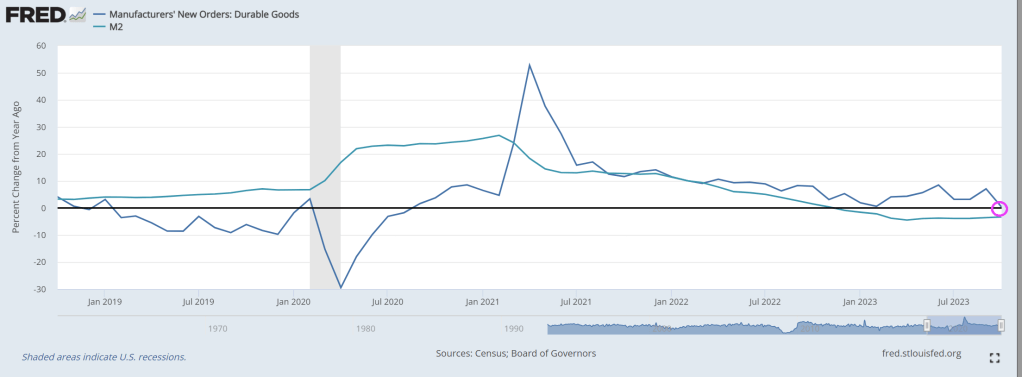

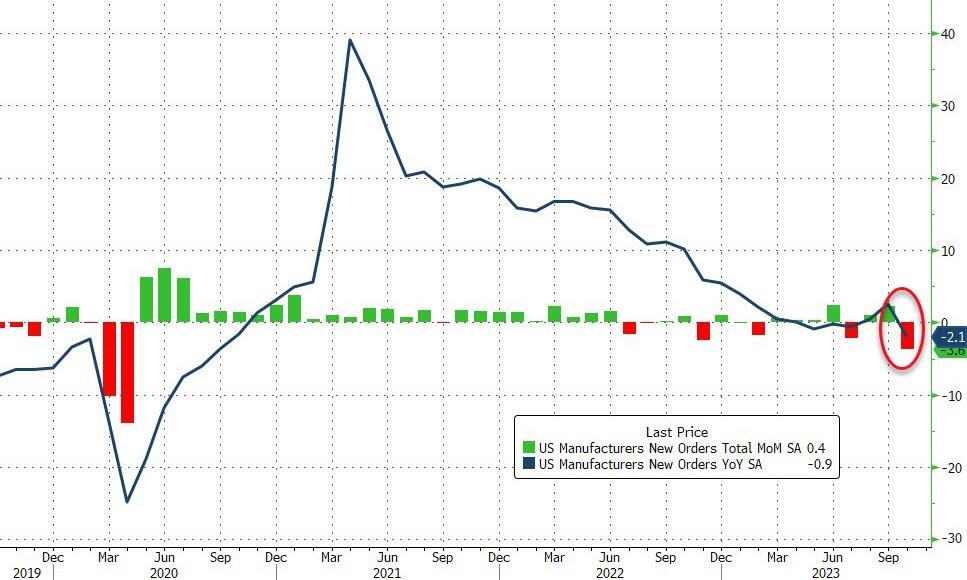

Factory orders tumbled even more than expected, down 3.6% MoM – the biggest drop since the COVID lockdowns (April 2020). September was also revised lower (making October’s decline even worse) from +2.8% MoM to +2.3% MoM…

Source: Bloomberg

The big monthly decline and revisions dragged orders down 2.1% YoY (the biggest drop since Sept 2020).

Core factory orders also dropped (-1.2% Mom), leaving them down 2.2% YoY – the eight month in a row of annual declines…

Source: Bloomberg

The final Durable Goods Orders data for October confirmed the preliminary print plunge down 5.4% MoM.

Finally, we note that it could have been a lot worse as Defense spending shot up 24.7% MoM (as non-defense dropped 15.8% MoM0…

While members of the Biden Administration party at DC nightclubs, the rest of America are drinking Carlo Rossi wine (a favorite of mine in high school!) and eating Spam.

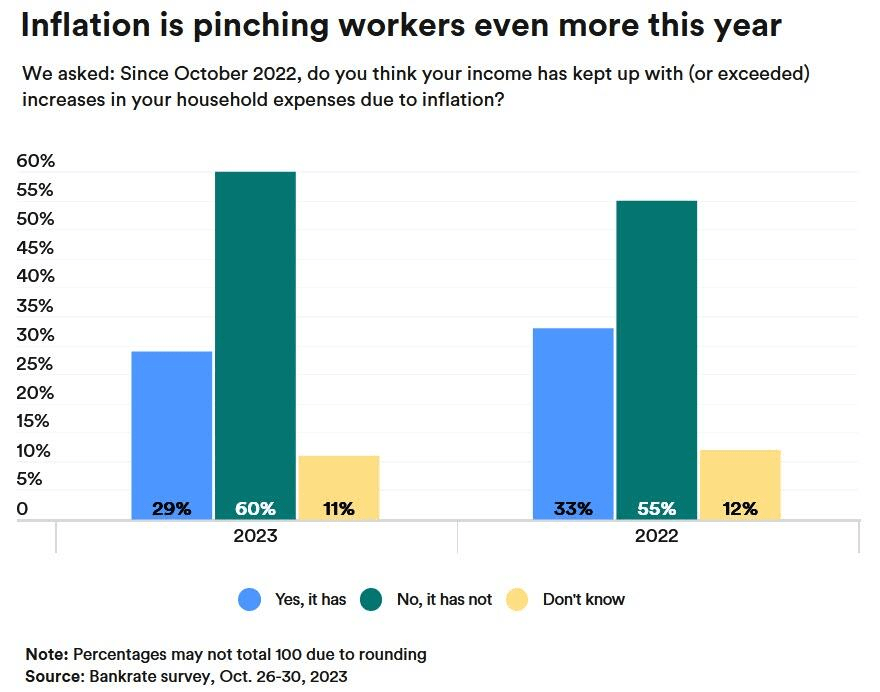

While hourly pay has increased, inflation has outpaced it.

Spending on basic survival needs like food, transportation, housing, and energy has increased, with households in the Mountain West facing the highest rates of inflation.

“We choose January 2021 as the base month because it was the last time inflation was within recent historical norms,” the report reads.

