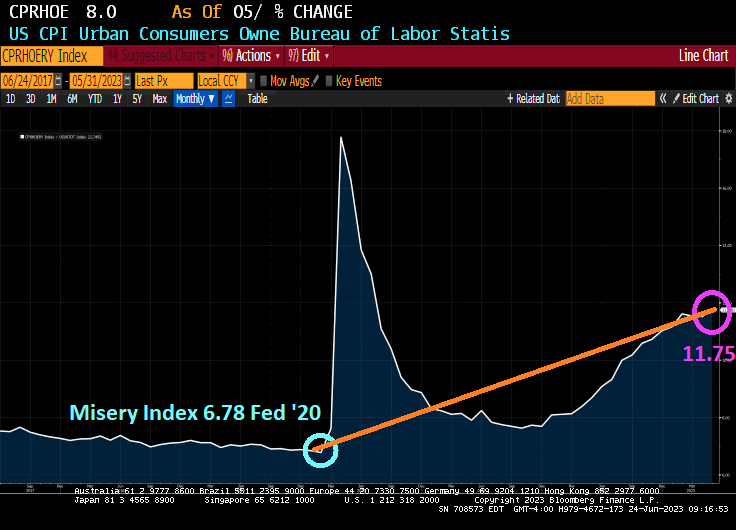

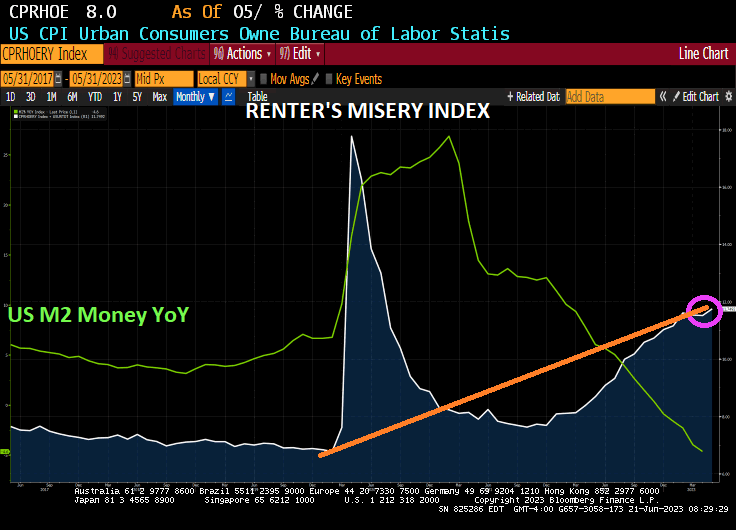

Speaking of the middle class and low wage workers, let’s look at the Renter’s Misery index (CPI Owner’s equivalent rent YoY + Unemployment rate). It was 6.78% in February 2020 under Trump and before Covid struck and is now 11.75% under Inflation Joe.

