Bidenomics, aka the Federal government takeover of the US economy with Soviet-style economic central planning, is highly dependent on loose Federal Reserve monetary policy (Janet Yellen and Powell’s wild overreaction to the massively inappropriate Covid shutdowns),

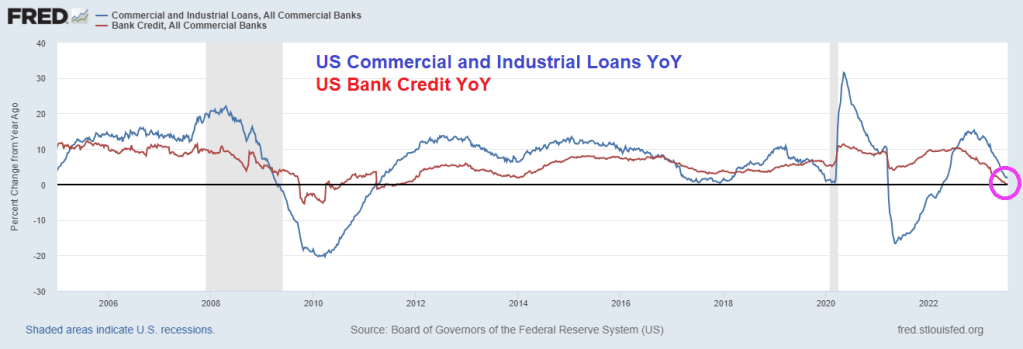

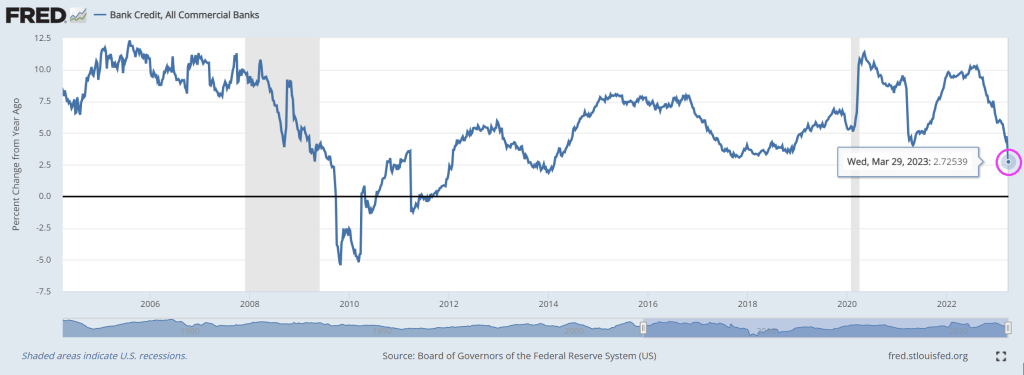

So, how is Bidenomics working out? On the bank lending front, commercial and industrial (C&I) lending growth is crashing along with bank credit growth YoY.