“Due to a combination of higher inflation rates and higher average household spending, inflation is imposing the highest monthly costs on families in the states of Colorado, Utah, and Arizona,” the report adds.

Families in Colorado and Washington, DC, are experiencing inflation costs higher than the national average.

Things are even worse in 2023 regarding inflation ravaging worker’s income. Over 60% of Americans reported that their wages were lagging well behind inflation.

Since January 2021, US purchasing power of the US Dollar is down a whopping -15.4% under Biden.

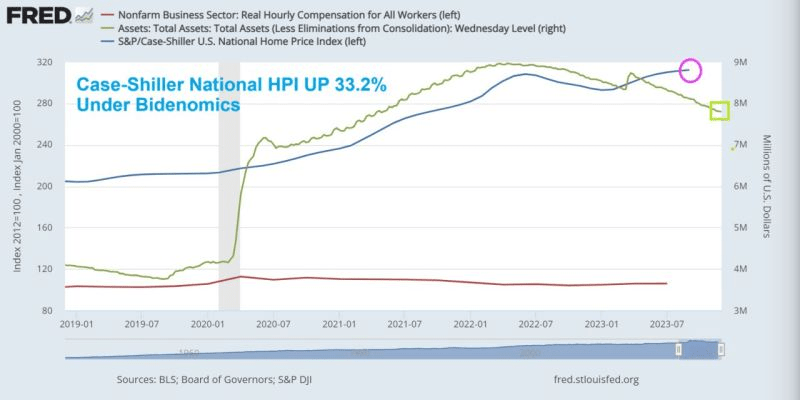

And home prices are up 33.2% under Biden, much of it due to The Feral Reserve money printing to fund Biden’s folicy initiatives. (I saw Biden claim he wrote the Inflation Reduction Act … the one thing we know is House legislation is written by an army of Congressional staffers, not El Presidente).

Home prices up 33.2% and purchasing power of US Dollar down -15.4% under Biden.

And like magic, Biden made $11,400 disappear from household income to pay for Bidenomics.

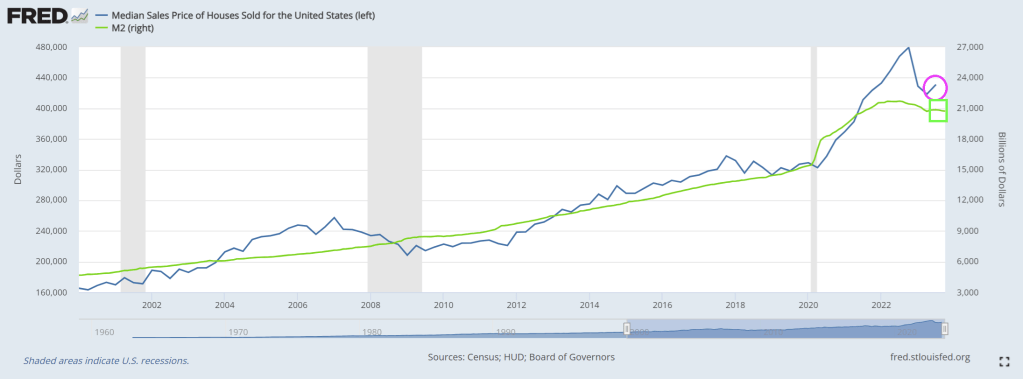

Median home prices are up a whopping 20% under Biden and his signature Bidenomics, growing the economy from the inside-out (?) instead of top-down. Excuse me Joe, Bidenomics is pure top-down Soviet-style economic planning. Markets be damned! The end result? Housing is far more expensive under Biden as are down payments.

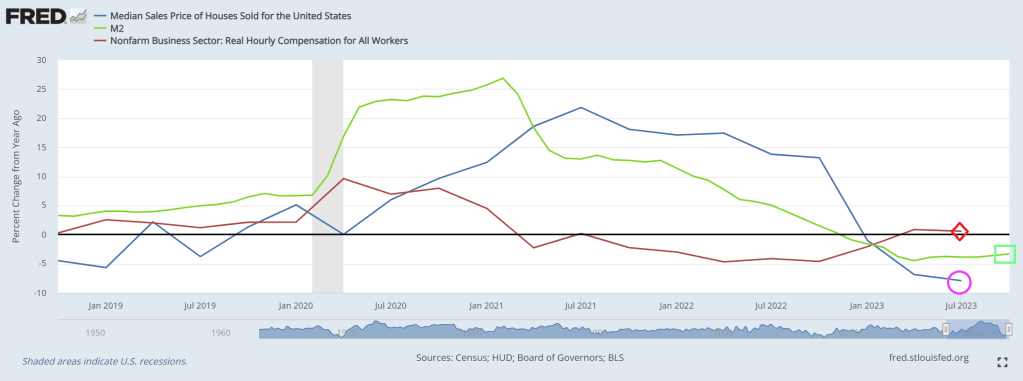

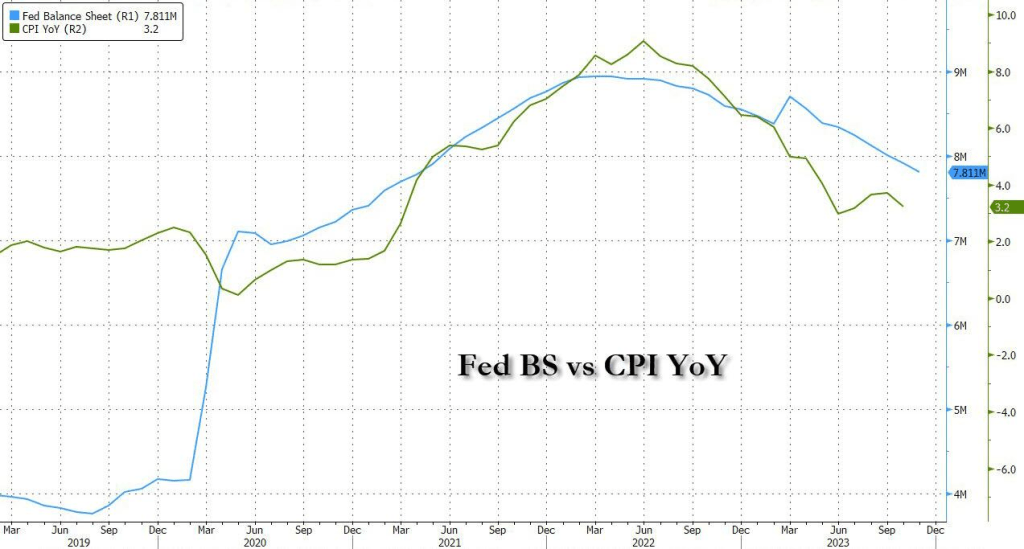

If we look at year-over-year (YoY), we can see the burst of Covid-related spending and M2 Money growth (green line) that surged in 2020/2021. And rising home prices followed shortly thereafter. But as M2 Money growth slows, median home price growth declined into negative growth. The only factor that is positive is real hourly compensation (red line). But that is barely above 0%.