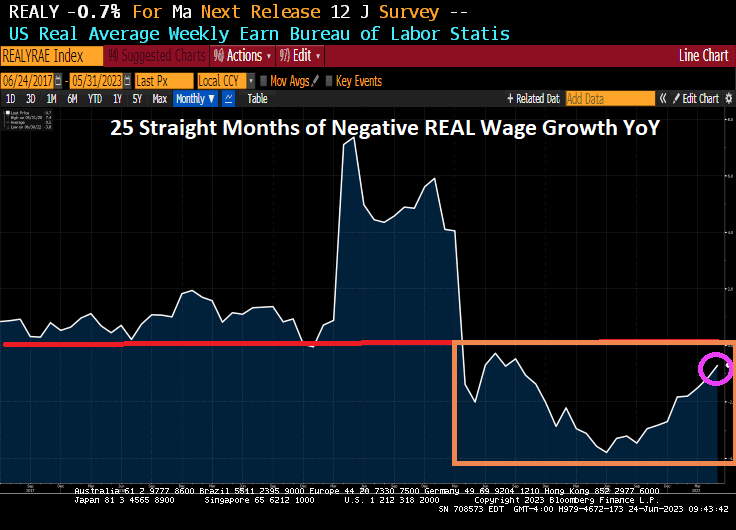

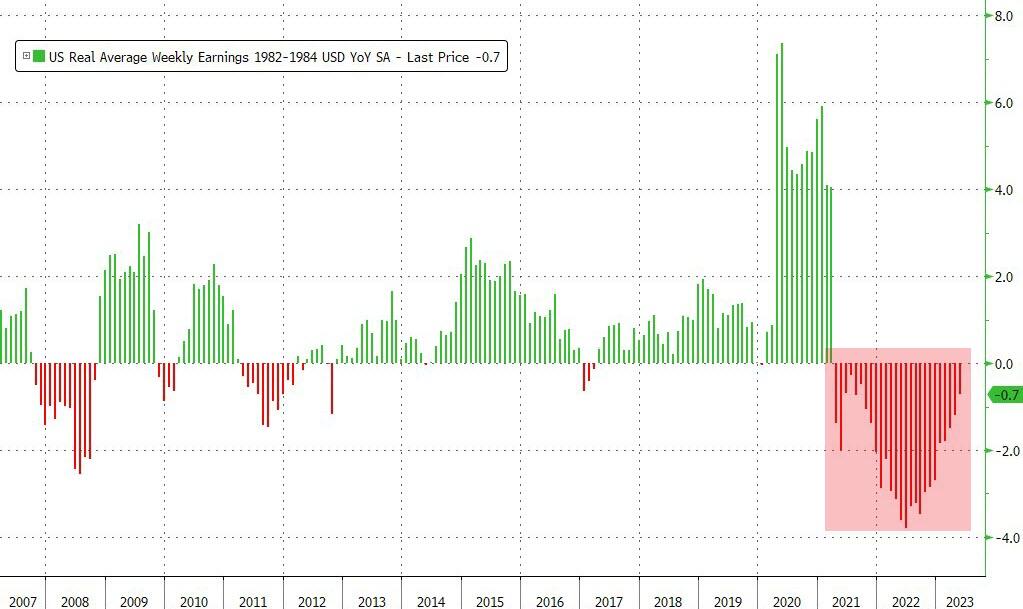

Speaking of misery, how 25 straight months of negative REAL wage growth? Real weekly wage growth went negative in April 2021, just a few months after Biden was installed as President.

Now, there was winners under Biden. Green energy donors, the big banks, big pharma, big tech, but media … essentially any big donors from big entities got massive payoffs. The middle class and low-wage workers? As Jerry Reid once sang, “They got the coal mine and we got the shaft.”

Expect a hawkish Fed Chairman Jerome Powell to double down on the Fed’s commitment to vanquish inflation at his semiannual testimony before Congress on June 21-22. While the immediate audience will be lawmakers, the message will be aimed at markets, which remain unconvinced the Fed will hike by another 50 basis points, as indicated in the dot plot from the June FOMC meeting. Powell may raise his hawkish tone to push back against such views.

Even as Powell is putting on a hawkish performance, confirmation hearings for World Bank Executive Director Adriana Kugler — as well as to extend Fed Governor Lisa Cook’s term — could reinforce the dovish faction on the Fed, somewhat diluting Powell’s message.

What we expect at the June 21-22 hearings:

The updated dot plot from the June FOMC meeting shows a majority of FOMC participants anticipate at least 50 bps more of rate hikes this year. Markets aren’t convinced – as of the time of writing, futures point to a 74% chance of rate hike in July and only a 10% chance of an additional rate hike in 2023.

Powell’s main task at the testimony will be to convince markets that officials stand behind the dot plot and anticipate multiple hikes.

Powell will likely be asked why the FOMC didn’t hike in June if inflation remains a threat. He’ll say that 500 bps of hikes to date allow the central bank to moderate its pace while gauging economic conditions, and will appeal to the Fed’s dual mandate as warranting a cautious approach. That will be music to the ears of Democrat lawmakers.

