The Federal Reserve forecast for the US economy is a dismal 0.50% YoY. Do I detect a trend?

The FOMC forecast for 2023 and 2024. Core PCE YoY (inflation) is forecast to drop to 3.50%, still considerably higher than The Fed’s target rate of inflation of 2%. And unemployment is forecast to be 4.60%.

To cope with Bidenflation, US personal savings rate as of October is -67.9% YoY. The “good” news is that rents YoY are crashing. But food prices under Inflation Joe remain very high. But most everything is slowing down, not due to Biden’s policies, but a global and US economic slowdown.

With a big slowdown coming our way, you can understand why The Fed’s December Dot Plot is showing declining Fed Funds Target rate starts declining in 2024.

Even US mortgage rates are headed down.

Speaking of going down, cryptos are down across the board with Cardano leading the decline at -6.91%.

Here is a chart (courtesy of Zero Hedge) showing reported payrolls and REVISED payrolls. Somehow, I don’t think Jean Pierre (Biden’s spokesperson, not the French chef) will be touting “Unlike Trump, our administration barely added any jobs in March, April, May and June 2022.

How will this revelation influence the Fed’s open market committee (FOMC) going forward knowing that the Biden Administrations job creation claims are wildly overstated?

Perhaps it doesn’t matter since Bernanke, Yellen and Powell don’t follow any rules (like the Taylor Rule), but generally with job creation almost nonexistant in March through June of 2022, The Fed should be cutting rates like mad. But wait! Can they with significant inflation?

The good news is that inflation is coming off its peak, but will take a while to get to The Fed’s 2% target. Hence The Fed may raise their target rate since they cannot achieve it will energy price up substantially since Biden became President.

The numbers coming out today are not good. November numbers were 1) US Industrial Production was down -0.2% MoM, 2) manufacturing production is down -0.6%, 3) retail sales advanced down -0.6% (most in 11 months) and …

The Empire State Manufacturing outlook was down -11.2% and the Philadelphia Fed (or Phed) business outlook was down -13.8% in November.

And with all this bad news, global equity markets are dropping like a paralyzed falcon.

But at least Biden traded a dangerous international arms dealer for WBNA star Brittney Griner. Possilby the worst trade in history after the Chicago Cubs traded future Hall of Famer Lou Brock for sore-arm pitcher Ernie Broglio. Griner is Ernie Broglio.

Fun week ahead. US inflation numbers are out on Tuesday (forecast? CPI YoY = 7.3%, Core CPI YoY = 6.1%) and The Federal Reserve’s Open Market Committee (FOMC) rate decision is on Wendesday.

So, where are we sitting on Monday?

First, the US Treasury 10Y-2Y yield curve has been inverted (a precursor to recession) for 116 straight days). Second, the likelihood of recession in 2023 is 100%. Third, with the forecast of core inflation at a still numbing 6.1%, The Fed seems dead set on raising their target rate by 50 basis points to 4.50% on Wednesday.

dddd

So, as The Fed debates recession versus fighting inflation (partly caused by The Fed), we have Kevin Malone from The Office debating Angela versus double-fudge brownies:

Central bankers won’t ride to the rescue when growth slows in this new regime, contrary to what investors have come to expect. They are deliberately causing recessions by overtightening policy to try to rein in inflation. That makes recession foretold. We see central banks eventually backing off from rate hikes as the economic damage becomes reality. We expect inflation to cool but stay persistently higher than central bank targets of 2%.