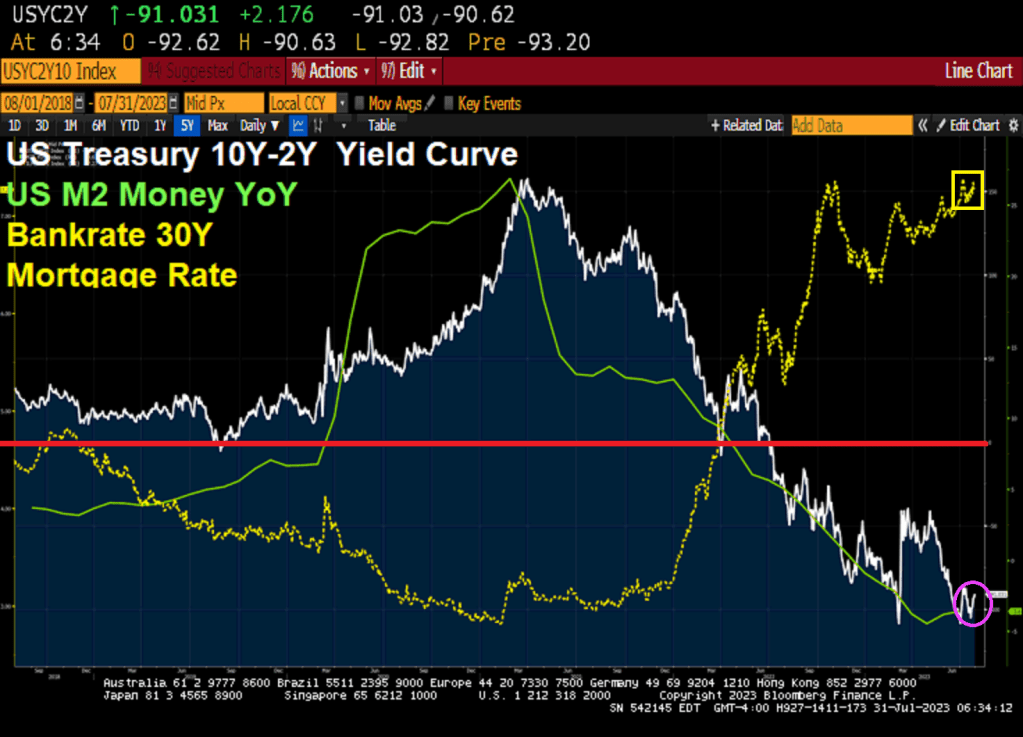

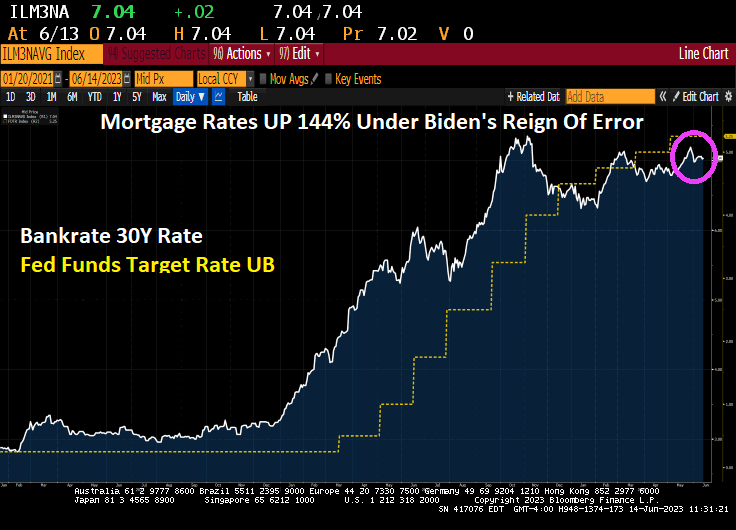

The US Treasury 10Y-2Y yield curve remains deeply inverted at -91.031 basis points and M2 Money growth has crashed. The 30 year mortgage rate is hovering around 7.27%.

Biden’s “reign of error” is horrific. The inflation caused by Biden’s policies, The Federal Reserve and insane Federal spending has caused mortgage rates to soar 144% since Biden took office.

While The Fed is likely to pause today, but Fed Funds are pricing in a July rate hike.

It is not a surprise that the ill-advised COVID economic shutdowns would harm small businesses that large corporations.

Yes, The Fed’s M2 Money printing press went wild with COVID emergency refief. And so did the discrepancy between the top 1% and the bottom 50% in terms of “Share of Total Net Worth Held.” The top 1% is in blue and the bottom 50% is in red. M2 Money is in green.

Compared to pre-COVID, the top 1% increased their share of total net worth from 29.7% to 31.9%, an increase of 7.4% since January 2020. The bottom 50% fell from 30% to 28.5%, a -5% decline. An elitist wonderland!

And The Biden family keeps raking in the money far about Joe’s salary.

And I assume Fed Chair Jerome Powell and Treasury Secretary Janet Yellen also made fortunes from COVID relief.

James Carter (no, not Mr. Peanut, the smart one at America First Policy Institute’s Center for American Prosperity) had a nice op-ed on American Thinker entitled “The Biden Administration’s Budget Hypocrisy.”

The Biden administration’s claims of deficit reduction come in stark contrast to the president and his team, having added $4.8 trillion to the deficit through 2031.

You might call anyone uttering such claims a hypocrite. As Adlai Stevenson, the grandfather of the future Illinois governor and two-time presidential candidate of the same name, reportedly quipped: “A hypocrite is the kind of politician who would cut down a redwood tree, then mount the stump and make a speech for conservation.” Sounds about right.

Why does this matter? It matters because President Joe Biden fancies himself a champion of deficit reduction. As he bragged in a “60 Minutes” interview last month, “By the way, we’ve also … reduced the deficit by $350 billion my first year. This year, it’s going to be over $1.5 trillion, reduced the debt.”

But the president’s attempts to redefine his reckless spending as deficit reduction don’t end there. According to The Washington Post, “Just in the week before the 60 Minutes interview, the president mentioned having reduced the budget deficit by $350 billion six times, sometimes saying he wants to counter accusations that he’s running up the federal tab.” (emphasis added)

What the president fails to mention, however, is that this near-term deficit reduction has nothing to do with him or his administration. Instead, it’s the result of emergency COVID-19 spending that is now ending as planned.