Powell said a decision on whether to hike at the July FOMC meeting will be “live.” We take that to mean the bar not to hike will be high, but it’s not a done deal. Powell will likely clarify that comment at his testimony.

The published semiannual monetary policy report offers a preview of how Powell will make the hawkish case:

While the labor market is still “very tight,” it has been softening gradually — and by some measures, labor-market tightness has eased “more substantially over the past year.”

Some outside studies are arguing that wages did not contribute to or lead inflation, but the monetary-policy report notes that “prospects for slowing inflation may depend in part on a further easing of tight labor-market conditions.” Thus, the Fed still stands by the conventional economic wisdom that the Phillips Curve is well and alive – and that a tradeoff exists between inflation and the unemployment rate.

Powell will probably reiterate that low inflation is a necessary condition for achieving the Fed’s mandate, as he has many times before: “Restoring price stability is essential to set the stage for achieving maximum employment and stable prices over the longer run.”

Our view is that if inflation remains as high as the FOMC projects, it would be appropriate for the Fed to hike by at least 50 bps more. But the latest batch of indicators show some encouraging progress on goods and housing disinflation; as a result, our baseline is for inflation to fall short of the median FOMC participant’s forecast.

The Senate Banking Committee hearing on the nominations of Cook, Kugler and Vice Chair Philip Jefferson will likely be less eventful. During this period of high inflation, nominees will need to lean more hawkish in their public statements than they otherwise would.

Nevertheless, if the full slate of nominees is confirmed, it will add one more dove to the board of governors, heightening discord on the FOMC.

Jefferson’s nomination to the vice-chair post vacated by Lael Brainard won’t affect policy direction, as he’s already serving on the board. He previously was confirmed by a vote of 91-7, and we expect his confirmation as vice chair to be similarly easy.

Though we have yet to hear much from Kugler on her monetary-policy outlook, her research focus on labor markets creates a likely bias toward the maximum-employment element of the Fed’s dual mandate.

In addition to Jefferson and Kugler’s nominations, Cook — whose term is slated to end in January 2024 — would see her governorship extended for the full 14-year term. If confirmed, it would keep her dovish voice on the FOMC longer than before.

Cook, who is perceived as more dovish and more political than the other nominees — she’s a former adviser to the Biden transition team – saw her previous nomination barely confirmed 51-50, with Vice President Kamala Harris casting the tie-breaking vote. It’s unclear if she’ll have enough support this time to clear the confirmation hurdle.

Bottom line: The hearings present an opportunity for Powell to bring market pricing in line with what has been put forth in the FOMC’s Summary of Economic Projections. We are doubtful that he will succeed.

The most recent Fed dots plot suggests rate declines in future years.

Cryptos are up this morning.

Commodities are down this AM.

So, like in the film Blue Velvet, we have the choice between Michelob or Pabst Blue Ribbon. Powell is choosing …. PBR!!