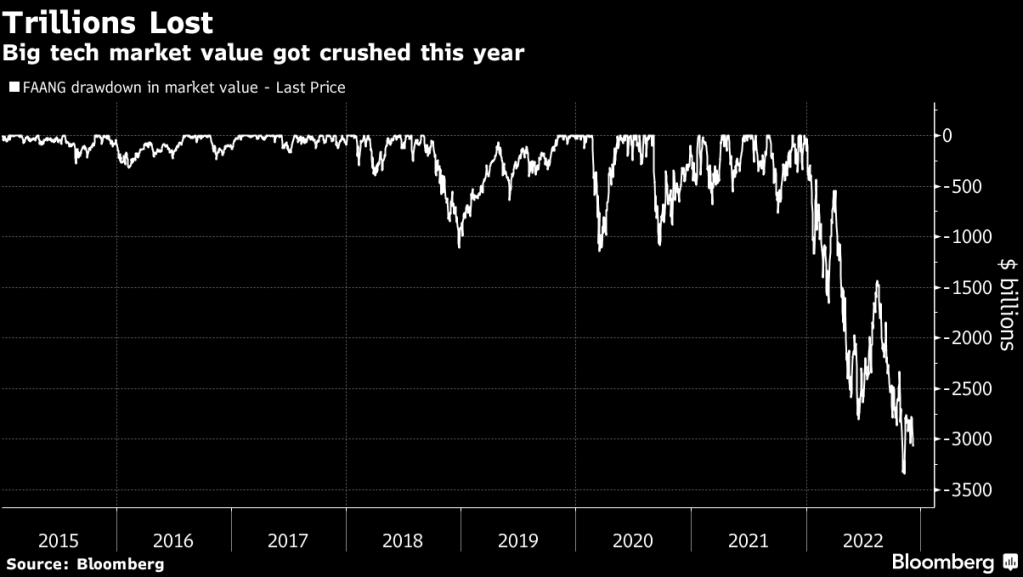

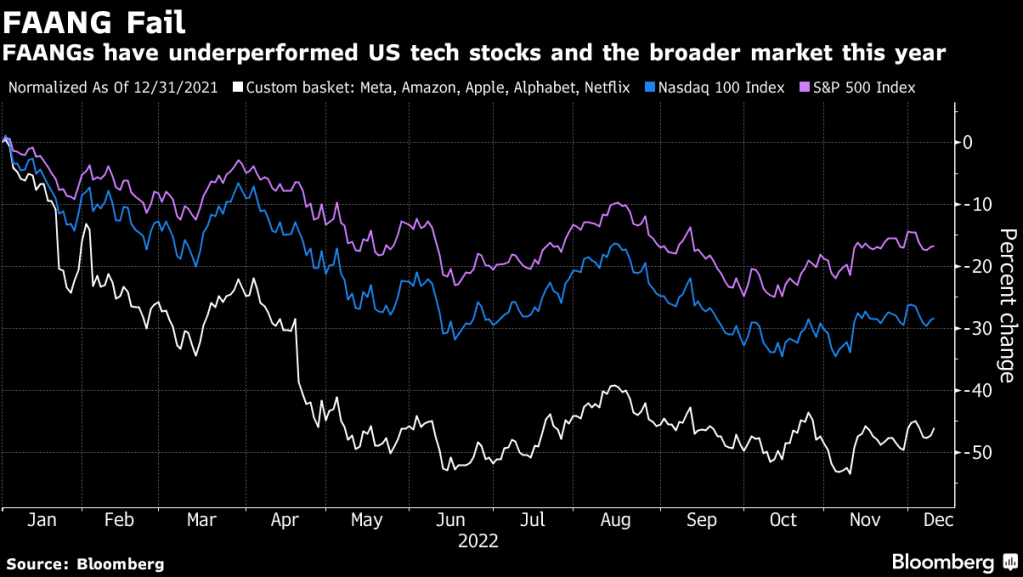

For some investors, this year’s rout in high-flying technology stocks is more than a bear market: It’s the end of an era for a handful of giant companies such as Facebook parent Meta Platforms Inc. and Amazon.com Inc.

Those companies — known along with Apple Inc., Netflix Inc. and Google parent Alphabet Inc. as the FAANGs — led the move to a digital world and helped power a 13-year bull run. And FAANG drawdown have reached over $3 trillion.

FAANGs (Meta, Amazon, Apple, Alphabet, Netflix) are getting clobbered in 2022.

Typically, when The Fed prints too much money, such as 10% or higher (red line), inflation follows. Particularly when The Fed prints at 25% YoY in Q4 2020, it was followed by the highest inflation rate in 40 years. But if M2 Money continues to slow, inflation will likely slow, but not to The Fed’s target of 2%.

Despite what Minneapolis Fed’s Neal Kashkari said about The Fed having infinite printing resourses, The Fed is going to fight inflation THAT THEY HELPED CAUSE. Biden’s energy policies (did you see that Elon Musk has a car that uses plentiful hydrogen?), and excessive Federal spending by Biden/Pelosi/Schumer, are culprits in creating the supply chain problems facing America. BUT after the 25% surge in M2 Money in 2020 and 2021, we saw M2 Money VELOCITY crash and burn to its lowest level in history. Which means the “bang for the buck” for printing more money is negligible.