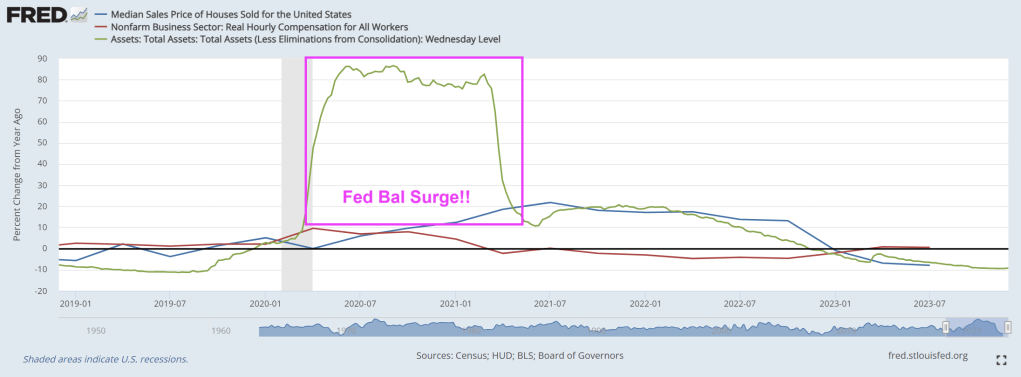

If we look at The Fed’s balance sheet surge (much like a storm surge), you can see the 2020/2021 overreaction to Covid and the various government shutdowns (along with school shutdowns).

The problem is that The Fed is shrinking their balance sheet like Biden shuffles. Maybe The Fed is following Biden’s lead: slow walking, incoherent messaging. And with the Fed storm surge of 2020/2021, Case-Shiller national home price index is up 33.2% under Bidenomics. Good luck with that down payment if you are renting and want to become a homeowner.

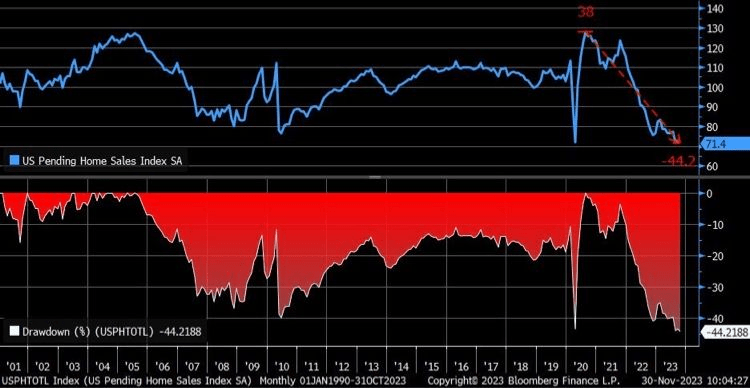

Pending home sales crash is showing why government usually fails to deliver sensible outcomes.

After all, Biden (and his overlord Obama) are truly addicted to gov solutions. Which means they are doomed to fail, as most government policies do.

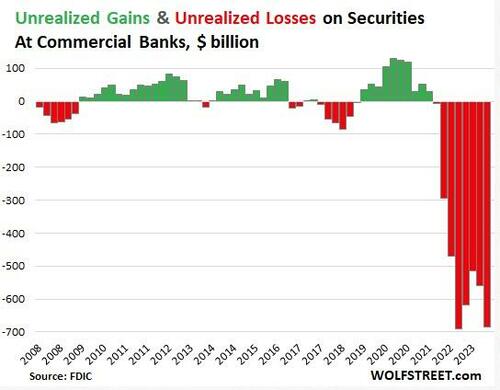

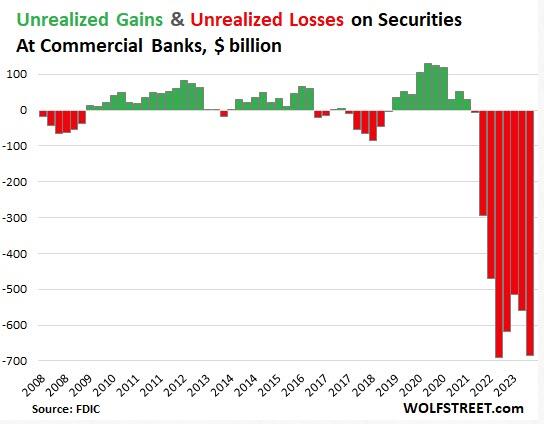

Unrealized losses on securities held by US banks exploded by 22% in the third quarter.

Of course, unrealized losses don’t really matter — until they do.

This is yet more evidence that the financial crisis that kicked off last March continues to bubble under the surface.

Unrealized losses, primarily on US Treasuries and mortgage-backed securities rose by $126 billion in Q3 and now total $684 billion, according to the FDIC’s quarterly bank data release.

Current unrealized losses are only slightly below the record set in the third quarter of 2022. This reflects the fact that the FDIC took over three failed banks earlier his year and ate their unrealized losses when it sold the banks’ assets, thus wiping them from the books.

Unrealized looses on securities are divided between two accounting methods.

Unrealized losses on held-to-maturity (HTM) securities jumped by $81 billion to $391 billion.

Unrealized losses on available-for-sale (AFS) securities jumped by $45 billion to $293 billion.

It’s important to understand these are only paper losses. Ostensibly, the banks will hold these bonds until maturity and then will be paid their face value. If it plays out this way, there won’t be any real losses.

The problem is that these unrealized losses drastically decrease a bank’s liquidity. If it has to sell bonds in order to raise capital, the bank will experience significant losses. This is exactly what took down Silicon Valley Bank last March.

