The 10Y-2Y yield curve hit the worst inversion since 2000 as the curve slope hit -47.7 basis points, inverting another -2.267 basis points today.

Yes, the 10Y-2Y Treasury yield curve is SCREAMING RECESSION.

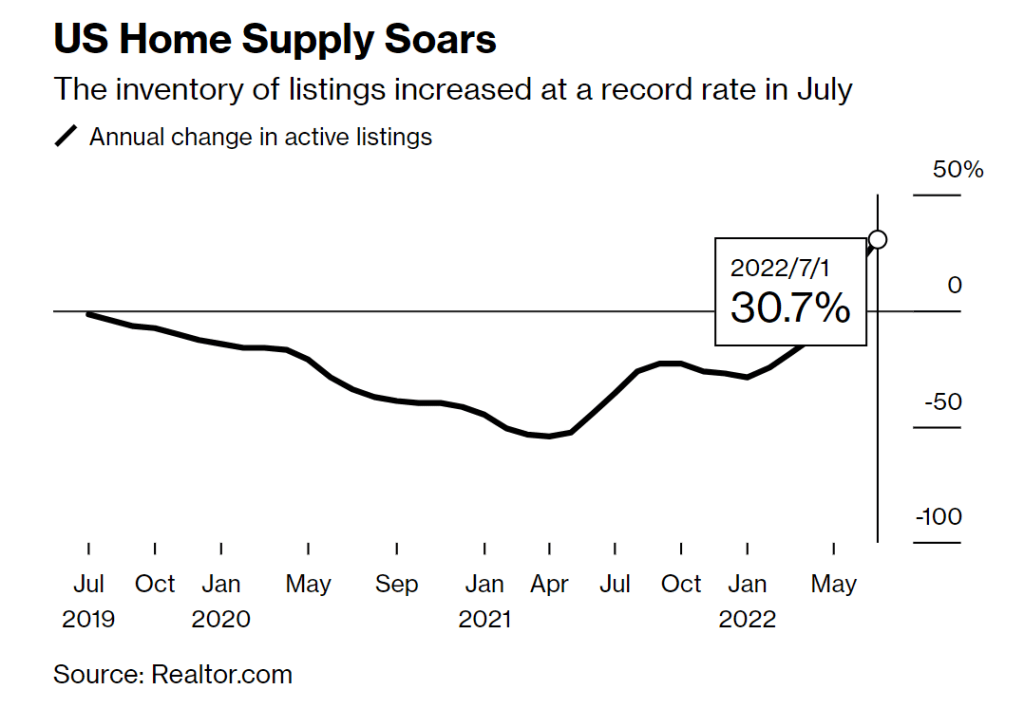

(Bloomberg) – Prashant Gopal – The supply of homes for sale across the US grew at a record rate last month, another sign that higher mortgage costs are cooling down the housing market.

The number of active listings nationwide jumped 31% from a year earlier, a record-high increase for a third straight month, according to a report Tuesday by Realtor.com.

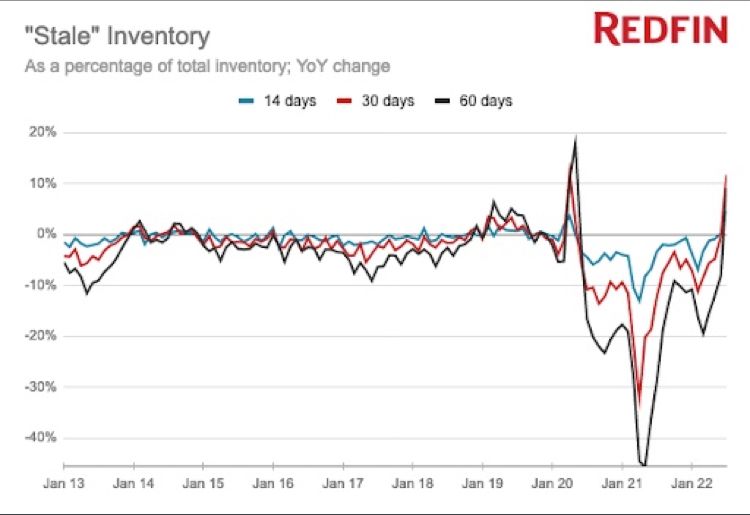

And according to Redfin, stale inventory is accelerating.

