Official estimates from the Congressional Budget Office (CBO) show that, since January 2021, legislation signed by President Biden has set in motion a record $3.37 trillion in new spending. And for all that spending, we get a pathetic 1.1% QoQ growth rate?

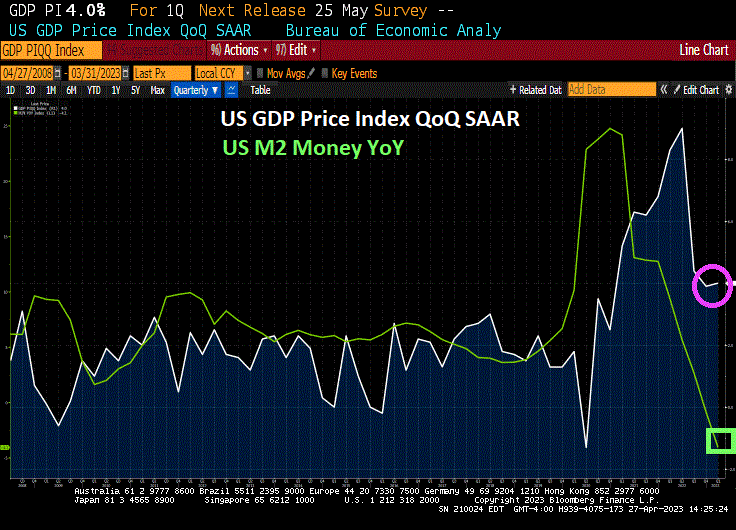

Inflation continues to be 4% QoQ despite M2 Money growth collapsing.

Gross private domestic investment crashed by -12.5% QoQ.

This is Biden’s idea of a strong economy? His lame campaign slogan is “Let’s finish the job!” Please don’t Joe!

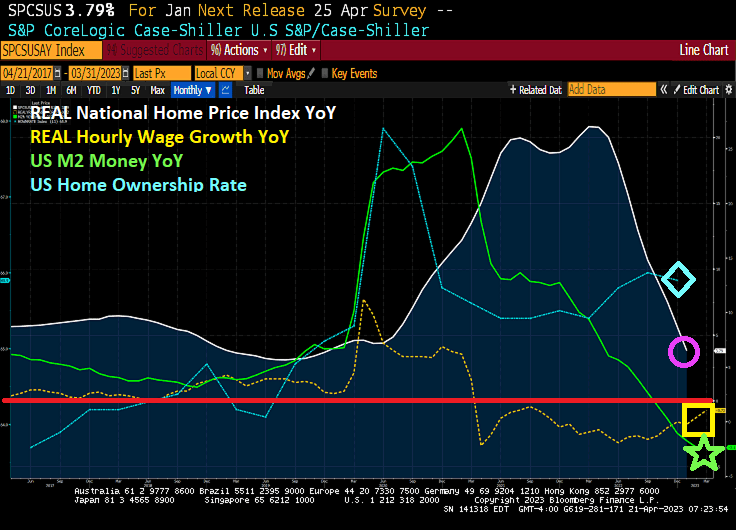

It has been a tough road for the US economy since Covid and Biden’s Reign of Error. For the first time since July 2020 under President Trump, we have finally seen average hourly earnings growth YoY exceed average home price growth YoY.

In REAL terms (after substracting out headline inflation), we see that US housing market is still plagued by 24 straight months of negative wage growth with REAL wage growth still being lower than REAL home price growth.

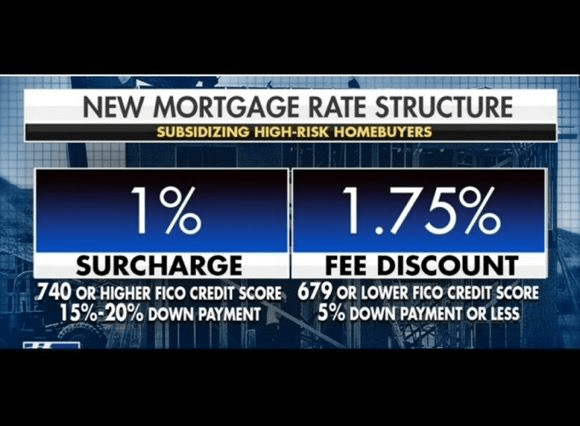

Then we have Biden’s Marxist mortgage model, making those who who saved and showed care in managing their credit score given money to those who didn’t save and are terrible at financial management. Just like taxpayers trusting DC bureaucrats to carefully spend their money.