Of course, big tech firms got caught influencing the 2020 Presidential election (see Musk’s release of Twitter files) and engaged in restriction of the 1st Amendment (Freedom of Speech). How much will that impact FAANG stocks going foward?

And yes, the US Treasury yield curve is inverted pointing to a recession in 2023.

And yes, apparently Biden was complicit in the Twitter fiasco.

This will be the last time (Fed rate hikes) as the US economy is forecast to either go into a recession in 2023 or slow down to an anemic 1.20% Real GDP YoY. Even the Fed is forecasting 3.10% core inflation in 2023, still higher than their target rate of 2%.

One of the sectors that is suffering is commercial real estate.

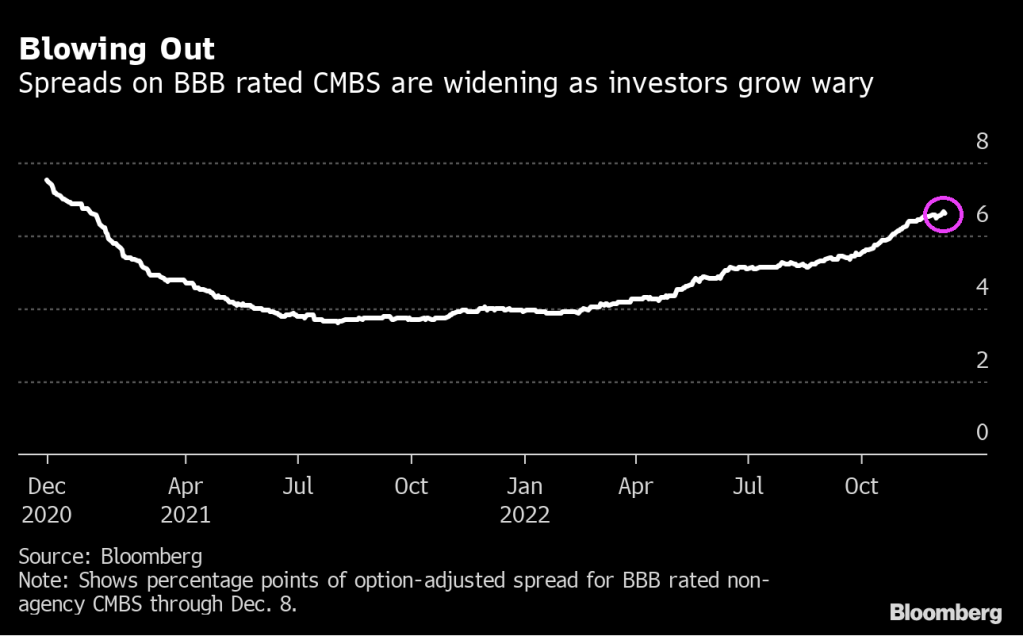

Commercial mortgage bonds could get clobbered in the coming months, and investors are backing away from the securities.

Some $34 billion of the bonds come due in 2023, and refinancing property loans is difficult now. Property prices could fall 10% to 15% next year, according to JPMorgan Chase & Co. strategists. And some types of properties seem particularly vulnerable as, for example, city workers are slow to come back to their offices full time.

That may be why spreads on BBB commercial mortgage bonds have widened by about 2.7 percentage points this year through Thursday to around 6.6%, for the securities without government backing. They are now at their widest since January 2021. They’ve been getting hit particularly hard in the last few months, even as risk premiums on investment-grade and high-yield corporates have been shrinking on hopes the Federal Reserve will scale back its tightening campaign.

“For CMBS investors, there’s lots of uncertainty, especially around whether maturing loans are going to get refinanced or not, and if not, what the resolution will be,” said David Goodson, head of securitized credit at Voya Investment Management, in an interview. “Layering in risk from lower office utilization makes the assessment even tougher.”

The trouble that the bonds face won’t necessarily translate to a surge in defaults in the near term, which is part of why betting against them is so difficult. When property owners can’t refinance mortgages that have been bundled into bonds, noteholders have a difficult choice to make. They can seize the buildings and liquidate them, or they can extend the debt and accept repayment later. They usually go for the second option.