The US housing market is simply unaffordable for millions of Americans. To illustrate the problem, here is a chart of the Case-Shiller National home price index less CPI YoY graphed against Average Hourly Wages less CPI YoY.

The gap between the REAL national home price index YoY and REAL US average hourly earnings YoY is near the largest since 1988. Inflation is making matters far worse since REAL average hourly earnings growth continues to decline.

The only thing positive to say is that REAL home price growth YoY is lower now than at the peak of the 2005 home price bubble that burst catastrophically.

Another “positive” is that the REAL 30-year mortgage rate has fallen to -3.23%. At the peak of the house price bubble in June 2005, the REAL 30-year mortgage rate was +2.58%. THAT is one big difference between the pre-2008 recession and today’s impending recession.

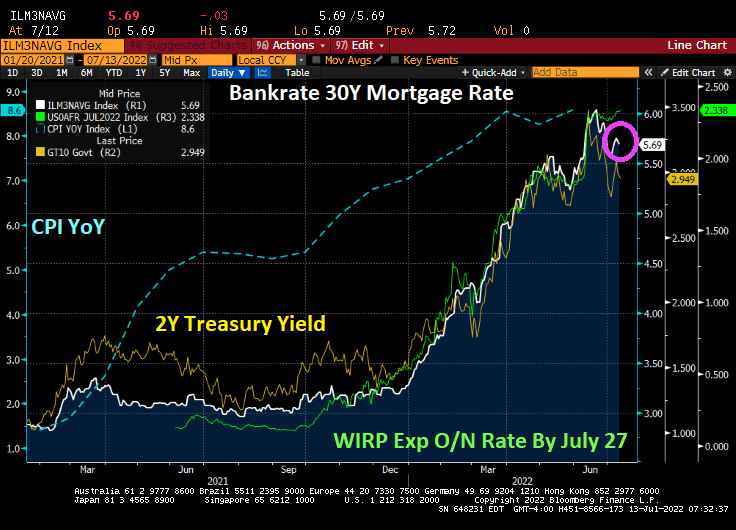

Here is your weekend update on Treasury and Mortgage markets.

The current US Treasury 10Y-2Y yield curve just slipped further into reversion at -40.299 basis points, screaming impending recession. Oddly, The Federal Reserve has been leaving its balance sheet of Agency Mortgage-backed Securities (MBS) in tact (green line).

On the mortgage front, Bankrate’s 30-year mortgage rate index rose to 5.60% while the affordability-friendly 5/1 Adjustable Rate Mortgage (ARM) rate rose to 4.21%.

Currently, a 5/1 ARM borrower can save 139 basis points over the traditional 30-year mortgage rate.

Today’s jobs report was … strange. While the US economy added more jobs than expected, we also saw labor force participation contract and real wage growth decline again.

The reaction in the bond market? US Treasury 10-year yields exploded by +14 basis points. As I used to tell my fixed-income students, any basis point jump or decline of 10 basis points or more is a BIG DEAL.