Here’s what happened.

SVB sold a large portion of its bond portfolio at a $1.8 billion loss. At the time, SVB CEO Greg Becke said the bank made the sale “because we expect continued higher interest rates, pressured public and private markets, and elevated cash burn levels from our clients.”

The bank bought the bonds when interest rates were low. As a result, the $21 billion available for sale (AVS) bond portfolio was not yielding above cash burn. Meanwhile, rising interest rates caused the value of the portfolio to fall significantly. The plan was to sell the longer-term, lower-interest-rate bonds and reinvest the money into shorter-duration bonds with a higher yield. Instead, the sale dented the bank’s balance sheet and caused worried depositors to pull funds out of the bank.

WolfStreet explained more generally how these “irrelevant” unrealized losses can suddenly become relevant.

Banks, via a quirk in bank regulations, don’t have to mark these securities to market value, but can carry them at purchase price. The difference between market value and purchase price is the ‘unrealized gain or loss’ that the bank must disclose in its quarterly financial filings, so that we the depositors can see them and get spooked by them and yank our money out, us billionaires and centimillionaires first, on the two fundamental principles of investing: 1, he who panics first, panics best; and 2, after us the deluge.”

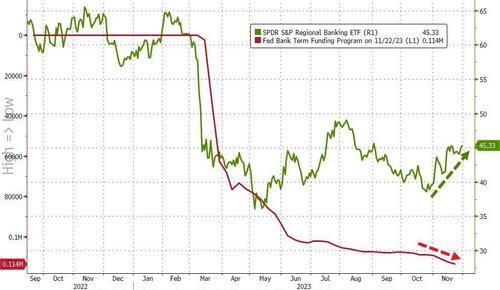

The Federal Reserve set up a bailout program to allow banks to deal with this problem. Instead of selling bonds at a loss, cash-strapped banks can go to the Fed’s Bank Term Funding Program (BTFP) and borrow against them “at par” (face value). This allows banks to use these undervalued assets to raise cash (at least temporarily) without realizing big losses on their balance sheets.

As unrealized losses rise, banks continue to tap into this bailout program more than nine months after the crisis kicked off.

In effect, the Fed managed to paper over the financial crisis with this bailout program.

It basically slapped a bandaid on it. But it has not addressed the underlying issue – the impact of rising interest rates on an economy and financial system addicted to easy money.

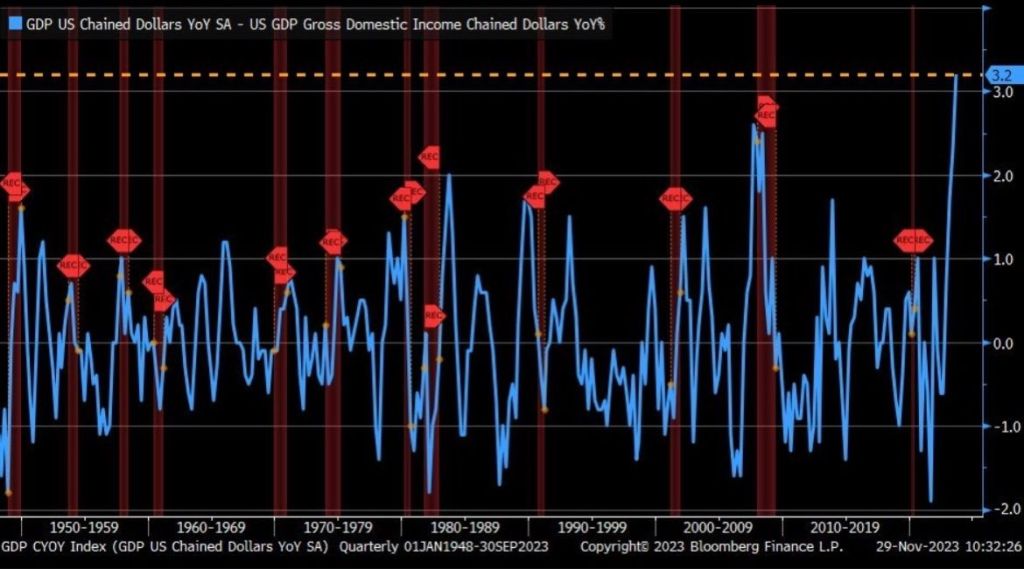

Remember, the US is on the cusp of a REAL recession, thank to Bidenomics.

The spread between real GDP and real Gross Domestic Income (GDI) just hit an all-time high. Even higher than The Great Recession of 2009.

Might as well have AC/DC’s Angus Young as US Treasury Secretary instead of tone-deaf Janet Yellen.

Despite The Fed’s attempts at cooling inflation down to 2%, we are seeing a re-animation of price increases. this time with home prices.

On a year-over-year basis, the Freddie Mac National FMHPI was up 6.0% in October, from up 5.1% YoY in September. The YoY increase peaked at 19.1% in July 2021, and for this cycle, bottomed at up 0.9% in April 2023. …

vv

Austin TX is the big loser, down -11.2% from peak. Followed by Idaho (largely people escaping from Newsomland (California) and speculators. The sixth leading area is Lake Havasu AZ.

As of October, 7 states and D.C. were below their previous peaks, Seasonally Adjusted. The largest seasonally adjusted declines from the recent peak were in Idaho (-4.5%), Utah (-2.7%), D.C. (-2.0%), and Nevada (-1.6%). Nevada, Idaho and Utah are now known as the Mild, Mild, West due to sagging home prices.

For cities (Core-based Statistical Areas, CBSA), here are the 30 cities with the largest declines from the peak, seasonally adjusted. Austin continues to be the worst performing city.

Speaking of inflation and The Fed, Biden claiming he lowered inflation is laughable if it wasn’t so sad. It is all The Fed. And their timidness is shrinking their balance sheet is contributing to persistent inflation.

So, yes, inflation is growing again. This time it is persisent and growing.