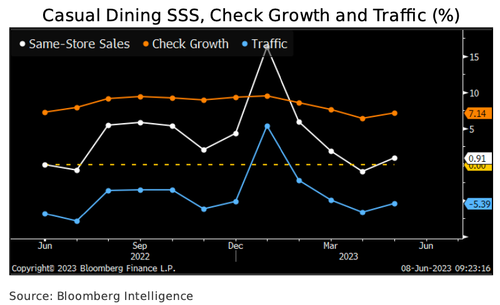

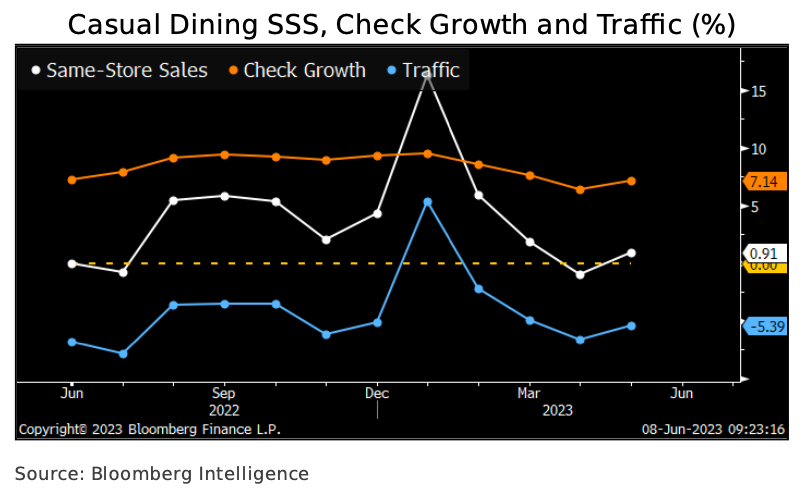

Bloomberg Intelligence’s Michael Halen penned a new note titled “2H Restaurant Sales: Inflation Killing Appetites.” It outlines, “Consumer spending finally buckles under more than two years of inflation and price hikes,” and the likely result is a trade-down of casual-dining chains like Brinker and Cheesecake Factory for quick-service chains like McDonald’s and Wendy’s.

The trade-down, which could start as early as this summer, is expected to dent consumer spending in restaurants such as Cheesecake Factory, Texas Roadhouse, and at brands operated by Brinker and Darden, Halen said.

Casual-dining industry same-store sales rose just 0.9% in May, according to Black Box Intelligence, as traffic dropped 5.4%. We expect cash-strapped low- and middle-income diners to cut restaurant visits and checks through year-end due to more than two years of real income declines and ballooning credit-card balances.

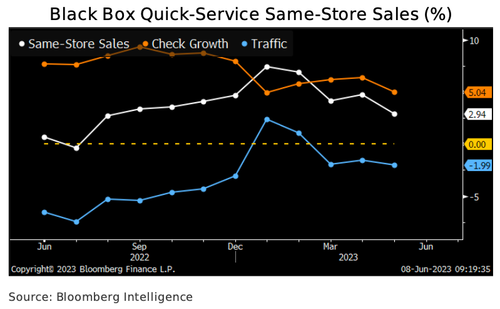

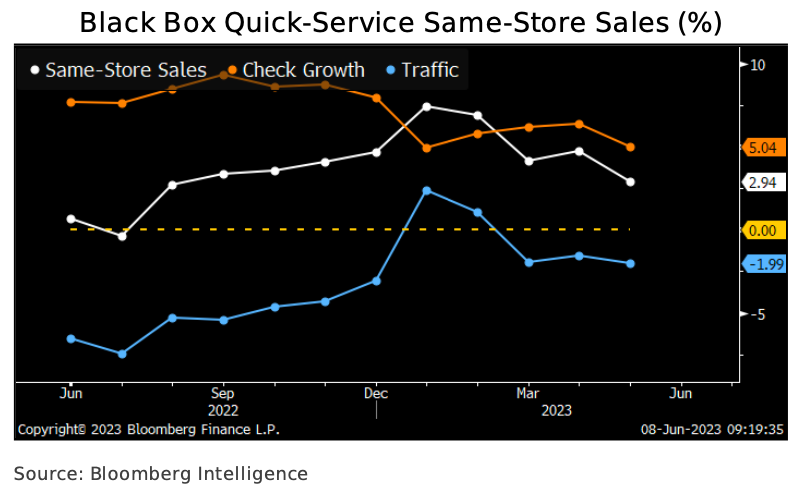

Halen provides more details about quick-service restaurants to fare better than causal-dining ones as “consumer spending finally buckles.”

Quick-service restaurants’ same-store sales could moderate with consumer spending in 2H but should fare better than their full-service competitors. Results rose 2.9% in May, according to Black Box data, as a 5% average-check increase was partly offset by a 2% guest-count decline. Check- driven comp-store sales gains are unsustainable, and we think inflation and menu price hikes will motivate low- and middle-income diners to reduce restaurant visits and manage their spending in 2H. On Domino’s 1Q earnings call, management said lower-income consumers shifted delivery occasions to cooking at home. Still, a trade-down from full-service dining due to cheaper price points may cushion the blow.