Maya MacGuineas, president of the nonpartisan Committee for a Responsible Federal Budget, points out what the Biden administration is loath to admit:

“The White House has been trying to paint President Biden as the champion of prudent economic stewardship. Biden’s ‘record on fiscal responsibility is second to none,’ it asserts. As temporary covid measures end — and record-high deficits predictably decline — the administration is congratulating itself for that supposed achievement.

But the administration’s record is, sadly, the opposite of what it argues. Since entering office, the president has approved policies adding $4.8 trillion to the deficit over the next decade. This is an extraordinary sum, which makes it all the more astonishing that the administration would try to pull off this claim.”

According to the Office of Management and Budget, even if the 117th Congress had enacted the Biden administration’s fiscal year 2023 budget in its entirety, net interest costs would more than triple from $352 billion in 2021 to $1.1 trillion by 2032. Is a tripling of future net interest costs something typically associated with an administration committed to tackling the federal budget deficit? No.

President Biden’s rhetoric aside, his mid-session budget review forecasts endless $1 trillion-plus annual deficits totaling more than $14 trillion over the coming decade. Even adjusted for inflation, these deficits would be among the largest ever generated by the federal government. Is that “fiscally responsible?” No.

President Biden is not serious about reducing the deficit. He claims progress on the deficit but obscures the facts that every American should know.

Not only does President Biden fail to try to balance the budget, but he actively pursues policies that he must know will balloon federal spending and deficits.

No, but Biden and Congress are serious about bankrupting the US Treasury and moving to a Socialist model.

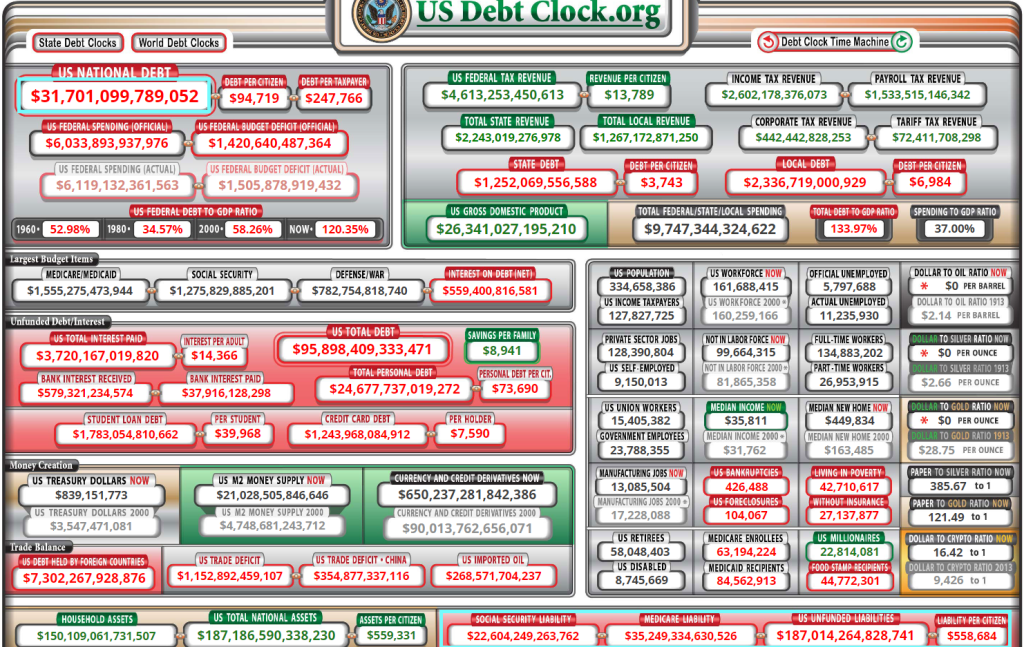

And what even James Carter doesn’t mention is the staggering levels of UNFUNDED LIABILITIES of $187 TRILLION. The question for Biden is …. how are deficits and the massive debt going to play out when we are on the hook for $187 TRILLION?

I am sure that Bernie Sanders, Elizabeth Warren and The Squad will suggest much higher taxes to cover it. And remember, Biden was the idiot that helped taxed Social Security for seniors. And he has also worked towards cutting Social Security and Medicare in the past.

The only out is 1) default on the US debt which would be catestophic and 2) renegging on the massive unfunded liability load. Remember, France is rioting over raising their retirement age by 2 years. Let’s see if Americans riot over inevitable cuts to Social Security, Medicare and Medicaid.

Cut mandatory spending without riots? Please.