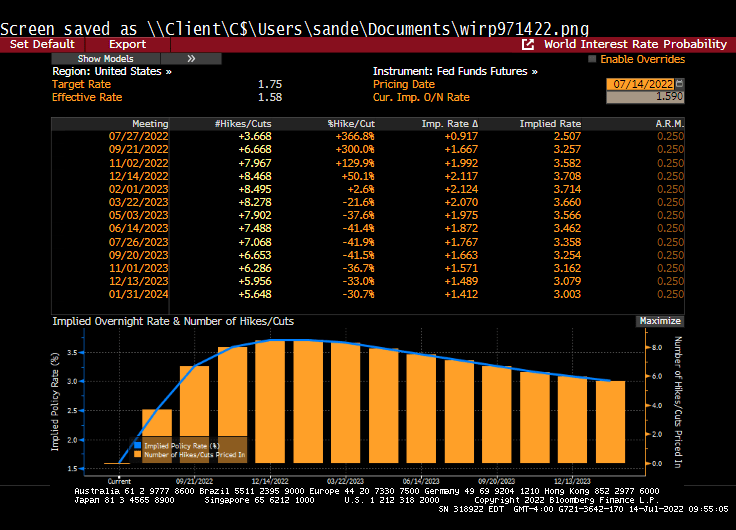

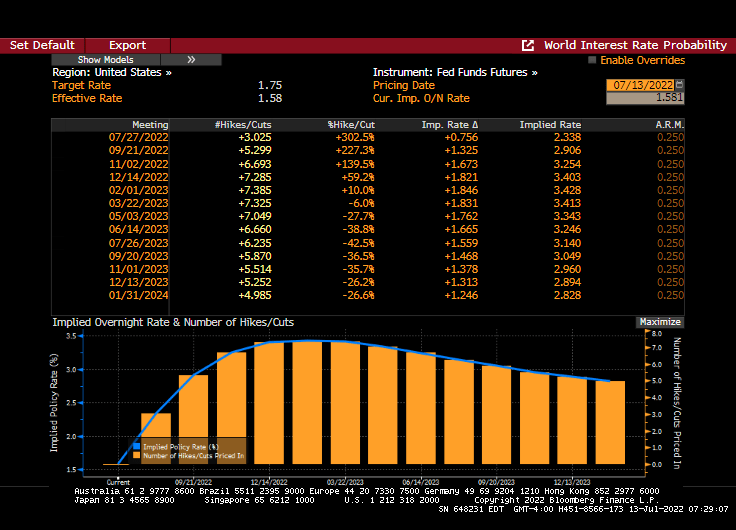

The implied target rate for The Fed (based on Fed Funds Futures) is now lower for the Jan 1, 2024 FOMC meeting (3.025%) than it is for the Sept 21, 2022 FOMC meeting (3.034%).

Mortgage rates? They will go up as The Fed removes its Brawndo, the economy mutilator.

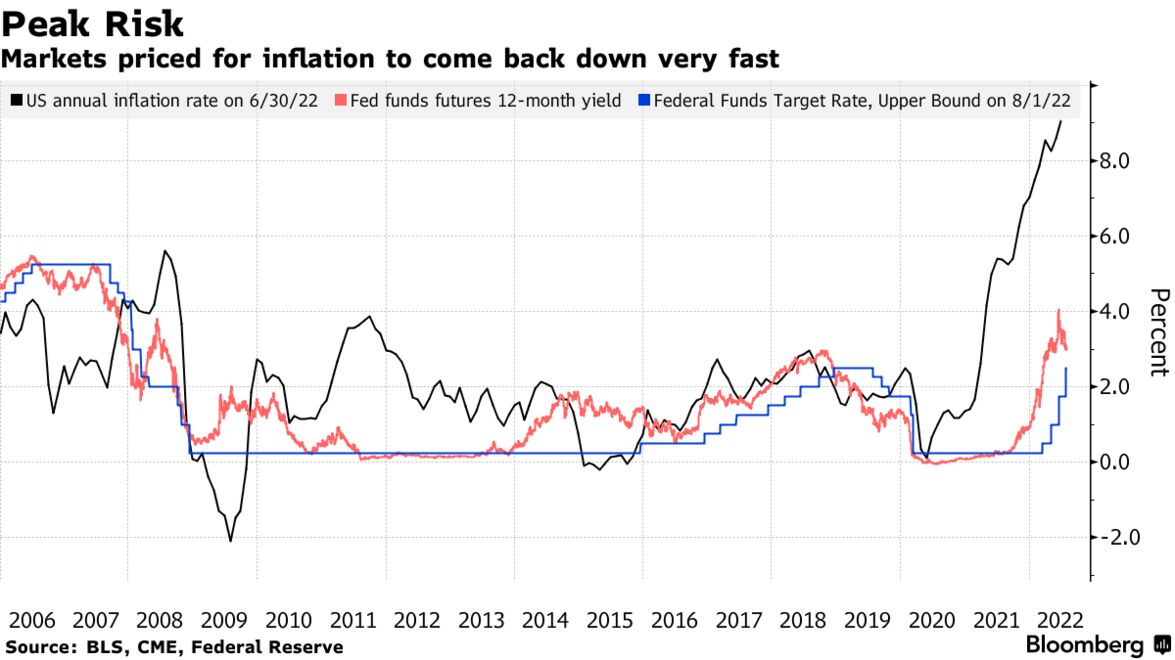

The US economy may need to undergo a deeper and longer recession than investors currently anticipate before inflation can be brought under control, according to Zoltan Pozsar of Credit Suisse Group AG.