McDonald’s, Burger King, Wendy’s, and Jack in the Box are among the quick-service chains in Black Box’s index.

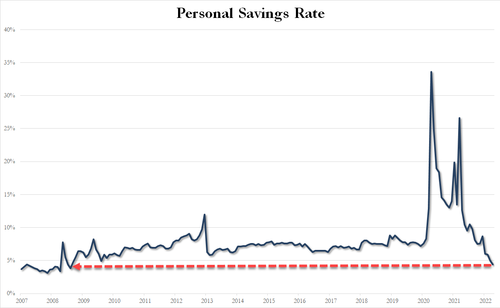

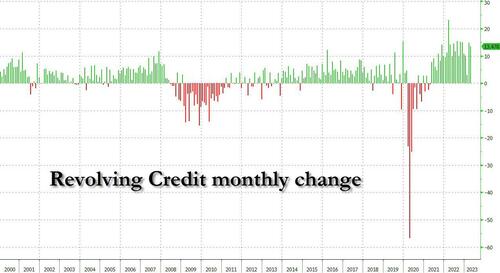

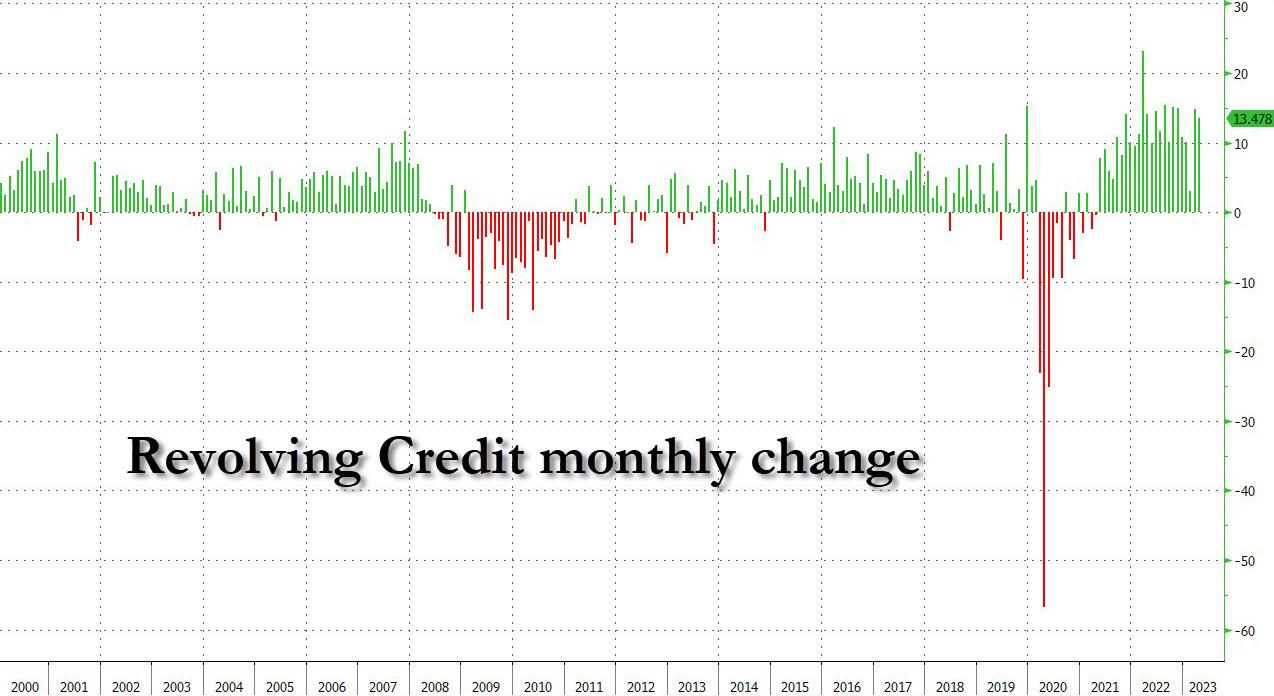

The latest inflation data shows consumers have endured the 26th straight month of negative real wage growth. What this means is that inflation is outpacing wage gains. And bad news for household finances, hence why many have resorted to record credit card usage.

