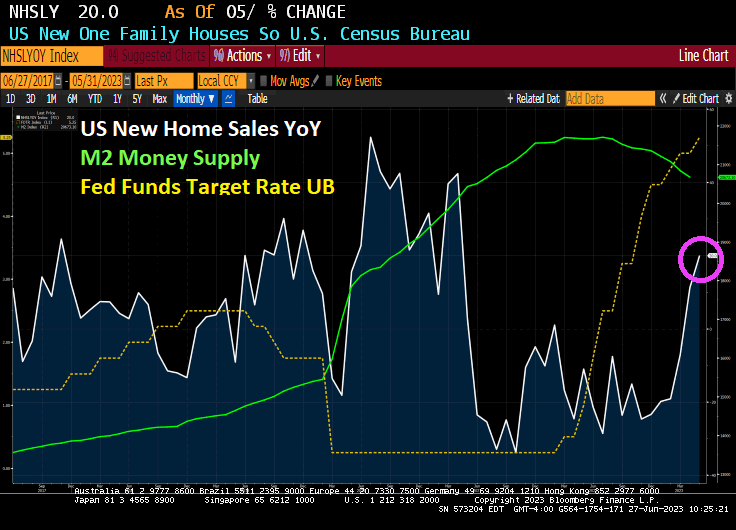

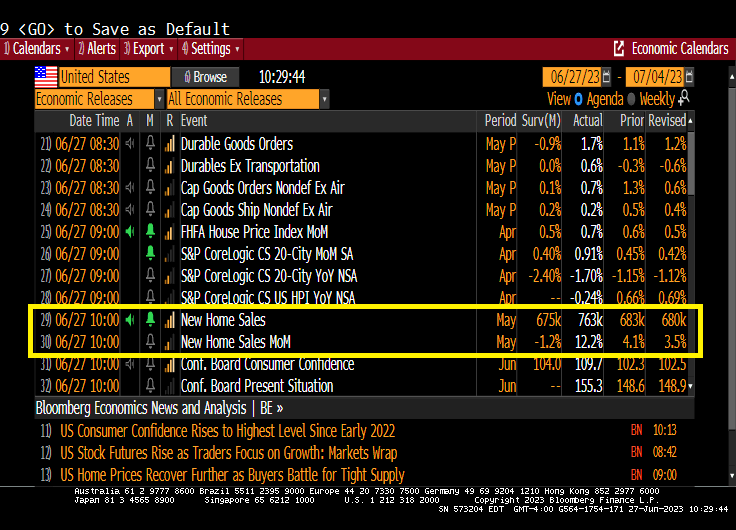

Well its about time that homebuilder started building again! And maybe it was The Fed rate hike pause (and possible rate cuts in the future.

US new home sales rose 20% in May as The Fed pauses rate hikes.

Fed Funds Futures point to one or two more rate hikes, then down she goes!!!