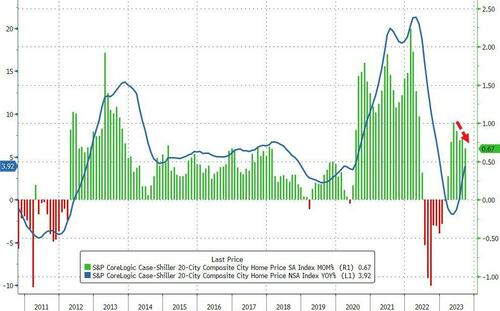

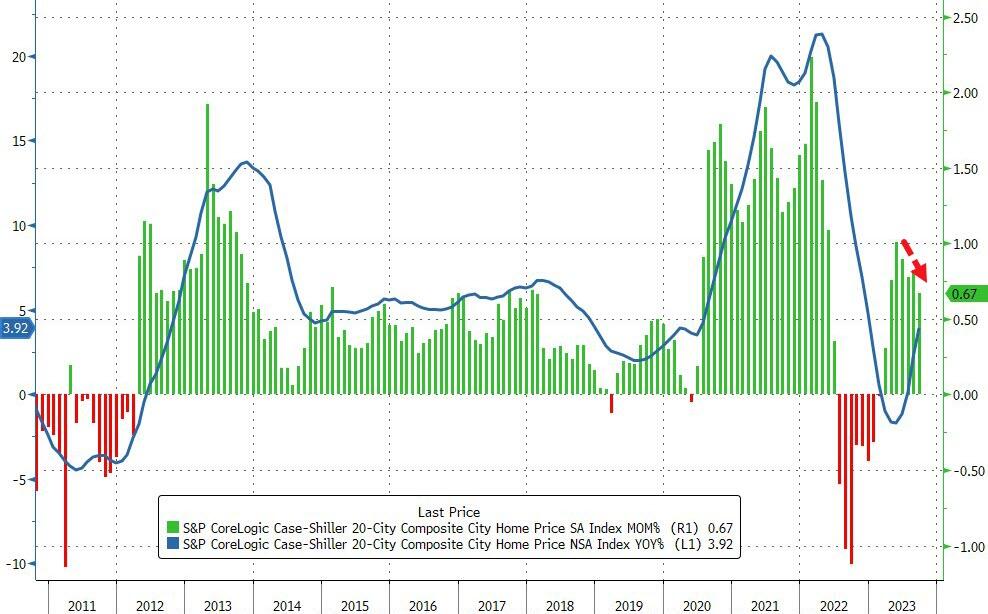

That pushed the YoY rise in prices up 3.92% – the fastest pace since Dec ’22 – but as the chart shows the MoM gains are slowing rapidly.