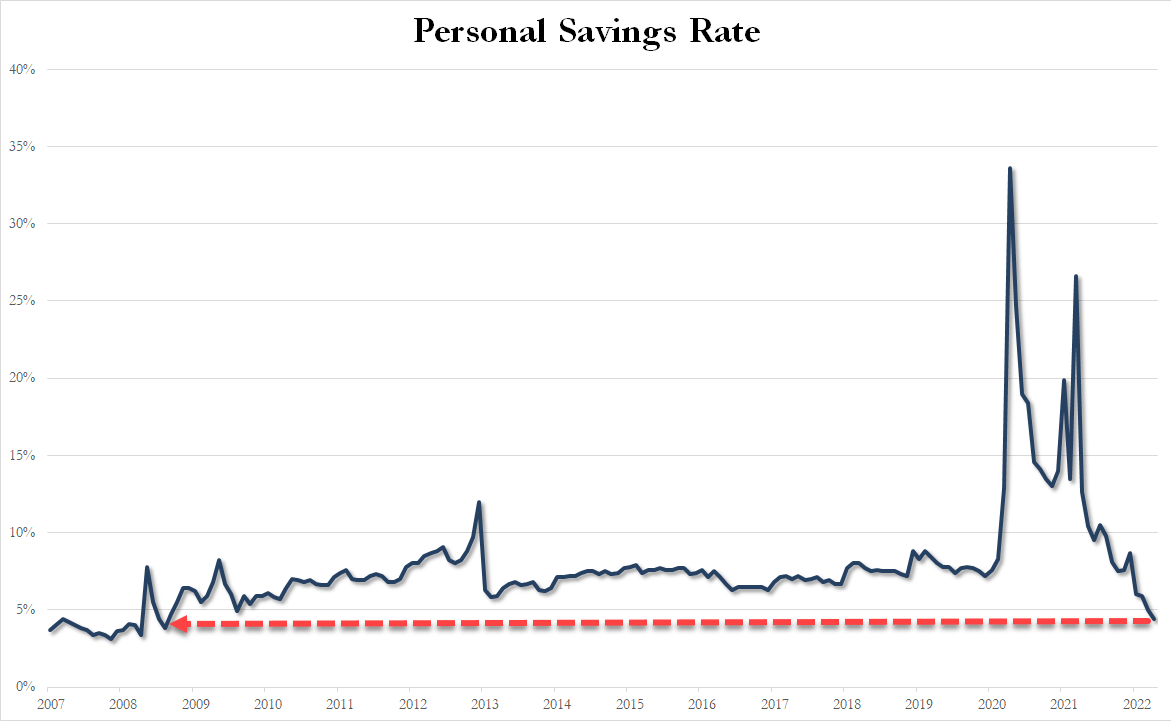

And the personal savings rate has collapsed to just 4.4%, its lowest level since Sept. 2008 (the dark days of Lehman). And why is this? To afford shelter, gas, and food, consumers are drawing from emergency funds due to the worst inflation storm in a generation.

As revolving consumer credit has exploded higher and the last two months have seen a near-record increase…