Markets expect the surge in consumer prices will soon peak and central banks will become less hawkish, but there’s a high risk that global cost pressures will remain elevated, Pozsar, global head of short-term interest-rate strategy at Credit Suisse in New York, wrote in a client note.

The world is being wracked by an economic war that’s undermining the deflationary relationships that have prevailed in recent decades where Russia and China supplied cheap goods and services to more developed nations such as the US and those in Europe, he said.

“War is inflationary,” Pozsar wrote. “Think of the economic war as a fight between the consumer-driven West, where the level of demand has been maximized, and the production-driven East, where the level of supply has been maximized to serve the needs of the West.” That pattern held “until East-West relations soured, and supply snapped back,” he said.

The result is that inflation is now a structural problem, rather than a cyclical one. Supply disruptions have arisen from the changes in Russia and China, along with tighter labor markets due to immigration restrictions and a reduction in mobility caused by the coronavirus pandemic, Pozsar said.

There’s now a risk the Federal Reserve under Chair Jerome Powell has to raise interest rates to 5% or 6% and keep them there to create a substantial and sustained reduction of aggregate demand to match the tighter supply profile, he said.

‘More Misguided’

Connect the dots on the biggest economic issues.Connect the dots on the biggest economic issues.Connect the dots on the biggest economic issues.

Dive into the risks driving markets, spending and saving with The Everything Risk by Ed Harrison.Dive into the risks driving markets, spending and saving with The Everything Risk by Ed Harrison.Dive into the risks driving markets, spending and saving with The Everything Risk by Ed Harrison.

Sign up to this newsletter

Pozsar’s warning that inflation will stay elevated puts him at odds with the Treasury market, which rallied last month as investors switched their focus to recession risks from inflation concern. While an economic slowdown typically weighs on consumer prices, the latest annual US inflation reading of 9.1% for June remains far above the Fed’s 2% goal, although the price surge is forecast to slow for the first time in three months to 8.8% in July according to a Bloomberg poll of economists.

The bond market is more misguided now than at any other time this year as traders wager the US central bank will start cutting rates in early 2023, Bloomberg Economics’ chief US economist Anna Wong and her colleagues said this week. Money markets are wagering on almost one percentage point of hikes by year-end followed by a quarter-point cut by June.

“Interest rates may be kept high for a while to ensure that rate cuts won’t cause an economic rebound (an ‘L’ and not a ‘V’), which might trigger a renewed bout of inflation,” Pozsar wrote in his note. “The risks are such that Powell will try his very best to curb inflation, even at the cost of a ‘depression’ and not getting reappointed.”

Speaking of “recession,” the US Treasury 10Y-2Y yield curve has inverted even further to -31.69 BPS.

We are seeing a slowing of the US economy. For example, the JOLTs (job openings) numbers are out for June and they are down -5.5% from May. And from April to May, JOLTs declined -3.2% MoM. That is a clear slowing trend.

And on the housing front, the CoreLogic HPI Forecast indicates that home prices will increase on a month-over-month basis by 0.6% from June 2022 to July 2022 and on a year-over-year basis by 4.3% from June 2022 to June 2023. But rose +18.3% YoY in June. Also a clear cooling trend.