The theme song of Biden’s insane, economy destroying, inflation creating budget should be “Keep on printing!”

Yes, this is Government Gone Wild! But no pics or videos of ancient Congress members like Warren or President Biden, please.

Inflation started with Biden’s misguided war on US energy, then Biden/Congress helped inflation with an epic spending splurge. The Federal Reserve counterattacked with Fed rate hikes.

Over the past year, The Fed Funds Effective rate has risen and US bank credit has crashed to 2.73% year-over-year.

Do I detect a trend?

Since 2005, the crash in US bank credit is looking like 2008/2009 all over again.

Whether Biden is Cap’n Crunch or Jerome Powell or Janet Yellen, they are all crunching the US economy.

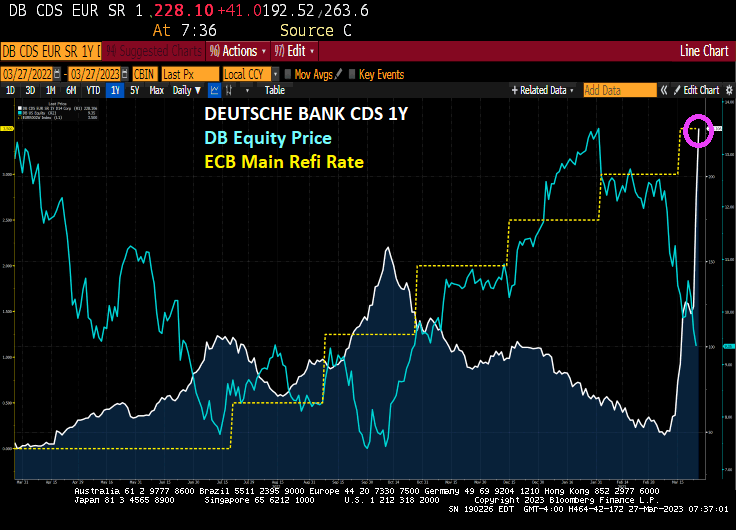

Are central banks like The Federal Reserve and European Central Bank ({ECB) sinking the banks?

Deutsche Bank, Germany’s largest bank (eerily like Germany’s World War II battleship The Bismarck) is seeing a blow out in its 1-year credit default swaps (CDS) as the ECB cranks up it main refinancing rate to fight inflation.

And then we have Deutsche’s Banks gross notional derivatives exposure (Euro 55.6 TRILLLION) dwarfing German GDP (Euro 2.7 Trillion). By a factor of greater than 20! Now, THAT’S a lot of derivatives exposure.

On the bond front (the NEW eastern front), we see the US Treasury 2-year yield rising 17.1 basis points. But European sovereign yields are up double digits as well (except for Italy).

The Federal Reserve never died. In fact, The Fed is growing its balance sheet again. Why? A slowing economy and weakness in the banking sector (thanks to inflation and the Fed trying to get inflation back to 2%.

And the banking fiasco keeps rolling, particularly in Europe where Credit Suisse has been in the news for failing and now my former employer, Deutsche Bank (aka, The Teutonic Titanic).

Deutsche Bank AG became the latest focus of the banking turmoil in Europe as ongoing concern about the industry sent its shares slumping the most in three years and the cost of insuring against default rising.

The bank, which has staged a recovery in recent years after a series of crises, said Friday it will redeem a tier 2 subordinated bond early. Such moves are usually intended to give investors confidence in the strength of the balance sheet, though the share price reaction suggests the message isn’t getting through.

“It is a clear case of the market selling first and asking questions later,” said Paul de la Baume, senior market strategist at FlowBank SA. “Traders do not have the risk appetite to hold positions through the weekend, given the banking risk and what happened last week with Credit Suisse and regulators.”

Deutsche Bank slumped as much as 15%, the biggest decline since the early days of the pandemic in March 2020. It was the worst performer in an index of European bank stocks, which fell as much as 5.7%. Crosstown rival Commerzbank AG, Spain’s Banco de Sabadell SA and France’s Societe Generale SA also saw steep drops.

The widespread declines undermine hopes among authorities that the rescue of Credit Suisse Group AG last weekend would stabilize the broader sector. Central banks from the Federal Reserve to the Bank of England this week raised interest rates once again, keeping their focus on inflation amid hopes that the worst of the financial turmoil was past.

All week, regulators and company executives have sought to reassure traders about the health of the banking industry. Deutsche Bank management board member Fabrizio Campelli said Thursday that the government-brokered takeover of Credit Suisse by UBS is “no indication” of the state of European banks.

Standard Chartered Plc Chief Executive Bill Winters said Friday that while there are still some issues to be addressed, “it seems that the acute phase of the crisis is done.”