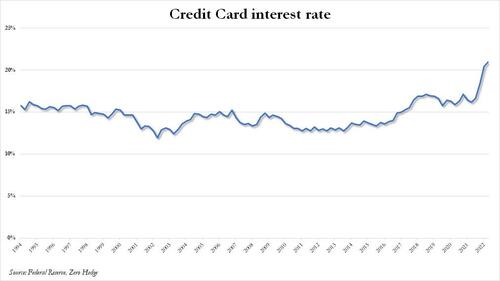

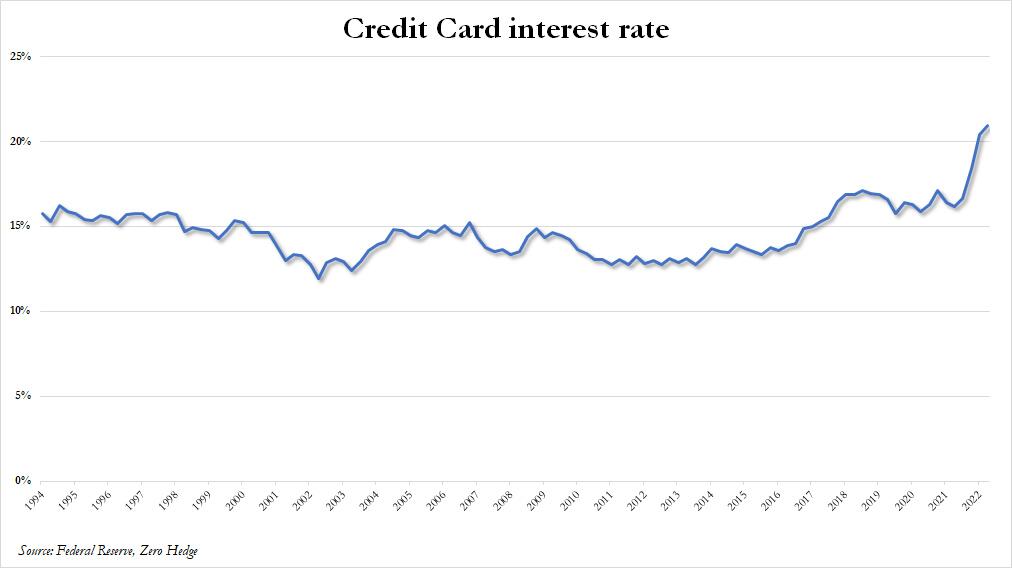

… even as the interest rate on credit cards has jumped to the highest on record.

With record credit card debt load and highest interest payments in years, plus depleted savings, oh yeah, and we forgot, the restart of student loan payments later this year, this all may signal a consumer spending slowdown at causal diners while many trade down for McDonald’s value menu. Even then, we’ve reported consumers have shown that menu items at the fast-food chain have become too expensive.

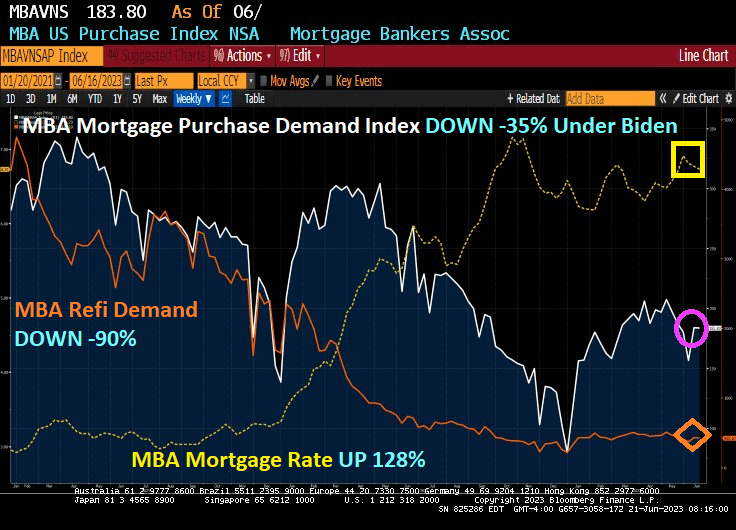

The good news? Mortgage purchase demand fell only -0.05% from last week. The bad news? Mortgage purchase demand is down -35% since Resident Biden was sworn in. And mortgage refinancing demand is down a whopping -90%. Reason? Mortgage rates are up 128% under Clueless Joe.

Mortgage applications increased 0.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 16, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 0.5 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 1 percent compared with the previous week. The Refinance Index decreased 2 percent from the previous week and was 40 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index decreased 0.1 percent compared with the previous week and was 32 percent lower than the same week one year ago.

And as Paul Harvey used to say, here is the rest of the story.

And the renter’s misery index, CPI for owner’s equivalent rent YoY + U-3 unemployment rate, is now a staggering 11.75% verus 6.78% in February 2020, the last month before the Chinese Wuhan virus led to economic and school shutdowns. And we have Donald Trump as President instead of this corrupt clown.