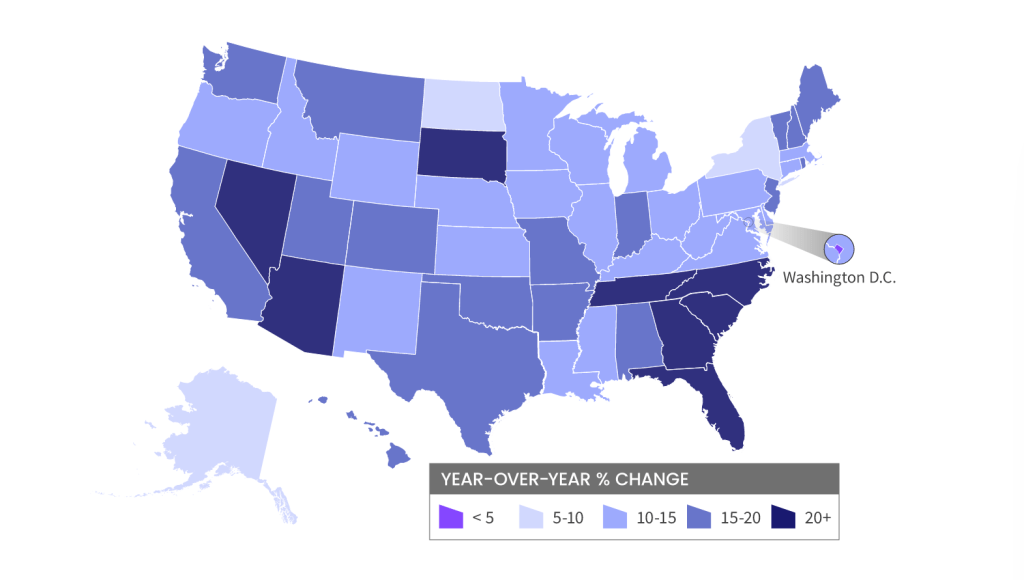

And its “Escape From Blue States” (perhaps a new Kurt Russell movie), with home prices rising fastest in red states (primarily The South). And contiguous migration from California to Nevada and Arizona.

The Fed Funds Futures market is pricing in rate hikes until the March 2023 FOMC meetings. After all, Prince Imhotep (aka, Minneapolis Fed’s Neel Kashkari) is screaming for more rate hikes to fight inflation … caused by 1) loose monetary policies since late 2008 and 2) insane Federal government spending.

Let’s see if “Mr. Freeze” (aka, Jerome Powell) relents on Fed rate increases before the March 2023 FOMC meeting.

Instead of The Boston Strangler, we now have the DC Strangler. Better known as The Federal Reserve and their war on inflation.

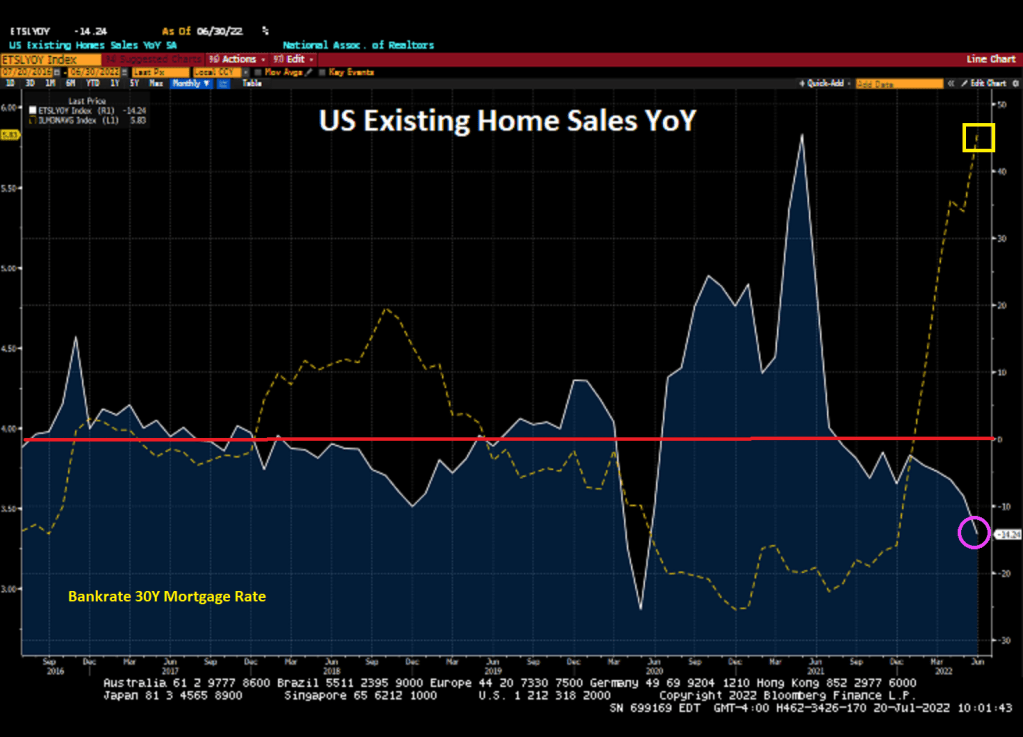

US existing home sales crashed -14.24% YoY and -5.40% MoM in June as The Fed tightens its icy grip on the housing market. Existing home sales were lower than expected at 5.12 million home sold SAAR.