Source: Bloomberg

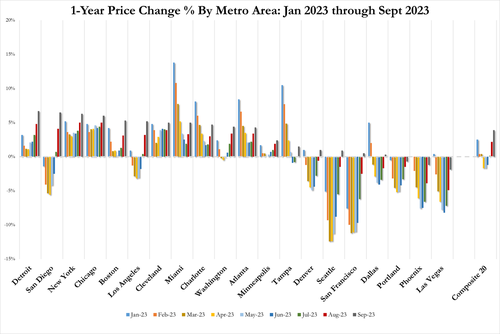

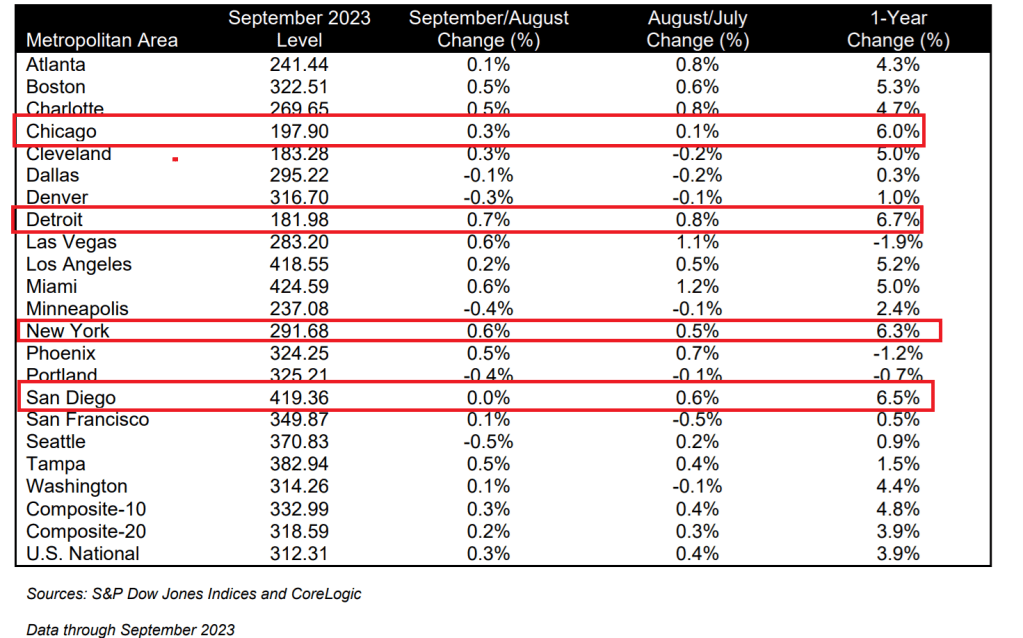

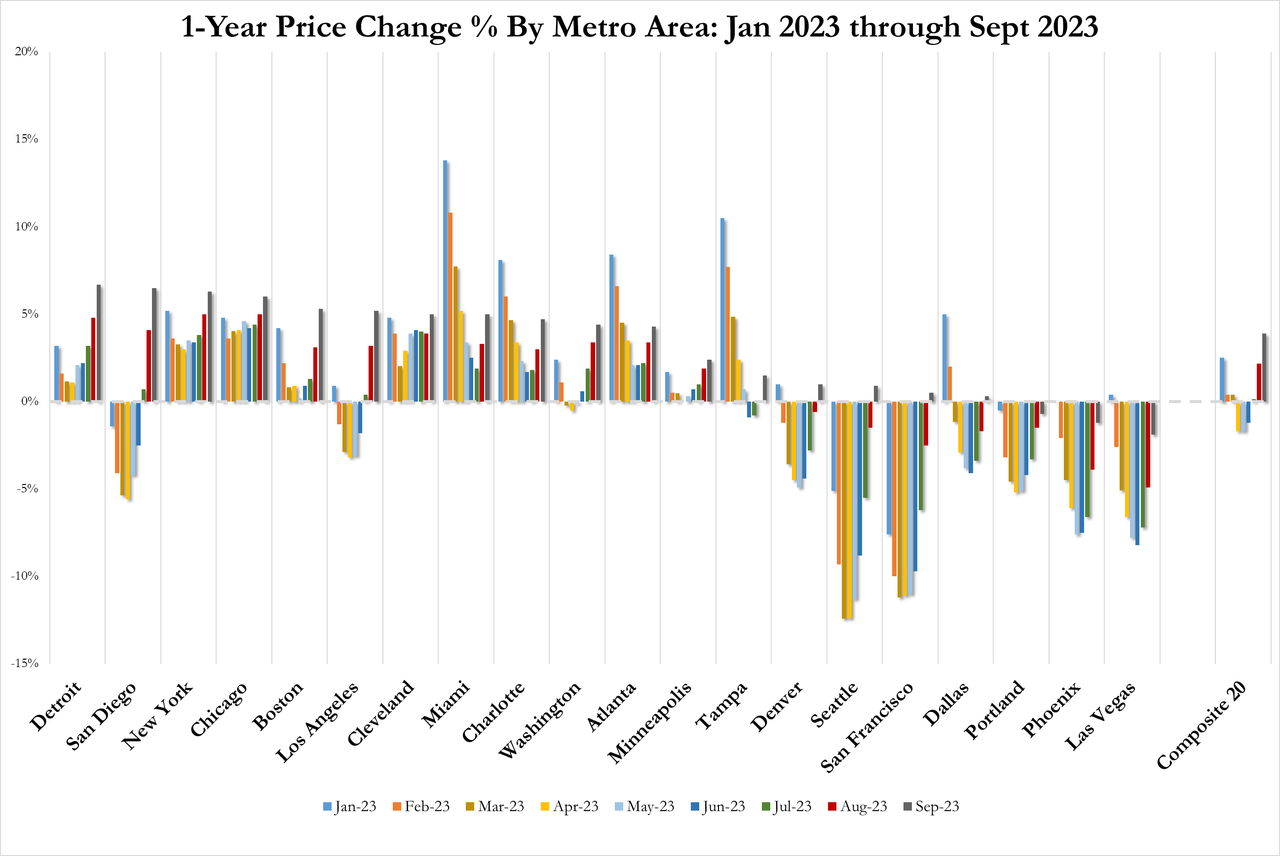

“On a year-over-year basis, the three best-performing metropolitan areas in September were Detroit (+6.7%), San Diego (+6.5%), and New York (+6.3%),” according to Craig J. Lazzara, Managing Director at S&P DJI.

“We’ve commented before on the breadth of the housing market’s strength, which continued to be impressive. On a seasonally adjusted basis, all 20 cities showed price increases in September”

But, judging by the resumption of the rise of mortgage rates since the Case-Shiller data was created, we would expect prices to also resume their decline…

Source: Bloomberg

Inventory is increasing (as homebuilders dump new homes on to the market), but existing home-buyers and -sellers are stuck still (affordability for the former and the mortgage cost gap for the latter), and – despite the market’s hopes – The Fed isn’t cutting rates any time soon (unless the economy utterly collapses). Be careful what you wish for…

Odd that 4 metro areas with 6% or higher home price growth are all cities with larger illegal immigrant migration: Chicago, Detroit, New York and San Diego (all blue cities). This is what is called housing displacement, A surge in immigration leads to rent stock being absorbed and housing prices rising.

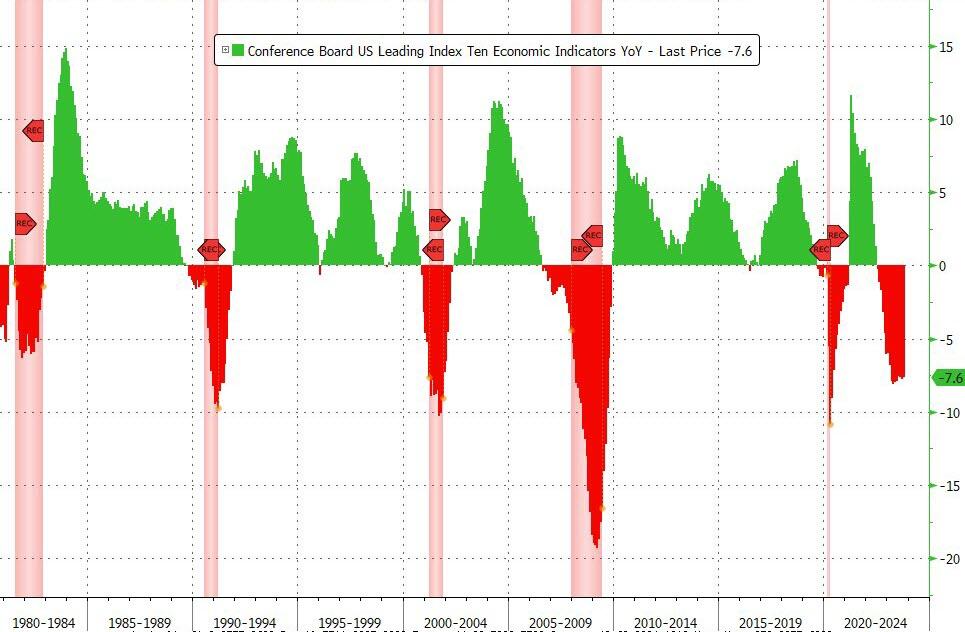

Bidenomics is the economy’s Highway to Hell! Massive, staggering misallocation of scare resources to fund endless wars, green energy fraud, and massive wealth transfers to immigrants while disabled veterans suffer. Now we see that the US leading economic indicators is down -7.6%, definitely smelling like a recession.

On a year-over-year (YoY) basis, the Leading Economic Indicators is down 7.6% (down YoY for 16 straight months) – close to its biggest YoY drop since 2008 (Lehman) outside of the COVID lockdown-enforced collapse.

On a monthly basis (MoM), leading economics indicators are down -0.8%. It has been going down for 16 straight months. Here are the components.

Most of the components are in red and need to be back in black for economic growth.

Treasury Secretary Janet Yellen, a mega pro-China elitist, acknowledges that Bidenomics isn’t popular but she attributes that to people not understanding how good Bidenomics is! It is good for the 1% elitist, donor class. But not for the US middle class.

At least Argentina elected AC/DC guitarist Angus Young as President!