What is the difference between baseball legend Shoeless Joe Jackson and Clueless Joe Biden? While both sold out their teams for personal wealth, at least Shoeless Joe was good at baseball. Clueless Joe is a corrupt bully. Shoeless Joe was allegedly stupid, but so is Clueless Joe.

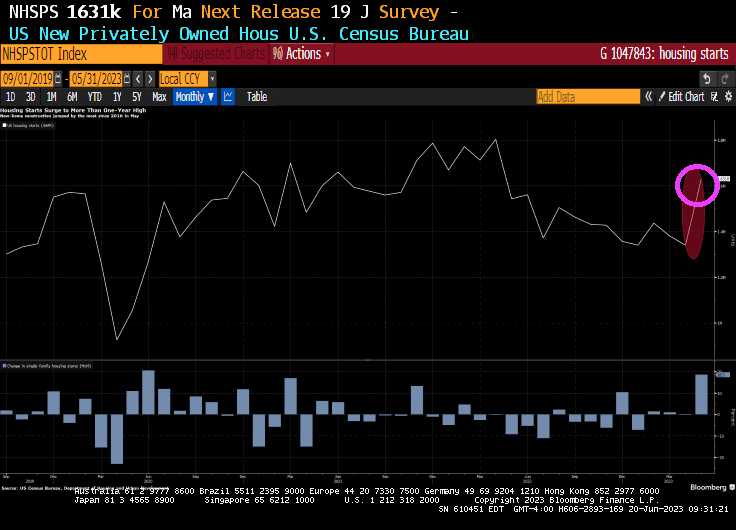

Well, not really unexpected since the housing sentiment index for home builders was above 50 yesterday. But with The Fed pausing rate hikes, housing starts are soaring!

US housing starts unexpectedly surged in May by the most since 2016 and applications to build increased, suggesting residential construction is on track to help fuel economic growth.

Beginning home construction jumped 21.7% to a 1.63 million annualized rate, the fastest pace in more than a year, according to government data released Tuesday. The pace exceeded all projections in a Bloomberg survey of economists. Single-family homebuilding rose 18.5% to an 11-month high.

Applications to build, a proxy for future construction, climbed 5.2% to an annualized rate of 1.49 million units. Permits for one-family dwellings increased.

Metric

Actual

Est.

Housing starts (SAAR)

1.63 mln

1.4 mln

One-family home starts (SAAR)

997,000

na

Building permits (SAAR)

1.49 mln

1.425 mln

One-family home permits (SAAR)

897,000

na

The figures corroborate Federal Reserve Chair Jerome Powell’s comments last week that the housing market has shown signs of stabilizing. Homebuilders, which are responding to limited inventory in the resale market, have grown more upbeat as demand firms, materials costs retreat and supply-chain pressures ease.

The housing starts data will feed into economists’ estimates of home construction’s impact on second-quarter gross domestic product. Prior to the report, the Atlanta Fed’s GDPNow forecast had residential investment subtracting about 0.1 percentage point from gross domestic product. Homebuilding last contributed to growth in the first quarter of 2021.

At the same time, elevated mortgage rates are crimping affordability, suggesting limited momentum in housing demand.

The increase in starts from a month earlier was the biggest since October 2016 and reflected gains in three of four US regions. Starts of apartment buildings and other multifamily projects jumped more than 27%.

The number of homes completed increased to a 1.52 million annualized rate. The level of one-family properties under construction were little changed at 695,000.

Existing-home sales data for May will be released on Thursday, while a report on new-home purchases is due next week.

Now only has The Fed paused, but the most recent Fed Dots Plot reveals that Fed open market committee (FOMC) members see The Fed slashing rates over the coming years. Just in time for creepy, demented Grandpa Joe to be reelected as President. In other words, the return of ZORP (zero outrageous rate policy).

Maybe The Fed should adopt the Coca Cola slogan “The Pause That Refreshes!”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.