This is life under Joe Biden. Record sovereign risk, record high debt, near 40-year highs in inflation, a hot war in Ukraine with Russia, failure of DOJ/FBI to do anything about the content of Hunter Biden’s laptop, repression of free speech, soaring crime, out of control borders. Should I keep going? It is a disastrous mess created by Obama/Biden and their creepy allies.

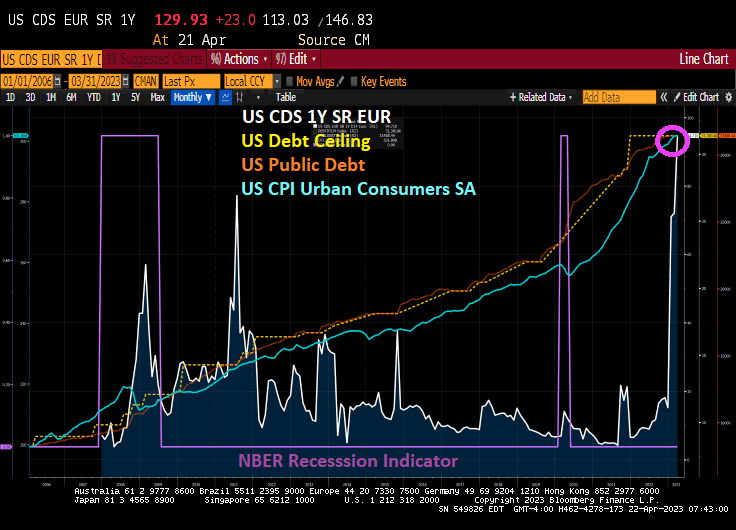

US sovereign risk just hit 130, the highest since CDS was recorded. This alligns with Biden/Congress massive borrow and spend policies where Federal debt has soared to it highest level in history. Inflation, while cooling, remains high.

On the housing front, REAL national home price growth is negative which makes sense since REAL average hourly wage growth has been negative for the last 24 months.

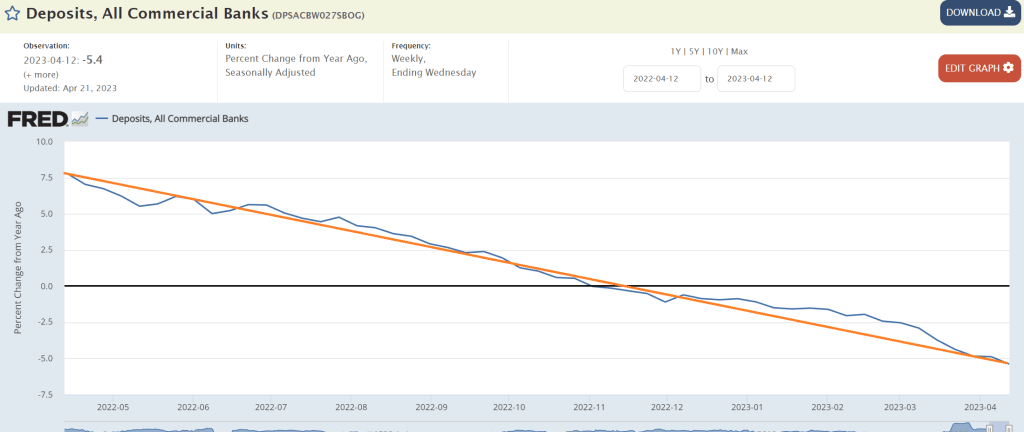

And just over the past year, commericial bank deposits are falling like a paralyzed falcon.

Biden and Obama’s chief hack in the White House, Susan Rice, are burning down the house.

It’s only mid April and mortgage demand should be approaching it’s yearly high. But under Biden and The Fed, mortgage demand seems to have peaked earlier than normal. It’s already late in mortgage cycle.