Median price for existing home sales declined to 13.27% YoY as inventory available for sale remains MIA. And The Fed’s balance sheet is still out in force.

The US housing market in terms of sales has entered a bear market, but with The Fed’s balance sheet stimulus still hunting asset prices, it is a grizzly bear market in terms of affordability.

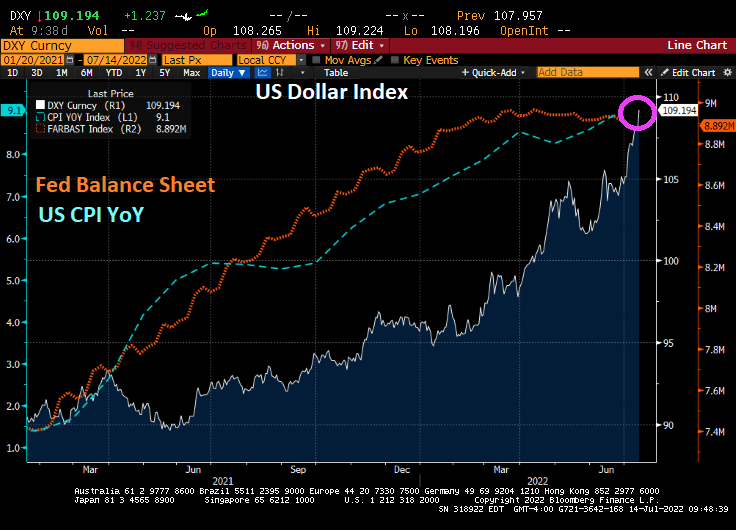

Bear in mind that a strong dollar is a two-edged sword. The US Dollar Index has risen 16% year-over-year, presenting a big hurdle for US firms with business overseas.

That strength of the greenback will rise until the Fed makes a dovish policy pivot.

And that pivot is forecast to occur at the Feb ’23 FOMC meeting.

The Federal Reserve is reversing its excessive monetary stimulus policies left over from the financial crisis of 2008 (and Covid) and the mortgage industry and potential home buyers are paying the price.

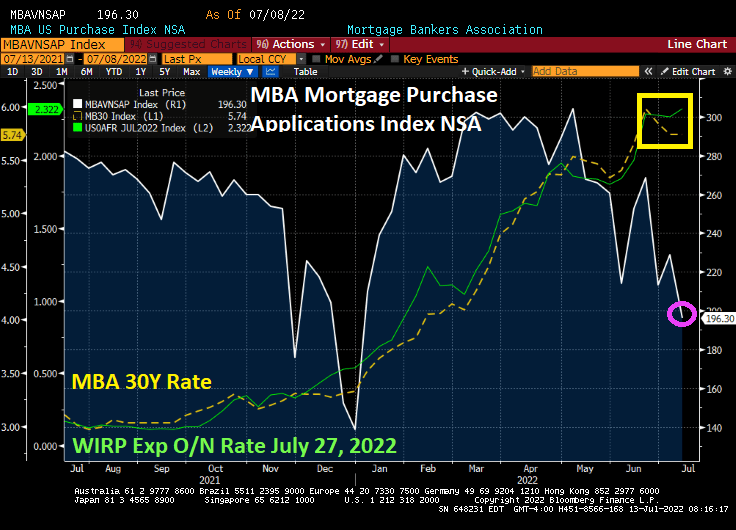

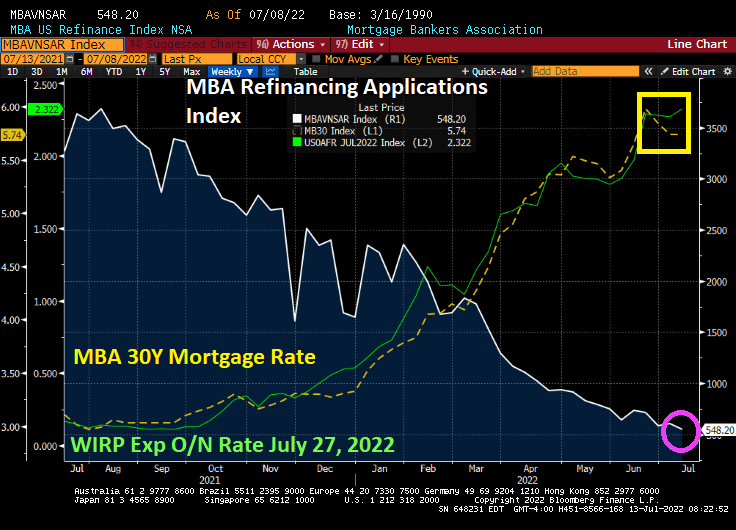

Mortgage applications decreased 1.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 8, 2022. This week’s results include an adjustment for the observance of Independence Day.