763k new homes were added in May

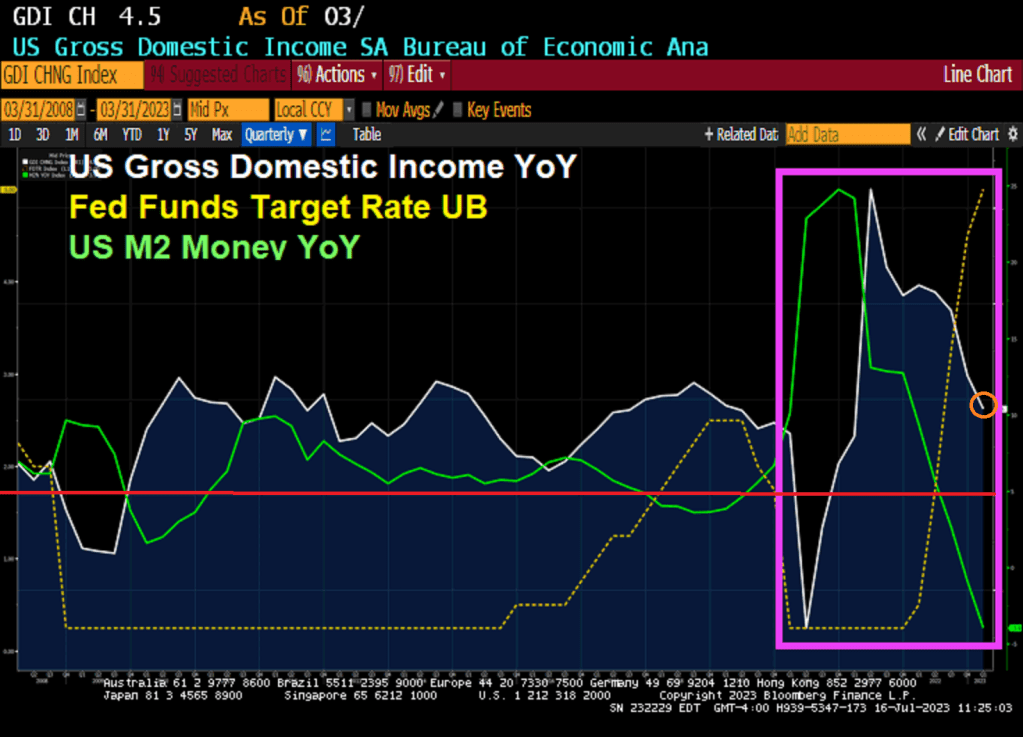

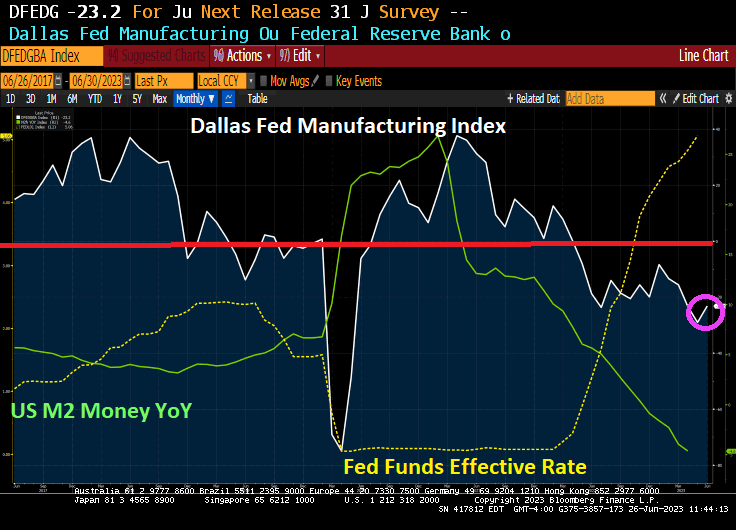

Remember, there is still a lot of stimulus (M2) sloshing around the economy. Perhaps we can rename all the infrastructure stimulus that is leaking out into the economy “Buttigieg Bucks.” Or “Buty Bucks!”

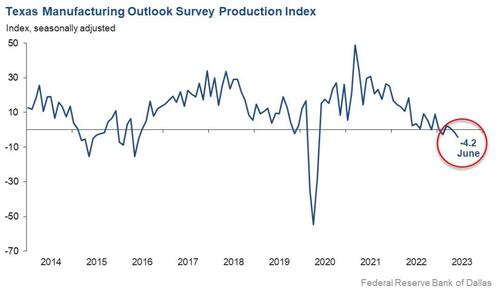

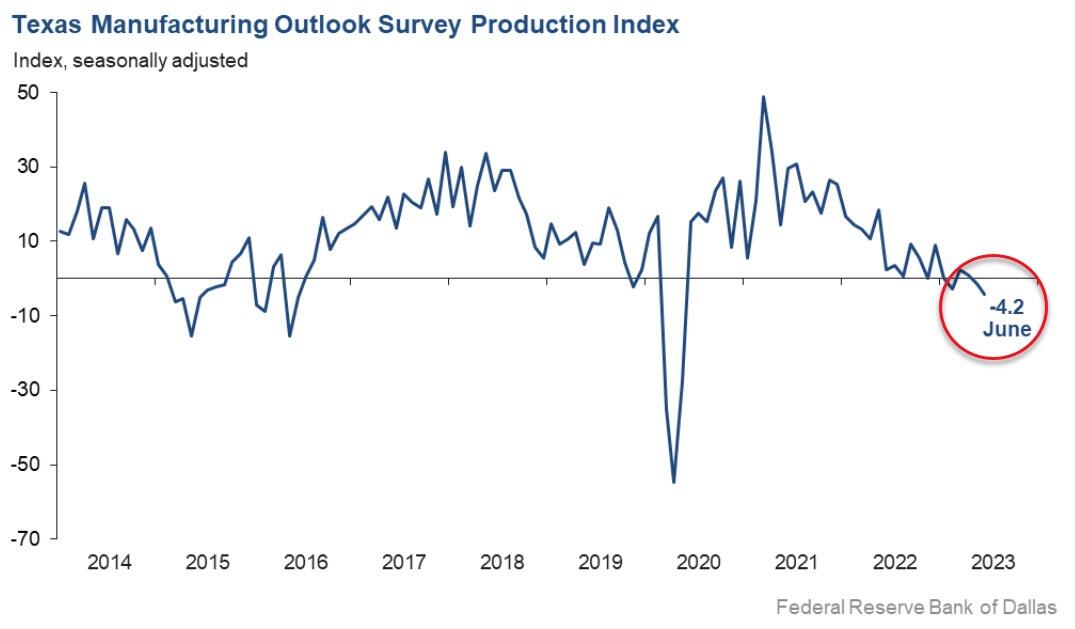

Texas factory activity declined in June, according to business executives responding to the Texas Manufacturing Outlook Survey. The production index, a key measure of state manufacturing conditions, fell three points to -4.2, a reading indicative of a slight contraction in output.

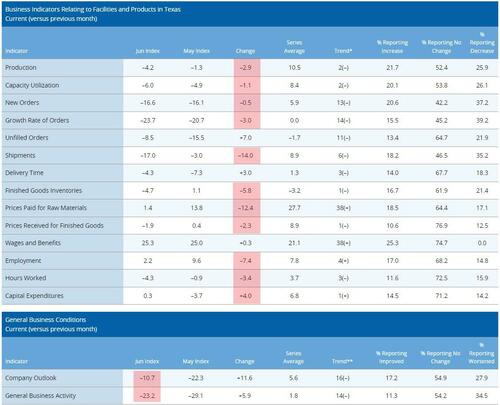

Labor market measures suggest weaker employment growth and declining work hours. Price pressures evaporated, while wage pressures remained elevated…

Yes, the Biden Administration may be the most incompetent administration in US history with Congress a close second. And did I mention CORRUPT??

The US is Living La Vida Biden (living the Biden life!) Which means you are making millions if you are a political elite, but suffering if you live on Main Street.