Extending maturities allows bondholders to kick the can down the road and potentially recover more later, said Stav Gaon, head of securitized products research at Academy Securities. The question is whether properties have permanently lost value as, for example, people reorder their lives after the pandemic, or whether declines may be more temporary because of higher rates.

“Foreclosing on a loan, rather than granting an extension, can be really messy — that’s a lesson that was learned during the great financial crisis,” said Gaon. “The lenders also recognize that today’s higher interest rates are a very sudden development that many high-quality borrowers need time to adjust to.”

Some investors that are still buying are focusing on higher-quality borrowers and properties, that are likelier to withstand any downturn in real estate prices without having to seek extensions on loans.

“We think trophy properties will fare better due to better access to the debt markets, lower potential property declines, and a continued tenant flight to quality,” said Zach Winters, senior credit analyst at USAA Investments.

He acknowledges that this strategy isn’t always popular now, even if it turns out to make sense.

“When we go out and bid on a bond tied to a trophy office building now, usually the number of buyers is significantly less than before,” Winters said.

After the Pandemic

The market for commercial mortgage bonds without government backing was about $670 billion as of the end of 2021, and although the securities soared in the second half of 2020 as the Fed opened the money spigots, they’re facing more difficulty now. With office occupancy still below 50% in many cities as more people work from home, corporate buildings may see their values drop. Retail space is similarly under pressure as consumers have grown used to buying more online. And while travel volume is rising, many hotels are struggling to reach 2019 levels for room charges.

A survey of institutional real estate market professionals in November found that firms expect office values to fall about 10% next year, and overall commercial property declines of 5%, according to the Pension Real Estate Association.

The $34 billion of bonds due next year includes mostly fixed-rate CMBS bonds sold without government backing. It’s a steep increase from the $24.4 billion of such bonds maturing this year, according to Academy Securities.

There’s another $103 billion of a type of CMBS known as single-asset single-borrower bonds maturing next year, according to Academy — although most of that debt pile has a built-in contractual ability to extend loans, meaning they’ll be able to seek extensions more easily.

Next year won’t be the first time that CMBS bondholders and servicers have faced tough choices about whether to allow en masse extensions to the underlying borrowers. After the 2008 financial crisis, commercial property values plummeted and many lenders chose to give owners of those properties more time to pay back their loans. As a result they ended up getting more money back than if they’d immediately foreclosed on the loans and liquidated the properties, said Jeff Berenbaum, head of CMBS and agency CMBS strategy at Citigroup.