The latest moves in Europe follow losses in US banks, which tumbled Thursday even after Treasury Secretary Janet Yellen told lawmakers that regulators would be prepared for further steps to protect deposits if needed.

And apparently bank bailouts never died. They just got relabeled.

And on growing banking fears, the 10-year Treasury yield is down -11.7 basis points.

First, The Fed’s discount window soared to its highest level since … you guessed it … the previous financial crisis of 2008/2009.

Second, the 10-year Treasury yield declined -16 basis points this morning as investors flee to safety.

Bankrate’s 3-year mortgage rate rose to 7%, but with today’s decline in the 10-year Treasury yield we should see mortgage rates declining.

Yes, much of the blame belongs to The Fed’s leadership (Bernanke, Yellen, Powell) for leaving rates too low for too long, then suddenly try to lower inflation by raising rates. Now we have The Fed’s balance sheet INCREASING again as the use of The Fed’s discount window soars to highest level since Lehman Bros fiasco.

Cry for Argentina! Their central bank boosted its benchmark Leliq rate by 300 basis points to 78%. The monetary authority’s board considered the increase in response to accelerating inflation and after leaving the key rate unchanged for several months.

Of course, the US Federal Reserve is going in the opposite direction to combat the US banking crisis created by inflation and Yellen’s “Too low for too long” Fed policies.

I am beginning to wonder in Treasury Secretary Janet Yellen and Chicago Mayor Lori Lightfoot are the same person. Both complete Statist screw-ups.

President Biden had better give his State of the Union Address before the economy worsens any more.

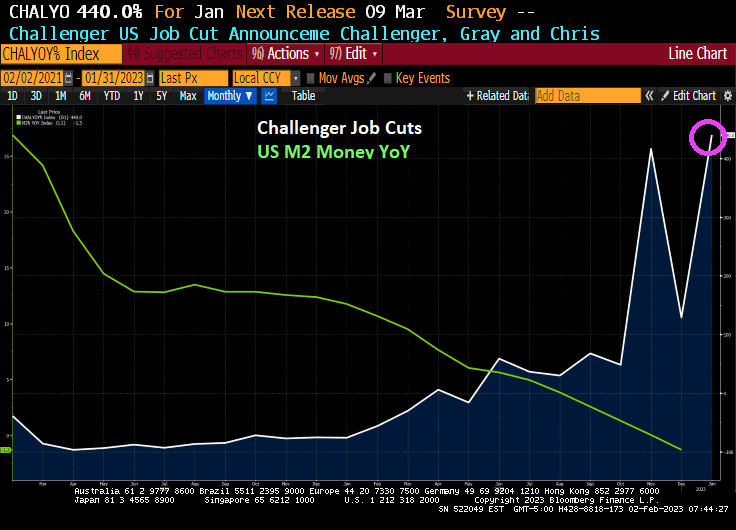

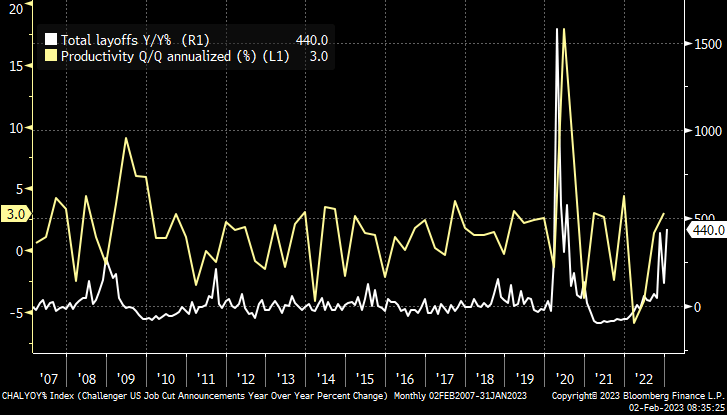

In January, the Challenger, Gray and Christmas jobs cuts index was a doozy. Jobs cuts rose 440%. This is happening as The Federal Reserve keeps its feet on the monetary brake pedal.

The Challenger report shows a big jump of 135.8 percent in layoff intentions to 102,943 in January, up from 43,651 in December and 440.0 percent higher than the 19,064 in January 2022. Many of the job cuts are in the tech sector, but job cuts are now spreading across the economy as a recession looms.

This morning, the US Treasury 10-year yield is down only -3.5 basis points, but it is Europe where the action is. UK is down -16.2 basis points and Italy is down -14.8 bps. UPDATE: US 10Y yield down -5.3 BPS, Italy 10Y down -29 bps.

You must be logged in to post a comment.