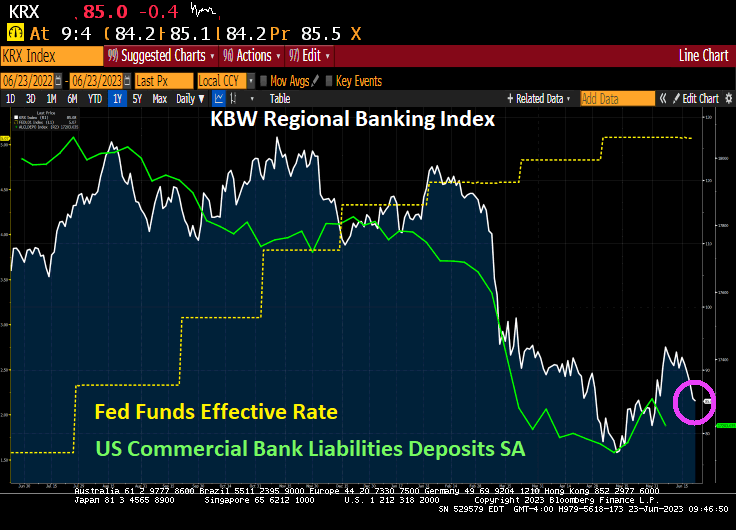

And regional banks (not the TBTF national banks) continue to suffer. The Bank Term Funding Program (1 of 2) is skyrocketing as The Fed cranks up rates to fight BidenFedflation (a combination of excessive monetary stimulus by The Fed and Biden’s lousy economic policies) and M2 Money growth crashes.

The regional banking index continues to fall as bank deposits shrink (like me when I used to jump in the Pacific Ocean in Santa Cruz).

Cryptos down this morning. But Bitcoin is above $30,000 … again.

Oil is down this morning but gold and silver are up slightly.

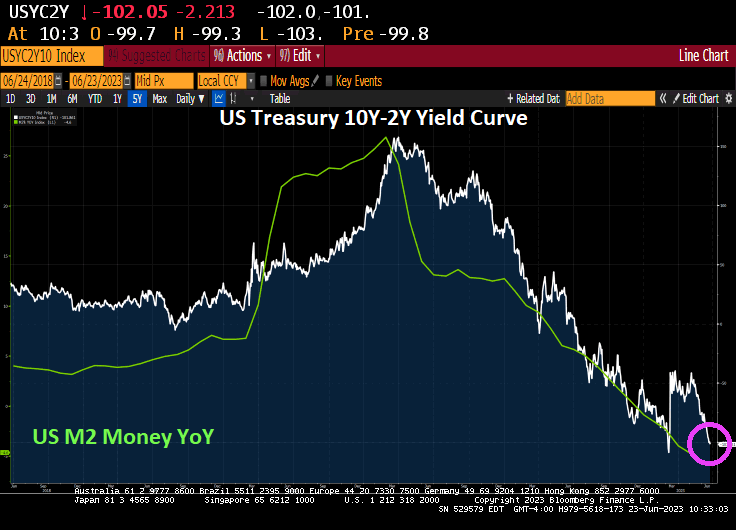

The 10Y-2Y US Treasury yield curve just dipped below -100 basis points (steep inversion) as M2 Money growth crashed and burned.

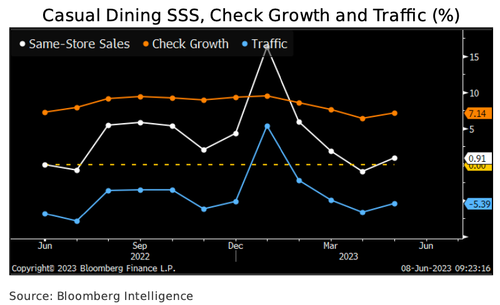

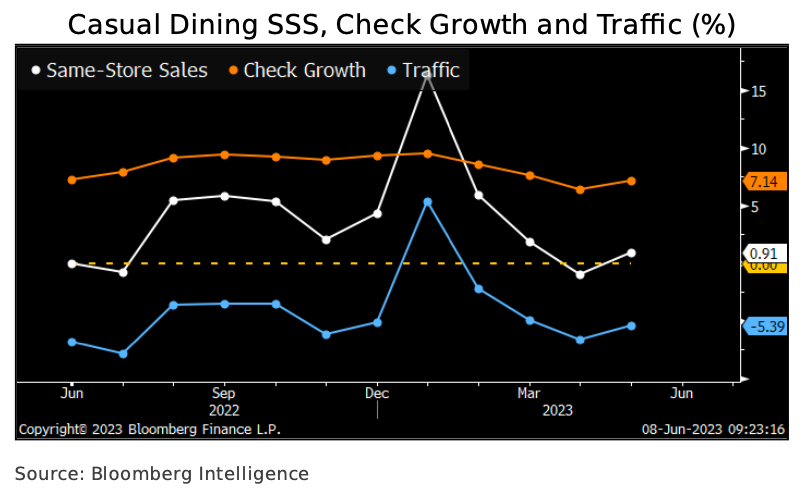

Bloomberg Intelligence’s Michael Halen penned a new note titled “2H Restaurant Sales: Inflation Killing Appetites.” It outlines, “Consumer spending finally buckles under more than two years of inflation and price hikes,” and the likely result is a trade-down of casual-dining chains like Brinker and Cheesecake Factory for quick-service chains like McDonald’s and Wendy’s.

The trade-down, which could start as early as this summer, is expected to dent consumer spending in restaurants such as Cheesecake Factory, Texas Roadhouse, and at brands operated by Brinker and Darden, Halen said.