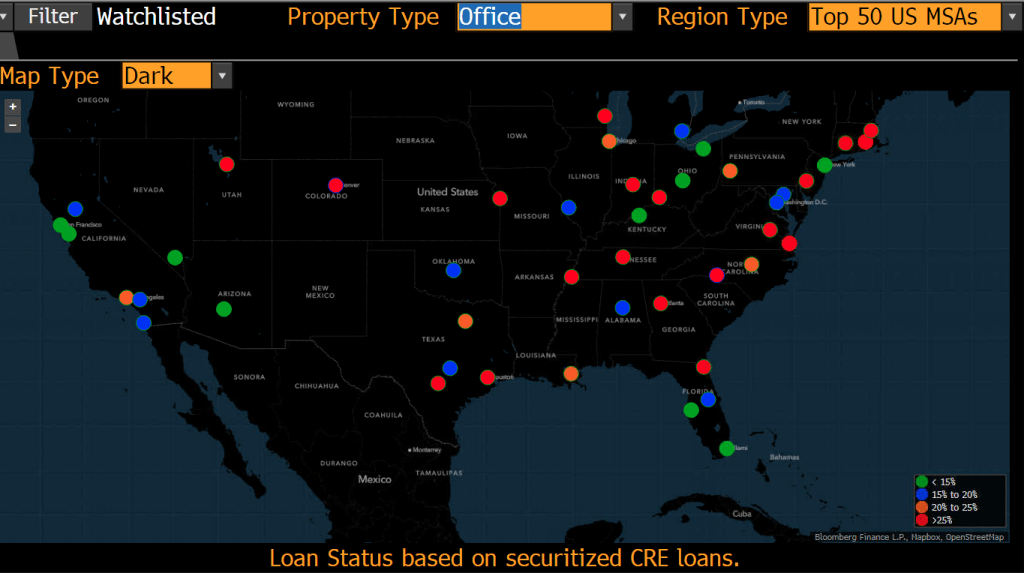

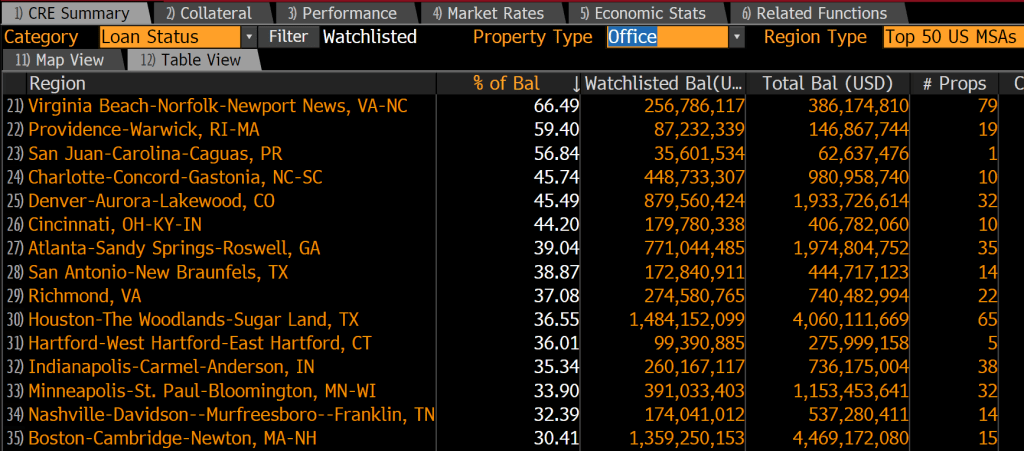

In terms of watchlisted CMBS loans, currently most of the USA is in the green (good) except for San Francisco, New Orleans, Memphis and Chicago all have elevated commercial loans on the watchlist (loans being watched for going late and into default). Puerto Rico is also in the red (>25%) watchlisted commercial loans, so I expect AOC to be asking for a bailout.

On the office property front, we can see red (>25% of commercial loans watchlisted) pretty much across the board.

The leading metro area in terms of watchlisted office property loans is … Virginia Beach-Norfolk-Newport News VA-NC at 66.49% (that is pretty bad). Providence RI is second and San Juan Puerto Rico is third followed by Charlotte NC in fourth place. The only Ohio city in top 15 is Cincinnati, home of Skyline Chili and Montgomery Inn.

While most are calling for more rate hikes in 2023, I predicted that December’s likely 50 basis point hike with be the last one for a while as the US economy grinds to a halt. Or it’s all over now for Fed rate hikes.

While The Fed predicts slow growth, markets are pointing to recession. The Fed is out of touch with reality. As is the US Secretarty of Treasury, “Too low for too long” Janet Yellen.

The good news for Americans? The global slowdown is helping to lower US Treasury yields which, in turn, helps to help to lower US mortgages rates. Kind of a perverse “good news” story when you think about it.

The bigger picture is the slowdown caused by 1) a global economic slowdown and 2) the tightening of Fed monetary policy to fight inflation.

Look at the Case-Shiller national home price growth YoY (blue line) against M2 Money growth YoY (green line). Just move the green line to the right and it covers home price growth. Both are slowing down with anticipated Fed rate hikes (red line) now at 50 basis points for the December 14th FOMC meeting. And note that The Fed’s balance sheet (orange line) has barely budged.

Unlike Archie Bell and the Drells, this tighten-up is about The Federal Reserve tightening-up its monetary policy.

On December 31, 2021, the US Treasury yield curve (10Y-2Y) stood at +77.4 basis points, generally a good omen.

Then markets woke up. And not in a woke way.