The seasonally adjusted Purchase Index decreased 4 percent from one week earlier. The unadjusted Purchase Index decreased 14 percent compared with the previous week and was 18 percent lower than the same week one year ago.

The Refinance Index increased 2 percent from the previous week and was 80 percent lower than the same week one year ago.

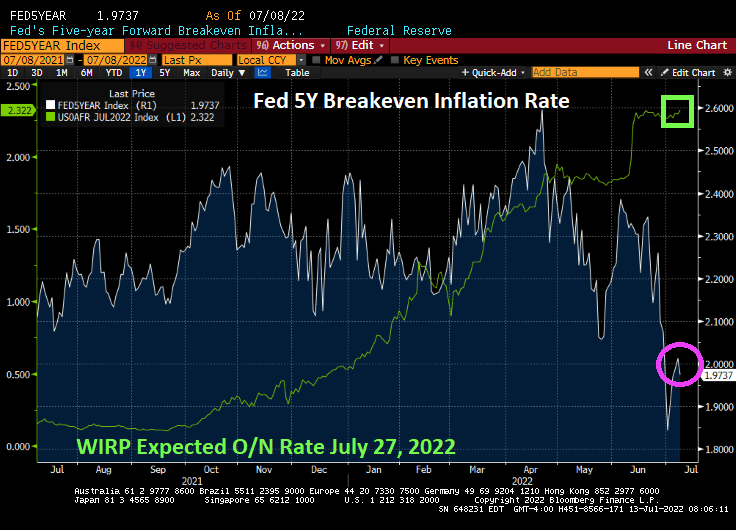

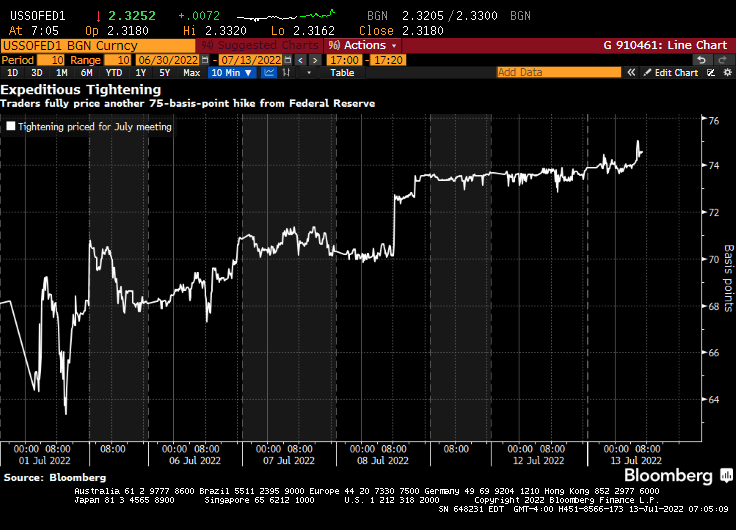

Here we go loop de loop! Traders are pricing in a 75 basis point rate increase at the July FOMC meeting despite collapsing Fed 5-year inflation breakeven rates.

Money markets are betting on a three quarter-percentage point hike by Federal Reserve officials later this month, wagering the US will need to ramp up the pace of monetary tightening to tame inflation.

The repricing comes ahead of a key inflation report due Wednesday. The headline figure for June is set to accelerate to 8.8% year over year, the highest since 1981.

Bankrate’s 30Y mortgage rate fell slightly ahead of today’s inflation report with the expectation of The Fed hiking their target rate by 75 basis points to 2.338% at the July 27th Fed Open Market Committee meeting.

Trader expectations from Fed Funds Futures data:

Last night I watched “The Shallows” on Peacock TV. I thought from the title that it was going to be a biography of The Federal Reserve, but it was a film about a surfer being attacked by a shark.

You must be logged in to post a comment.