Casual-dining industry same-store sales rose just 0.9% in May, according to Black Box Intelligence, as traffic dropped 5.4%. We expect cash-strapped low- and middle-income diners to cut restaurant visits and checks through year-end due to more than two years of real income declines and ballooning credit-card balances.

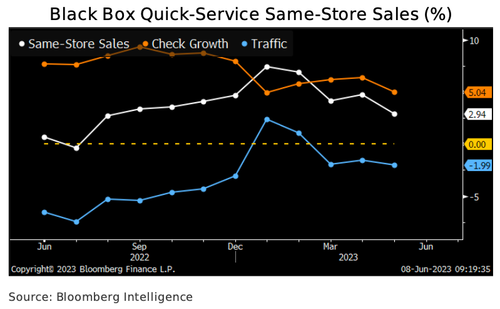

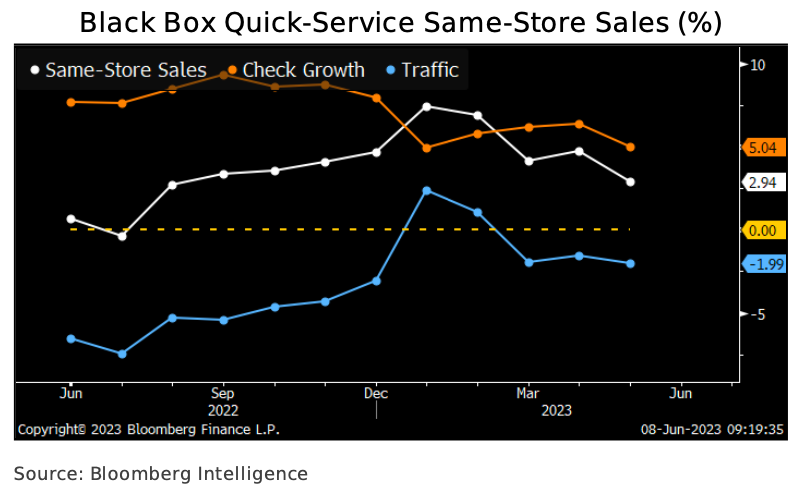

Halen provides more details about quick-service restaurants to fare better than causal-dining ones as “consumer spending finally buckles.”

Quick-service restaurants’ same-store sales could moderate with consumer spending in 2H but should fare better than their full-service competitors. Results rose 2.9% in May, according to Black Box data, as a 5% average-check increase was partly offset by a 2% guest-count decline. Check- driven comp-store sales gains are unsustainable, and we think inflation and menu price hikes will motivate low- and middle-income diners to reduce restaurant visits and manage their spending in 2H. On Domino’s 1Q earnings call, management said lower-income consumers shifted delivery occasions to cooking at home. Still, a trade-down from full-service dining due to cheaper price points may cushion the blow.

McDonald’s, Burger King, Wendy’s, and Jack in the Box are among the quick-service chains in Black Box’s index.