Mortgage applications decreased 8.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 14, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 8.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 8 percent compared with the previous week. The Refinance Index decreased 6 percent from the previous week and was 56 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 10 percent from one week earlier. The unadjusted Purchase Index decreased 9 percent compared with the previous week and was 36 percent lower than the same week one year ago.

The US is beginning to be out of time for agreeing on a debt limit increase. But you don’t need a fortune teller to tell you that Biden and McCarthy will eventually agree to increase the US debt limit because everyone in Washington DC love to borrow and spend money. Regardless, we are seeing the 1-year US Credit Default Swap (SR, EUR) rise above 100, higher than during the 2008/2009 financial crisis.

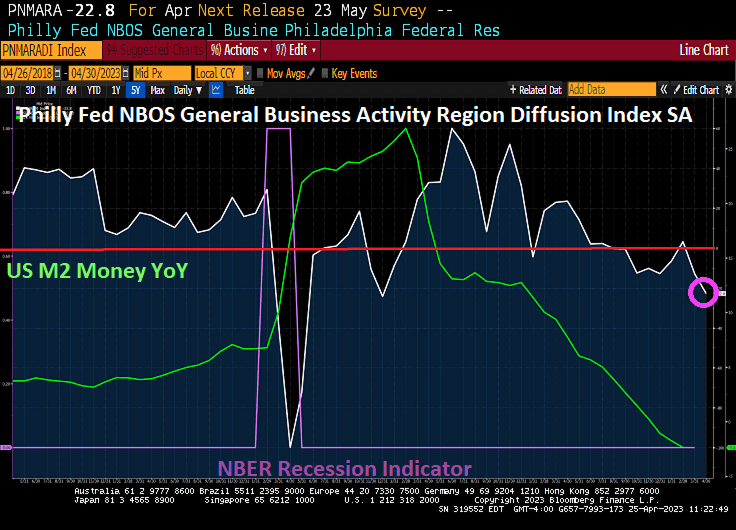

This is occuring as the US Treasury 10Y-2Y yield curve remains inverted and M2 Money growth has crashed.

But never fear! The Evil Hobbitt (aka, Janet Yellen) is still US Treasury Secretary. You know, the one who left interest rates too low for too long (TLFTL) as Federal Reserve Chair, then tightened as soon as Donald Trump was elected President.

Here is a chart of US office vacancies nationally (yellow), New York (white), San Franciso (green) and Los Angeles (orange). Note the rapid decline in office vacancies just prior to the financial crisis (often mislabeled as the subprime mortgage crisis). Then look at office vacancies after The Fed’s massive monetary experiment of setting rates to near zero and buying a ton of Treasuries, Agency MBS. etc. While San Francisco returned to pre-financial crisis levels of office vacancy, in general the office market never fully recovered.

And then “the slammer” struck: the COVID economic shutdowns. After 2020 shutdowns, office vacancy rates rose dramatically. Two complicating factors: 1) the US moved to working at home rather than commuting to an office and largely remains that way. 2) crime is going bonkers in American cities, particularly New York, Los Angeles and San Francisco (don’t worry, I haven’t forgotten about other gang nests like Chicago and Detroit). I saw that California’s woke governor Gavin “Nancy Pelosi’s nephew” Newsom said the word “gang” then apologized and replaced it with “organized groups.” No wonder Newsom can’t fix anything, but he is running for President of the US! (insert Edvard Munch’s “The Scream” painting here,)

The Fed responded to the financial crisis by lower rates to 25 basis points and printing a boat load of money. Unfortunately, office vacancies rose to a peak in October 2010 then began falling again. Only to start rising again after Trump took office in 2017. Alas, Covid struck in 2020, The Fed and Federal government panicked. States and local governments (not to mention teacher’s unions) shut down economies and schools. Office vacancies are now higher than at peak of the Covid shutdowns!!!

I feel like I am watching the Star Trek original series episode “The Doomsday Machine” as former Fed Chair and current US Treasury Secretary effectively just guaranteed ALL US bank deposits. Aka, a massive bank bailout. The episode was about a robot space vehicle that destroy planets … and anything in its path. And if it changed course to destroy something, it gradually returned to its original destructive path. Like The Federal Reseve.