Rubino says, “If the U.S. government is running crisis level deficits, which it is right now, borrowing money and paying interest on it means we are in a financial death spiral…”

“The debt goes up, the interest on the debt goes up and that raises the debt even further, and you just spiral out of control.

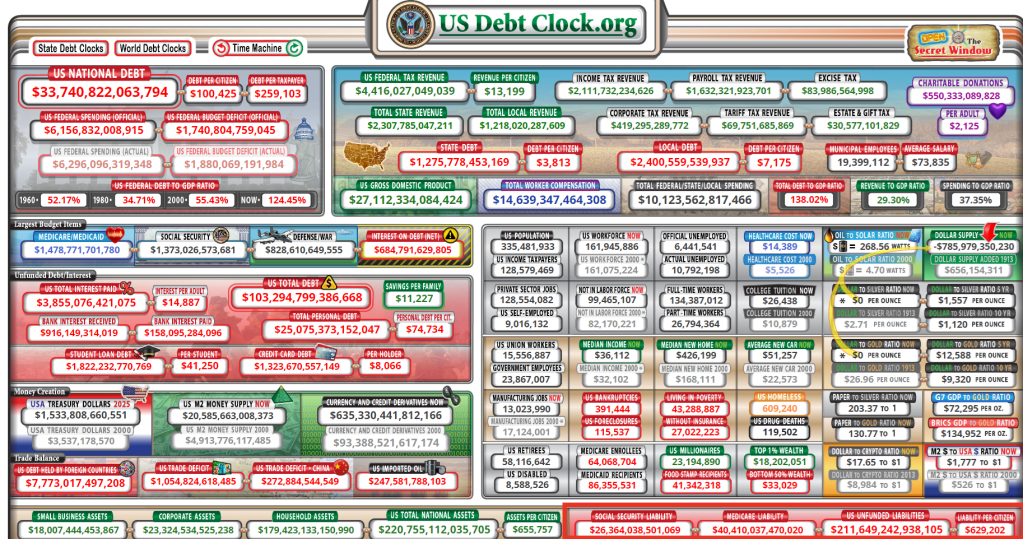

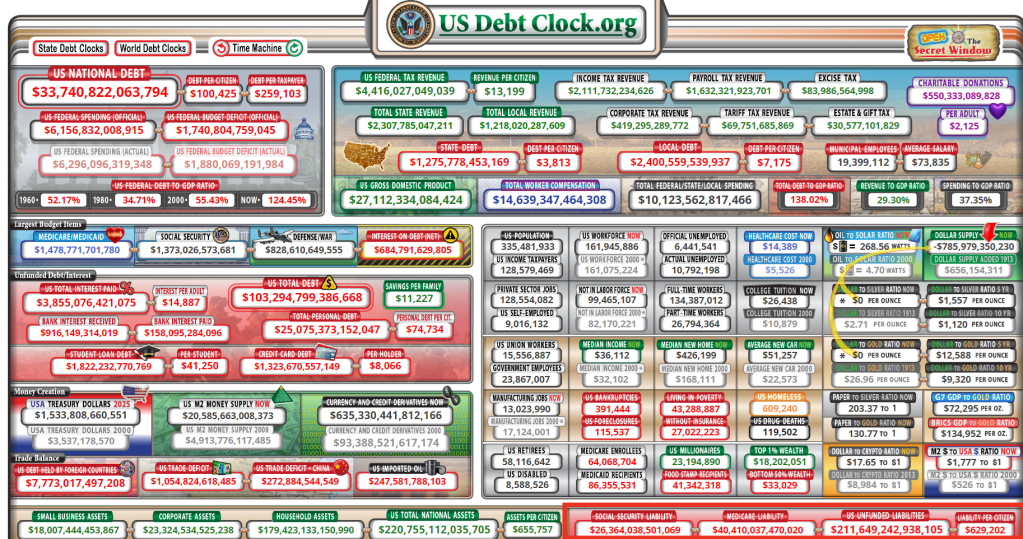

We are there right now. The official U.S. debt is $33.5 trillion. It’s growing by $1.7 trillion a year, and $1 trillion of that is interest costs.

Interest costs are rising as the overall debt goes up. Then throw in this incredibly reckless military spending in the guise of foreign aid, and you get a society that has completely lost control.

That’s where we are now.

We are in the blowoff stage of a 70-year credit super-cycle.

Those things do not end with a whimper, and they certainly do not end with a soft landing. They end with a bang, and the bang is going to be centered on the currency.

People are going to look at this and say, ‘Do I really want to hold the currency or bonds of a country that is destroying its finances at this trajectory and this scale?’ The answer will be ‘No.’

At that point, it is game over for a deeply indebted economy. We are headed that way fast, and these wars are taking us that way even faster.”

If the Fed keeps raising interest rates, the economy tanks, but you protect the dollar. If you cut interest rates, you spike inflation even more, and the U.S. dollar tanks.

Rubino says in the end, we get a “massive reset,” and the everything bubble explodes.

Rubino says the dollar is going to decline and, at some point, it starts to go into freefall in terms of buying power. Rubino explains,

“If a currency starts to decline in a disorderly way, then you have a massive financial crisis on your hands.

That is definitely where Japan is right now. The U.S. is headed that way fast.

So, once we reach that point, there is no fix.

Then it is only a matter of time that everybody realizes that there is no fix, and they just bail on the whole experiment, and that’s where we are headed.”

Rubino talks about plunging home prices, more trouble coming in the commercial real estate market and why you need gold and silver as core assets during a currency reset.

Riots, already happening in American cities (not to mention looting in New York City, Chicago, San Francisco and Los Angeles), will accelerate if Congress attempts to curtail entitlements (now at $211.65 TRILLION).

The S&P 500 real estate sector is now just 5% of the entire S&P 500.

Even at the 2008 low, in the worst real estate crisis of all time, this percentage barely dropped below 6%. Meanwhile, demand for commercial real estate (CRE) loans is now at 2008 levels.

Office building prices are down ~30% over the last year and apartments are down ~15%.

Also, Delinquent commercial real estate loans at US banks have hit their highest level in a decade.

The strength of the housing market is masking the weakness of CRE.

Speaking of the housing market, the US is overly dependent on the lopsided 30-year fixed-rate mortgage. Where under inflation and rising rate, the lender (investor) loses. If inflation cools and rates fall, the borrower refinances.