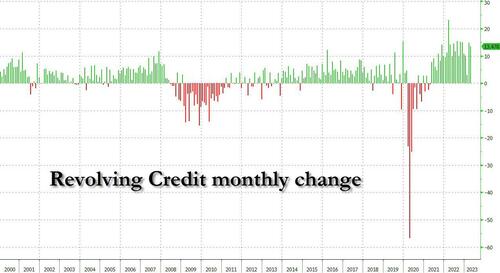

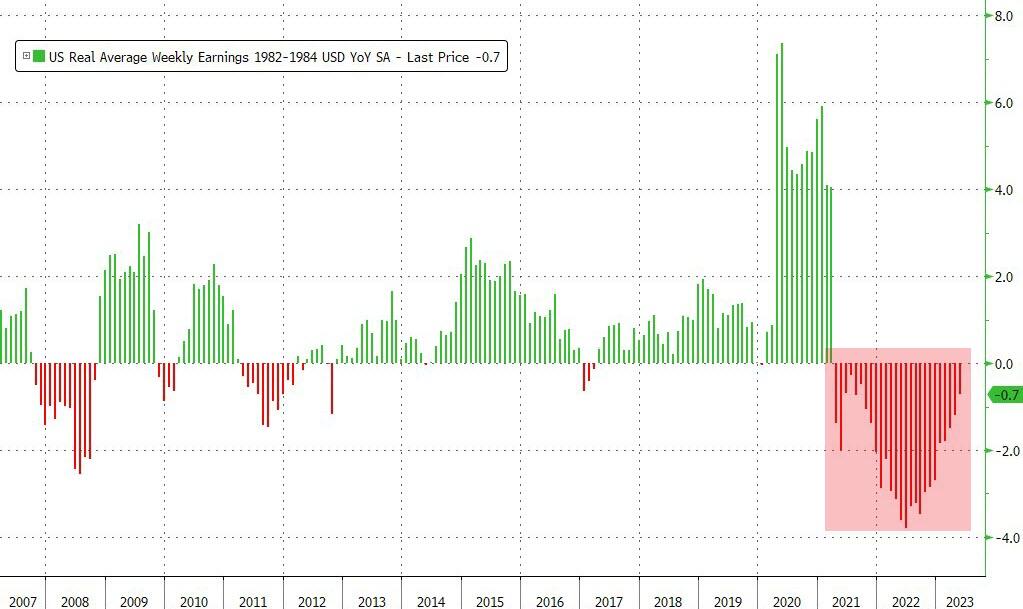

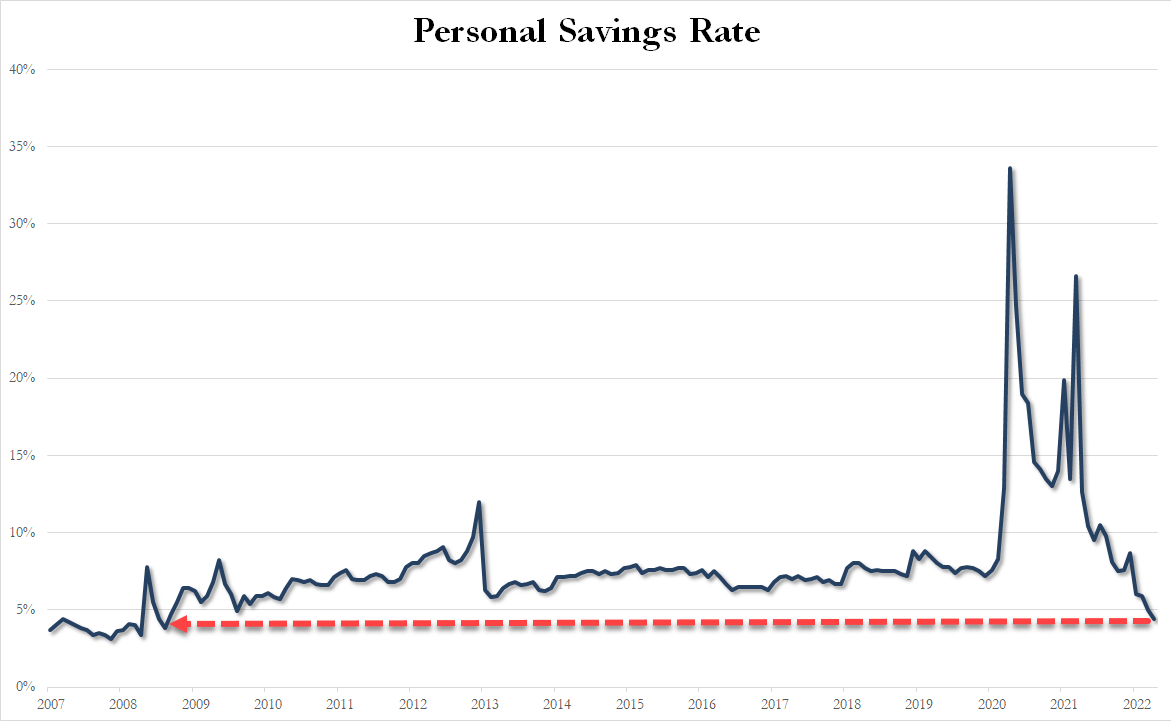

The latest inflation data shows consumers have endured the 26th straight month of negative real wage growth. What this means is that inflation is outpacing wage gains. And bad news for household finances, hence why many have resorted to record credit card usage.

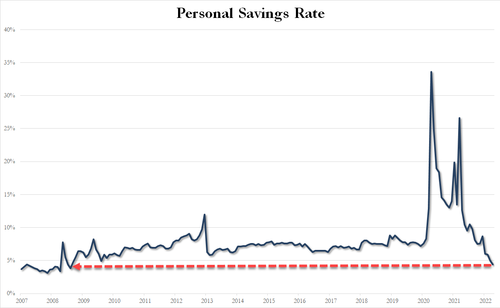

And the personal savings rate has collapsed to just 4.4%, its lowest level since Sept. 2008 (the dark days of Lehman). And why is this? To afford shelter, gas, and food, consumers are drawing from emergency funds due to the worst inflation storm in a generation.