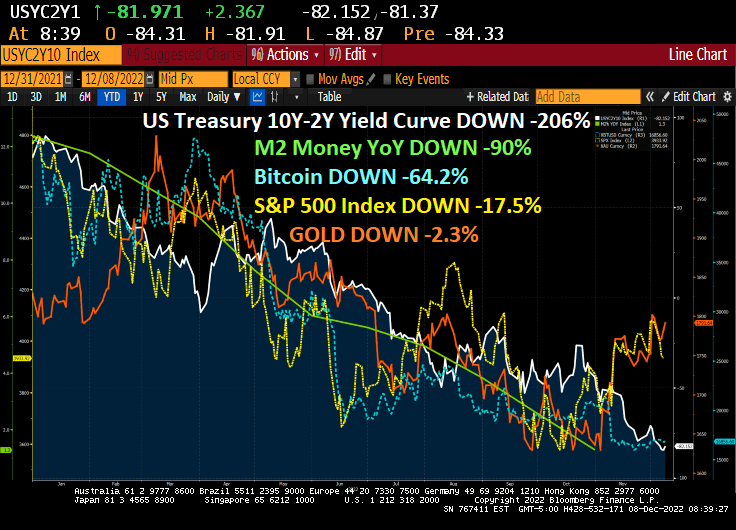

As The Fed tightens to tamp down on inflation in 2022, we are seeing a pattern. The US Treasury 10Y=2Y yield curve has sunk to -82 basis points, a -206% decline.

In addition to the inversion of the US Treasury yield curve we have witnessed M2 Money growth declining -90%, the S&P 50) index down -17.5%, Bitcoin down -64.2% and gold down only -2.3%.

But we now have to worry about Project Cedar, a seemingly innocent project to replace the US Dollar. A new digital currency would allow Washington DC to monitor your purchases and behavior. And perhaps create a Social Credit Score like in China measuring how well you conform to Biden’s notion of a utopian, green society.

And the US yield curve has been inverted for 109 straight days.

Unlike yesterday’s ADP jobs report (only 127k jobs added), the official Federal government report shows 263k jobs added. I like the ADP report, but The Fed pays attention to the BLS numbers. So, …

U.S. employers added 263,000 jobs in November, and the nation’s unemployment rate stayed the same at 3.7 percent, according to data released Friday by the Labor Department. Meanwhile, average hourly pay for workers rose 5.1 percent from a year earlier, to $32.82 from $31.23. But the US headline inflation rate at the last reading was 7.7% YoY that equates to -2.2% REAL Average Hourly Earnings YoY.

Mortgage rates fell to 6.51 yesterday, but expectations of Fed rate hikes (WIRP) and the 10-year Treasury yield are up today. In fact, the 10-year US Treasury yield is up 10 basis points this morning. This will likely translate to higher mortgage rate today.

Inflation is still the humming dragon crushhing the US middle class and at last report stood at 7.7% YoY. Average hourly earnings YoY rose to 5.1% in November, which is good. But inflation takes a huge bite out that number, resulting in -2.2% YoY REAL average hourly earnings.

And the US 10Y-2Y Treasury yield curve has been inverted for 109 straight days.

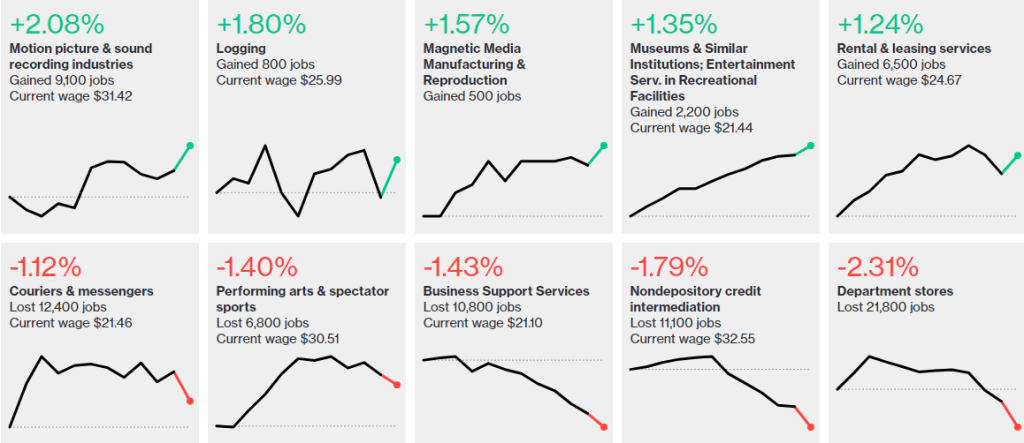

Here is the rest of the jobs report.

The biggest gainer? Motion picture and sound recording industries followed by logging (with rising energy prices, people have to heat their homes somehow).

You must be logged in to post a comment.