But these consumer benefits to the 30-year mortgage have costs. It is costly to provide a fixed nominal interest rate for as long as 30 years. And the prepayment option creates significant costs. If rates rise, the lender has a below market rate asset on its books. If rates fall, the lender again loses as the mortgage is replaced by another with a lower interest rate. To compensate for this risk, lenders incorporate a premium in mortgage rates that all borrowers pay regardless of whether they benefit from refinance. Exercise of the prepayment option in the contract also has significant transactions costs for the borrower and imposes additional operating costs on the mortgage industry.

Another major reason for the FRM’s dominance is government support and regulatory favoritism. The FRM is subsidized through the securitization activities of Fannie Mae, Freddie Mac and Ginnie Mae.

Their securities benefit from a government guarantee that lowers the relative cost of the instrument, which is their core product. These guarantees have a significant cost as the government backing of Fannie Mae and Freddie Mac has exposed taxpayers to large losses. Are the FRM’s benefits worth its costs? Would the FRM disappear if Fannie and Freddie stopped financing it? Are there mortgage alternatives that balance the needs of consumers and investors without exposing the taxpayer to inordinate risk?

The instrument’s supporters point out that it is easier for investors than consumers to manage interest-rate risk. It is true that lenders and investors have more tools at their disposal to manage interest-rate risk. But managing prepayment risk is costly and difficult and many institutions have suffered significant losses as a result (e.g., savings and loans in the 1980s; hedge funds and mortgage companies in the 1990s and 2000s).

Furthermore, borrowers rarely stay in the same home or keep the same mortgage for 15 to 30 years, so one can reasonably ask why rates should be fixed for such long periods (increasing the loan’s cost and risk). Also, the taxpayer ultimately bears a significant portion of the risk through support of Fannie Mae and Freddie Mac.

One of the lingering questions about government loan modification programs is why borrowers are refinanced into longer-term FRMs rather than less expensive ARMs, such as a 5/1 ARM.

ARMs allow protection for lenders (investors) from inflation and interest rate increases. Consider this another entitlement that elected officials give away and refuse to cut. After all, unfunded entitlements are already at $211.65 TRILLION.

But typically we get scare tactics about ARMs (or VRMs), like this one.

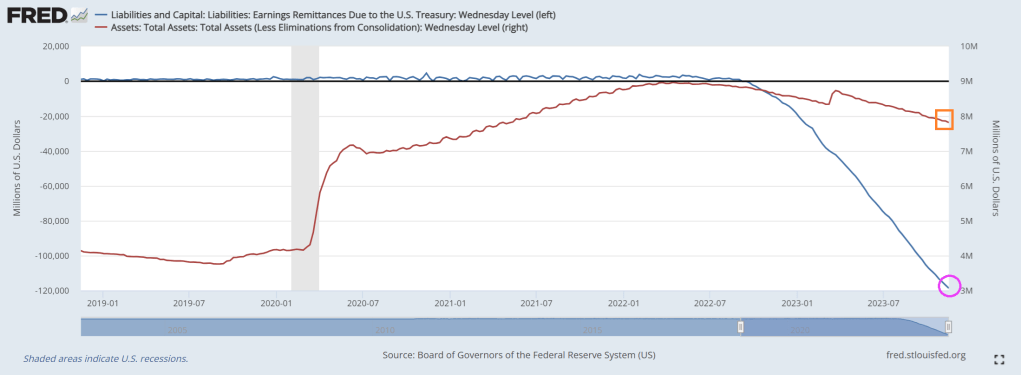

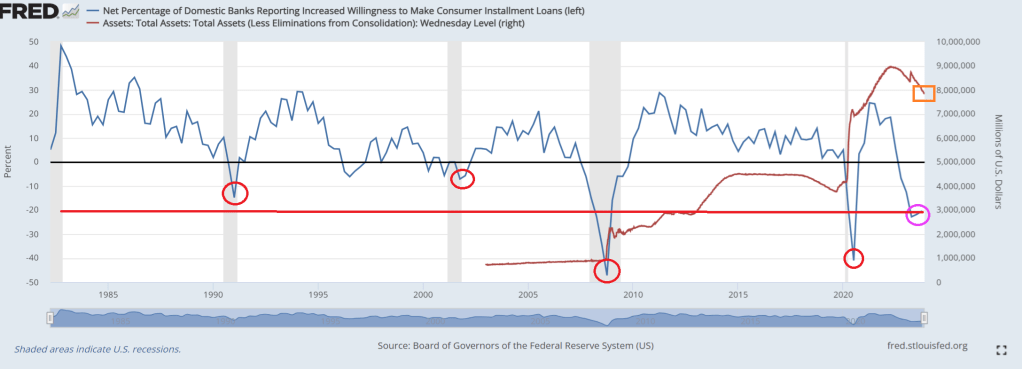

Biden’s terrible economic policies and horrid fiscal managment has put stress on The Federal Reserve. The Federal Reserve paid an estimated $76 billion to the Treasury in 2022 while banks’ willingness to lend has plummeted.

One of the key ways central banks absorb liquidity back out of the market is through reverse repo. These are short-term transactions where the Fed sells securities to banks and agrees to buy back at a higher price the next day.

This means banks are being paid to park cash with the Fed instead of injecting it into the economy through loans and fanning the fires of inflation.

That alone is costing the Fed $200M every single day.

In addition, the Fed is spending another $500M in daily interest payments on its reserve policy, i.e. balances that banks are holding in their reserve accounts at the Fed.

Banks’ willingness to lend has plummeted making credit availability increasingly tighter. Current levels have typically ended in recessions.This time is NOT different.

And on the energy side of the market, Biden Invokes ‘Wartime Powers’ to Attack Gas-Powered Furnaces. Of all the stupid things Biden has done, invoking wartime powers to make households use inefficent electric heat pumps instead of gas furnaces in stupid of two levels. First, invoking wartime powers for things unrelated to national defense is reckless and capricious. Second, electric heat pumps in the colder areas of the country is stupid as well. Electric heat pumps are inefficient, unless the goal of Biden and his Idiocracy is to “cull the herd” or kill off people during winter months (I had an electric heat pump in a condo I owned and it was terrible in winter months).

Yes, the Biden Administration and The Fed are economic mutilators!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.