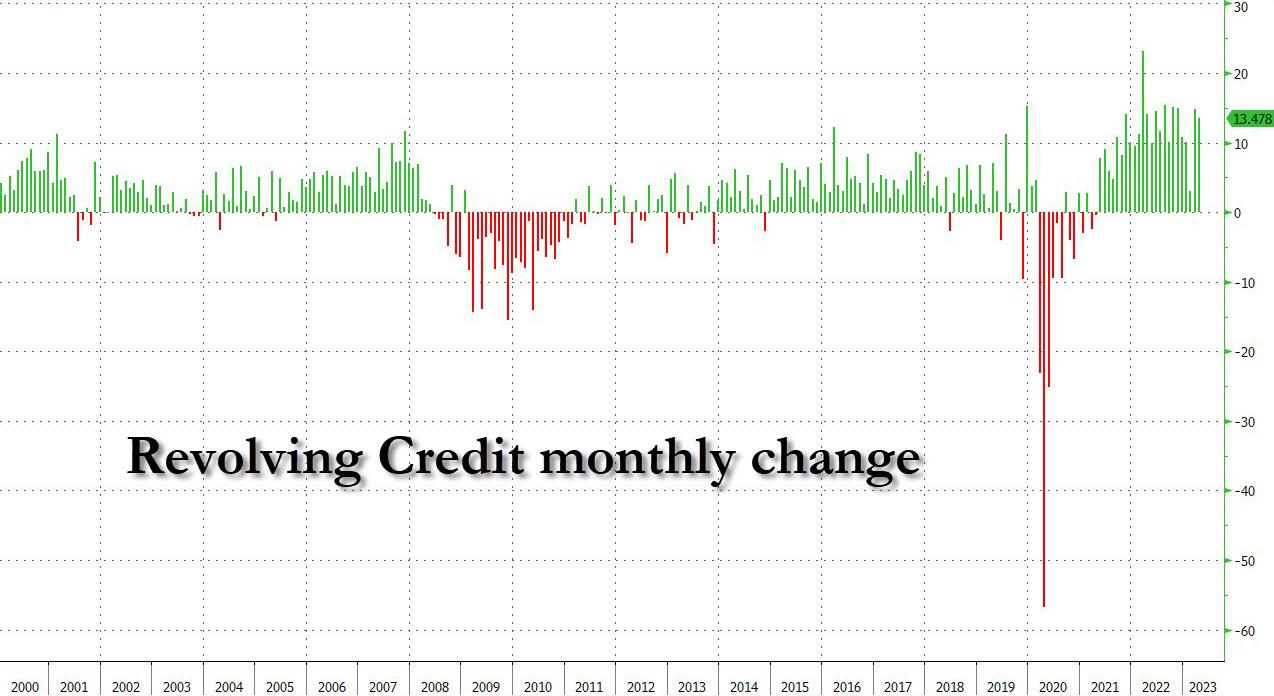

As revolving consumer credit has exploded higher and the last two months have seen a near-record increase…

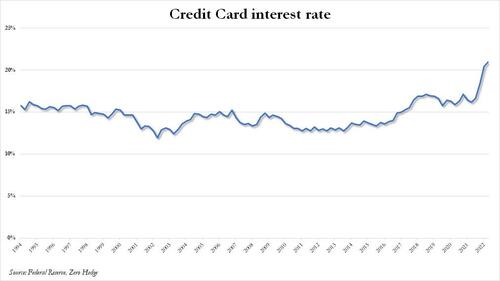

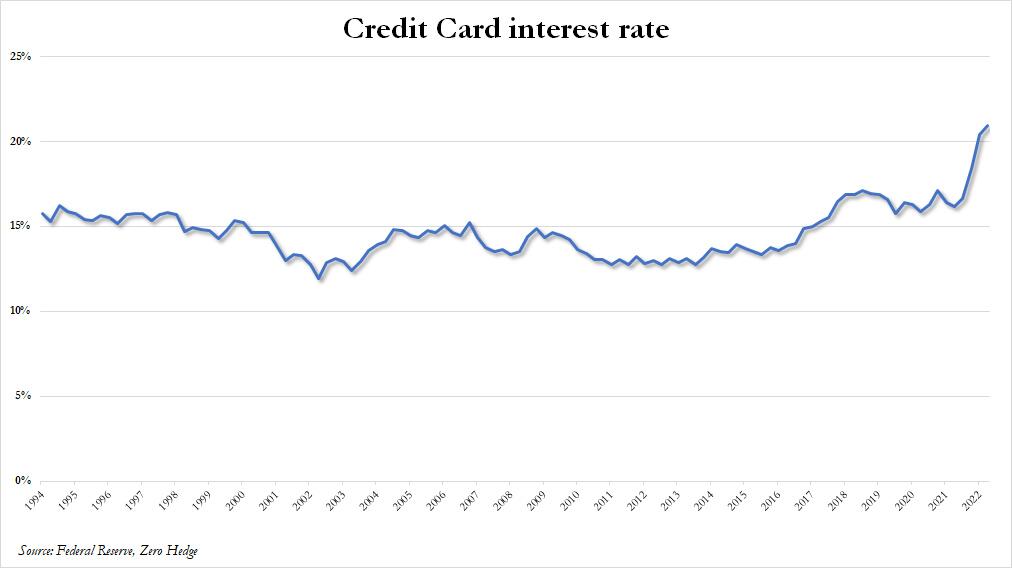

… even as the interest rate on credit cards has jumped to the highest on record.

With record credit card debt load and highest interest payments in years, plus depleted savings, oh yeah, and we forgot, the restart of student loan payments later this year, this all may signal a consumer spending slowdown at causal diners while many trade down for McDonald’s value menu. Even then, we’ve reported consumers have shown that menu items at the fast-food chain have become too expensive.