But after a few days of declining Treasury yields because of the mess created by Bernanke/Yellen’s too low for too long policies, and the Biden/Congress insane spending, the US Treasury 2-year yield is up 16.1 basis points.

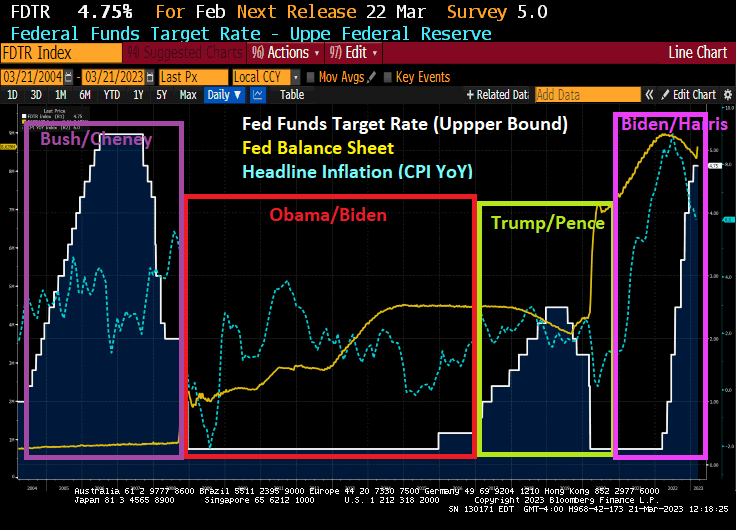

Whether it was politcally motivated to protect Obama/Biden or Obama/Biden’s economic recovery was terrible, The Fed only raised their target rate once before Trump’s election. And then Yellen raised rates like crazy. Only to hand her mess off to Powell who had to drop rates like a rock and massively expand the balance sheet … again … to fight Covid.

First, The Fed’s discount window soared to its highest level since … you guessed it … the previous financial crisis of 2008/2009.

Second, the 10-year Treasury yield declined -16 basis points this morning as investors flee to safety.

Bankrate’s 3-year mortgage rate rose to 7%, but with today’s decline in the 10-year Treasury yield we should see mortgage rates declining.

Yes, much of the blame belongs to The Fed’s leadership (Bernanke, Yellen, Powell) for leaving rates too low for too long, then suddenly try to lower inflation by raising rates. Now we have The Fed’s balance sheet INCREASING again as the use of The Fed’s discount window soars to highest level since Lehman Bros fiasco.

Apparently, the NEO financial crisis (not the subprime, but The Fed’s “too low for too long” crisis) is still with us.

Credit Suisse Group AG’s top shareholder, whose stake has lost more than one-third of its value in three months, ruled out investing any more in the troubled Swiss bank as a bigger holding would bring additional regulatory hurdles.

“The answer is absolutely not, for many reasons outside the simplest reason, which is regulatory and statutory,” Saudi National Bank Chairman Ammar Al Khudairy said in an interview with Bloomberg TV on Wednesday. That was in response to a question on whether the bank was open to further injections if there was another call for additional liquidity.

Credit Suisse says it has identified material weaknesses in its internal control over financial reporting as of December 31, 2022 and 2021, according to the annual report.

The material weaknesses relate to the failure to design and maintain an effective risk assessment to identify and analyze the risk of material misstatements in its financial statements and the failure to design and maintain effective monitoring activities relating to: – Providing sufficient management oversight over the internal control evaluation process to support the Group’s internal control objectives – Involving appropriate and sufficient management resources to support the risk assessment and monitoring objectives Assessing and communicating the severity of deficiencies in a timely manner to those parties responsible for taking corrective action

And it could simply be that Credit Suisse was caught in the Central Bank “Bear Trap” where banks get clobbered as interest rates rise.

Credit Suisse’s CDS (credit default swap) is soaring!

And on the “it ain’t over till its over” news from Credit Suisse, the US Treasury 2-year yield plunged -40.4 basis points.

And the US Treasury 10-year yield plunged -24.8 basis points.

The official logo of the Federal Reserve should be Munch’s The Scream.

You must be logged in to post a comment.