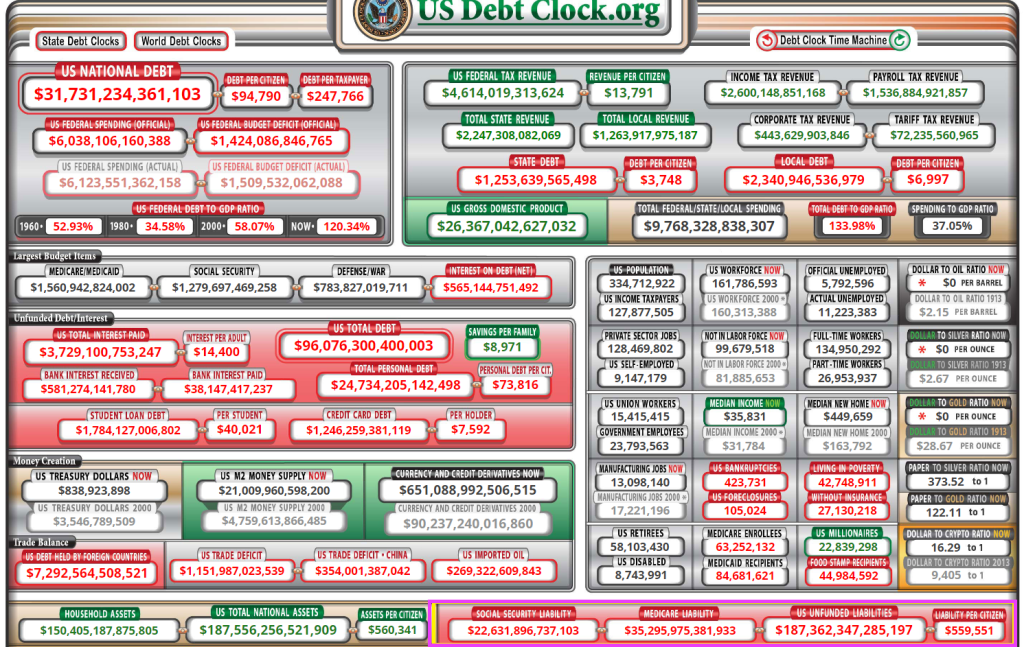

The Federal government in Washington DC is broken beyond repair. Politicians get elected by promising free or cheap things, so they keep delivering the bacon. Or pork to political donors. The top 1% get massive payoffs (like green energy subsidies or bank bailouts), the bottom 99% get out of control entitlements like Social Security, Medicare and Medicaid. And other unsustainable entitlements. In fact, student loans are now an entitlement since some voters will vote for the corrupt politician (no, Joe Biden isn’t the only corrupt politician in Washington DC) who will forgive their student loans.

In fact, we now have $187 TRILLION in UNFUNDED liabilities that were promised to the 99%. The 1% will always get their political contributions paid. Biden and Schumer have promised their donor class trillions in spending, so that are threatening to let the US debt default to protect the 1%.

And unfunded entitlements are expected to soar, particularly Medicare.

Mandatory spending is expected to soar while discretionary spending is almost flat in terms of growth.

Meanwile, the US credit default swap remains elevated as the US Treasury short curve (2Y-3M) is near the most inverted in history.

And this headline, “Biden Not Ready Yet to Invoke 14th Amendment to Avoid US Default”. That means Biden would adopt extraordinary powers to prevent a debt default. Hence, the idiocy like the trillion dollar coin.

Nobel Laureate and Statist useful idiot Paul Krugman wants to keep spending trillions. As a result, he argues “Don’t worry about the declining US dollar hegemony … as long as the US doesn’t default.” Translation: Krugman agrees with Dementia Joe that Republicans should just pass Biden’s budget with no strings attached. C’mon Krugman. The growth of BRICs (Brazil, Russia, India, South Africa and growing) is partly due to 1) perceived weakness of Senile Grandpa Joe and 2) the fiscal spending and debt growth in Washington DC. Of course it matters, but Krugman wants to keep spending on green lunacy and entitlements until we break the back of the country. Sounds like Krugman is on board with Cloward-Piven.

They can’t cut promised entitlements. Look at France where Macron raised the retirement age by 2 years and there are endless riots. So debt default is the only option, though painful.

Will Congress and future administrations stop prominsing endless spending that benefits the 1%? Not likely. Our political system is hopelessly broken.

I am sure that China’s Communist Party has sent Dementia Joe a message “We own you! You better not default on what you owe us!!” Or default so we can own you financially.

Three of the four horsemen of the financial apocalypse. Yellen is the fourth horseman, but is too short to appear in the picture.

My friend Phill Hall asked me about the state of the US housing market yesterday. My answer? “Chaos.” Why chaos? Here is why: 23 consecutive months of NEGATIVE real wage growth, declining availability of homes for sale, still expensive home prices following the Covid spending surge, and rising mortgage rates as The Fed fights inflation.

And now we have mortgage demand shrinking 4.1% from the previous week according to the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 31, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 4.1 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 4 percent compared with the previous week. The Refinance Index decreased 5 percent from the previous week and was 59 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 4 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 35 percent lower than the same week one year ago.

Throw in the declining inventory of homes for sales, and we have chaos.

Not to mention 23 consecutive months of negative REAL wage growth.

Well, at least REAL home prices are growing more slowly (-3.86% YoY) than REAL weekly wage growth -1.9% YoY). So much for housing as a hedge against inflation!

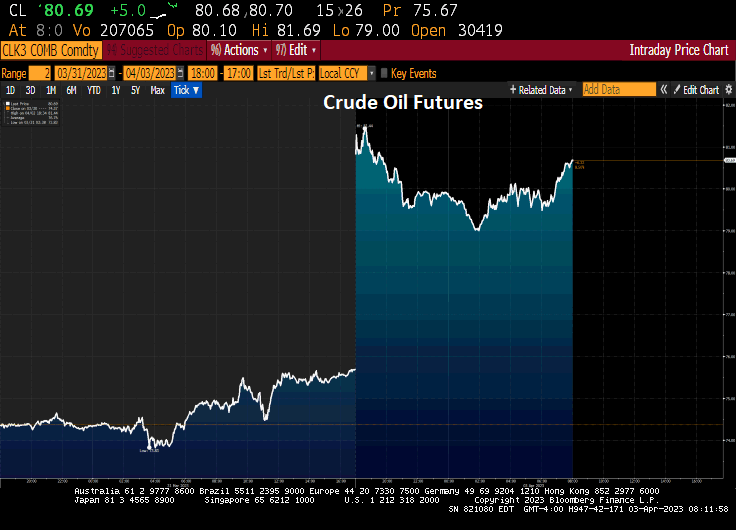

While Resident Biden is on good terms with the Mexican drug and sex trafficing cartels that control our southern border, the oil cartel just stuck their fingers in Biden’s eyes by cutting oil productions. Riyadh, Saudi Arabia was irritated last week that the Biden administration publicly ruled out new crude purchases to replenish SPR

Cartel removes more than 1 million barrels a day from market

Analysts say the decline in oil inventories will accelerate

Today, crude oil futures are up 6.62% to over $80 per barrel.

Sunday’s surprise OPEC+ production cuts have redefined the outlook for crude prices, bringing $100 a barrel back into the frame.

Prior to the announcement, the cartel’s own numbers suggested the group would need to pump more oil, not less, in the second half. With the International Energy Agency expecting a demand surge later this year, there’s now renewed risk of a fresh inflationary impetus for the global economy.

Under Biden’s Reign of Error, diesel prices are up 64% while the Strategic Petroleum Reserves (SPR) have been drained by -42%.

St. Benedict, help protect us from Biden and The Federal Reserve.

For all the focus on whether the Federal Reserve is about to pause its interest-rate hikes, there’s another critical policy decision sure to draw plenty of attention come Wednesday: What the central bank does with its massive pile of bond holdings.

The banking-sector turmoil that has only appeared to deepen, combined with a previous increase in funding pressures, has left financial markets keenly attuned to what the Fed will say about its $8.6 trillion balance sheet.

Until this month the stash had been shrinking as part of the Fed’s efforts to return it back to pre-pandemic levels. But now it has started to expand again as the Fed acts to bolster the banking system through a slate of emergency lending programs. Its latest step came Sunday, when it moved with other central banks to boost US dollar liquidity.

Some say financial-stability concern may spur policymakers to dial back the runoff of its bond portfolio, a process known as quantitative tightening that’s designed to drain reserves from the system. Still, others argue that even if the Fed does pause its rate increases, the central bank’s overarching goal of taming inflation means it’s unlikely it will signal any shift this week in efforts to shrink the holdings of Treasuries and mortgage-backed debt. The one exception, they note, would be if stress in the banking sector were to become much more severe.

The Fed’s move to backstop US banks “clearly expands the Fed’s balance sheet,” said Subadra Rajappa, head of US rates strategy at Societe Generale SA. If usage of the Fed’s liquidity facilities is “small and contained they probably continue QT, but if the take-up is large then they probably stop as it then starts to raise concerns over reserve scarcity.”

The fate of the Fed’s portfolio is a subject of debate after the collapse of several US lenders led the central bank to create a new emergency backstop, known as the Bank Term Funding Program, which it announced March 12. Banks borrowed $153 billion from the Fed’s discount window — lenders’ traditional liquidity backstop — in the week ended March 15, Fed data show, a record that eclipsed the previous all-time high set during the 2008 financial crisis. They also tapped the new program for $11.9 billion.

The central bank’s various liquidity programs added about $300 billion to the Fed’s balance sheet last week, reversing about half of the reduction the Fed has achieved since the runoff began last June. But some economists say the two programs can work in tandem, with the banking efforts targeting financial stability and QT remaining a steady part of the Fed’s plan to remove the support it provided during the pandemic.

It looks like a 25 basis point increase at the next meeting, then cuts in The Fed Funds Target Rate to 3.820% by January 2024.

The labor market is still tight. So tight, we get this!!

Its Gov’t Gone Wild! Insane spending budget by “Sloppy Joe” Biden, Yellen asking Warren Buffet for banking advice (seriously??), a war in Ukraine that America doesn’t seem to actually want to win, etc. But its the banking system where banks are getting crushed by rising inflation and interest rates (but failed to hedge). Sigh.

As I always told my investments and fixe-income students at University of Chicago, Ohio State University and George Mason University, a 10 basis point change in the 2-year and 10-year US Treasury yield is a big deal. This morning, the US Treasury 2-year yield fell -32 basis points while the 10-year Treasury yield fell -14.8 basis points.

At the same time, gold 3.8% and silver rose 4.7% on banking fears.

Debt would hit a new record by 2027, rising from 98 percent of GDP at the end of 2023 to 106 percent by 2027 and 110 percent by 2033. Nominal debt would grow by $19 trillion, from $24.6 trillion today to $43.6 trillion by 2033.

Deficits would total $17.1 trillion (5.2 percent of GDP) between FY 2024 and 2033, rising to $2.0 trillion, or 5.1 percent of GDP, by 2033.

Spending and revenue would average 24.8 and 19.7 percent of GDP, respectively, over the next decade, with spending reaching 25.2 percent of GDP and revenue totaling 20.1 percent by 2033. The 50-year historical average is 21.0 percent of GDP for spending and 17.4 percent of GDP for revenue.

Proposals in the budget would reduce projected deficits by $3 trillion through 2033, including $400 billion through 2025 when it could help fight inflation. The budget proposes $2.8 trillion of new spending and tax breaks, $5.5 trillion of revenue and savings, and saves $330 billion from interest.

The budget relies on somewhat optimistic economic assumptions, including stronger long-term growth, lower unemployment, and lower long-term interest rates than the Congressional Budget Office (CBO). The budget assumes 0.4 percent growth this year, 2.1 percent growth next year, and 2.2 percent by the end of the decade – compared to CBO’s 0.1 percent, 2.5 percent, and 1.7 percent, respectively. The budget also assumes ten-year interest rates fall to 3.5 percent by 2033, compared to CBO’s 3.8 percent.

And then we have Sloppy Joe and Statist Janet Yellen meeting with mega donor Warren Buffet for advice on dealing with the banking crisis … made by Biden’s energy policy and insane Covid spending by the Administration. And, of course, The Fed’s “too low for too long” monetary policy. What is 92-year old Warren Buffet going to say?

Meanwhile, Fed Funds Futures are pointing to one more rate hike then a series of rate cuts down to 3.737 by January 2024.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.